Acute Care Needleless Connectors Market Report

First published: 11 October 2024 | Last updated: 25 May 2026 | Report Code: acute-care-needleless-connectors

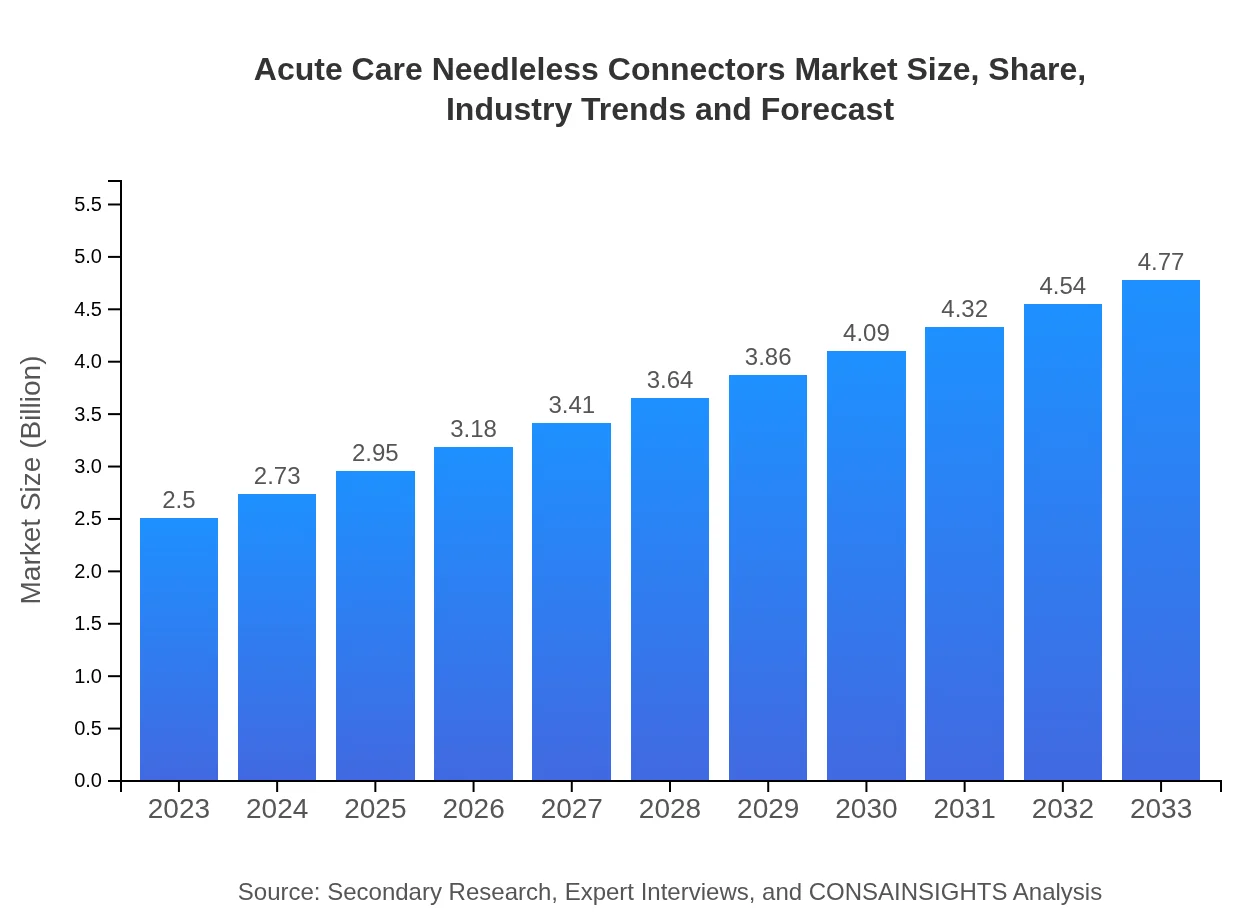

Acute Care Needleless Connectors Market — USD 2.5 billion in 2023, Growing to USD 4.77B by 2033 at 6.5% CAGR

This report provides a comprehensive analysis of the Acute Care Needleless Connectors market, covering insights, growth projections, and industry trends from 2023 to 2033. Key metrics include market sizing, segmentation, and forecasts for regional markets and product types.

Key Takeaways

- Global market value rises from $2.50 Billion in 2023 to $4.77 Billion in 2033 at a 6.5% CAGR across 2023 to 2033.

- North America is largest regional market, while no single fastest-growing region is stated because regional CAGR differences remain within 0.15 percentage points.

- Regional expansions are visible in Europe ($0.70 Billion to $1.34 Billion) and Asia Pacific ($0.47 Billion to $0.89 Billion).

- Product and safety innovations, stronger infection-prevention standards, and hospital demand drive adoption.

- Major players include B. Braun Melsungen AG, BD (Becton, Dickinson and Company), Cardinal Health, Fresenius Kabi, and C.R. Bard, Inc. (now part of BD).

Acute Care Needleless Connectors Market Report — Executive Summary

North America remains largest market by forecast-period value, while no single fastest-growing region is stated because top regional growth rates are separated by less than 0.15 percentage points. This report examines market dynamics shaping acute care needleless connectors, a segment critical to vascular access safety. The market is valued at $2.50 Billion in 2023 and is projected to grow to $4.77 Billion by 2033 at a 6.5% CAGR for 2023 to 2033. Growth is supported by emphasis on infection prevention, ongoing design improvements, and adoption across hospitals, ambulatory surgical centers, and home healthcare. Regulatory expectations and competitive investment in research are influencing product features and usability. Regional performance varies, with North America leading in absolute value. The analysis covers segmentation by end user, material, application, product type, and distribution channel, and profiles leading industry participants. Findings are intended to inform strategic planning, product development, and market-entry decisions for stakeholders in life sciences and medical devices.

Key Growth Drivers

- Rising infection-prevention protocols in healthcare settings increase demand for safer vascular access solutions.

- Continuous design enhancements and new connector technologies improve clinical usability and reduce contamination risk.

- Expansion of hospital services and ambulatory care facilities supports higher procurement of needleless connectors.

- Regulatory focus on device safety and manufacturer investments in product validation boost market confidence and adoption.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $2.50 Billion |

| CAGR (2023-2033) | 6.5% |

| 2033 Market Size | $4.77 Billion |

| Top Companies | B. Braun Melsungen AG, BD (Becton, Dickinson and Company), Cardinal Health, Fresenius Kabi, C.R. Bard, Inc. (now part of BD) |

| Published Date | 11 October 2024 |

| Last Modified Date | 25 May 2026 |

Acute Care Needleless Connectors Market Overview

Customize Acute Care Needleless Connectors Market Report market research report

- ✔ Get in-depth analysis of Acute Care Needleless Connectors market size, growth, and forecasts.

- ✔ Understand Acute Care Needleless Connectors's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Acute Care Needleless Connectors

What is the Market Size & CAGR of Acute Care Needleless Connectors Market Report market in 2023?

Acute Care Needleless Connectors Industry Analysis

Acute Care Needleless Connectors Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Acute Care Needleless Connectors Market Report Market Analysis Report by Region

Europe Acute Care Needleless Connectors Market Report:

Europe grows from $0.7 Billion in 2023 to $1.34 Billion in 2033. Regional expansion is supported by strengthened infection-control protocols, hospital modernization, and regulatory attention to device performance.Asia Pacific Acute Care Needleless Connectors Market Report:

Asia Pacific grows from $0.47 Billion in 2023 to $0.89 Billion in 2033. Demand is driven by expanding healthcare infrastructure, broader access to acute care services, and interest in technologies that reduce catheter-related complications.North America Acute Care Needleless Connectors Market Report:

North America is largest regional market, rising from $0.96 Billion in 2023 to $1.84 Billion in 2033. This growth reflects concentrated hospital demand, emphasis on clinical safety, and manufacturer presence supporting adoption in acute care settings.South America Acute Care Needleless Connectors Market Report:

Latin America grows from $0.12 Billion in 2023 to $0.23 Billion in 2033. Market progression is influenced by growing clinical capacity, selective adoption in hospitals, and an increasing focus on patient safety measures.Middle East & Africa Acute Care Needleless Connectors Market Report:

Middle East and Africa grows from $0.25 Billion in 2023 to $0.48 Billion in 2033. Growth stems from investments in healthcare facilities, rising awareness of infection-prevention practices, and procurement for acute care environments.Tell us your focus area and get a customized research report.

Research Methodology

Acute Care Needleless Connectors Market Analysis By Product Type

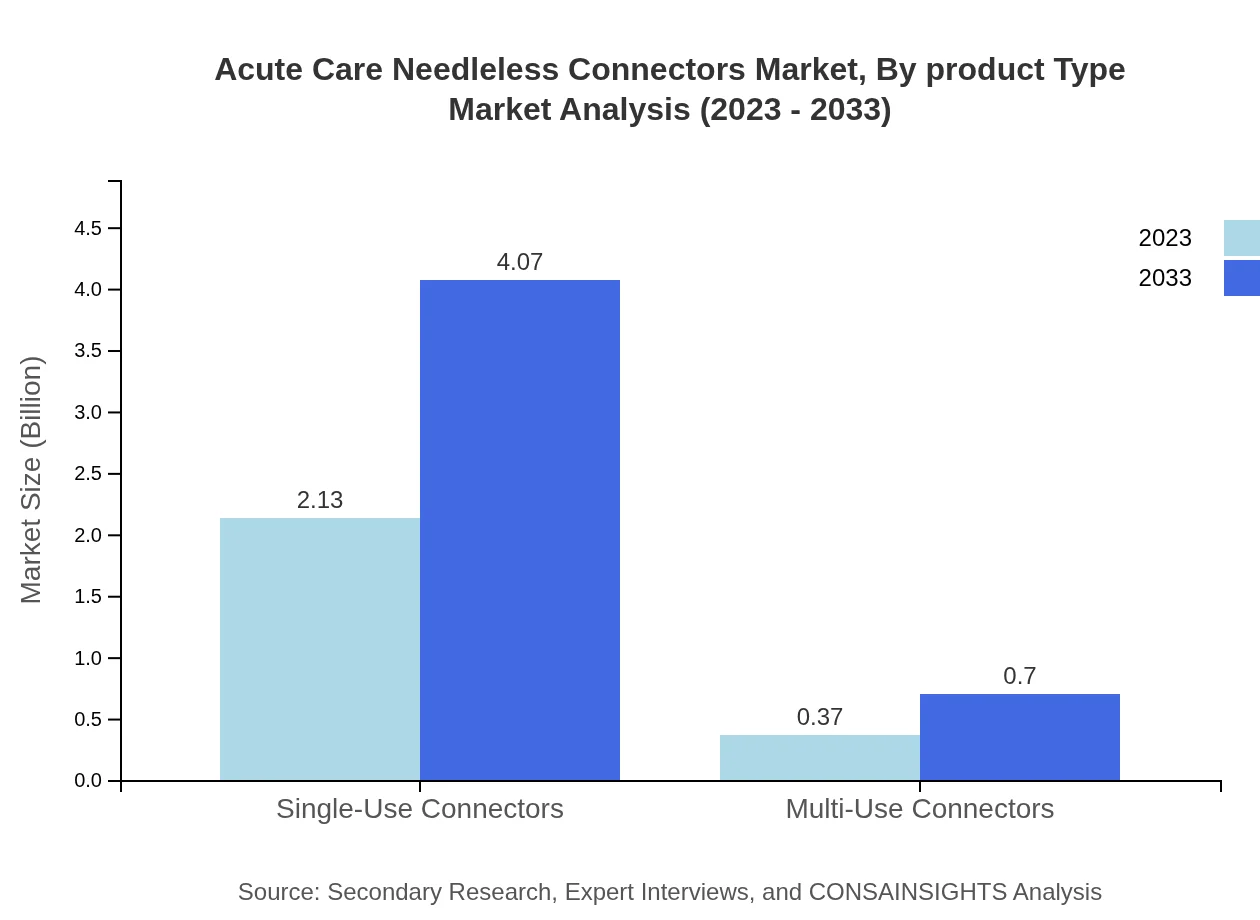

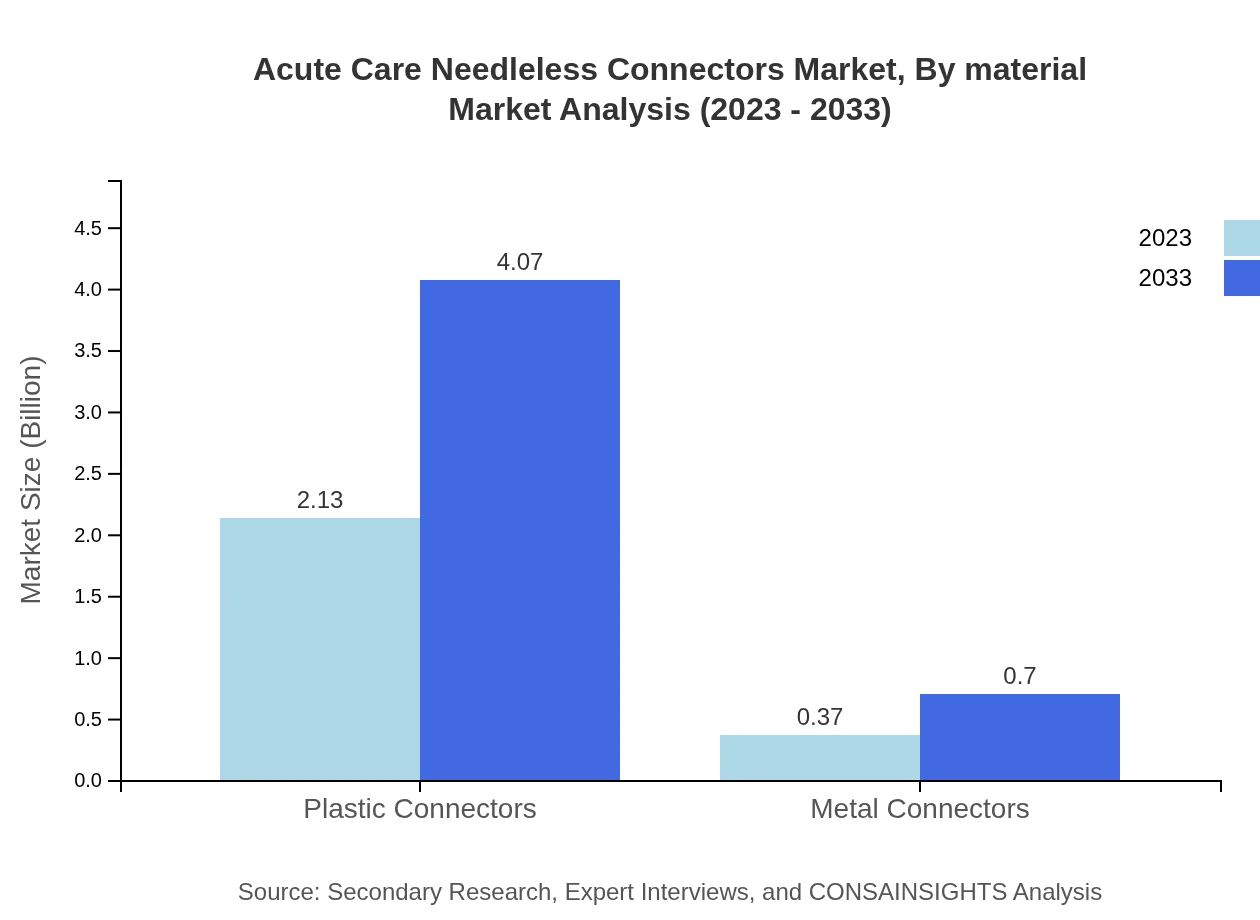

The market for Acute Care Needleless Connectors is dominated by plastic connectors, which account for 85.31% market share in 2023, projected to grow from $2.13 billion to $4.07 billion by 2033. Metal connectors account for 14.69% of the market, showing growth from $0.37 billion to $0.70 billion. This reflects a consumer preference for single-use and disposable options to minimize infection risks.

Acute Care Needleless Connectors Market Analysis By Application

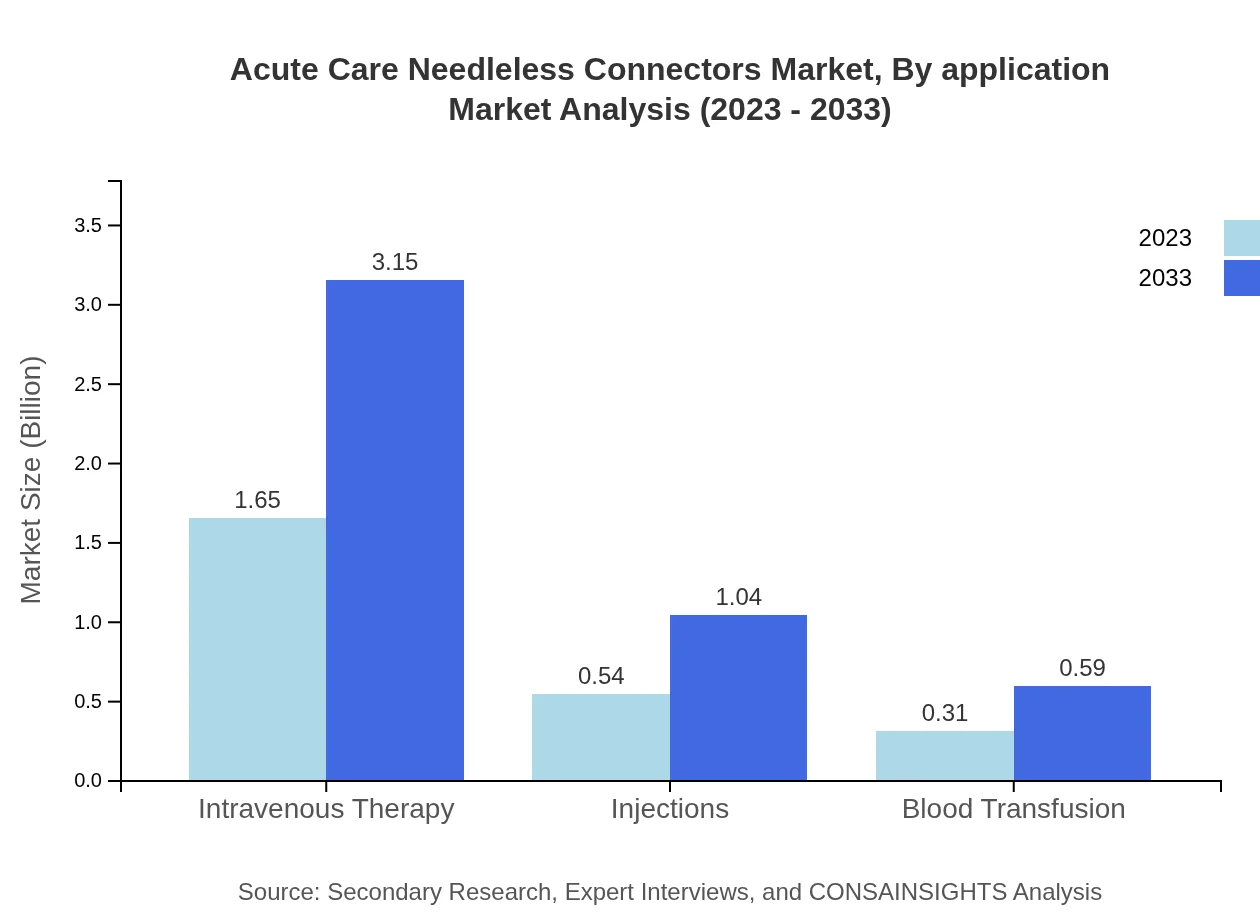

In terms of applications, intravenous therapy holds the largest share at 65.95%, with market size increasing significantly from $1.65 billion in 2023 to $3.15 billion in 2033. Other applications such as injections (21.71% share) and blood transfusion (12.34% share) also showcase robust growth trajectories, promoting increased safety in patient care.

Acute Care Needleless Connectors Market Analysis By End User

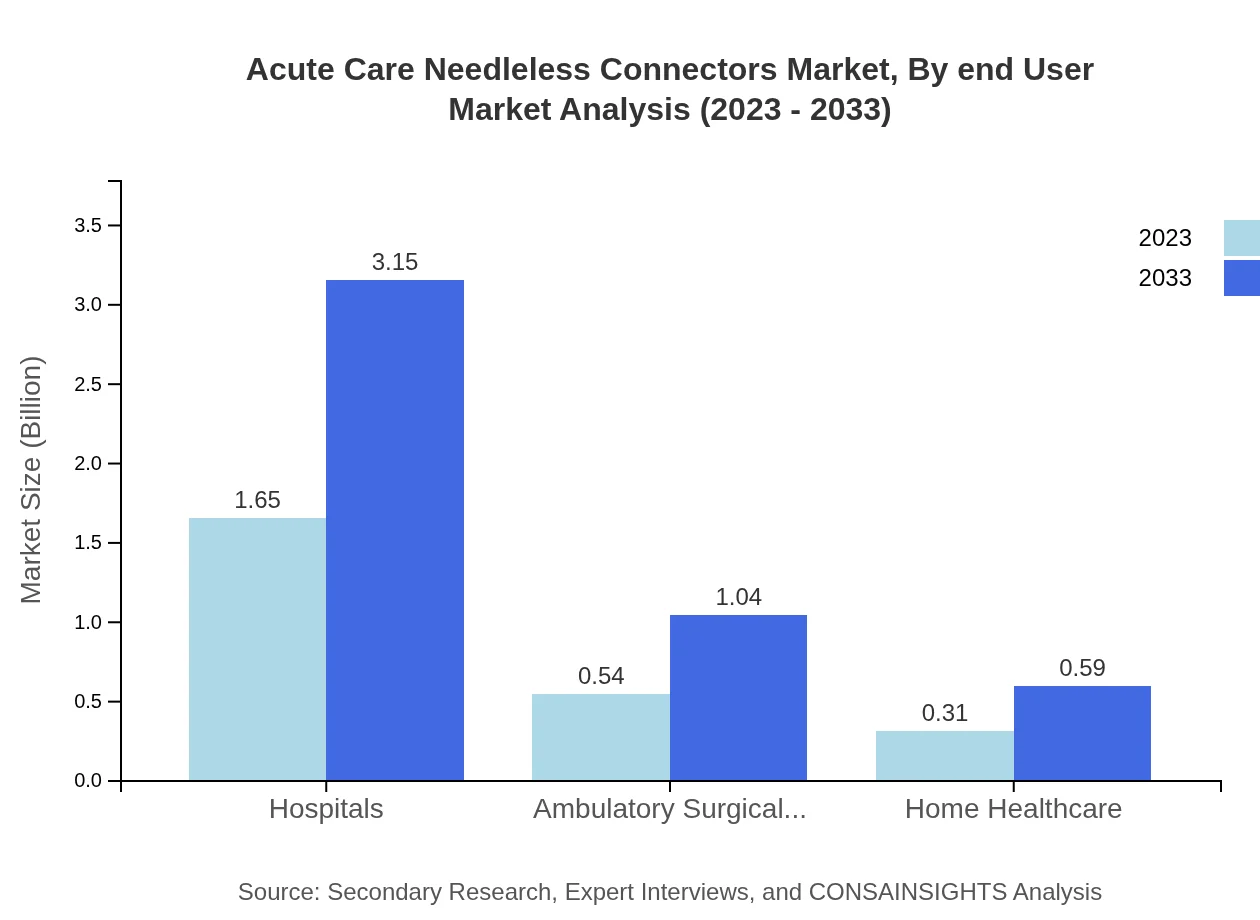

The end-user segment shows hospitals as the primary consumers, accounting for 65.95% market share and growing from $1.65 billion to $3.15 billion. Ambulatory surgical centers have a share of 21.71%, while home healthcare represents 12.34%. The expansion in these areas is driven by increasing surgical procedures and patient preferences for at-home care.

Acute Care Needleless Connectors Market Analysis By Material

Analyzing the market based on material, single-use connectors dominate the landscape, representing 85.31% of the market, increasing from $2.13 billion to $4.07 billion. Multi-use connectors, accounting for 14.69%, are expected to grow from $0.37 billion to $0.70 billion, reflecting trends towards cost-effectiveness combined with safety.

Acute Care Needleless Connectors Market Analysis By Distribution Channel

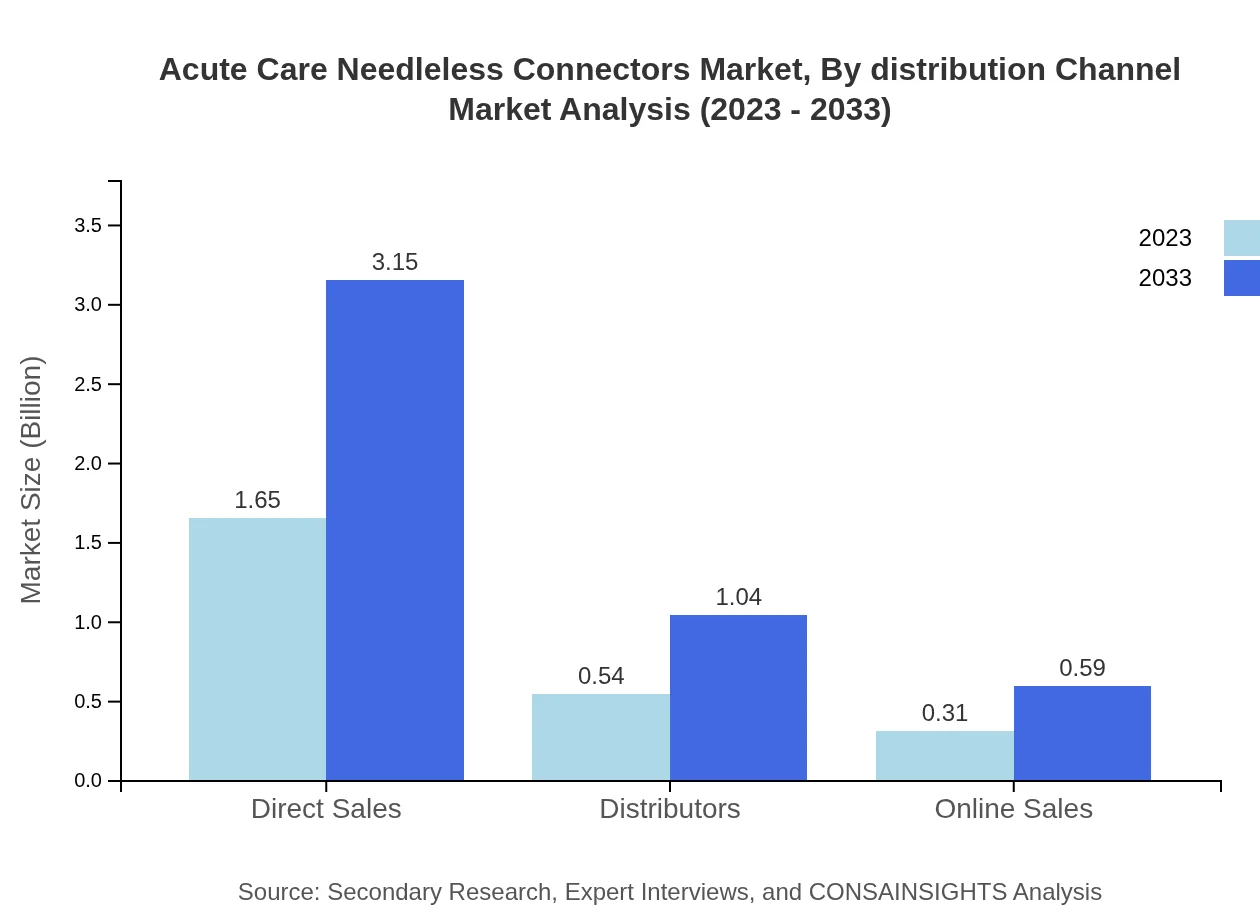

Distribution channels for Acute Care Needleless Connectors include direct sales (65.95% market share), distributors (21.71%), and online sales (12.34%). This segmentation illustrates growing trends toward direct relationships for healthcare procurement while also acknowledging the rising prominence of online sales amid changing shopping behaviors.

Acute Care Needleless Connectors Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Acute Care Needleless Connectors Industry

B. Braun Melsungen AG:

A leading global player in medical technology, B. Braun specializes in infusion therapy, offering innovative needleless connector solutions aimed at enhancing patient safety.BD (Becton, Dickinson and Company):

As a major player in the healthcare sector, BD provides comprehensive solutions for medication delivery, including advanced needleless connectors designed to reduce infection risk.Cardinal Health:

Cardinal Health supplies products and services across the healthcare system, focusing on medication management that includes an extensive range of needleless connection devices.Fresenius Kabi:

Fresenius Kabi develops and manufactures essential medicines and medical devices, including sophisticated needleless connectors that enhance safety and efficiency.C.R. Bard, Inc. (now part of BD):

Known for its innovations in vascular and surgical products, Bard offers a variety of needleless connector systems that help minimize risk in healthcare procedures.We're grateful to work with incredible clients.

FAQs

What is the market size of the Acute Care Needleless Connectors Market Report in 2023?

The market size in 2023 is $2.50 Billion, based on reported values for the acute care needleless connectors segment and used as the baseline for the 2023 to 2033 forecast period.

How big will the market be by 2033?

By 2033 the market is projected to reach $4.77 Billion, reflecting the ten-year forecast outcome reported for acute care needleless connectors across the 2023 to 2033 period.

What is CAGR for the forecast period?

The compound annual growth rate for the market over 2023 to 2033 is 6.5%, representing the reported annualized growth rate applied across the ten-year projection.

Is there a single fastest Growing region in the Acute Care Needleless Connectors Market Report market?

No single fastest-growing region is stated for the Acute Care Needleless Connectors Market Report market because the top regional implied CAGR values are within 0.15 percentage points of each other, making the ranking too close to call reliably.

Which companies are listed as leading players?

Top companies named include B. Braun Melsungen AG, BD (Becton, Dickinson and Company), Cardinal Health, Fresenius Kabi, and C.R. Bard, Inc. (now part of BD).

Who are primary end users for these connectors?

Primary end users reported include hospitals, ambulatory surgical centers, and home healthcare settings, reflecting delivery points for vascular access devices and therapies.

What product types are covered in the segmentation?

Segmentation includes single-use connectors and multi-use connectors, which are listed as the two product-type subsegments within the report's structure.

How are distribution channels categorized?

Distribution channels in the report are Direct Sales, Distributors, and Online Sales, representing primary routes for product delivery to healthcare providers.