Reports >

Life Sciences

>

Bone Densitometer Devices Market Report

Bone Densitometer Devices Market Report

Published Date: 31 January 2026 | Report Code: bone-densitometer-devices

Bone Densitometer Devices Market Size, Share, Industry Trends and Forecast to 2033

This report provides an in-depth analysis of the Bone Densitometer Devices market from 2023 to 2033, covering market size, growth projections, and key trends affecting the industry. It offers insights into segments, regional performance, and leading market players.

| Metric | Value |

|---|---|

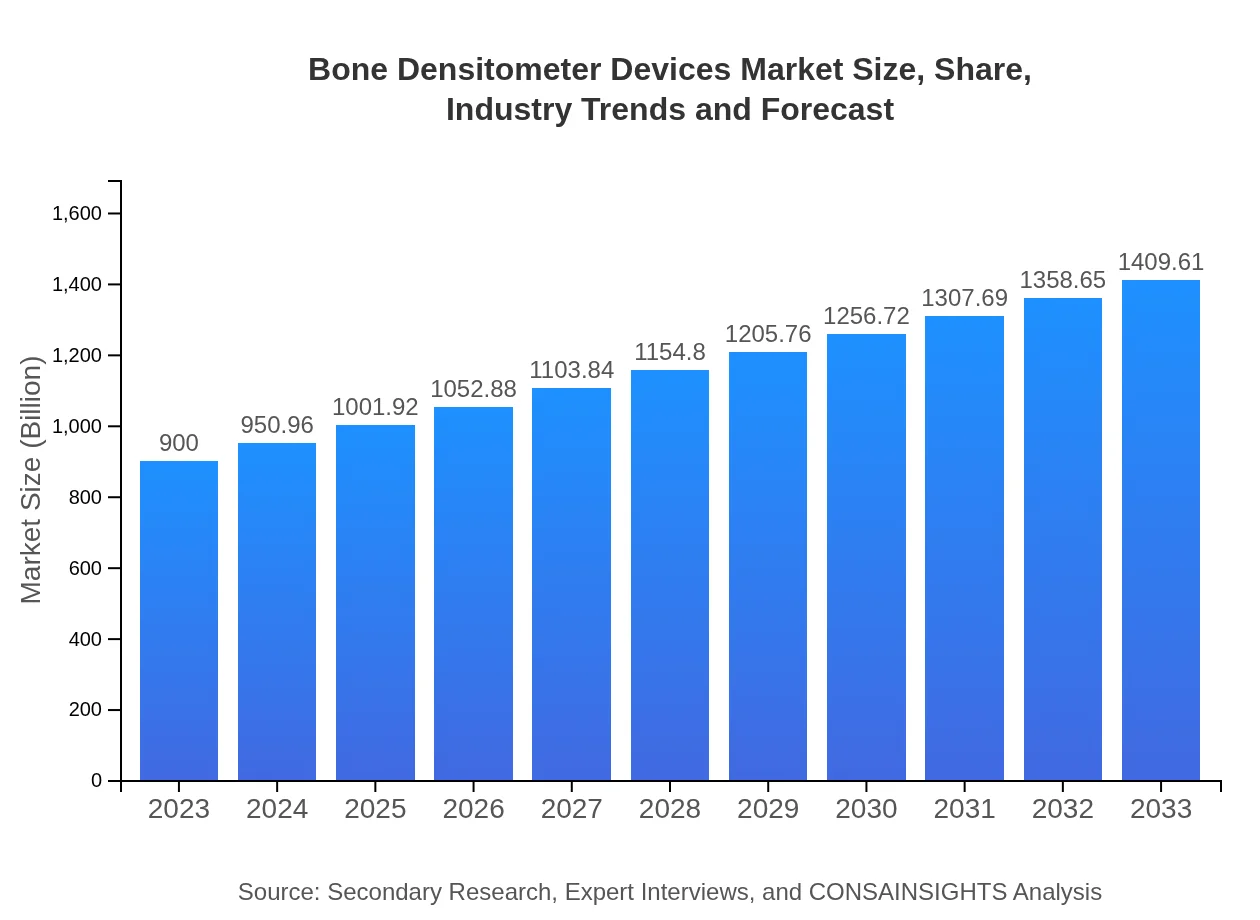

| Study Period | 2023 - 2033 |

| 2023 Market Size | $900.00 Million |

| CAGR (2023-2033) | 4.5% |

| 2033 Market Size | $1409.61 Million |

| Top Companies | Hologic, Inc., GE Healthcare, Siemens Healthineers, Phillips Healthcare |

| Last Modified Date | 31 January 2026 |

Bone Densitometer Devices Market Overview

Customize Bone Densitometer Devices Market Report market research report

- ✔ Get in-depth analysis of Bone Densitometer Devices market size, growth, and forecasts.

- ✔ Understand Bone Densitometer Devices's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Bone Densitometer Devices

What is the Market Size & CAGR of Bone Densitometer Devices market in 2023 and 2033?

Bone Densitometer Devices Industry Analysis

Bone Densitometer Devices Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Bone Densitometer Devices Market Analysis Report by Region

Europe Bone Densitometer Devices Market Report:

The European market is projected to grow from $240.48 million in 2023 to $376.65 million by 2033. The rise in geriatric populations and government healthcare spending on diagnostic tools enhances market potential.Asia Pacific Bone Densitometer Devices Market Report:

The Asia Pacific region is expected to witness substantial growth, with the market size projected to expand from $192.42 million in 2023 to $301.37 million in 2033. Factors contributing to this growth include rising healthcare expenditure, an aging population, and increasing awareness about bone health.North America Bone Densitometer Devices Market Report:

North America holds a significant share of the market, with a forecasted increase from $330.39 million in 2023 to $517.47 million by 2033. The factors supporting growth include advanced healthcare technologies and a high prevalence of osteoporosis.South America Bone Densitometer Devices Market Report:

In South America, the Bone Densitometer Devices market is anticipated to grow from $14.40 million in 2023 to $22.55 million by 2033. Market growth is driven by improving healthcare infrastructure and government initiatives aimed at enhancing medical diagnostics.Middle East & Africa Bone Densitometer Devices Market Report:

The Middle East and Africa market is expected to expand from $122.31 million in 2023 to $191.57 million by 2033. Boosts in healthcare investments and awareness are crucial factors fueling market growth in this region.Tell us your focus area and get a customized research report.

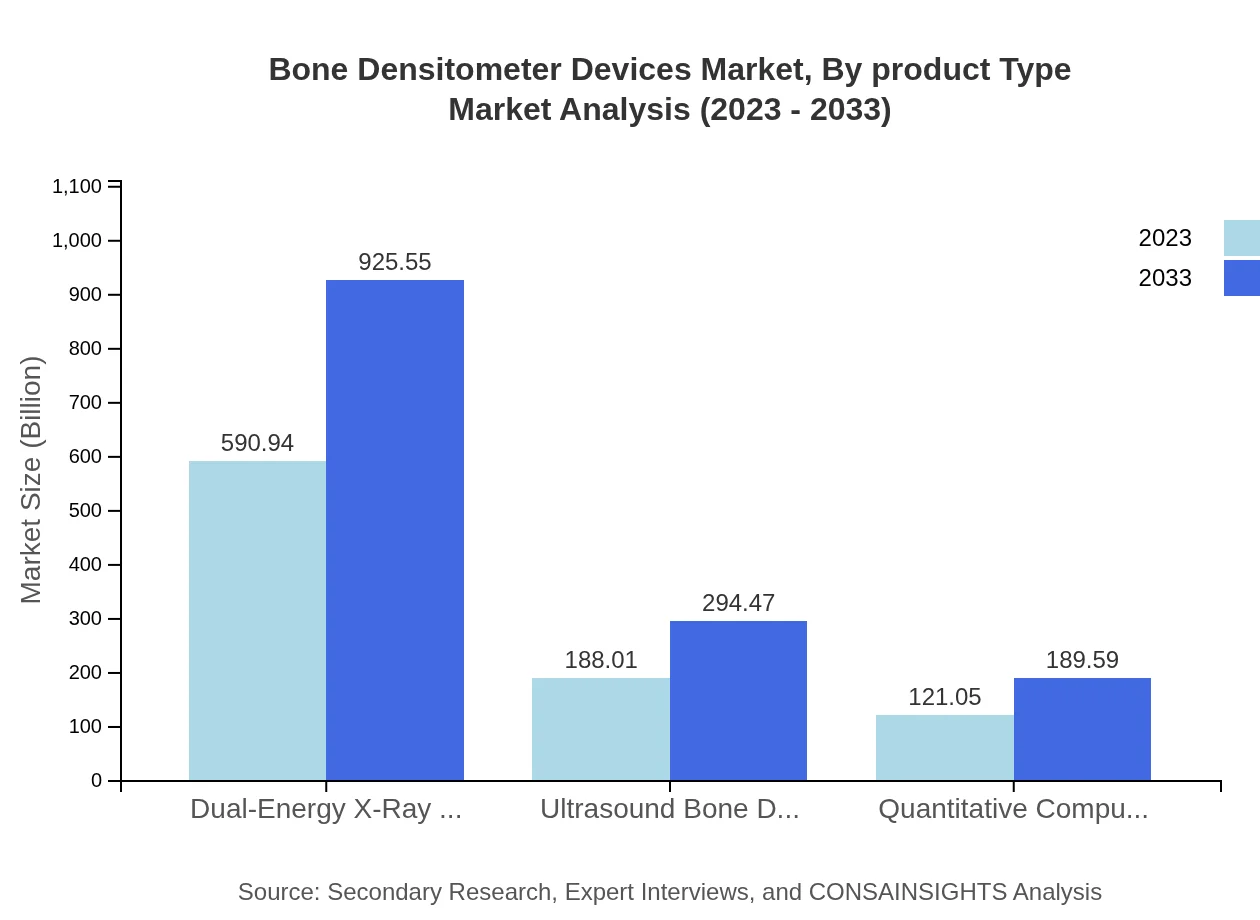

Bone Densitometer Devices Market Analysis By Product Type

The market is led by Dual-Energy X-Ray Absorptiometry (DEXA), generating $590.94 million in 2023, projected to reach $925.55 million by 2033, dominating the segment at 65.66%. Ultrasound Bone Densitometers and Quantitative Computed Tomography (QCT) follow, with respective market sizes of $188.01 million and $121.05 million in 2023.

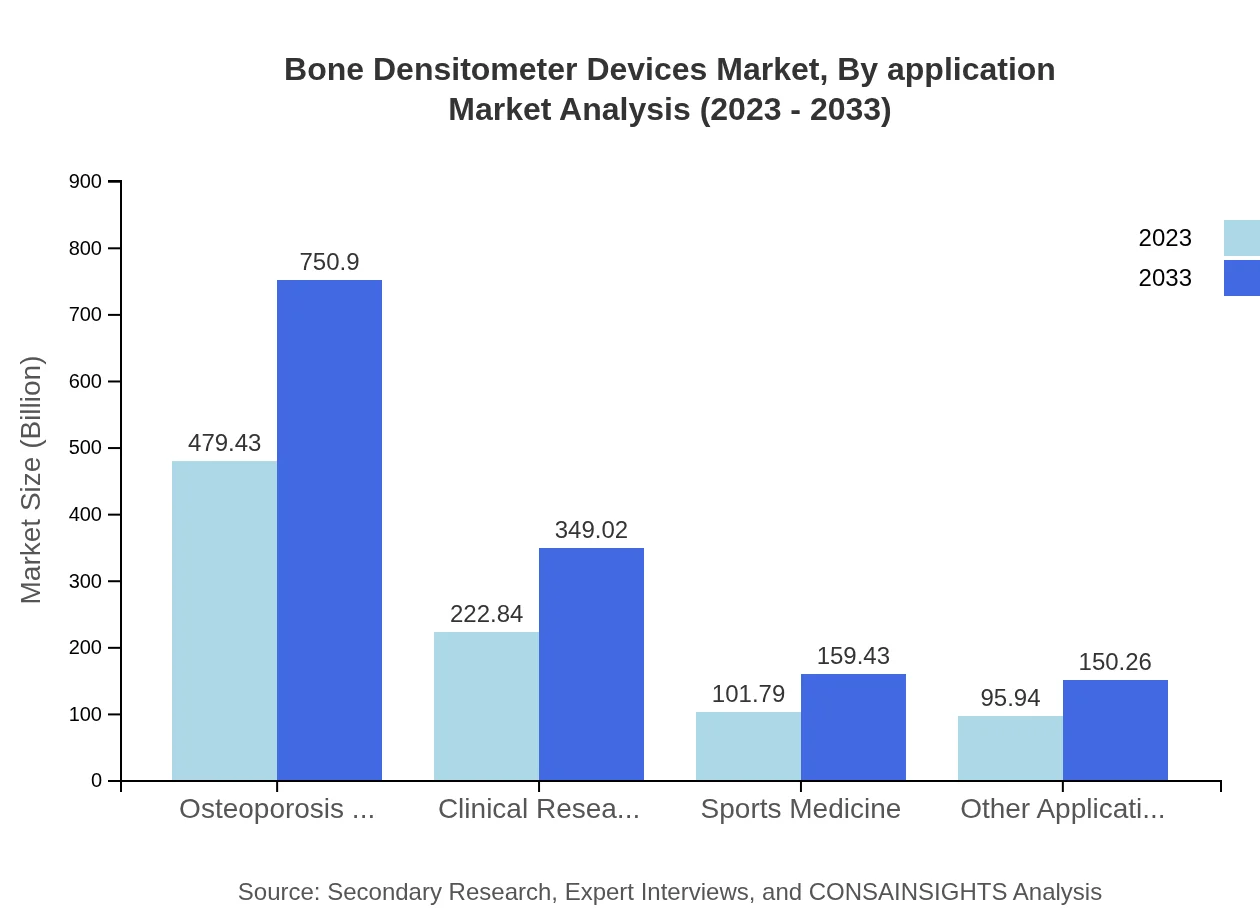

Bone Densitometer Devices Market Analysis By Application

Osteoporosis Diagnosis and Clinical Research applications are crucial, each representing substantial market shares of 53.27% and 24.76% respectively. Their market values are projected to increase from $479.43 million and $222.84 million in 2023 to $750.90 million and $349.02 million in 2033.

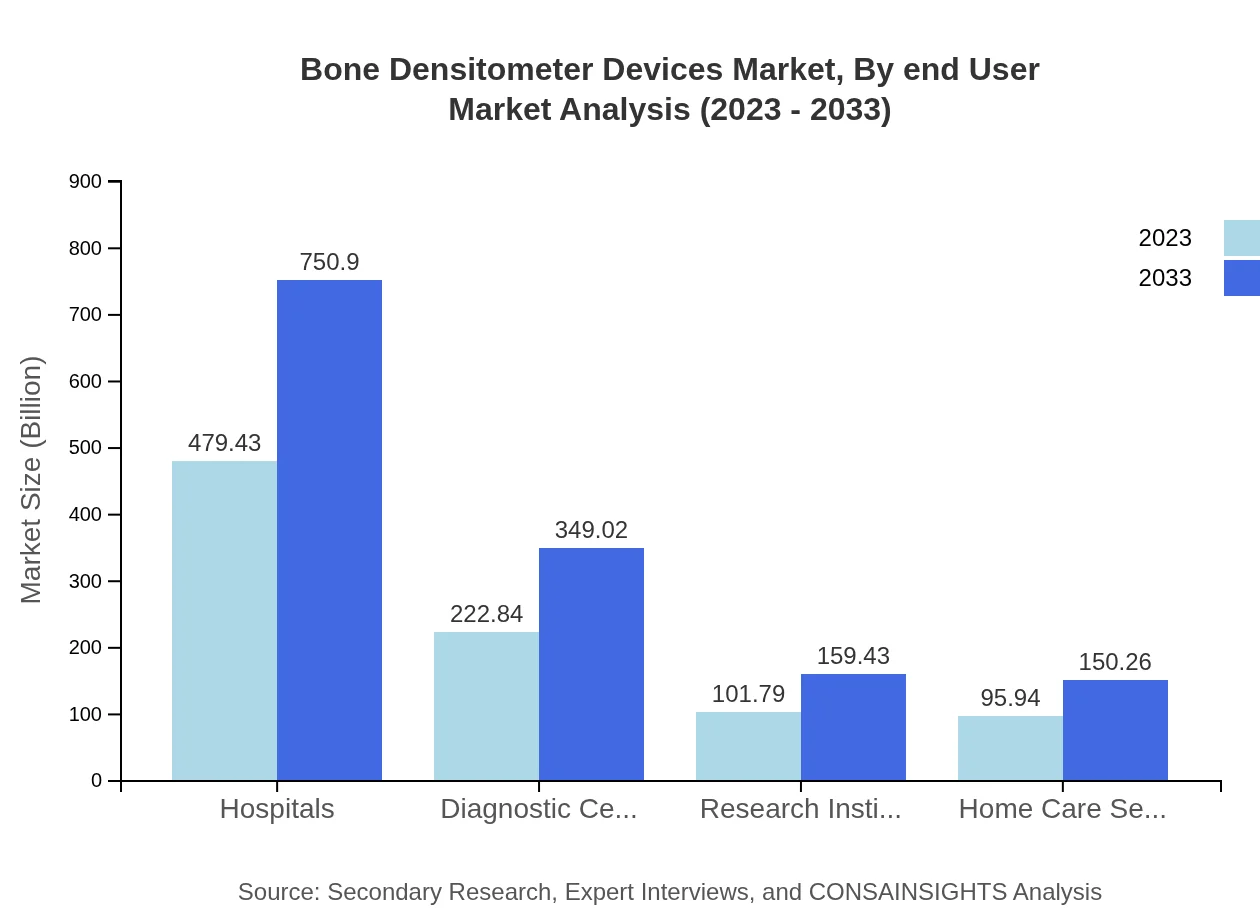

Bone Densitometer Devices Market Analysis By End User

Hospitals make up the majority share of the market at 53.27%, with a market size rising from $479.43 million in 2023 to $750.90 million by 2033. Diagnostic Centers and Research Institutes follow with shares of 24.76% and 11.31% respectively.

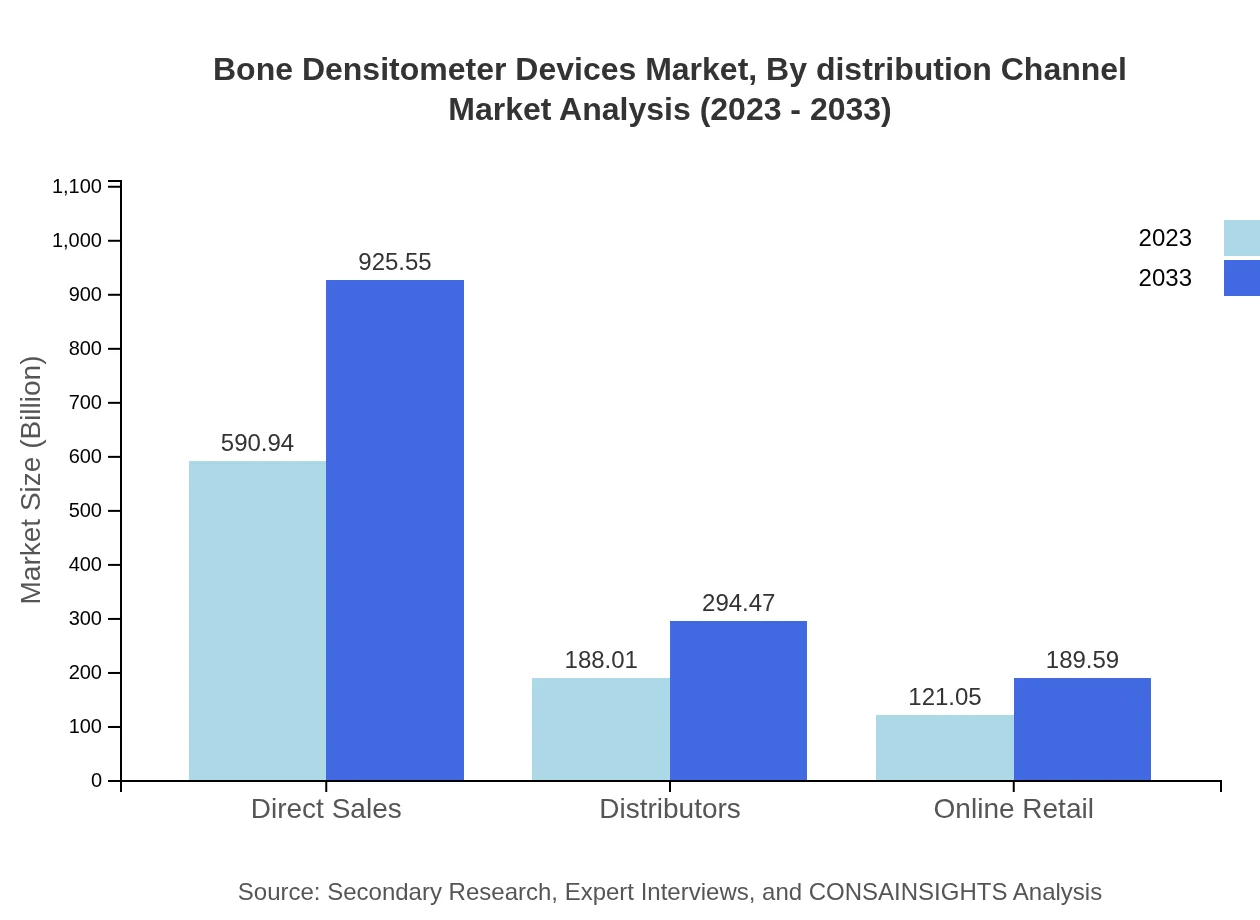

Bone Densitometer Devices Market Analysis By Distribution Channel

Direct Sales segments significantly impact the market, accounting for 65.66% in 2023, growing from $590.94 million to $925.55 million by 2033. Other channels include Distributors and Online Retailers, contributing growing segments to the overall market structure.

Bone Densitometer Devices Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Bone Densitometer Devices Industry

Hologic, Inc.:

A leading manufacturer of medical devices, Hologic specializes in women’s health and offers advanced bone densitometry devices, renowned for their innovative and accurate imaging technologies.GE Healthcare:

GE Healthcare provides a wide range of healthcare solutions, including high-quality bone densitometers that are integral for diagnosing and managing osteoporosis and other bone diseases.Siemens Healthineers:

Siemens Healthineers offers state-of-the-art imaging solutions, including bone densitometry devices known for their precision and integration in comprehensive health assessments.Phillips Healthcare:

Phillips Healthcare is a prominent player in medical technology, focusing on advanced imaging techniques, including bone densitometers for accurate bone density evaluation.We're grateful to work with incredible clients.

FAQs

What is the market size of bone Densitometer Devices?

The global market size for bone densitometer devices is projected to reach approximately $900 million by 2033, expanding at a CAGR of 4.5% from its current valuation.

What are the key market players or companies in the bone Densitometer Devices industry?

Key players include notable medical technology companies, although specific names and market shares require detailed market analysis typically conducted by firms like ConsaInsights.

What are the primary factors driving the growth in the bone Densitometer Devices industry?

Growth is driven by factors such as the increasing prevalence of osteoporosis, advancements in technology, and rising age demographics globally, prompting a higher need for bone density screening.

Which region is the fastest Growing in the bone Densitometer Devices market?

The fastest-growing region in the bone densitometer devices market is Asia Pacific, projected to grow from $192.42 million in 2023 to $301.37 million by 2033.

Does ConsaInsights provide customized market report data for the bone Densitometer Devices industry?

Yes, ConsaInsights offers customized market reports tailored to specific requirements, allowing clients to obtain in-depth insights and data pertinent to the bone densitometer devices market.

What deliverables can I expect from this bone Densitometer Devices market research project?

Expect comprehensive reports that include market analysis, participant profiling, trend exploration, future forecasts, and segmented data for various applications and regions.

What are the market trends of bone Densitometer Devices?

Market trends indicate a shift towards more advanced imaging technology and portable devices, increasing focus on preventative healthcare along with a growing geriatric population that boosts the demand for bone-density assessments.