Atomic Layer Deposition Equipment Market Report

Published Date: 31 January 2026 | Report Code: atomic-layer-deposition-equipment

Atomic Layer Deposition Equipment Market Size, Share, Industry Trends and Forecast to 2033

This report provides a comprehensive analysis of the Atomic Layer Deposition Equipment market, covering trends, forecasts, and insights from 2023 to 2033. It examines market size, growth opportunities, regional dynamics, and key players, offering valuable data for stakeholders.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

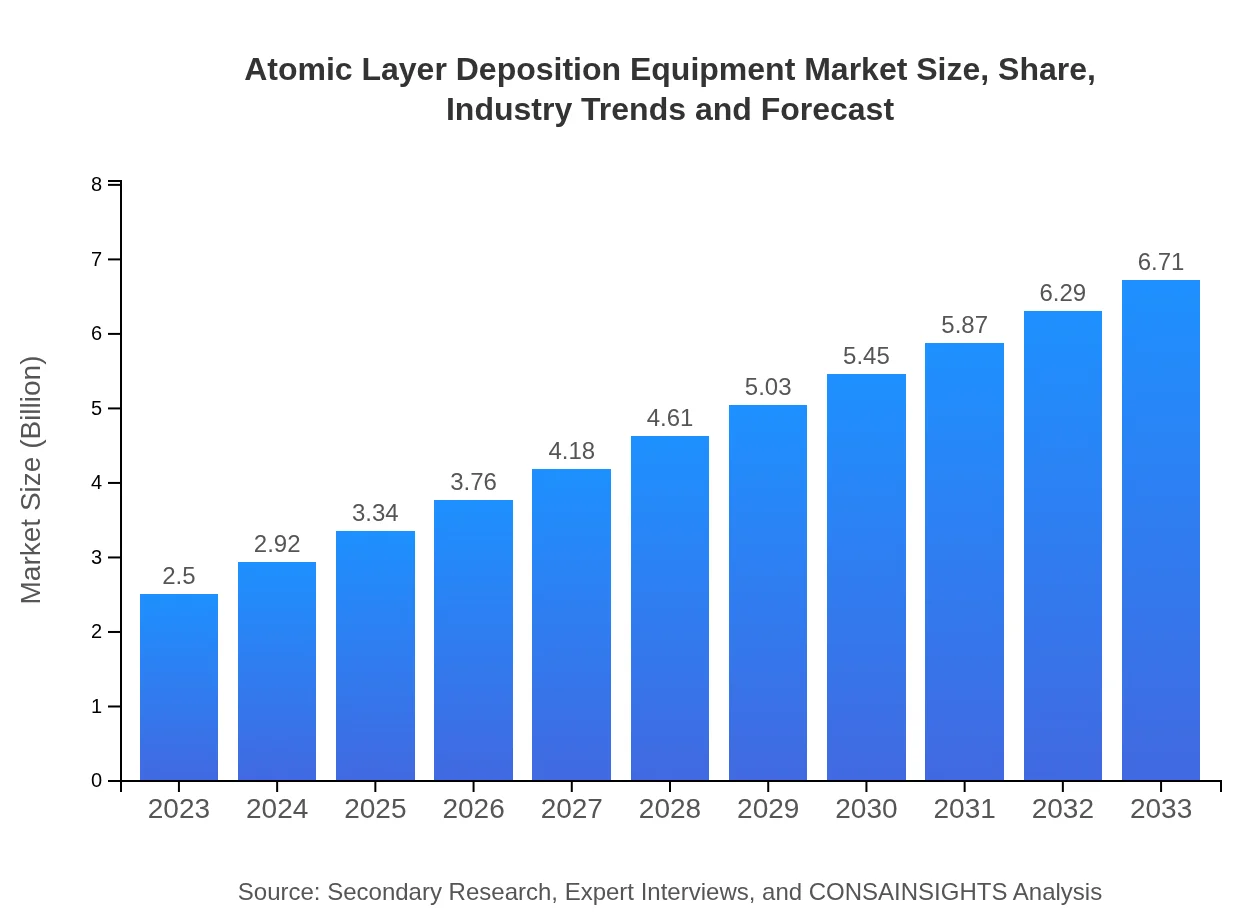

| 2023 Market Size | $2.50 Billion |

| CAGR (2023-2033) | 10% |

| 2033 Market Size | $6.71 Billion |

| Top Companies | Applied Materials, ASM International, Lam Research, Tokyo Electron Limited, Beneq |

| Last Modified Date | 31 January 2026 |

Atomic Layer Deposition Equipment Market Overview

Customize Atomic Layer Deposition Equipment Market Report market research report

- ✔ Get in-depth analysis of Atomic Layer Deposition Equipment market size, growth, and forecasts.

- ✔ Understand Atomic Layer Deposition Equipment's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Atomic Layer Deposition Equipment

What is the Market Size & CAGR of Atomic Layer Deposition Equipment market in 2023?

Atomic Layer Deposition Equipment Industry Analysis

Atomic Layer Deposition Equipment Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Atomic Layer Deposition Equipment Market Analysis Report by Region

Europe Atomic Layer Deposition Equipment Market Report:

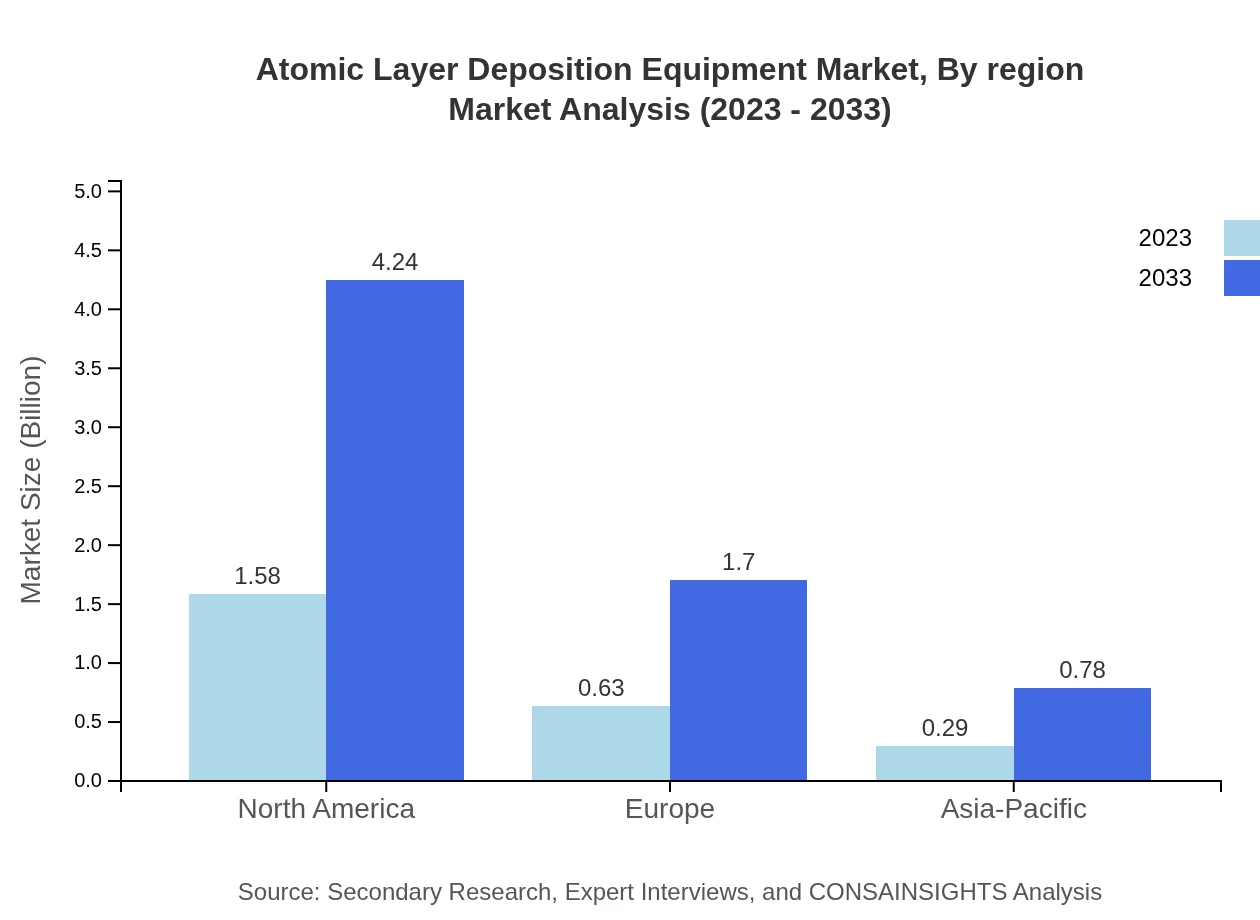

Europe's market size, growing from $0.78 billion in 2023 to $2.10 billion by 2033, is driven by stringent regulations promoting higher manufacturing standards and sustainability initiatives. The increasing number of semiconductor fabrication plants across Europe also encourages demand for ALD technologies.Asia Pacific Atomic Layer Deposition Equipment Market Report:

The Asia-Pacific region, valued at approximately $0.42 billion in 2023, is expected to grow to $1.13 billion by 2033. This growth is primarily driven by the increasing adoption of advanced electronics manufacturing and a robust semiconductor market. The region houses some of the largest semiconductor manufacturers, contributing significantly to the ALD equipment demand.North America Atomic Layer Deposition Equipment Market Report:

North America is anticipated to expand from $0.94 billion in 2023 to $2.52 billion by 2033. The region is recognized for its strong emphasis on R&D, particularly within advanced packaging and electronic applications, fostering a favorable environment for ALD equipment innovations.South America Atomic Layer Deposition Equipment Market Report:

In South America, the ALD Equipment market is valued at $0.12 billion in 2023 and is projected to reach $0.32 billion by 2033. The growth is mainly supported by increasing investments in renewable energy sectors and technological advancements in the materials industry.Middle East & Africa Atomic Layer Deposition Equipment Market Report:

The Middle East and Africa market, valued at $0.24 billion in 2023, is projected to reach $0.64 billion by 2033, primarily due to growing investments in the nanotechnology sector and increased focus on enhancing manufacturing capabilities in various industries.Tell us your focus area and get a customized research report.

Atomic Layer Deposition Equipment Market Analysis By Technology

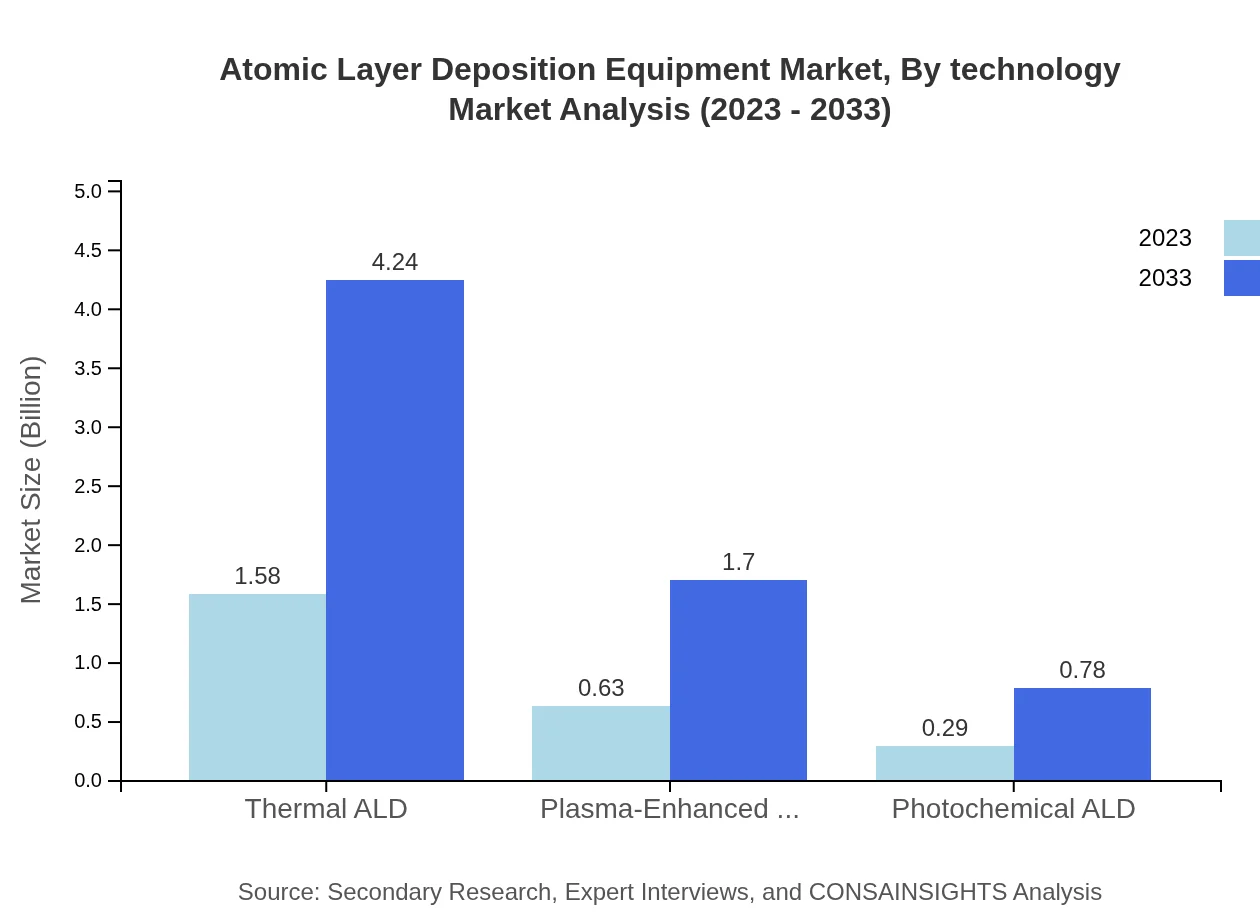

The market is dominated by Thermal ALD, which holds a significant share due to its efficiency in thin film deposition for semiconductor applications, accounting for approximately 63.17% of the market. Plasma-Enhanced ALD follows, capturing a share of about 25.27%, preferred for its rapid processing capabilities. Photochemical ALD, with an 11.56% market share, is gradually gaining traction in specialized applications. Each segment's growth reflects technological advancements and changing consumer needs across industries.

Atomic Layer Deposition Equipment Market Analysis By End User

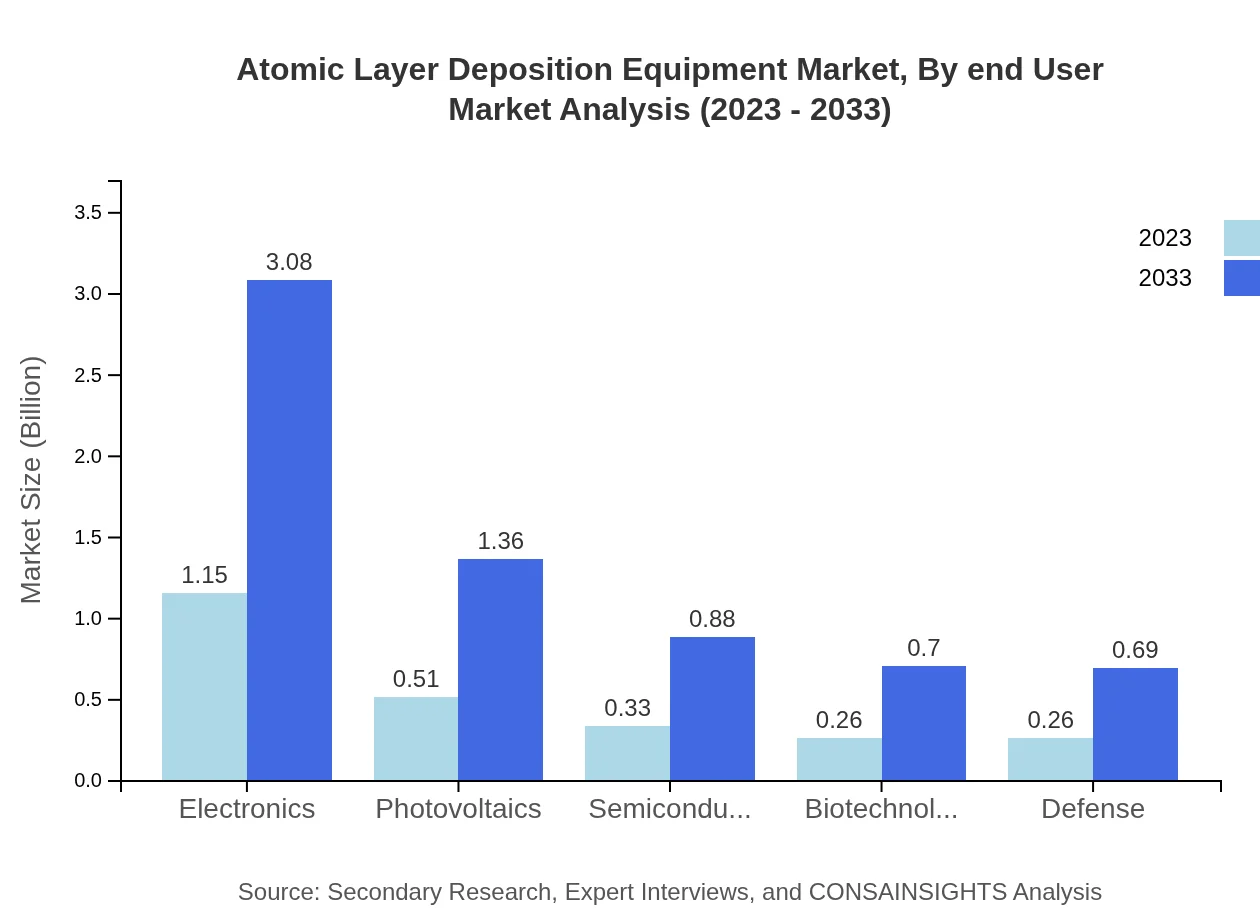

Key end-users of ALD equipment include electronics, photovoltaics, semiconductors, and biotechnology. The electronics sector is the largest consumer, representing almost 45.86% of the total market share. Following this, photovoltaics and semiconductors hold shares of 20.31% and 13.05%, respectively. Emerging industries like biotechnology and defense are also witnessing increased adoption of ALD technology for creating specialized materials, contributing to market diversification.

Atomic Layer Deposition Equipment Market Analysis By Application

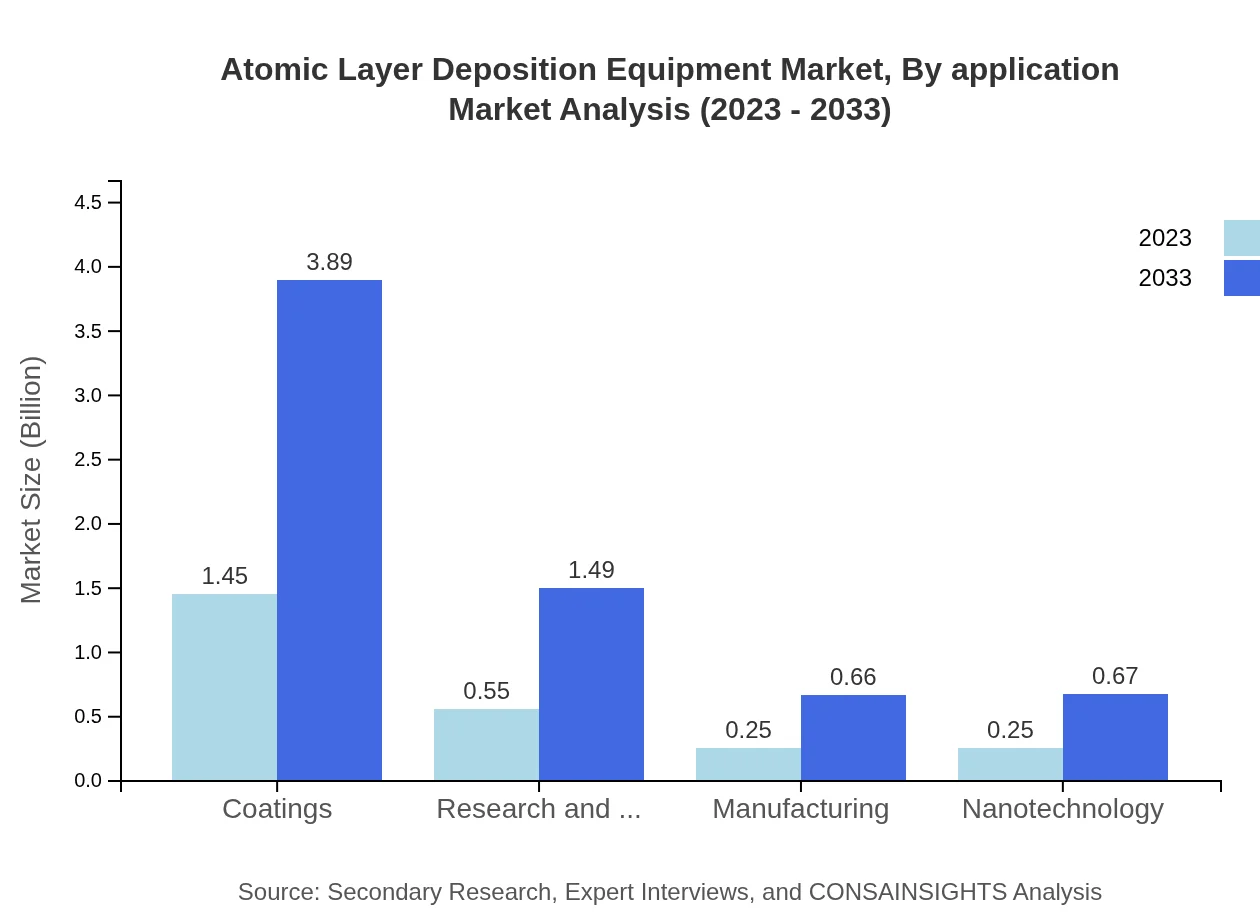

The applications of ALD equipment span coatings, research and development, manufacturing, and nanotechnology. Coatings are the leading application area, consuming about 57.97% of the market. It is followed by R&D applications, which constitute 22.16% of the market. The rising demand for nanotechnology-related applications is expected to drive further innovation and growth within the industry.

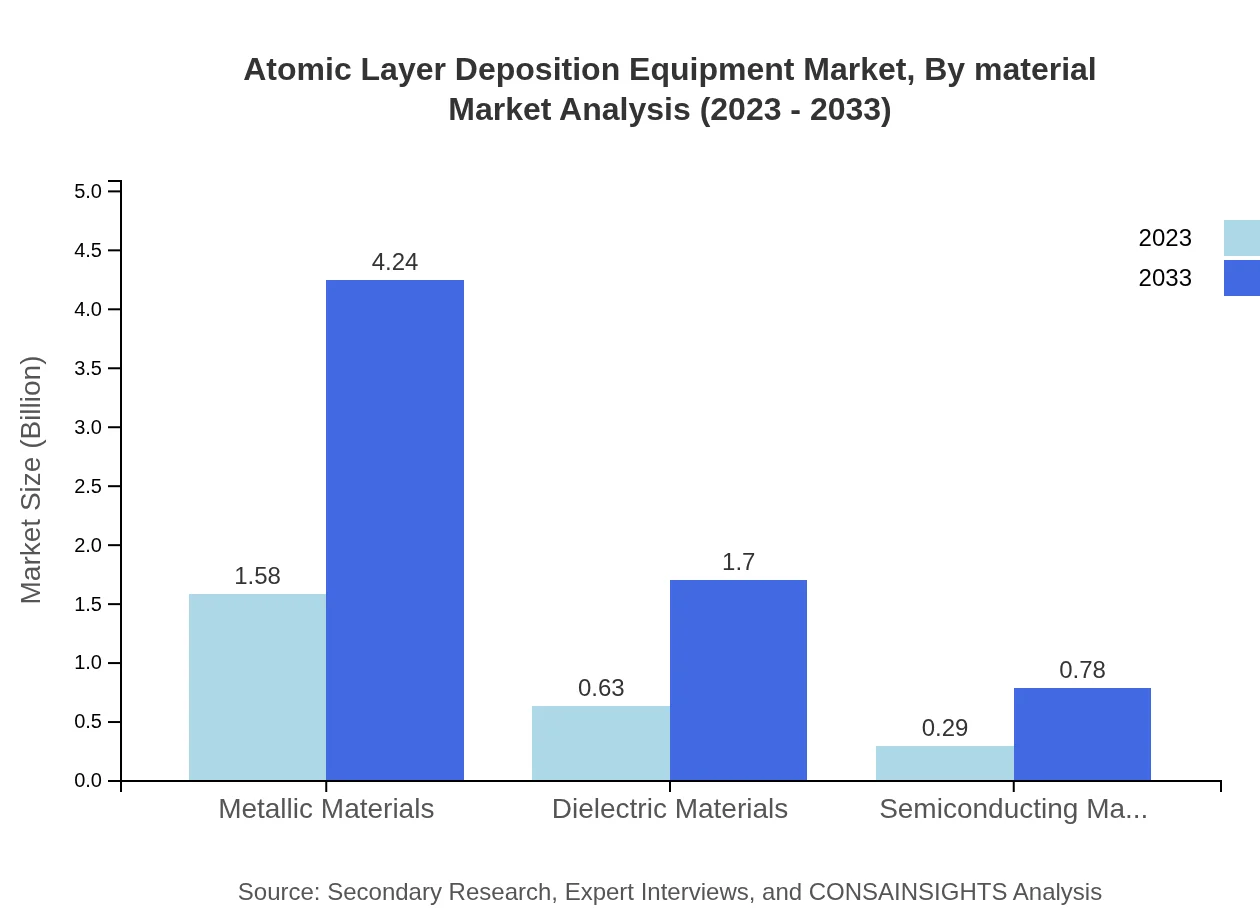

Atomic Layer Deposition Equipment Market Analysis By Material

In terms of materials, metallic materials dominate the ALD equipment segment, accounting for 63.17%, followed by dielectric materials at 25.27%. The need for precise material manipulation in electronic devices and components significantly supports these segments. The growing interest in semiconducting materials, with an 11.56% share, indicates potential growth opportunities as new applications arise.

Atomic Layer Deposition Equipment Market Analysis By Region

Regionally, North America leads with a share of 63.17% in the ALD equipment market, driven by strong electronic manufacturing capabilities. Europe follows with a 25.27% share, boosted by regulatory standards and sustainability goals. Asia-Pacific's growth is propelled by rapid technological advancements and strong semiconductor industries. South America and the Middle East & Africa, although smaller markets, show potential for growth due to increased investments in technology.

Atomic Layer Deposition Equipment Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Atomic Layer Deposition Equipment Industry

Applied Materials:

A leading player in the semiconductor equipment industry, Applied Materials offers innovative ALD systems that enhance manufacturing efficiency and product performance.ASM International:

ASM is recognized for its cutting-edge ALD technologies that cater to the semiconductor and advanced packaging industries, providing key equipment for diverse applications.Lam Research:

A significant contender in the semiconductor industry, Lam Research provides a variety of ALD solutions aimed at improving device performance across various sectors.Tokyo Electron Limited:

One of the foremost manufacturers of semiconductor production equipment, Tokyo Electron is known for its advanced ALD technologies that enable high throughput and precision.Beneq:

Beneq specializes in high-performance ALD systems used in various industries, including electronics, optics, and nanotechnology, focusing on innovation and sustainability.We're grateful to work with incredible clients.

FAQs

What is the market size of atomic Layer Deposition Equipment?

The global atomic layer deposition equipment market is projected to reach $2.5 billion by 2033, growing at a CAGR of 10% from its current size in 2023. This growth reflects increasing demand across various industries.

What are the key market players or companies in this atomic Layer Deposition Equipment industry?

Key players in the atomic layer deposition equipment market include major manufacturers and suppliers of deposition technology. Their innovative solutions and significant market shares determine the competitive landscape and influence industry advancements.

What are the primary factors driving the growth in the atomic Layer Deposition Equipment industry?

Growth in the atomic layer deposition equipment market is driven by technological advancements in electronics and semiconductors, increased adoption across industries, and the growing demand for high-precision deposition techniques in manufacturing.

Which region is the fastest Growing in the atomic Layer Deposition Equipment market?

North America is currently the fastest-growing region in the atomic layer deposition equipment market, expected to grow from $0.94 billion in 2023 to $2.52 billion by 2033, driven by a robust electronics industry.

Does ConsaInsights provide customized market report data for the atomic Layer Deposition Equipment industry?

Yes, ConsaInsights offers customized market report data tailored to clients’ specific needs in the atomic layer deposition equipment industry, providing detailed insights and analysis relevant to their business objectives.

What deliverables can I expect from this atomic Layer Deposition Equipment market research project?

From the atomic layer deposition equipment market research project, clients can expect comprehensive reports including market size analysis, growth forecasts, competitive landscape insights, and strategic recommendations tailored to key market segments.

What are the market trends of atomic Layer Deposition Equipment?

Current trends in the atomic layer deposition equipment market include the increasing use of ALD in semiconductor manufacturing, a rise in demand for environmentally friendly processes, and the growing relevance of nanotechnology in various applications.