Reports >

Technology And Media

>

Anomaly Detection Market Report

Anomaly Detection Market Report

Published Date: 31 January 2026 | Report Code: anomaly-detection

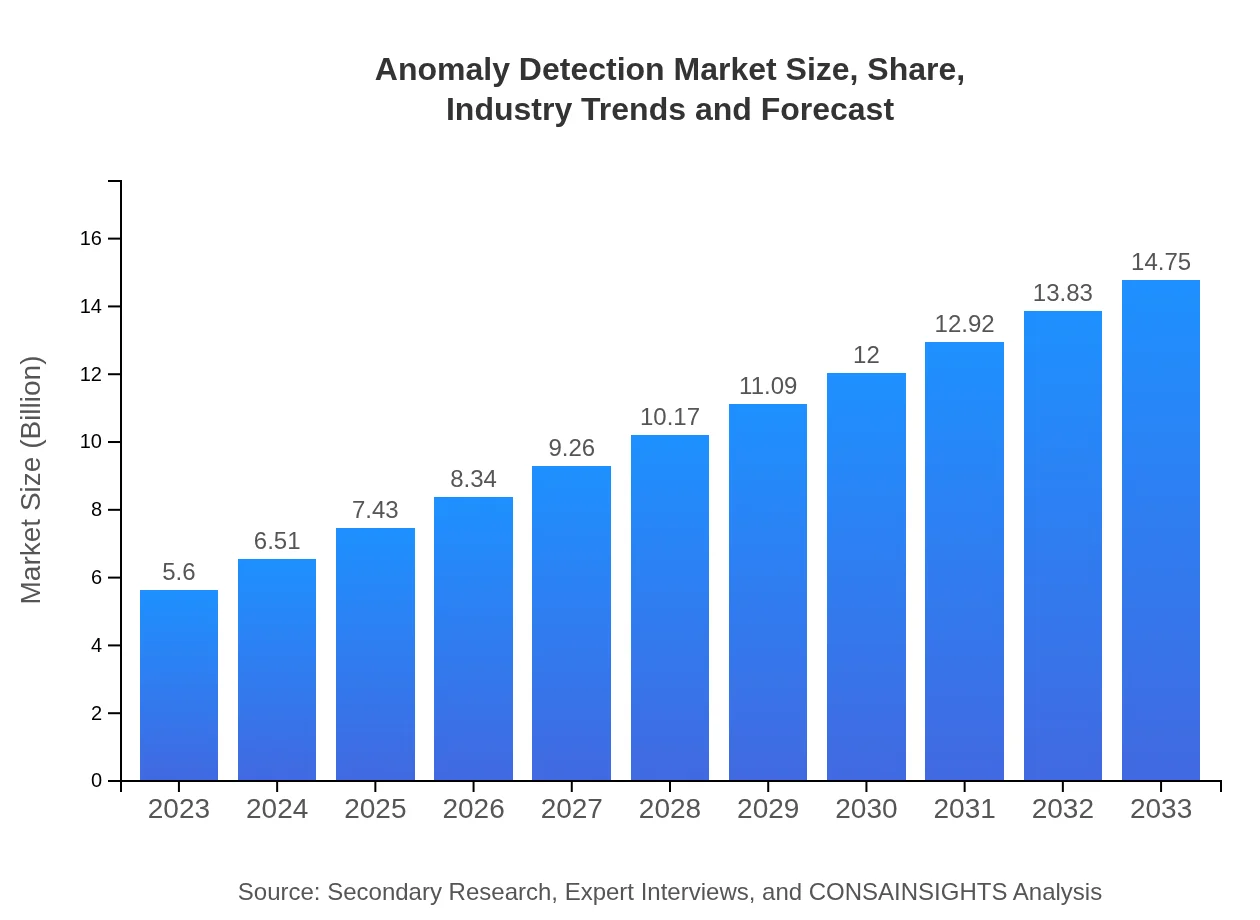

Anomaly Detection Market Size, Share, Industry Trends and Forecast to 2033

This report provides an in-depth analysis of the anomaly detection market, detailing its size, growth prospects, and key trends from 2023 to 2033. It also explores regional insights and industry segments contributing to the market's expansion.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.60 Billion |

| CAGR (2023-2033) | 9.8% |

| 2033 Market Size | $14.75 Billion |

| Top Companies | IBM, Microsoft, SAS Institute, Splunk |

| Last Modified Date | 31 January 2026 |

Anomaly Detection Market Overview

Customize Anomaly Detection Market Report market research report

- ✔ Get in-depth analysis of Anomaly Detection market size, growth, and forecasts.

- ✔ Understand Anomaly Detection's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Anomaly Detection

What is the Market Size & CAGR of Anomaly Detection market in 2023 and beyond?

Anomaly Detection Industry Analysis

Anomaly Detection Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Anomaly Detection Market Analysis Report by Region

Europe Anomaly Detection Market Report:

The European market for anomaly detection is anticipated to grow from $1.44 billion in 2023 to $3.78 billion by 2033. The region's stringent regulations surrounding data protection and a proactive approach to cybersecurity investments are significant factors contributing to this growth.Asia Pacific Anomaly Detection Market Report:

In the Asia Pacific region, the anomaly detection market is expected to expand from $1.08 billion in 2023 to approximately $2.86 billion by 2033. The growth is fueled by rapid digital transformation and the increasing focus on cybersecurity across countries like China, India, and Japan, where technology adoption is on the rise.North America Anomaly Detection Market Report:

North America leads the market with an estimated size of $2.12 billion in 2023, expected to expand to $5.59 billion by 2033. This region has a well-established infrastructure for anomaly detection and is a hub for technological innovations, making it the primary market for advanced observation technologies.South America Anomaly Detection Market Report:

The anomaly detection market in South America is projected to grow from $0.25 billion in 2023 to $0.66 billion by 2033. While this growth is comparatively slower, the rising concerns regarding fraud in the finance and banking sectors are likely to fuel adoption in the coming years.Middle East & Africa Anomaly Detection Market Report:

The middle East and Africa market, currently valued at $0.71 billion, is expected to witness growth to around $1.86 billion by 2033. Increased investments in smart infrastructure and the growing need for enhanced cybersecurity protocols across multiple sectors are driving this expansion.Tell us your focus area and get a customized research report.

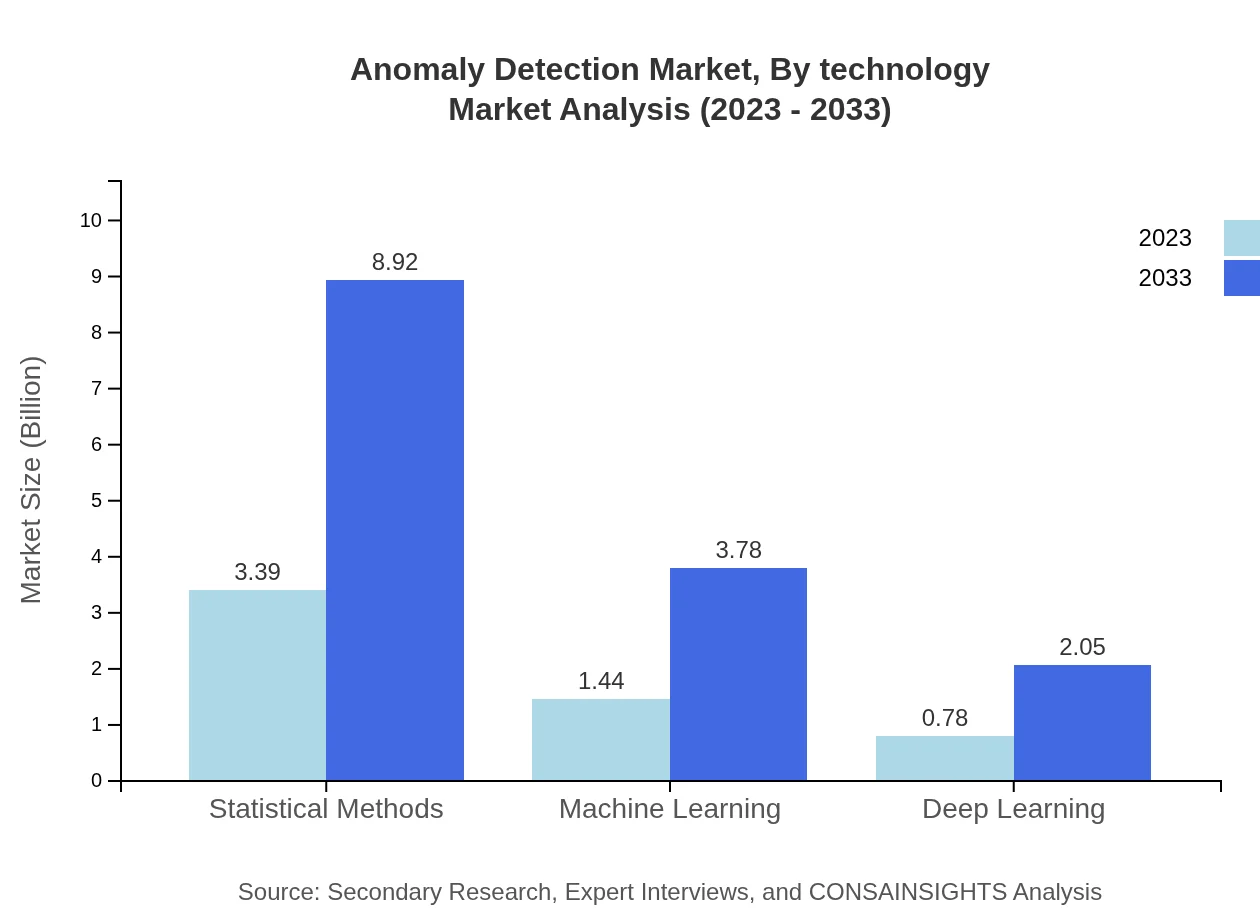

Anomaly Detection Market Analysis By Technology

The anomaly detection market is majorly driven by statistical methods, which are anticipated to grow from $3.39 billion in 2023 to $8.92 billion by 2033. Other contributing technologies include machine learning and deep learning, demonstrating significant segments that focus on more complex data patterns, thereby improving the detection processes.

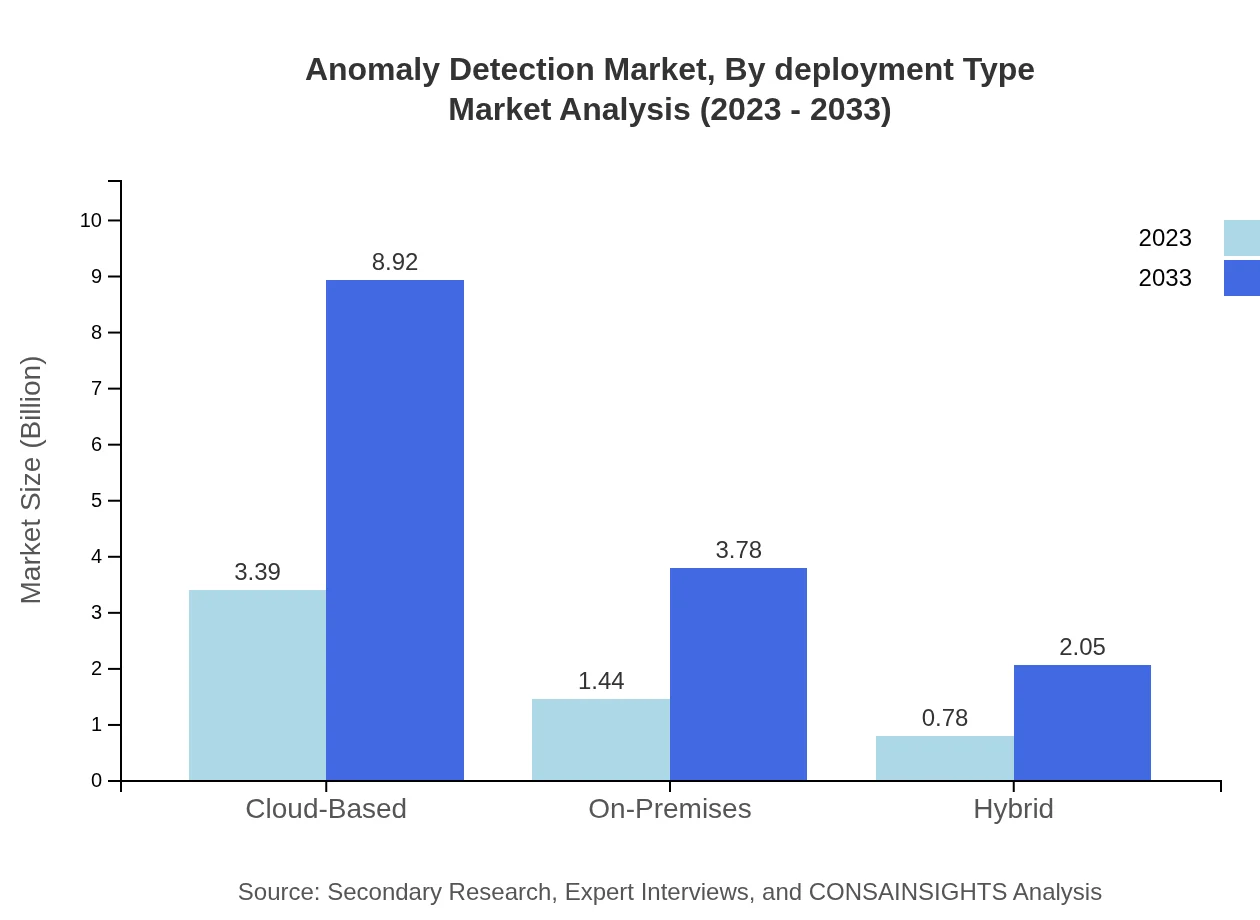

Anomaly Detection Market Analysis By Deployment Type

The market analysis by deployment type shows cloud-based solutions leading with a size of $3.39 billion in 2023 to $8.92 billion in 2033. On-premises deployments are also significant with a growth projection from $1.44 billion to $3.78 billion, indicating a preference amongst organizations for tailored solutions.

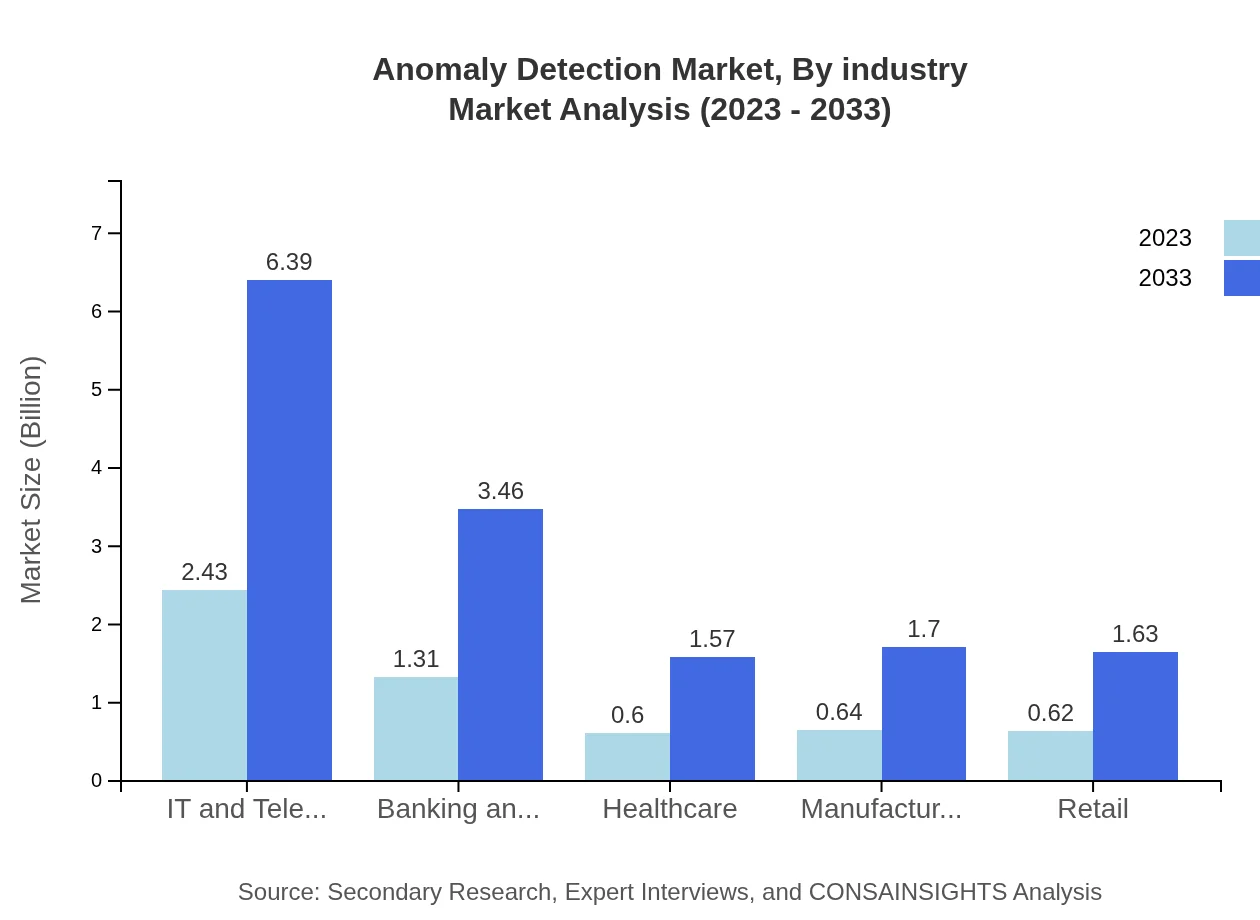

Anomaly Detection Market Analysis By Industry

Industries such as IT and telecom, and banking and finance form the backbone of the anomaly detection market, with sizes of $2.43 billion and $1.31 billion in 2023, respectively. By 2033, these industries are expected to maintain similar growth patterns, developing robust defenses against fraud and anomalies.

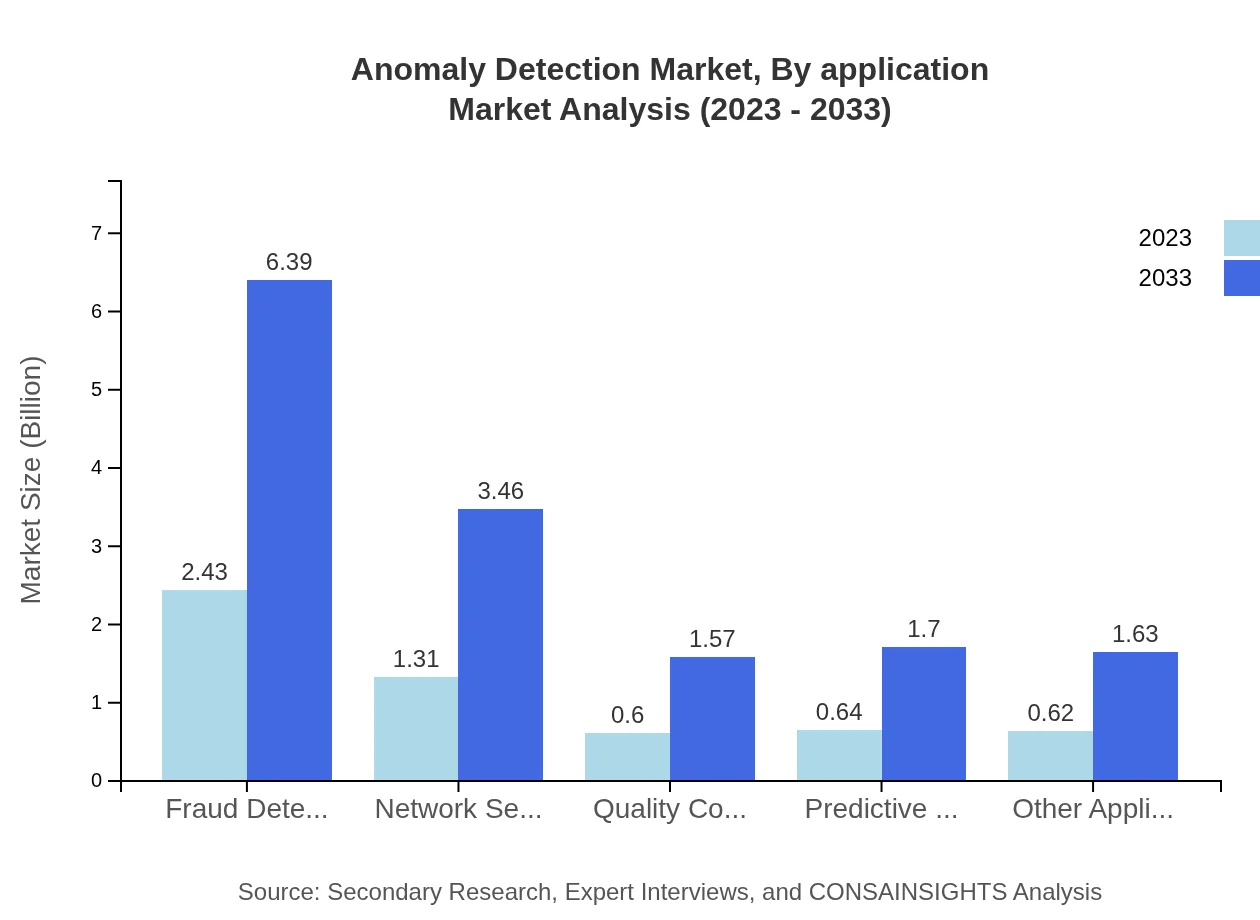

Anomaly Detection Market Analysis By Application

In terms of application, real-time monitoring leads with revenues increasing from $2.88 billion in 2023 to $7.59 billion by 2033. This significant growth underscores the critical need for continuous surveillance and oversight within various sectors, especially in finance and operations.

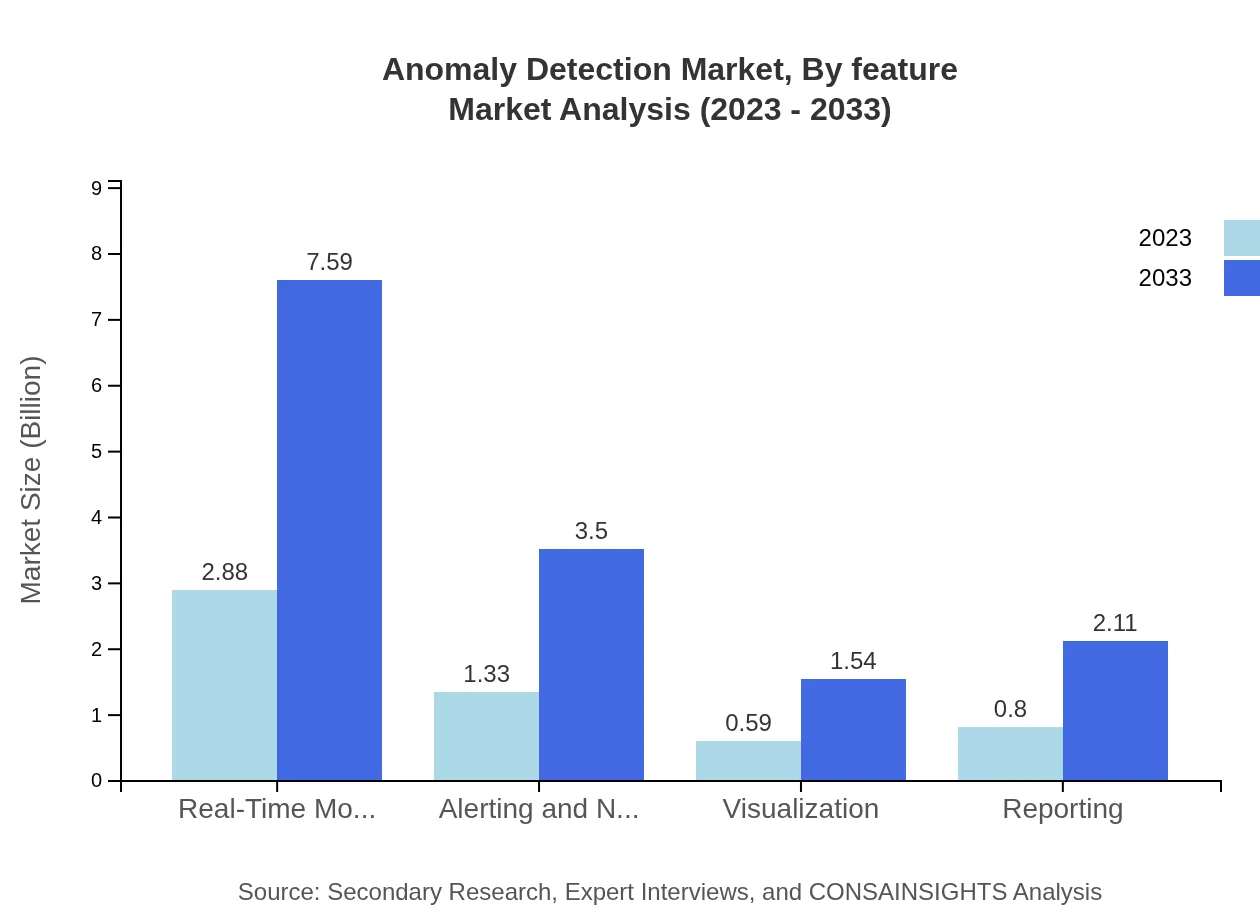

Anomaly Detection Market Analysis By Feature

The feature segment highlights critical capabilities such as alerting and notification systems, which are projected to grow from $1.33 billion in 2023 to $3.50 billion by 2033. This area signifies the shift towards proactive analytics, allowing businesses to respond quickly to potential threats.

Anomaly Detection Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Anomaly Detection Industry

IBM:

IBM is a leading player in the anomaly detection market, providing advanced AI and machine learning capabilities that enhance threat detection and response for its global clientele.Microsoft:

Microsoft offers an integrated suite of security products, leveraging its cloud platform to deliver robust anomaly detection systems for enterprises worldwide.SAS Institute:

SAS Institute specializes in advanced analytic solutions, helping businesses detect anomalies through powerful statistical and machine learning methodologies.Splunk:

Splunk is a major player in operational intelligence and is recognized for its ability to provide real-time insights through anomaly detection solutions tailored for various industries.We're grateful to work with incredible clients.

FAQs

What is the market size of anomaly Detection?

The anomaly-detection market is valued at $5.6 billion in 2023, with a projected CAGR of 9.8%, indicating strong growth potential through 2033.

What are the key market players or companies in this anomaly Detection industry?

Key players in the anomaly-detection industry include IBM, Microsoft, SAS Institute, and Splunk, among others. These companies are recognized for their innovative technologies and services that enhance anomaly detection capabilities.

What are the primary factors driving the growth in the anomaly Detection industry?

The growth in the anomaly-detection industry is driven by increasing cybersecurity threats, the rising adoption of IoT devices, and demand for efficient data analysis technologies, which enhance decision-making processes in various sectors.

Which region is the fastest Growing in the anomaly Detection?

North America is the fastest-growing region in the anomaly-detection market, projected to grow from $2.12 billion in 2023 to $5.59 billion by 2033, reflecting an escalating demand for technological advancements.

Does ConsaInsights provide customized market report data for the anomaly Detection industry?

Yes, ConsaInsights offers customized market reports tailored to the specific needs of clients in the anomaly-detection industry, ensuring relevant insights and data for strategic decision-making.

What deliverables can I expect from this anomaly Detection market research project?

Typical deliverables from an anomaly-detection market research project include comprehensive market analysis, regional insights, competitive landscape assessments, and tailored recommendations for market positioning.

What are the market trends of anomaly Detection?

Current trends in anomaly-detection include an increased focus on machine learning and AI technologies, a shift towards cloud-based solutions, and an emphasis on real-time monitoring and threat detection in various applications.