3d Semiconductor Packaging Market Report

Published Date: 31 January 2026 | Report Code: 3d-semiconductor-packaging

3d Semiconductor Packaging Market Size, Share, Industry Trends and Forecast to 2033

This report provides an in-depth analysis of the 3D Semiconductor Packaging market, covering market size, trends, and insights for the forecast period from 2023 to 2033. We examine key technologies, segments, regional dynamics, and leading companies driving the growth in this market.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

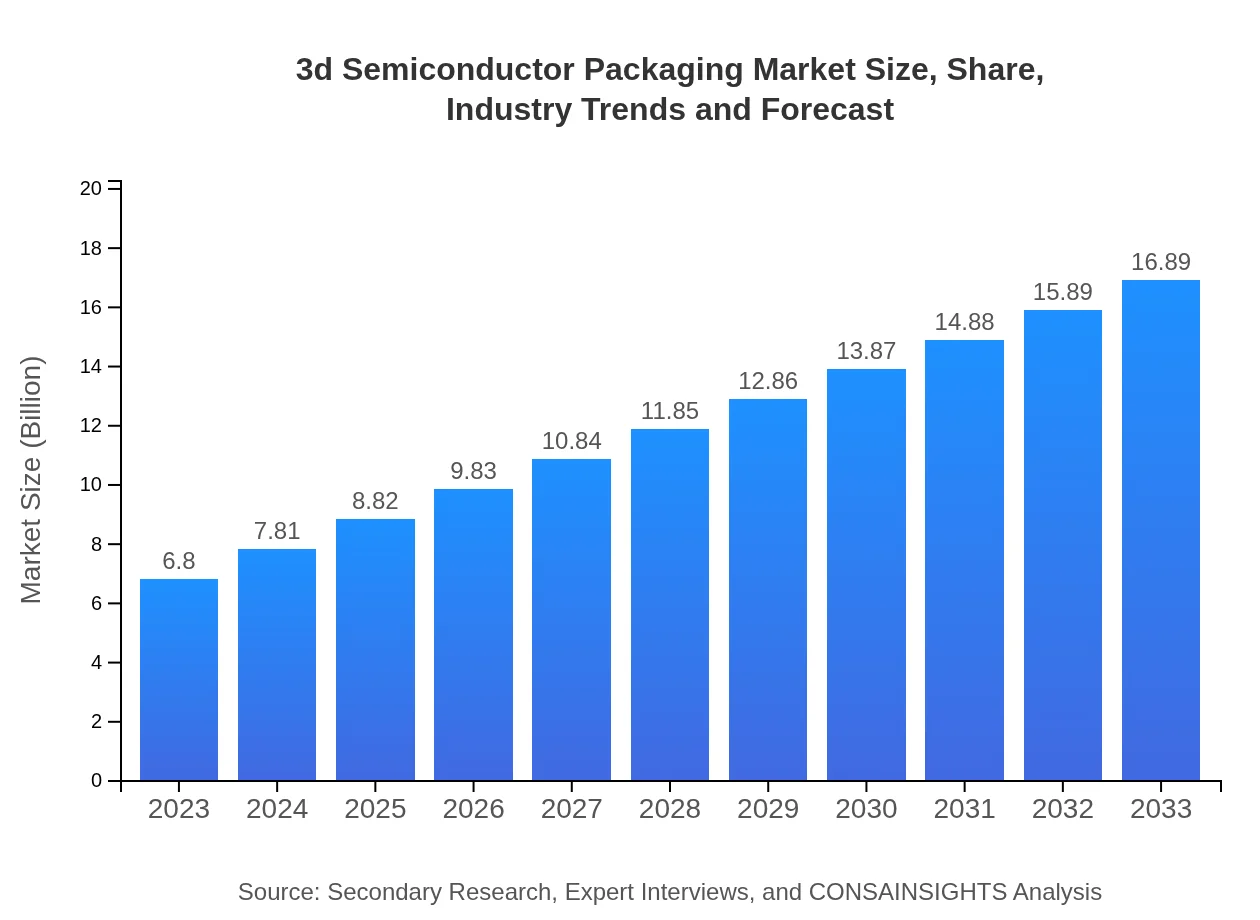

| 2023 Market Size | $6.80 Billion |

| CAGR (2023-2033) | 9.2% |

| 2033 Market Size | $16.89 Billion |

| Top Companies | Intel Corporation, Texas Instruments, ASE Technology Holding Co., STMicroelectronics |

| Last Modified Date | 31 January 2026 |

3d Semiconductor Packaging Market Overview

Customize 3d Semiconductor Packaging Market Report market research report

- ✔ Get in-depth analysis of 3d Semiconductor Packaging market size, growth, and forecasts.

- ✔ Understand 3d Semiconductor Packaging's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in 3d Semiconductor Packaging

What is the Market Size & CAGR of 3D Semiconductor Packaging market in 2023?

3d Semiconductor Packaging Industry Analysis

3d Semiconductor Packaging Market Segmentation and Scope

Tell us your focus area and get a customized research report.

3d Semiconductor Packaging Market Analysis Report by Region

Europe 3d Semiconductor Packaging Market Report:

Europe's market is projected to showcase a rise from USD 2.18 billion in 2023 to USD 5.42 billion by 2033, supported by stringent regulations demanding enhanced technology in electronic devices, particularly in automotive and industrial applications.Asia Pacific 3d Semiconductor Packaging Market Report:

The Asia Pacific region commanded a significant market share, valued at USD 1.11 billion in 2023, and is projected to reach USD 2.75 billion by 2033. Countries like China, Japan, and South Korea are major players due to their advanced technology hubs and manufacturing capabilities in semiconductor production.North America 3d Semiconductor Packaging Market Report:

North America is anticipated to grow from USD 2.56 billion in 2023 to USD 6.35 billion by 2033. The region's growth is attributed to the presence of leading semiconductor companies and a strong push towards automotive and healthcare innovations.South America 3d Semiconductor Packaging Market Report:

In South America, the market value for 3D Semiconductor Packaging is estimated at USD 0.61 billion in 2023 and is expected to reach USD 1.51 billion by 2033. The growth is driven by increasing investments in electronics manufacturing and rising demand for consumer gadgets.Middle East & Africa 3d Semiconductor Packaging Market Report:

In the Middle East and Africa, the 3D Semiconductor Packaging market is expected to grow from USD 0.35 billion in 2023 to USD 0.87 billion by 2033, driven by increased investments in telecom infrastructure and consumer electronics expansion.Tell us your focus area and get a customized research report.

3d Semiconductor Packaging Market Analysis By Technology

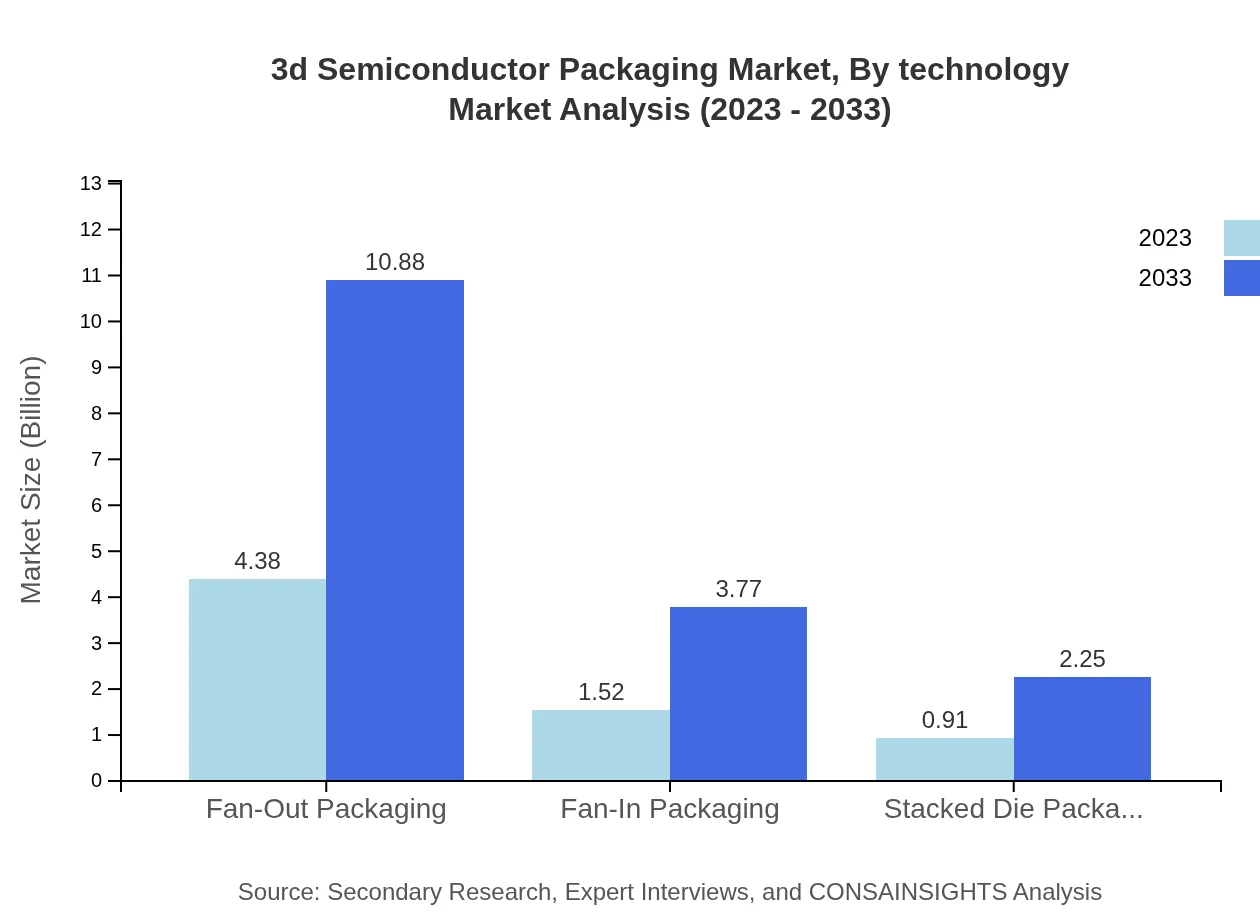

Substrates dominate the market, with a size of USD 3.78 billion in 2023, anticipated to grow to USD 9.39 billion by 2033, holding a consistent share of 55.59%. Fan-Out Packaging is also significant, valued at USD 4.38 billion in 2023, with projections of reaching USD 10.88 billion by 2033, maintaining a share of 64.37%. Other categories like Epoxy and Silicon also signify growing traction in technological innovation within the industry.

3d Semiconductor Packaging Market Analysis By Application

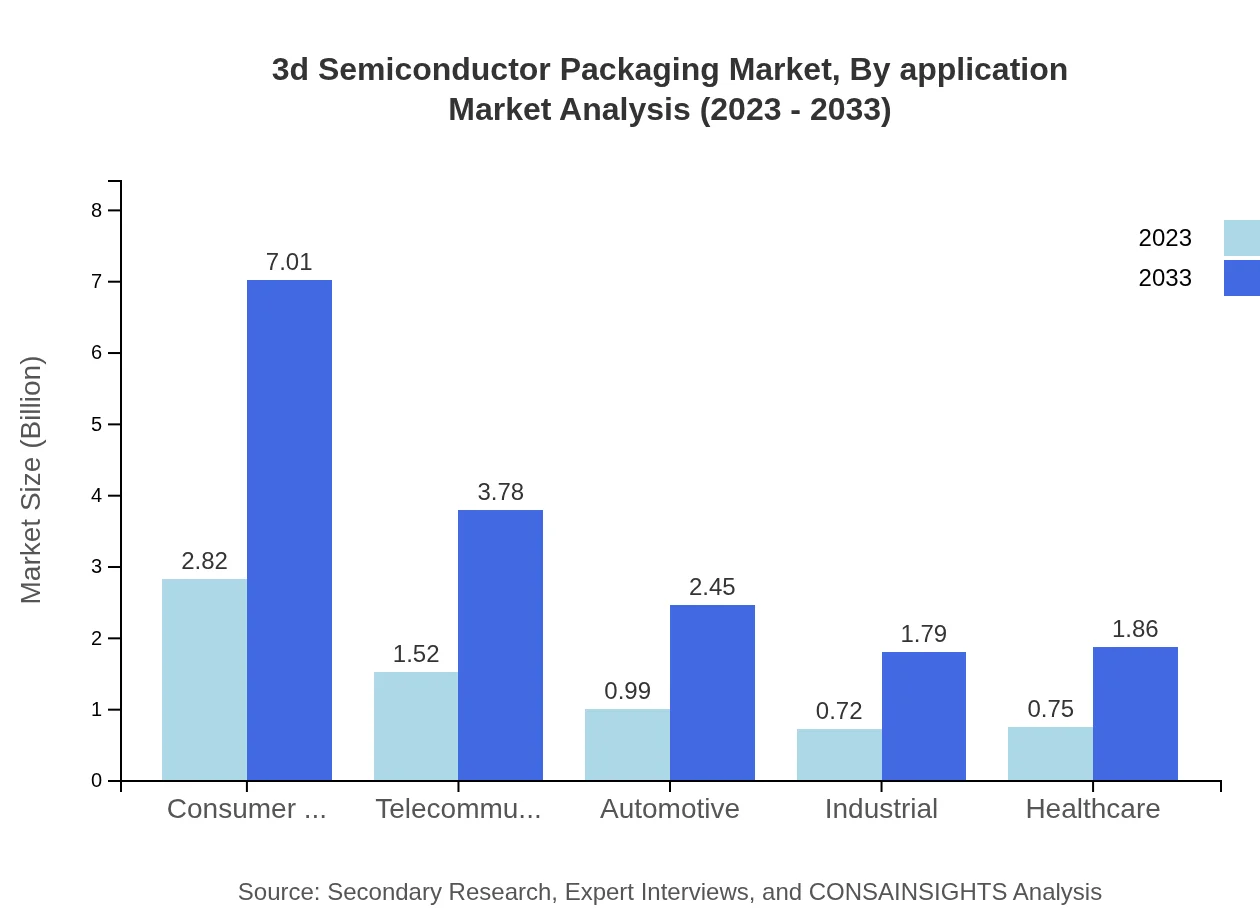

Consumer Electronics holds a substantial portion of the market, with a size of USD 2.82 billion in 2023 and expected to grow to USD 7.01 billion by 2033, reflecting a stable share of 41.51%. Telecommunications and automotive applications also show promise, indicating overall healthy expansion in various sectors due to increasing demand for smarter and integrated technologies.

3d Semiconductor Packaging Market Analysis By Material

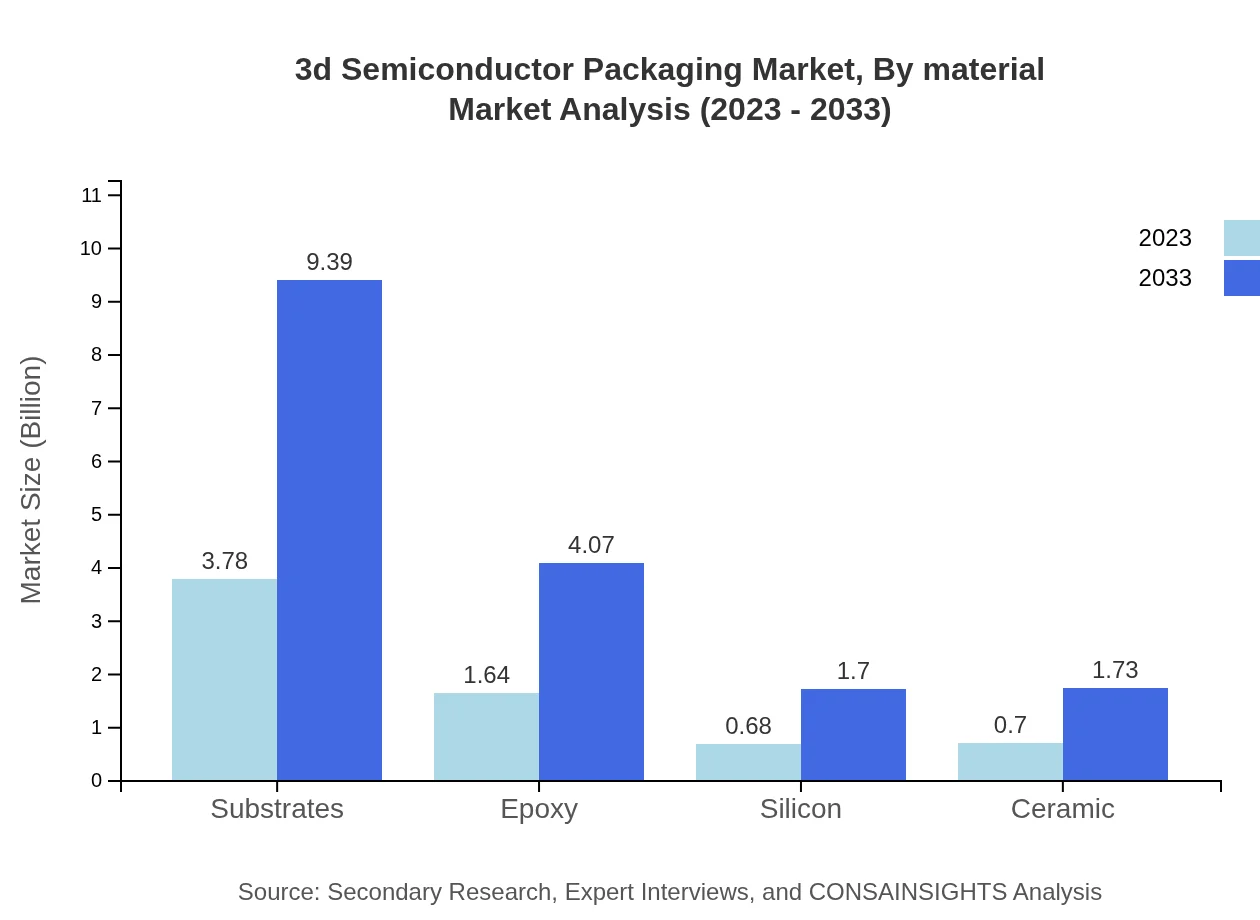

The market by material is led by Fan-Out Packaging and Wafer-Level Packaging, showcasing notable market sizes. Epoxy encapsulation is also crucial with a size projected to grow from USD 1.64 billion in 2023 to USD 4.07 billion by 2033, maintaining a 24.11% share, evidencing its importance in reliability and durability of products.

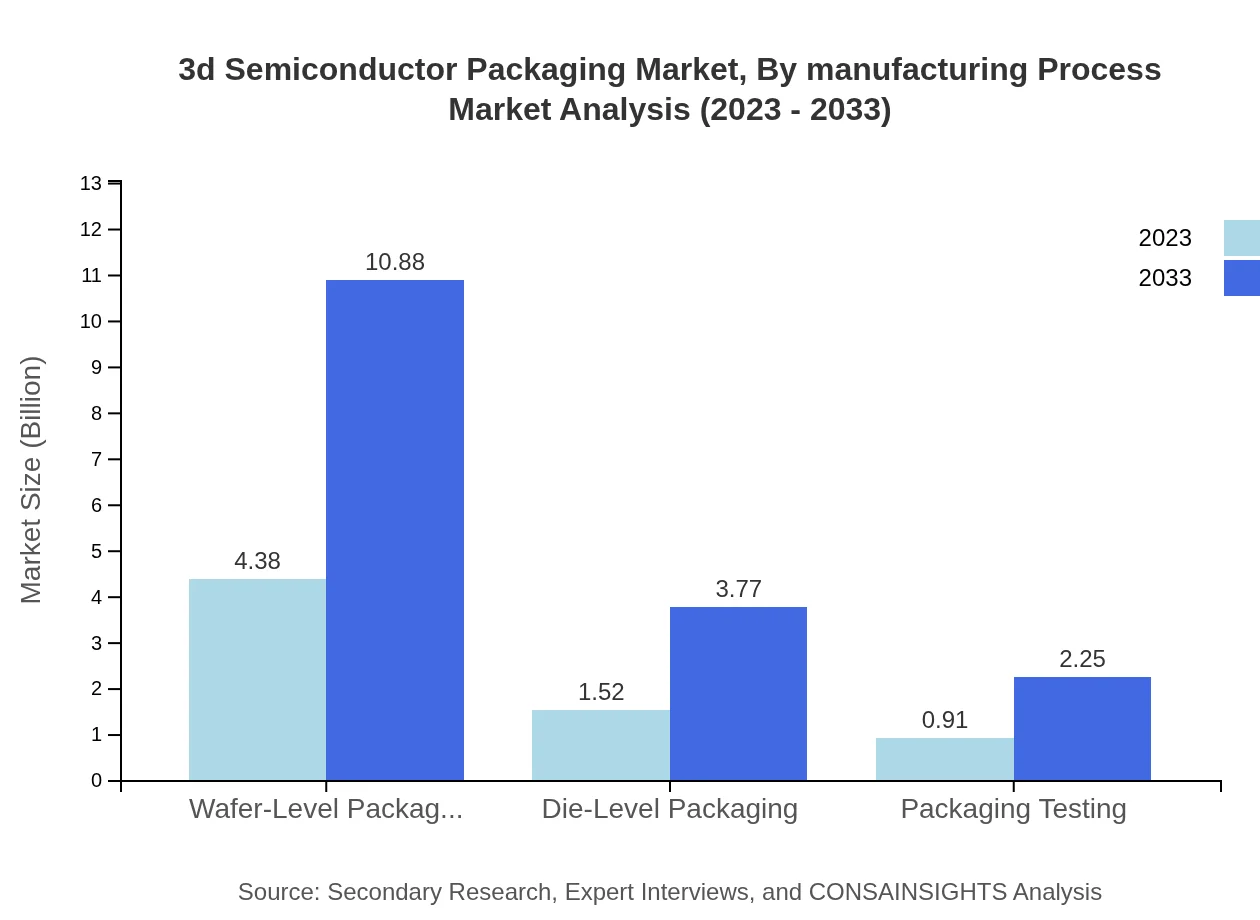

3d Semiconductor Packaging Market Analysis By Manufacturing Process

Manufacturing processes like Die-Level Packaging and Packaging Testing together provide insights on the production efficiencies and innovations shaping the market. Die-Level Packaging shows significant growth potential as it is projected to grow from USD 1.52 billion in 2023 to USD 3.77 billion by 2033, alongside notable strategies enhancing operational capacities.

3D Semiconductor Packaging Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in 3d Semiconductor Packaging Industry

Intel Corporation:

A leading player in semiconductor manufacturing, Intel focuses on advanced packaging technologies to enhance performance and efficiency in electronic devices.Texas Instruments:

Renowned for its expertise in designing and manufacturing semiconductors, TI actively invests in 3D packaging innovations to support high-performance electronics.ASE Technology Holding Co.:

One of the largest providers of independent semiconductor packaging and testing services, ASE is pivotal in advancing 3D packaging technologies.STMicroelectronics:

A significant player in the semiconductor market, STMicroelectronics emphasizes energy-efficient 3D packaging solutions to cater to automotive and industrial applications.We're grateful to work with incredible clients.

FAQs

What is the market size of 3D semiconductor packaging?

The 3D semiconductor packaging market is projected to reach a size of $6.8 billion by 2033, growing at a CAGR of 9.2% from its current value in 2023. This growth reflects the increasing demand for advanced packaging solutions.

What are the key market players or companies in the 3D semiconductor packaging industry?

Key players in the 3D semiconductor packaging industry include major companies like Intel, TSMC, Amkor Technology, ASE Group, and SPIL. These companies are leading innovations and advancements in semiconductor packaging technologies.

What are the primary factors driving the growth in the 3D semiconductor packaging industry?

The growth in this industry is driven by the rising demand for miniaturized electronic devices, the need for enhanced performance and efficiency in semiconductors, and increased adoption of IoT devices. Additionally, technological advancements in packaging techniques contribute significantly.

Which region is the fastest Growing in the 3D semiconductor packaging?

The fastest-growing region in the 3D semiconductor packaging market is North America, which is expected to grow from $2.56 billion in 2023 to $6.35 billion by 2033. Other notable regions include Europe and Asia-Pacific, showcasing substantial growth.

Does ConsaInsights provide customized market report data for the 3D semiconductor packaging industry?

Yes, ConsaInsights offers tailored market report data for the 3D semiconductor packaging industry. Clients can receive customized reports based on specific needs, including focused analysis on particular segments and regions.

What deliverables can I expect from this 3D semiconductor packaging market research project?

Upon completion of the 3D semiconductor packaging market research project, clients can expect comprehensive reports that include market size, growth forecasts, competitive analysis, segmentation data, and regional insights tailored for strategic decision-making.

What are the market trends of 3D semiconductor packaging?

Current market trends in 3D semiconductor packaging show a shift towards fan-out and wafer-level packaging technologies. The integration of AI and machine learning in packaging processes and increasing investments in R&D for advanced materials are also prominent trends.