Automotive Catalytic Converter Market Report

Published Date: 22 January 2026 | Report Code: automotive-catalytic-converter

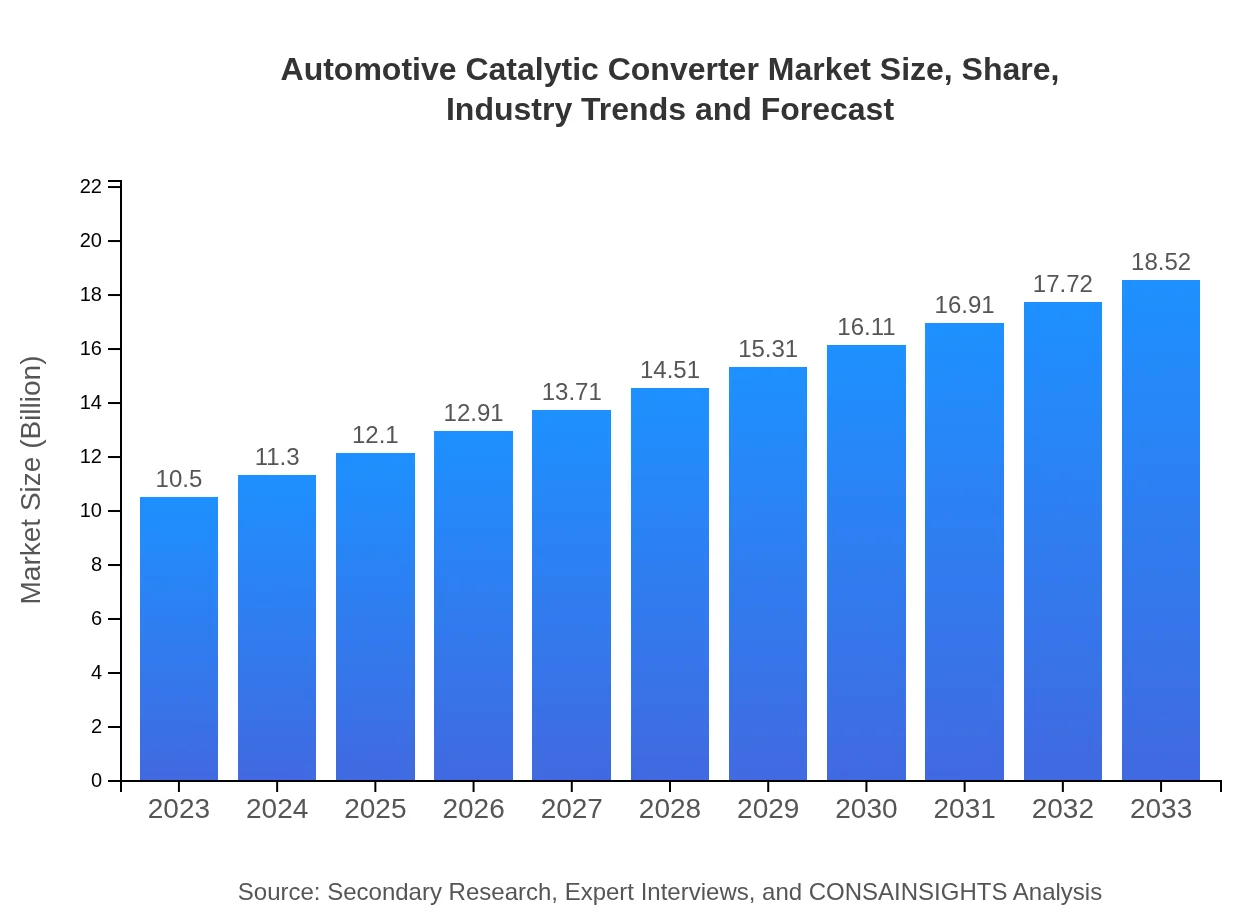

Automotive Catalytic Converter Market Size, Share, Industry Trends and Forecast to 2033

This report provides a comprehensive analysis of the Automotive Catalytic Converter market from 2023 to 2033, covering market size, growth trends, segmentation, and analysis by region. It includes insights into leading market players and future market forecasts.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $10.50 Billion |

| CAGR (2023-2033) | 5.7% |

| 2033 Market Size | $18.52 Billion |

| Top Companies | BASF, Umicore, Johnson Matthey, Friedrichshafen Ag |

| Last Modified Date | 22 January 2026 |

Automotive Catalytic Converter Market Overview

Customize Automotive Catalytic Converter Market Report market research report

- ✔ Get in-depth analysis of Automotive Catalytic Converter market size, growth, and forecasts.

- ✔ Understand Automotive Catalytic Converter's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Automotive Catalytic Converter

What is the Market Size & CAGR of Automotive Catalytic Converter market in 2023?

Automotive Catalytic Converter Industry Analysis

Automotive Catalytic Converter Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Automotive Catalytic Converter Market Analysis Report by Region

Europe Automotive Catalytic Converter Market Report:

Europe’s market for automotive catalytic converters was valued at USD 2.59 billion in 2023, with expectations to climb to USD 4.56 billion by 2033. The EU’s aggressive emissions targets and the transition toward electric vehicles are key growth drivers.Asia Pacific Automotive Catalytic Converter Market Report:

In the Asia Pacific region, the market value was estimated at USD 2.17 billion in 2023 and is projected to reach USD 3.82 billion by 2033. The growth is attributed to rising car production in countries like China and India, coupled with significant investments in reducing automotive emissions.North America Automotive Catalytic Converter Market Report:

North America is a substantial market, expected to increase from USD 3.99 billion in 2023 to USD 7.03 billion by 2033. Stringent regulatory standards in the U.S. and Canada regarding carbon emissions are driving this growth.South America Automotive Catalytic Converter Market Report:

The South American market, valued at USD 0.75 billion in 2023, is set to grow to USD 1.32 billion by 2033. Initiatives toward improving air quality and a rise in automobile usage make this region a potential growth area.Middle East & Africa Automotive Catalytic Converter Market Report:

The Middle East and Africa market stood at USD 1.01 billion in 2023 and is forecasted to grow to USD 1.79 billion by 2033, aided by increasing vehicle counts and improved emissions regulations.Tell us your focus area and get a customized research report.

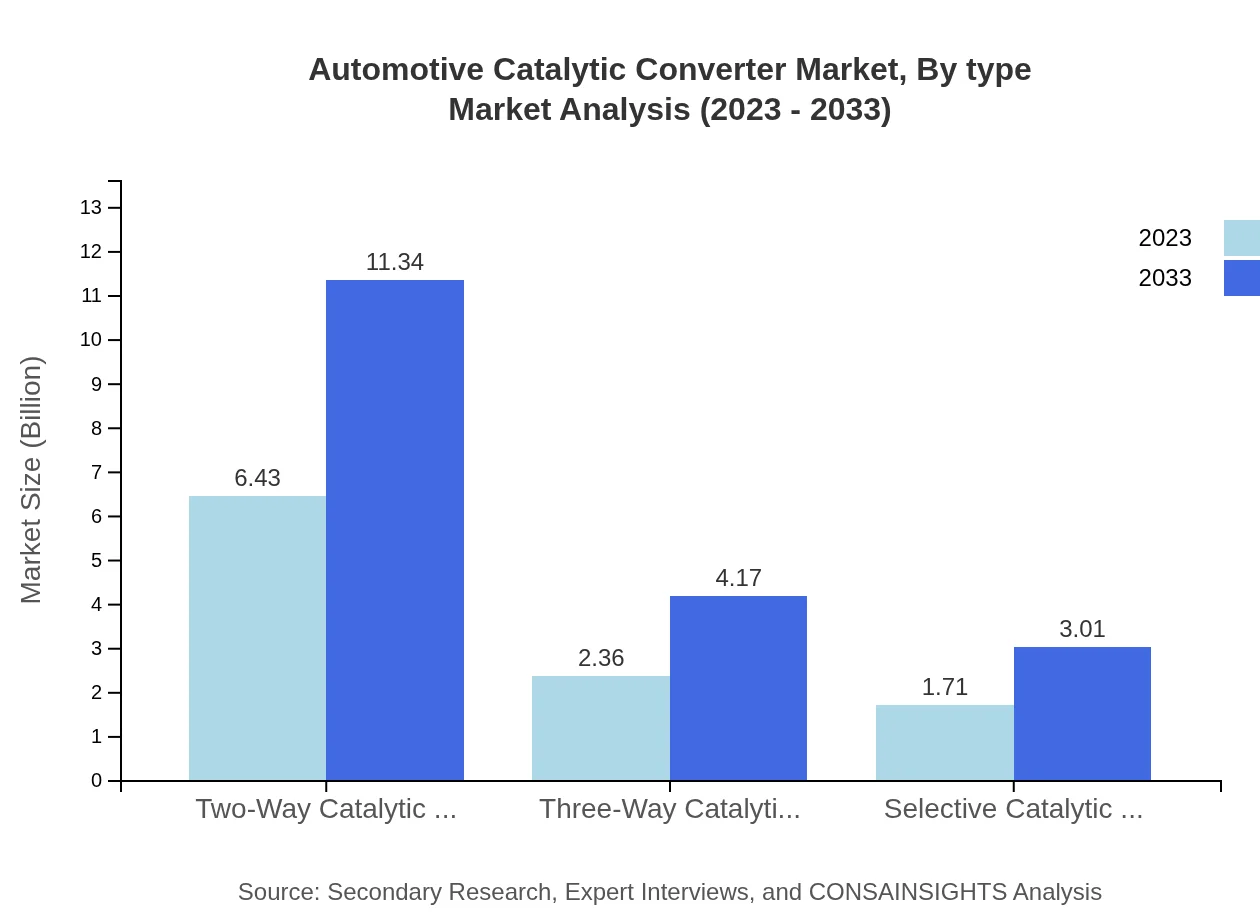

Automotive Catalytic Converter Market Analysis By Type

The market by type reveals a significant share for Two-Way Catalytic Converters, with values projected at USD 6.43 billion in 2023, expanding to USD 11.34 billion by 2033. Three-Way Catalytic Converters are also noteworthy with expected growth from USD 2.36 billion to USD 4.17 billion. Selective Catalytic Reduction (SCR) converters, comprising a key environmental technology, are forecasted to increase from USD 1.71 billion to USD 3.01 billion within the same period.

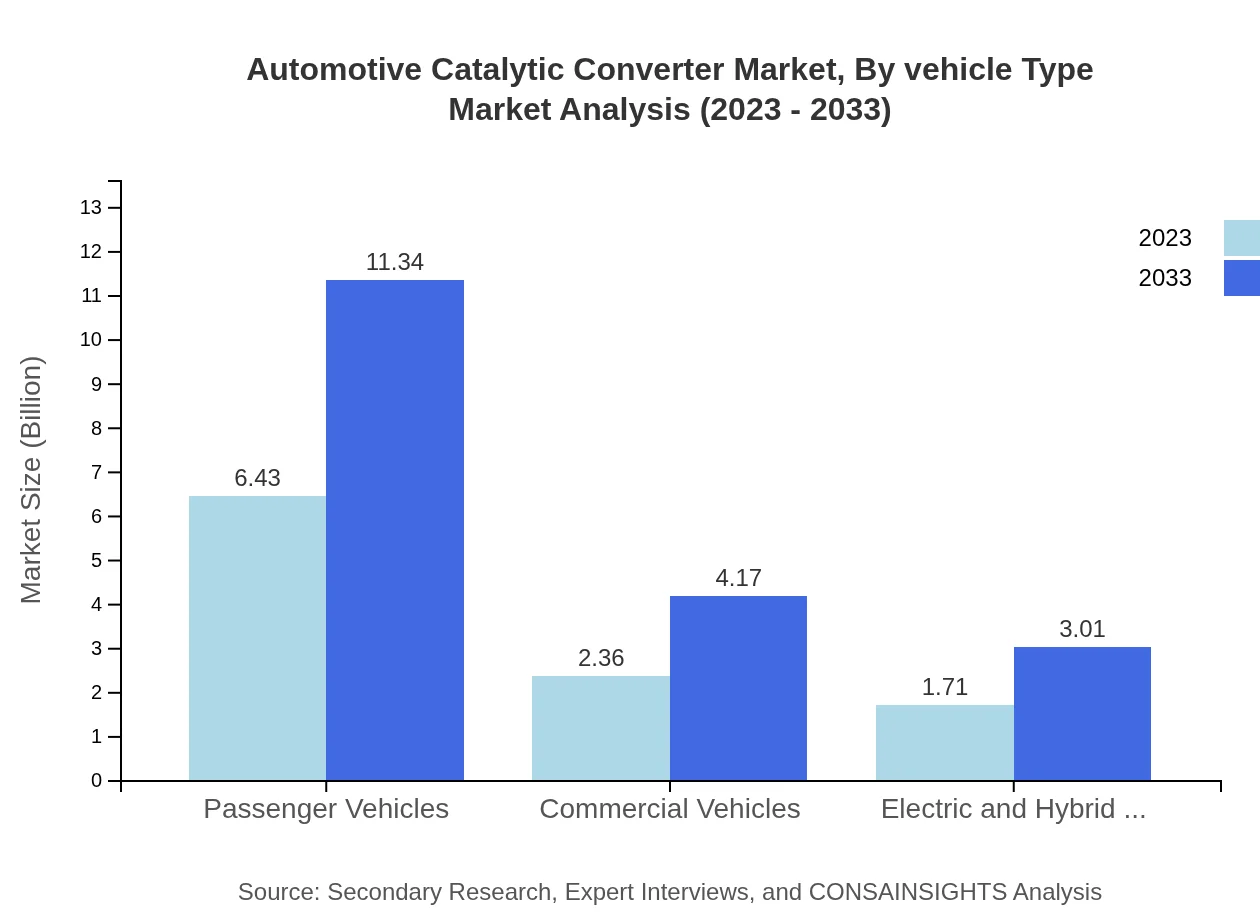

Automotive Catalytic Converter Market Analysis By Vehicle Type

Passenger Vehicles dominate the market with a share expected to remain steady at 61.24%, equating to USD 6.43 billion in 2023, growing to USD 11.34 billion by 2033. Commercial Vehicles are projected to move from USD 2.36 billion to USD 4.17 billion and Electric and Hybrid Vehicles from USD 1.71 billion to USD 3.01 billion, reflecting the shifting focus toward environmentally friendly transportation.

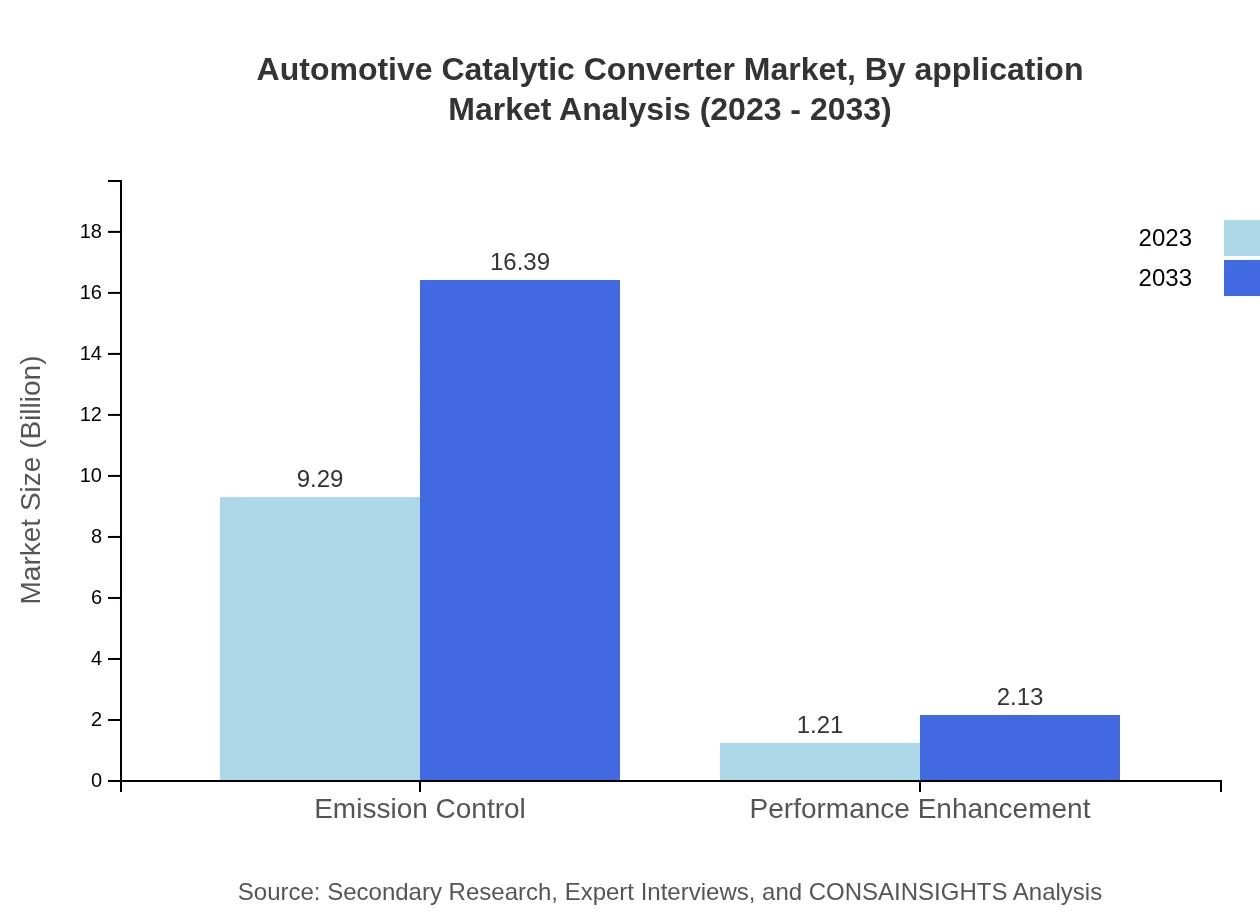

Automotive Catalytic Converter Market Analysis By Application

Key applications include Emission Control, expected to hold an 88.48% market share, translating to USD 9.29 billion in 2023 and growing to USD 16.39 billion by 2033. Performance Enhancement applications currently hold an 11.52% share, with growth driven by advancements in engine technologies and consumer demands for higher performance.

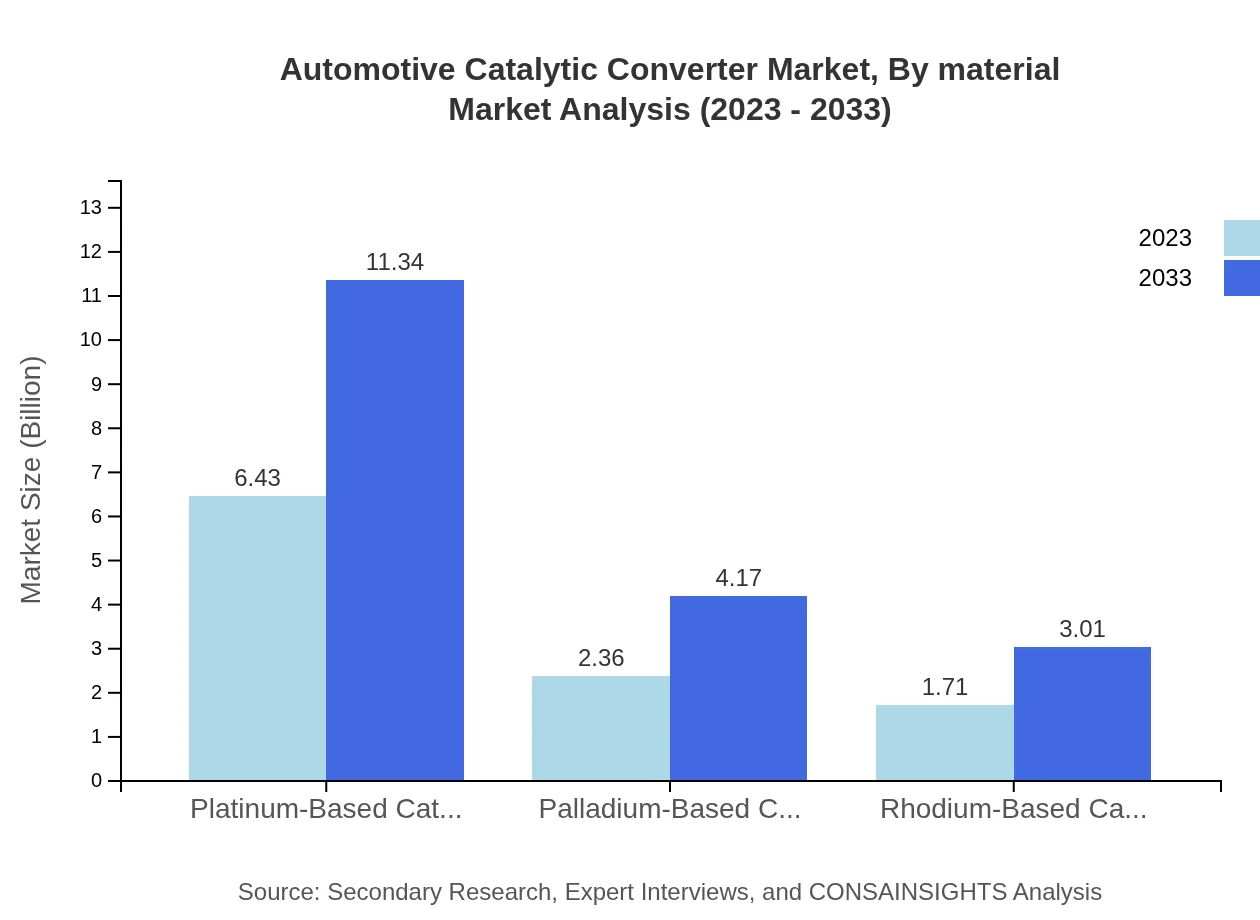

Automotive Catalytic Converter Market Analysis By Material

The market by material highlights Platinum-Based Catalytic Converters leading with a share of 61.24%, showing expected growth from USD 6.43 billion to USD 11.34 billion, while Palladium and Rhodium-based converters also contribute significantly, reflecting trends in cost and availability of noble metals needed for manufacturing.

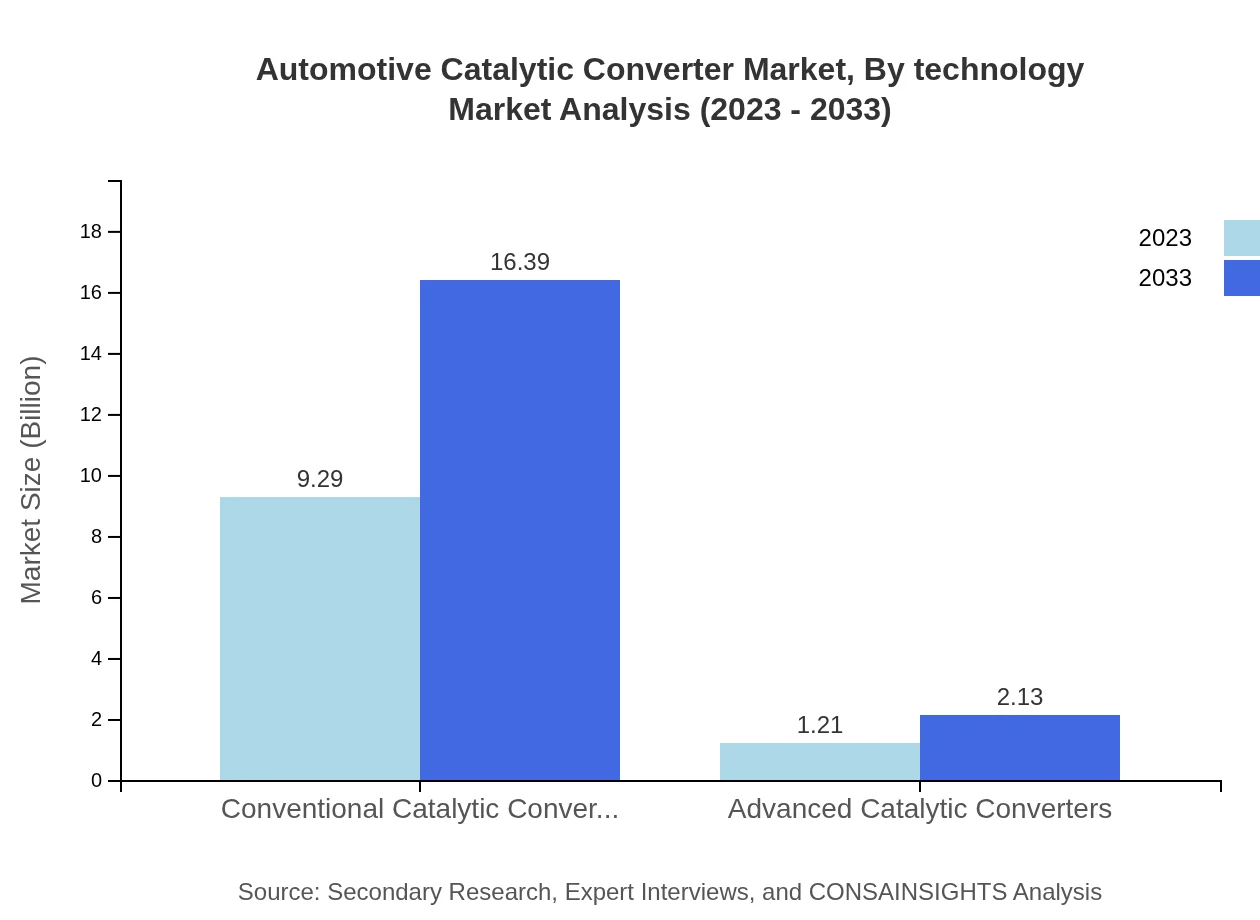

Automotive Catalytic Converter Market Analysis By Technology

Conventional Catalytic Converters represent a significant segment at an expected USD 9.29 billion in 2023, equating to an 88.48% share, while Advanced Catalytic Converters are projected to grow from USD 1.21 billion to USD 2.13 billion, highlighting an industry trend towards enhancing efficiency through advanced technology.

Automotive Catalytic Converter Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Automotive Catalytic Converter Industry

BASF:

A major contributor to the automotive catalyst market, BASF is known for innovative technologies that improve emissions reduction performance.Umicore:

Umicore specializes in material technology and plays a vital role in catalyst development, particularly in optimizing precious metal usage.Johnson Matthey:

Johnson Matthey is a global leader in sustainable technologies, providing a comprehensive portfolio of catalytic solutions that meet stringent emission regulations.Friedrichshafen Ag:

Important in the automotive sector, Friedrichshafen focuses on systems that enhance catalytic efficiency and vehicle performance.We're grateful to work with incredible clients.

FAQs

What is the market size of the automotive catalytic converter industry?

The automotive catalytic converter market is valued at approximately $10.5 billion in 2023, with a projected CAGR of 5.7% affecting its growth until 2033. This indicates a significant expansion and growing demand in the industry.

What are the key market players or companies in the automotive catalytic converter industry?

Major players in the automotive catalytic converter industry include companies like Johnson Matthey, BASF SE, and Eberspaecher. These companies are renowned for their innovative solutions and market-leading positions, significantly influencing industry trends and standards.

What are the primary factors driving the growth in the automotive catalytic converter industry?

Key growth factors include stringent emission regulations, increased vehicle production rates, and rising environmental concerns. The push for cleaner technologies and rising demand for fuel efficiency are also critical contributors to market expansion.

Which region is the fastest Growing in the automotive catalytic converter market?

North America is the fastest-growing region in the automotive catalytic converter market, projected to grow from $3.99 billion in 2023 to $7.03 billion by 2033. This growth is driven by regulatory support for emissions reduction and technological advancements.

Does ConsaInsights provide customized market report data for the automotive catalytic converter industry?

Yes, ConsaInsights offers customized market report data tailored to client specifications in the automotive catalytic converter sector. Clients can expect detailed insights reflecting their unique needs, competitive landscape, and market dynamics.

What deliverables can I expect from this automotive catalytic converter market research project?

Deliverables include comprehensive reports featuring market size forecasts, growth trends, regional analyses, competitive landscape overviews, and segment performance. Detailed actionable insights will support strategic decision-making for stakeholders.

What are the market trends of the automotive catalytic converter industry?

Market trends include a shift towards advanced catalytic converter technologies, increasing adoption in electric and hybrid vehicles, and growing initiatives for recycling catalytic materials. Emphasis on sustainability and tougher regulations will dominate the sector in coming years.