Ablation Technologies Market Report

First published: 07 October 2024 | Last updated: 25 May 2026 | Report Code: ablation-technologies

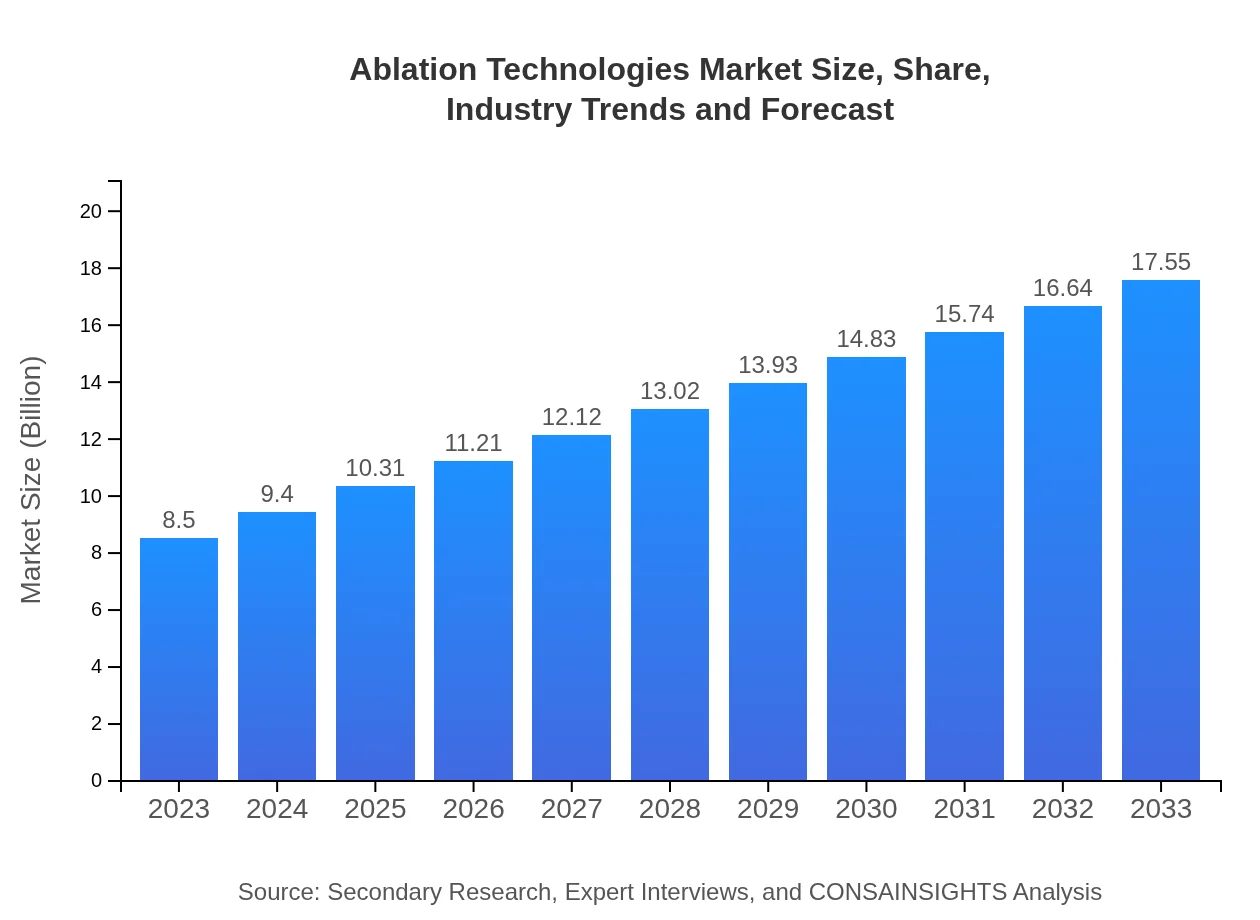

Ablation Technologies Market — USD 8.5 billion in 2023, Growing to USD 17.55B by 2033 at 7.3% CAGR

This comprehensive market report covers the dynamics of the Ablation Technologies industry from 2023 to 2033, providing insights into market sizing, growth trends, regional analysis, and competitive landscape.

Key Takeaways

- Market value rising from $8.50 Billion in 2023 to $17.55 Billion in 2033 at a 7.3% CAGR.

- Europe is largest regional market, while no single fastest-growing region is stated because regional CAGR differences remain within 0.15 percentage points.

- Europe holds the largest regional share, increasing from $3 Billion in 2023 to $6.19 Billion in 2033.

- North America advances from $2.86 Billion to $5.9 Billion between 2023 and 2033.

- Thermal and non-thermal technologies, and devices plus consumables, represent core product groupings driving adoption.

- Hospitals, ambulatory surgical centers, and clinics are principal end-user channels for ablation solutions.

Ablation Technologies Market Report — Executive Summary

Europe remains largest market by forecast-period value, while no single fastest-growing region is stated because top regional growth rates are separated by less than 0.15 percentage points. The market for ablation technologies is expanding steadily, supported by rising procedural volumes, adoption of minimally invasive techniques, and continuous device innovation. Key drivers include greater demand in oncology and cardiology applications, and enhancements in thermal and non-thermal ablation systems. Product segmentation centers on devices, consumables, and software, while end users comprise hospitals, ambulatory surgical centers, and clinics. Europe is identified as the largest regional market. Leading firms such as Medtronic, Boston Scientific, Abbott Laboratories, AngioDynamics, and Hologic, Inc. are active in advancing technology and supporting clinical adoption. The report synthesizes primary interviews, company publications, and internal validation to provide a verified market outlook and strategic insights for stakeholders.

Key Growth Drivers

- Rising preference for minimally invasive procedures increases demand for ablation devices and consumables.

- Technological improvements in real-time imaging and energy delivery expand clinical applications across oncology and cardiology.

- Growing procedural volumes in hospitals and ambulatory surgical centers drive consumable and device consumption.

- Investment by leading firms in R&D and product launches supports market expansion and broader clinical adoption.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $8.50 Billion |

| CAGR (2023-2033) | 7.3% |

| 2033 Market Size | $17.55 Billion |

| Top Companies | Medtronic , Boston Scientific, Abbott Laboratories, AngioDynamics, Hologic, Inc. |

| Published Date | 07 October 2024 |

| Last Modified Date | 25 May 2026 |

Ablation Technologies Market Overview

Customize Ablation Technologies Market Report market research report

- ✔ Get in-depth analysis of Ablation Technologies market size, growth, and forecasts.

- ✔ Understand Ablation Technologies's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Ablation Technologies

What is the Market Size & CAGR of Ablation Technologies Market Report market in 2023?

Ablation Technologies Industry Analysis

Ablation Technologies Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Ablation Technologies Market Report Market Analysis Report by Region

Europe Ablation Technologies Market Report:

Europe is largest regional market, rising from $3 Billion in 2023 to $6.19 Billion in 2033. Growth is supported by expanding use of minimally invasive procedures, strong hospital networks, and active participation by leading medical device companies.Asia Pacific Ablation Technologies Market Report:

Asia Pacific grows from $1.42 Billion in 2023 to $2.93 Billion in 2033. Market progression is influenced by growing procedural capacity, rising healthcare investment, and increasing acceptance of advanced ablation technologies in clinical practice.North America Ablation Technologies Market Report:

North America grows from $2.86 Billion in 2023 to $5.9 Billion in 2033. 86 Billion in 2023 to $5.9 Billion in 2033, reflecting steady uptake in hospitals and ambulatory centers. Local drivers include high procedural volumes, established clinical infrastructure, and ongoing product innovation from major suppliers.South America Ablation Technologies Market Report:

Latin America grows from $0.68 Billion in 2023 to $1.41 Billion in 2033. 68 Billion in 2023 to $1.41 Billion in 2033, driven by gradual increases in surgical procedures, improving healthcare access, and adoption of minimally invasive techniques in key urban centers.Middle East & Africa Ablation Technologies Market Report:

Middle East and Africa grows from $0.55 Billion in 2023 to $1.13 Billion in 2033. 55 Billion in 2023 to $1.13 Billion in 2033, supported by infrastructure investments, expansion of clinical services, and growing demand for advanced therapeutic procedures.Tell us your focus area and get a customized research report.

Research Methodology

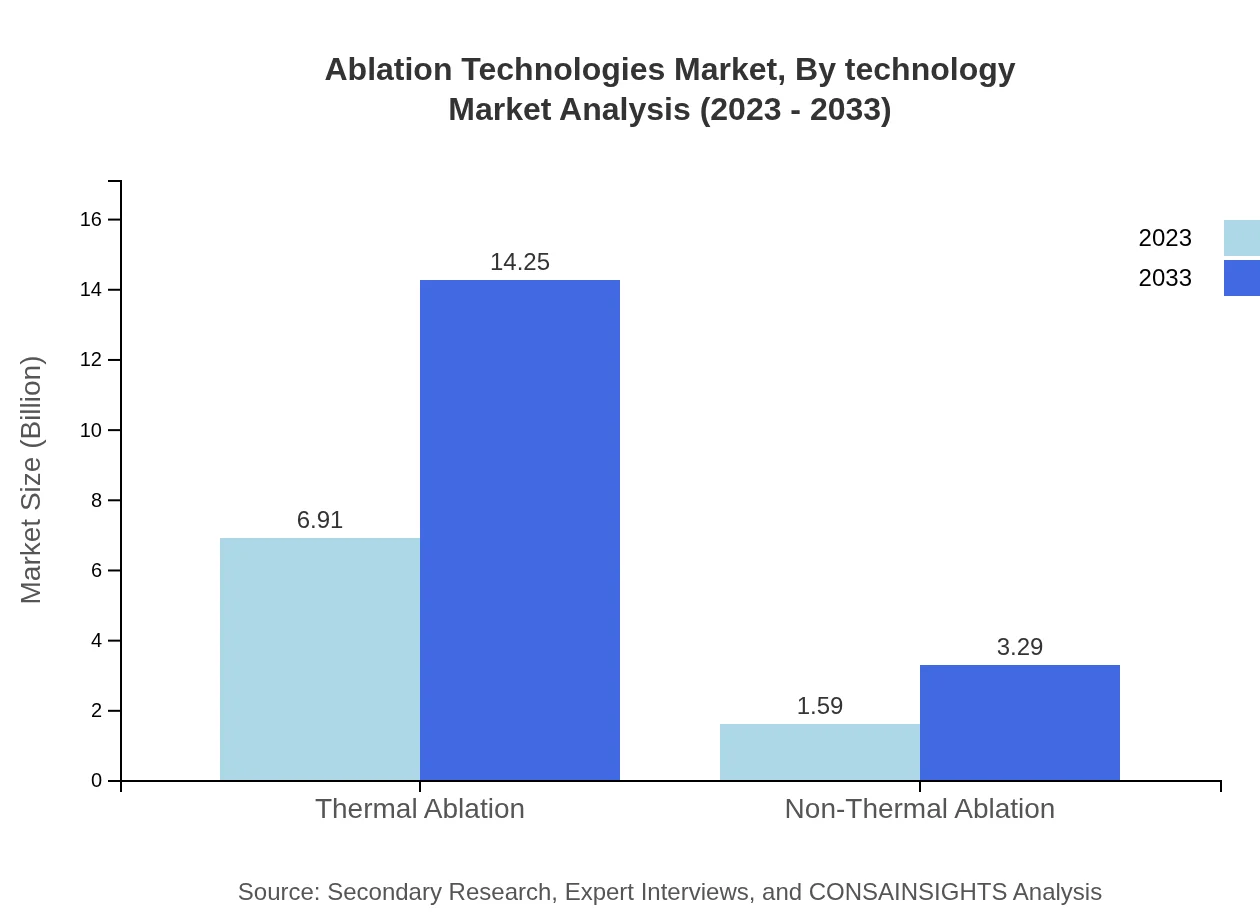

Ablation Technologies Market Analysis By Technology

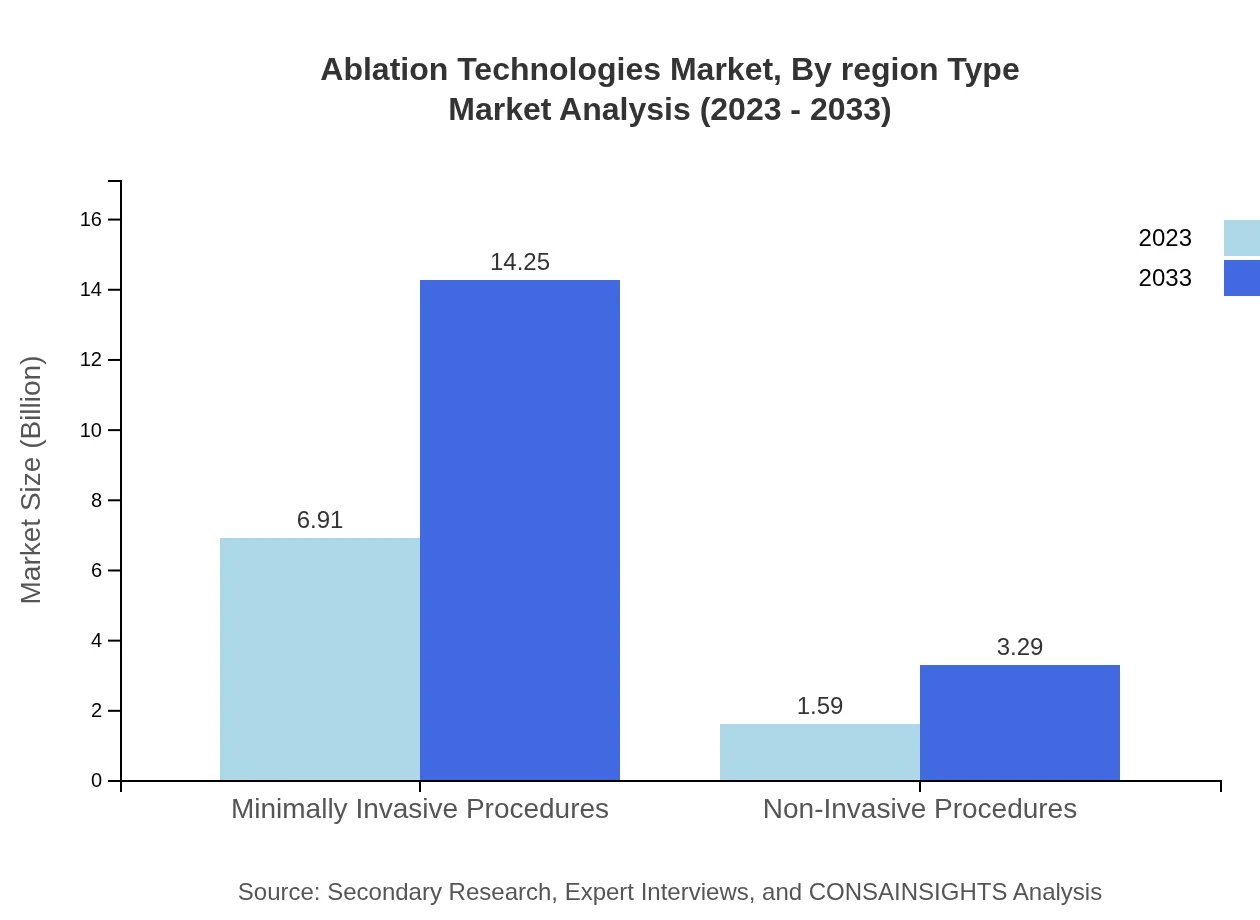

The Ablation Technologies market by technology is divided predominantly into thermal and non-thermal technologies. In 2023, thermal ablation dominates with market shares of approximately 81.24%, demonstrating its significant preference in medical settings. This segment is expected to grow to around $14.25 billion by 2033. Non-thermal ablation, although smaller, also shows potential growth from $1.59 billion in 2023 to $3.29 billion in 2033.

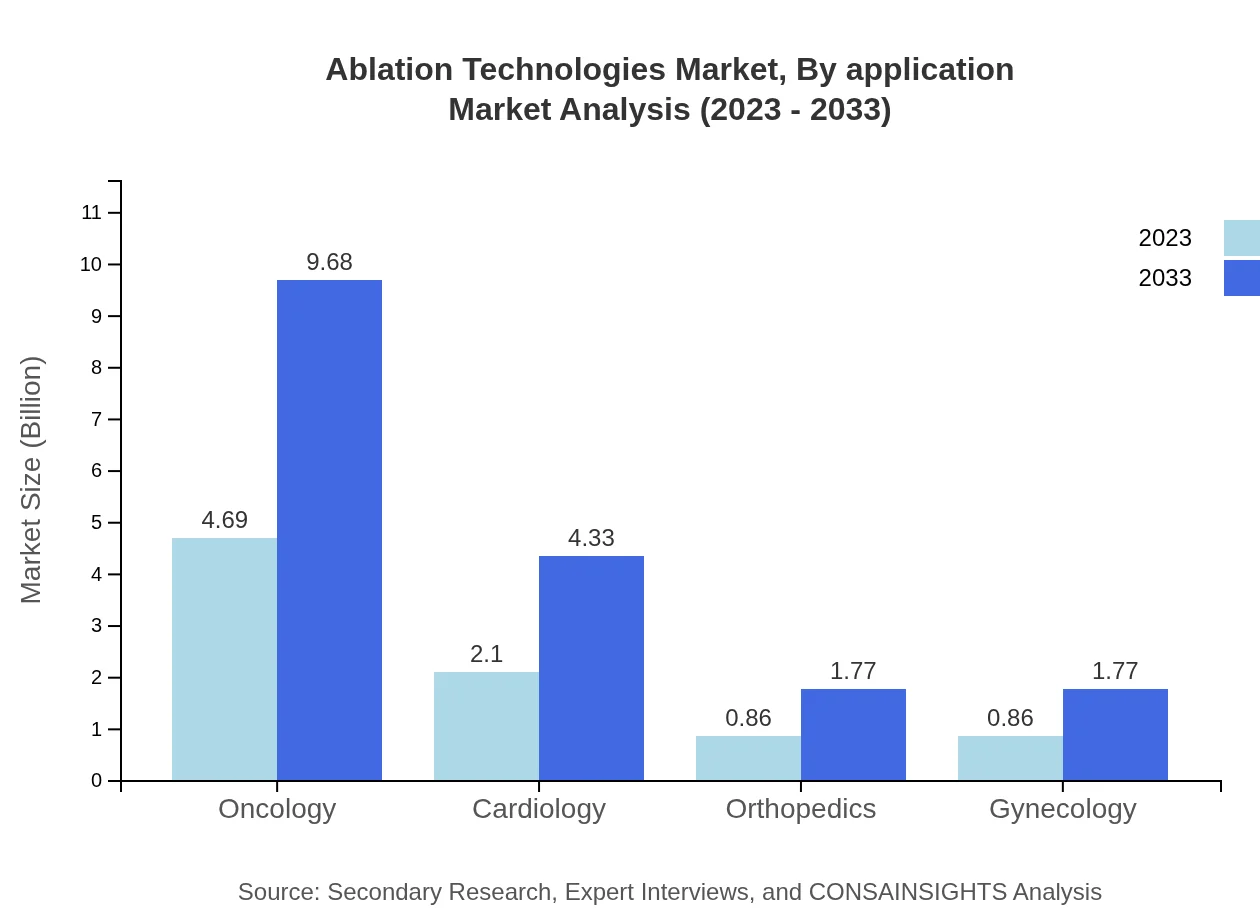

Ablation Technologies Market Analysis By Application

By application, the market is primarily divided into oncology, cardiology, orthopedics, and gynecology. The oncology segment is noteworthy, contributing about $4.69 billion in 2023 and expected to expand to $9.68 billion by 2033, maintaining around 55.15% market share. The cardiology segment holds a significant share as well, projected to grow from $2.10 billion in 2023 to approximately $4.33 billion by 2033.

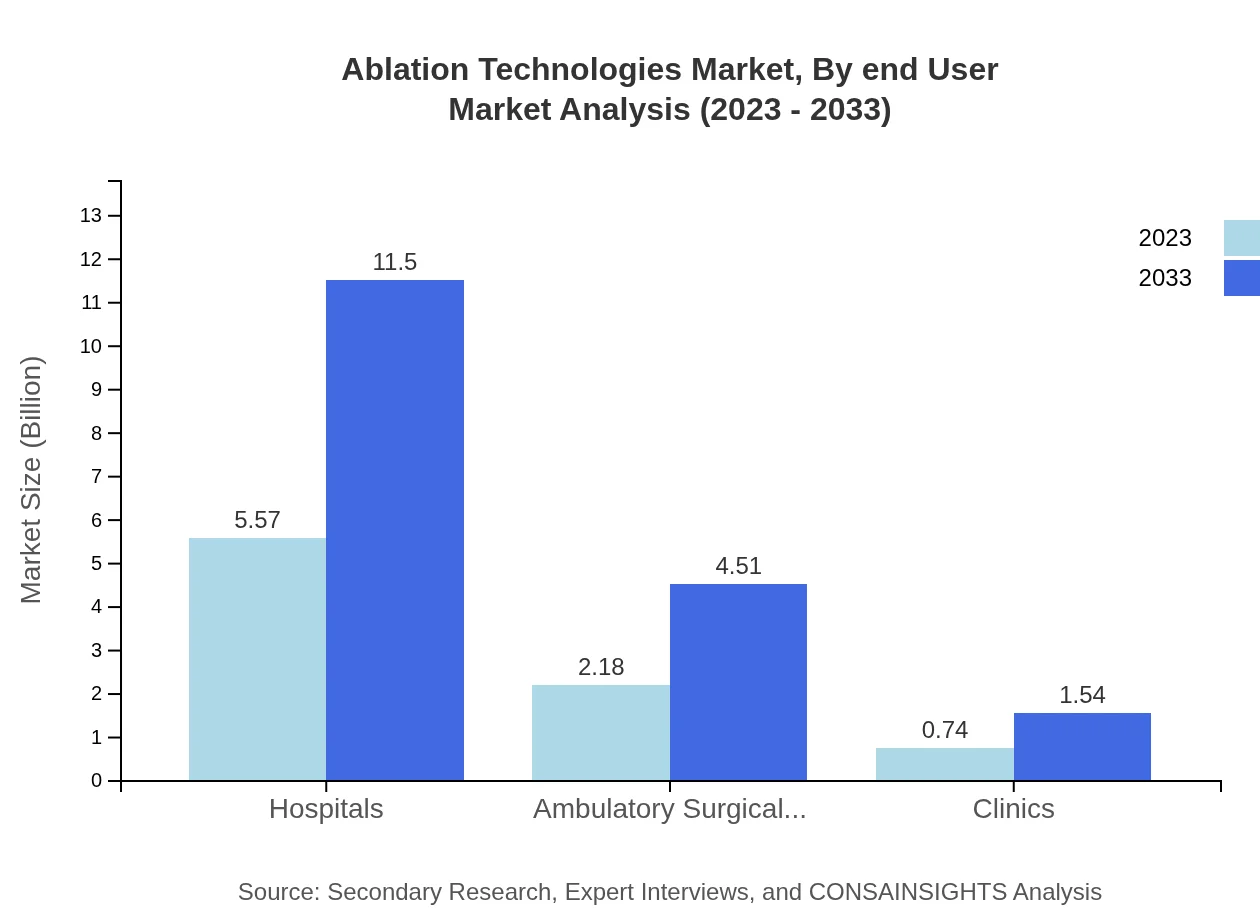

Ablation Technologies Market Analysis By End User

End-user analysis of the Ablation Technologies market reveals hospitals as the primary consumers, expected to maintain a significant share of 65.56% with revenues of about $5.57 billion in 2023 and growing to $11.50 billion by 2033. Ambulatory surgical centers also represent a substantial segment, with projections rising from $2.18 billion to $4.51 billion in the same timeframe.

Ablation Technologies Market Analysis By Region Type

The Ablation Technologies market exhibits varied trends across regions, with North America leading in innovation and spending, while Asia-Pacific shows rapid growth due to improving healthcare systems and increasing surgical procedures. Europe is characterized by stringent regulations and high technological adoption, while South America is gradually growing with healthcare advancements. The Middle East and Africa face challenges but are witnessing increased investments in healthcare.

Ablation Technologies Market Analysis By Product

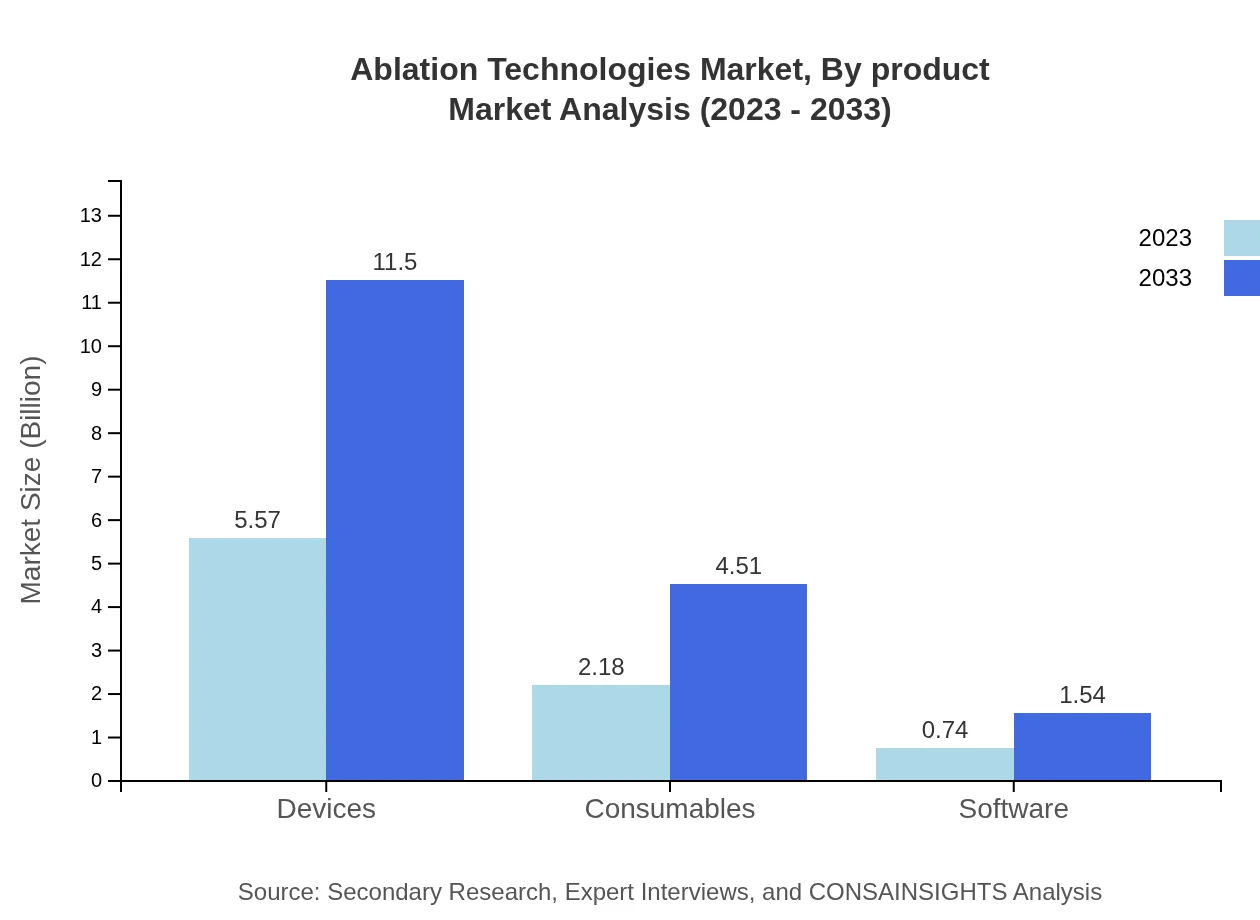

The Ablation Technologies market can also be segmented into devices, consumables, and software. The devices segment dominates with a market size of $5.57 billion in 2023, steadily growing to about $11.50 billion by 2033. Consumables hold a share of approximately 25.68% with growth anticipated from $2.18 billion to $4.51 billion. Software remains a smaller but growing segment, expected to reach around $1.54 billion by 2033 from an initial size of $0.74 billion.

Ablation Technologies Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Ablation Technologies Industry

Medtronic :

A leading company in medical technologies, Medtronic specializes in various ablation technologies and has a strong presence in cardiac and vascular therapies.Boston Scientific:

Boston Scientific is known for its advanced therapeutic solutions, including a wide array of ablation devices that cater to different medical applications.Abbott Laboratories:

Abbott focuses on innovative therapies and technologies in the cardiovascular space, providing top-tier ablation solutions.AngioDynamics:

Specializing in minimally invasive medical devices, AngioDynamics offers a range of ablation technologies particularly for vascular access and oncology.Hologic, Inc.:

A global leader in women's health, Hologic develops unique ablation technologies designed to treat gynecological conditions.We're grateful to work with incredible clients.

FAQs

What is the market size of the ablation technologies market in 2023?

The market size in 2023 is $8.50 Billion, reflecting current product adoption and clinical use across hospitals, ambulatory surgical centers, and clinics globally.

How big will the market be in 2033?

By 2033 the market is projected to reach $17.55 Billion, based on ongoing technological adoption and expanding use in oncology, cardiology, orthopedics, and gynecology.

What is CAGR for the forecast period?

The compound annual growth rate (CAGR) over the 2023 to 2033 forecast period is 7.3%, driven by increasing minimally invasive procedures and device innovation.

Is there a single fastest Growing region in the Ablation Technologies Market Report market?

No single fastest-growing region is stated for the Ablation Technologies Market Report market because the top regional implied CAGR values are within 0.15 percentage points of each other, making the ranking too close to call reliably.

What are primary product segments covered?

Primary product groups include devices, consumables, and software, each supporting procedures across various clinical applications and end-user settings.

Why is Europe significant for this market?

Europe is the largest regional market, growing from $3 Billion in 2023 to $6.19 Billion in 2033, reflecting robust adoption and established clinical infrastructure.

Which end users drive market demand?

Hospitals, ambulatory surgical centers, and clinics form the main end-user base, providing the procedural volume and repeat consumable demand that support market growth.

What factors support long Term market growth?

Sustained growth is supported by technological advancement, increased procedural adoption in oncology and cardiology, and investments by major medical device companies.