Cancer Registry Software Market Report

Published Date: 31 January 2026 | Report Code: cancer-registry-software

Cancer Registry Software Market Size, Share, Industry Trends and Forecast to 2033

This report provides an in-depth analysis of the Cancer Registry Software market from 2023 to 2033, covering market size, growth trends, regional insights, competitive landscape, and emerging technologies that are shaping the industry.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

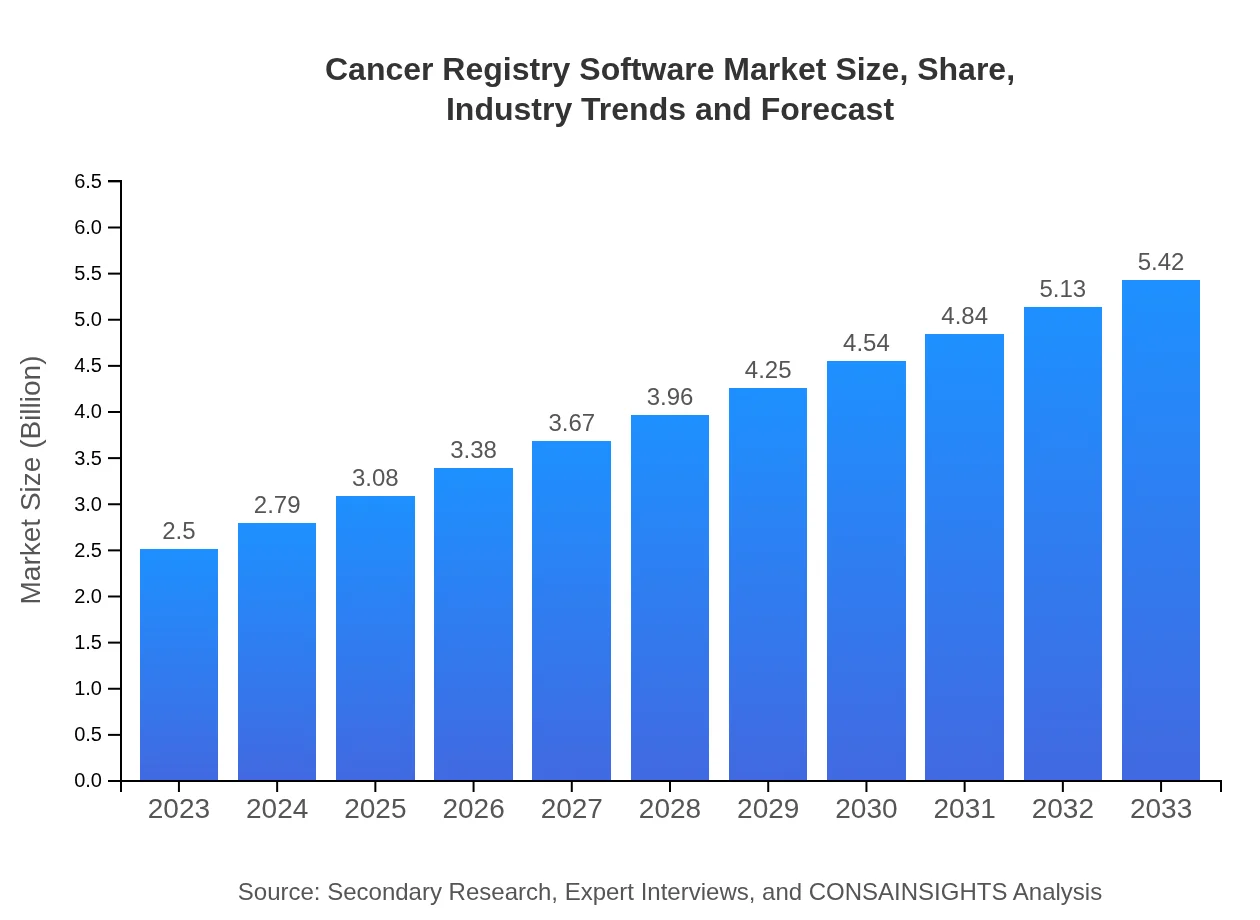

| 2023 Market Size | $2.50 Billion |

| CAGR (2023-2033) | 7.8% |

| 2033 Market Size | $5.42 Billion |

| Top Companies | Cerner Corporation, McKesson Corporation, Epic Systems Corporation, IBM Watson Health, Allscripts Healthcare Solutions |

| Last Modified Date | 31 January 2026 |

Cancer Registry Software Market Overview

Customize Cancer Registry Software Market Report market research report

- ✔ Get in-depth analysis of Cancer Registry Software market size, growth, and forecasts.

- ✔ Understand Cancer Registry Software's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Cancer Registry Software

What is the Market Size & CAGR of Cancer Registry Software market in 2023?

Cancer Registry Software Industry Analysis

Cancer Registry Software Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Cancer Registry Software Market Analysis Report by Region

Europe Cancer Registry Software Market Report:

The European market is expected to grow from $0.67 billion in 2023 to $1.45 billion by 2033. This growth is driven by stringent regulations on healthcare data management and the increased need for systematic cancer reporting.Asia Pacific Cancer Registry Software Market Report:

In the Asia Pacific region, the Cancer Registry Software market is estimated at $0.50 billion in 2023 and is expected to grow to $1.08 billion by 2033. Driven by increasing healthcare investments and rising cancer incidences, countries like India and China are emphasizing technology adoption in healthcare.North America Cancer Registry Software Market Report:

North America leads the market with a value of $0.91 billion in 2023, anticipated to reach $1.98 billion by 2033. The robust healthcare infrastructure and early adoption of advanced healthcare technologies are key factors influencing market growth.South America Cancer Registry Software Market Report:

The South American market for Cancer Registry Software is valued at $0.20 billion in 2023, projected to grow to $0.44 billion by 2033. The growth is supported by governmental health initiatives aimed at improving cancer care and data collection.Middle East & Africa Cancer Registry Software Market Report:

The Middle East and Africa market is relatively smaller, starting at $0.21 billion in 2023 and expected to reach $0.46 billion by 2033. Growth is anticipated as countries focus on developing their healthcare systems and improving cancer datasets.Tell us your focus area and get a customized research report.

Cancer Registry Software Market Analysis By Product

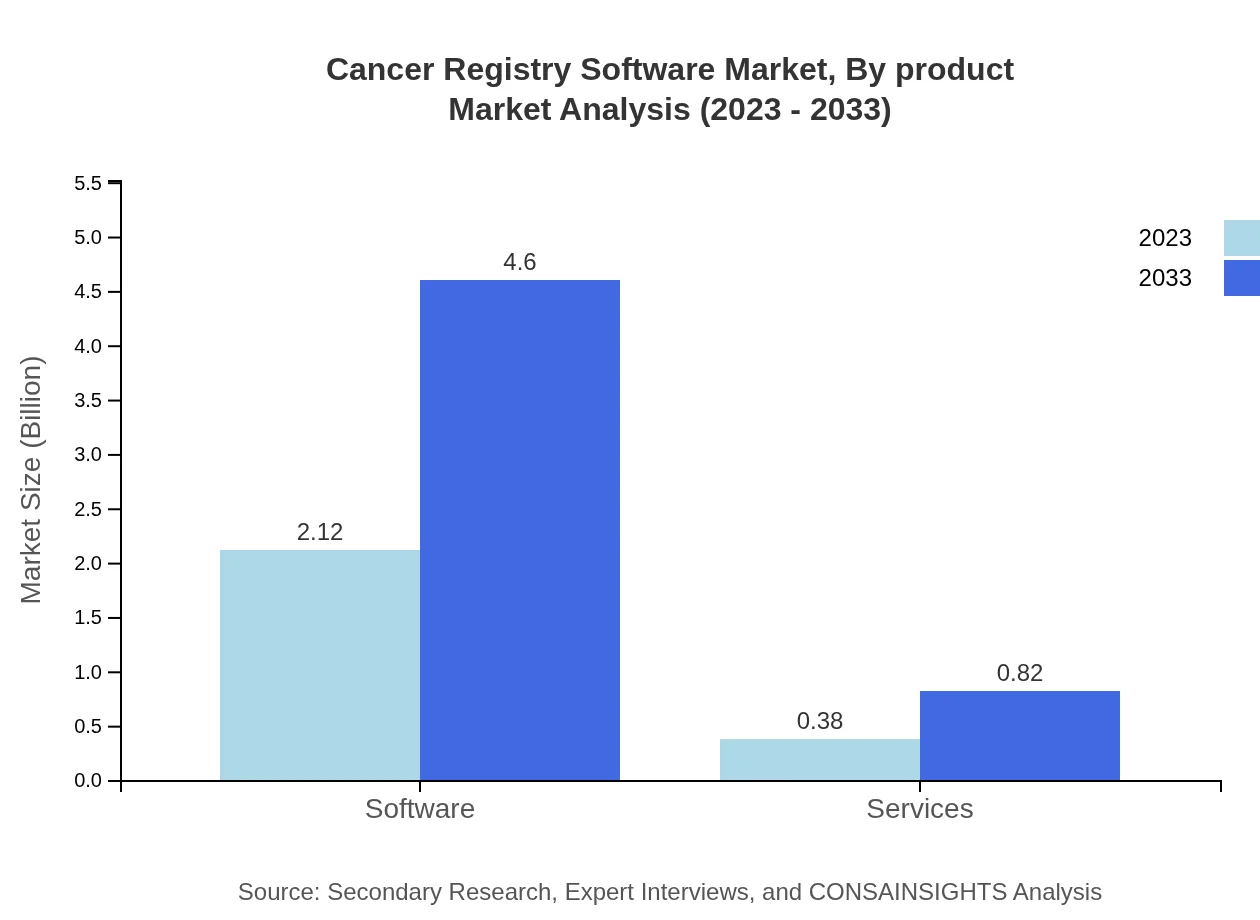

The Cancer Registry Software market is predominantly categorized into software solutions and services. The software segment is leading the market with a size of $2.12 billion in 2023, projected to grow to $4.60 billion by 2033, consistently holding an 84.79% market share. In contrast, the services segment, valued at $0.38 billion in 2023, is expected to see growth to $0.82 billion by 2033, corresponding to a market share of 15.21%.

Cancer Registry Software Market Analysis By Application

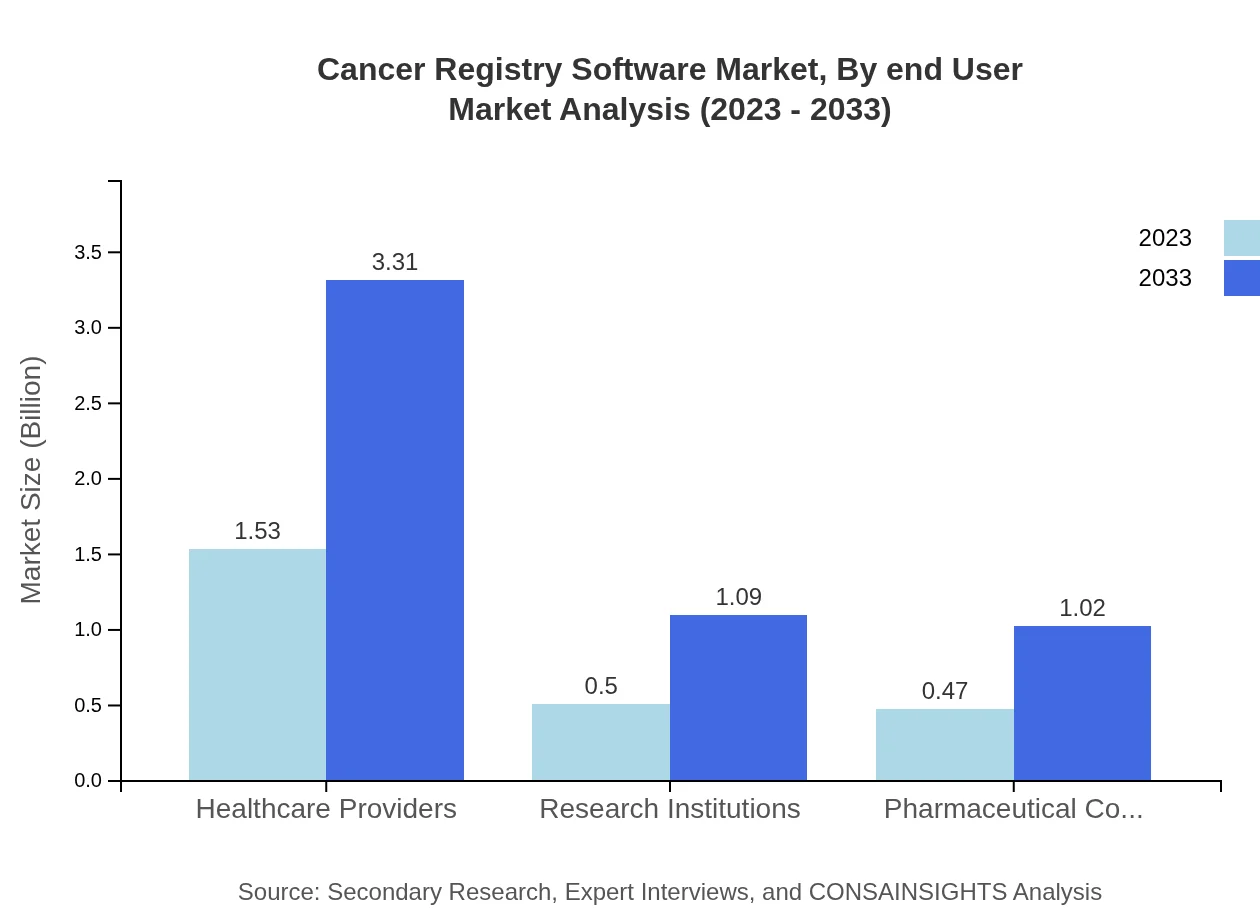

The market is segmented by application into healthcare providers, research institutions, pharmaceutical companies, and government agencies. The healthcare providers segment holds the largest share, valued at $1.53 billion in 2023 and expected to grow to $3.31 billion by 2033, representing 61.02% of the market. Research institutions and pharmaceutical companies also contribute significantly, with sizes of $0.50 billion and $0.47 billion in 2023, respectively.

Cancer Registry Software Market Analysis By End User

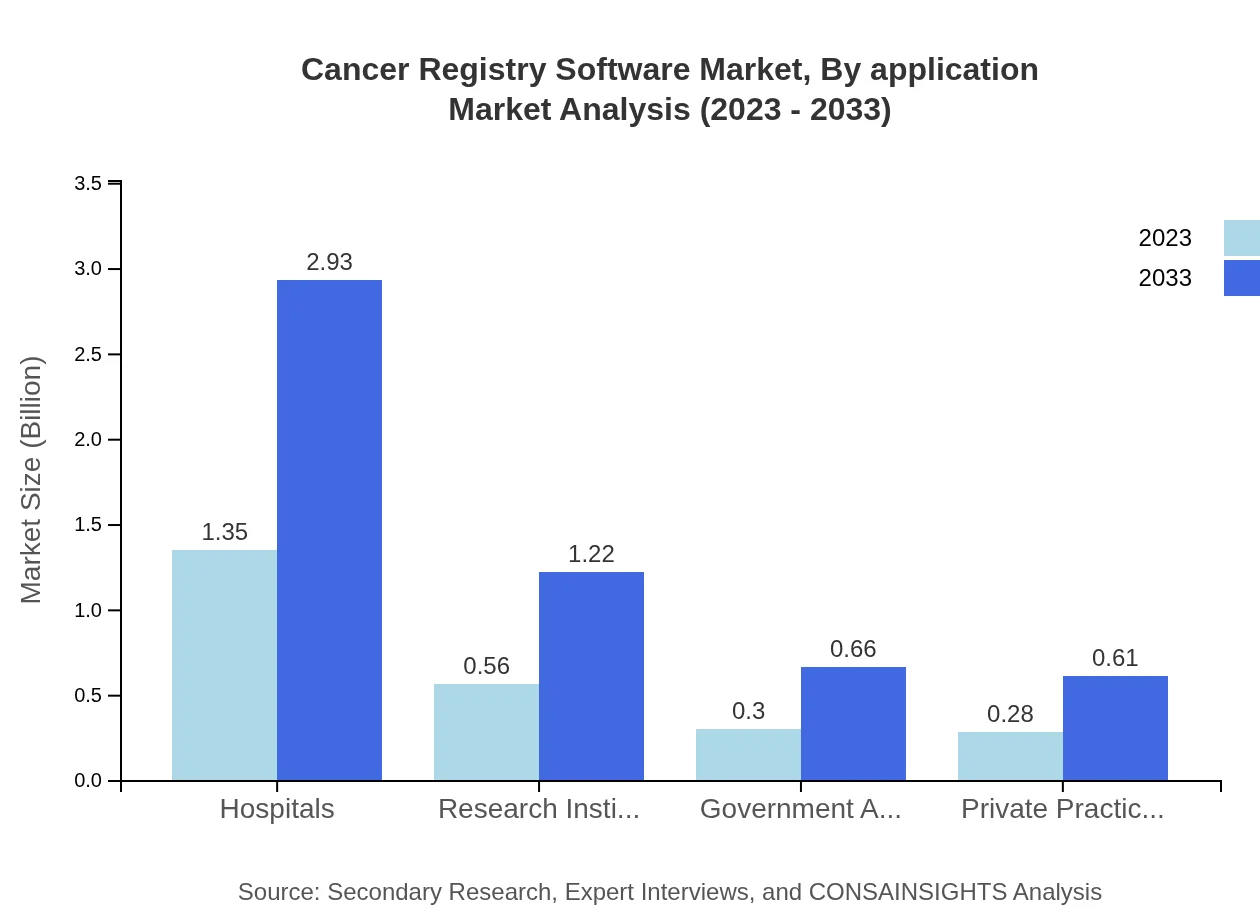

End-users of the Cancer Registry Software include hospitals, research institutes, government agencies, and private practices. Hospitals lead with a market size of $1.35 billion in 2023, projected to grow to $2.93 billion by 2033, accounting for 54.14% of the market share. Research institutes are also key players, with market sizes anticipated to grow from $0.56 billion to $1.22 billion in the same period.

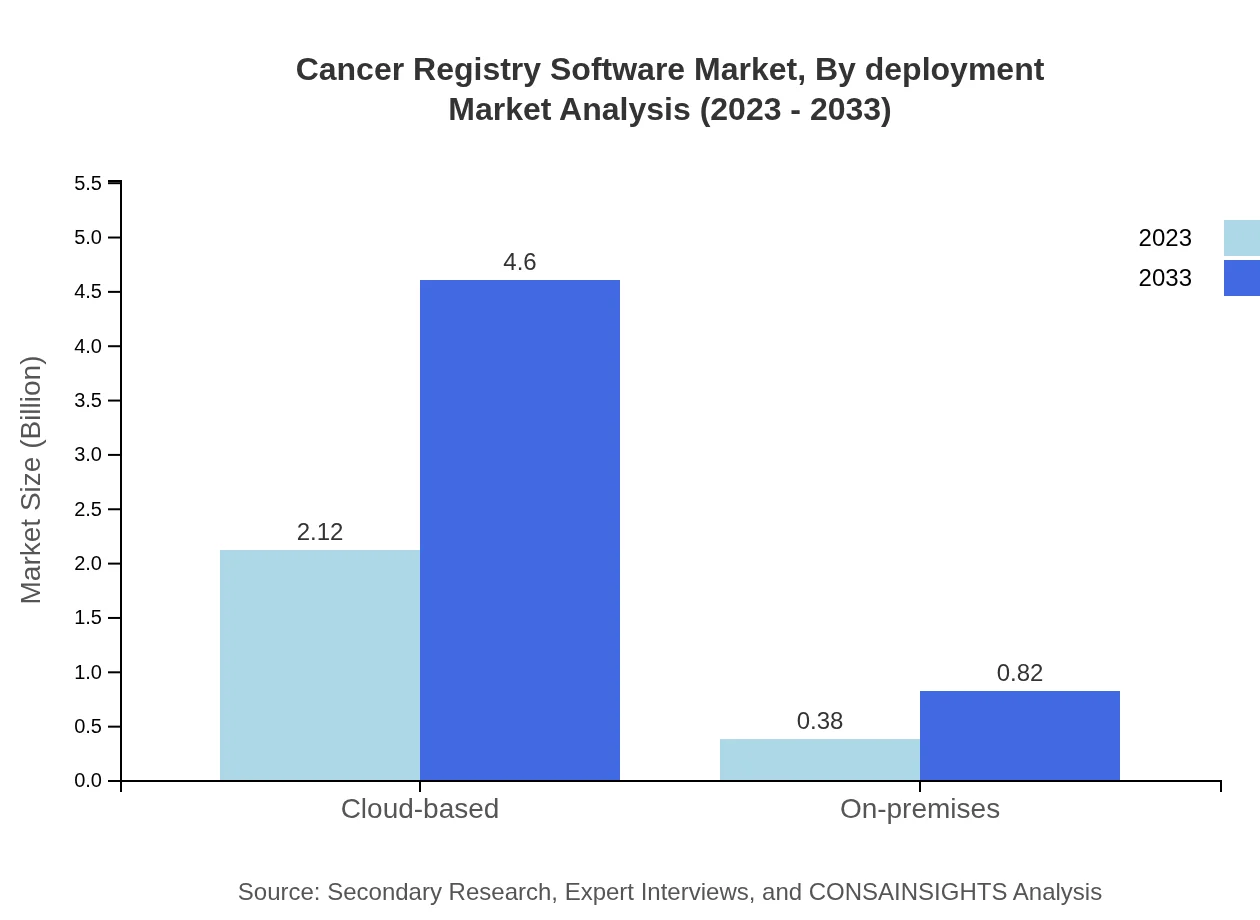

Cancer Registry Software Market Analysis By Deployment

In terms of deployment, the Cancer Registry Software market is categorized into cloud-based and on-premises solutions. The cloud-based segment leads the market, valued at $2.12 billion in 2023 and expected to grow to $4.60 billion by 2033, holding 84.79% of the market share. Meanwhile, on-premises solutions start at $0.38 billion and are forecasted to reach $0.82 billion, holding a 15.21% share.

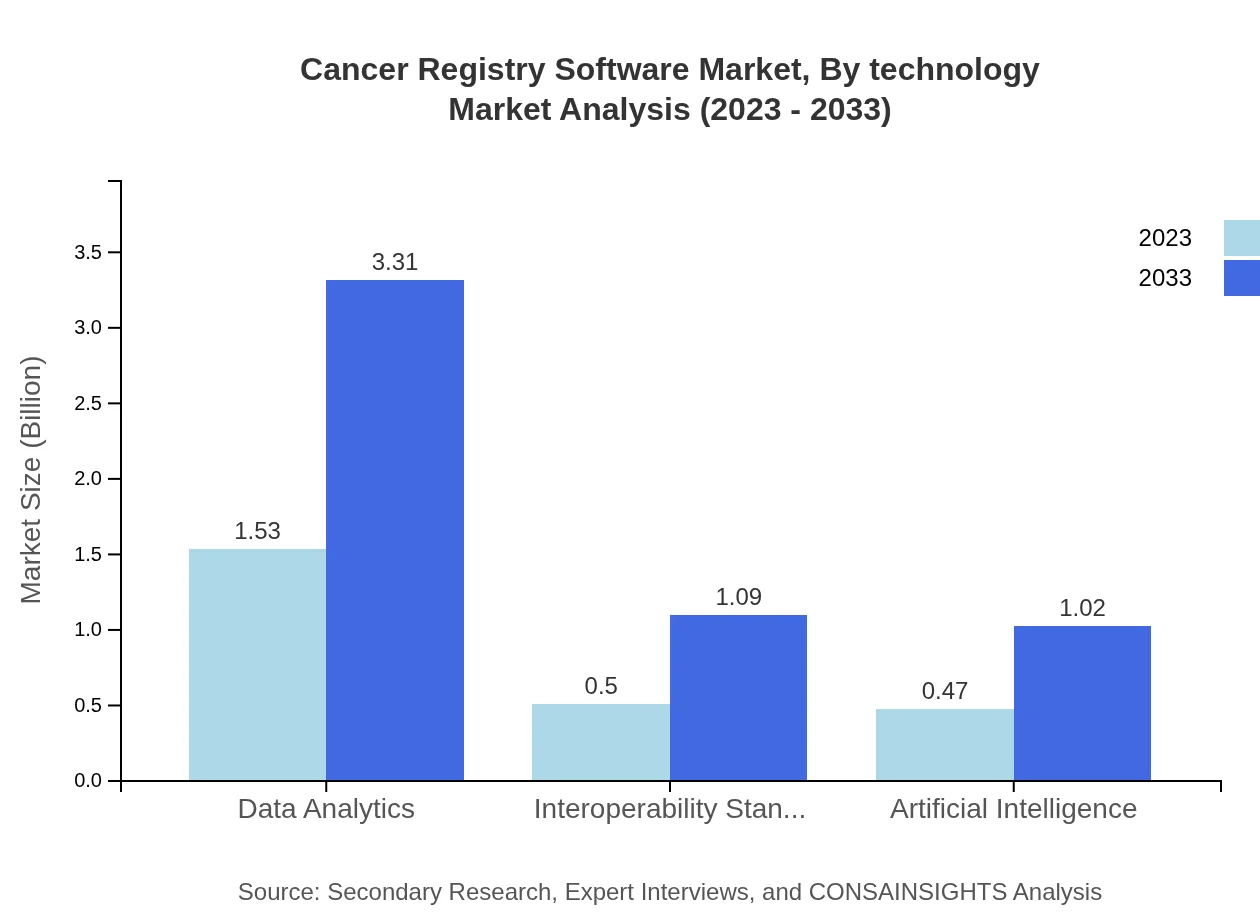

Cancer Registry Software Market Analysis By Technology

The technological advancements in the Cancer Registry Software market are evident in the segments of data analytics, interoperability standards, and artificial intelligence. Data analytics tools are projected to grow from $1.53 billion in 2023 to $3.31 billion by 2033, with a share of 61.02%. Similarly, interoperability standards and AI capabilities are crucial for the integration of cancer registries with other healthcare systems, with projected sizes of $0.50 billion and $0.47 billion respectively by 2033.

Cancer Registry Software Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Cancer Registry Software Industry

Cerner Corporation:

Cerner provides healthcare solutions, including comprehensive cancer registry software that enhances data management and improves patient outcomes.McKesson Corporation:

McKesson offers innovative solutions that streamline cancer data collection and reporting, emphasizing patient safety and treatment efficacy.Epic Systems Corporation:

Epic's software solutions are widely used for managing cancer registries, focusing on ease of access and integration with existing healthcare systems.IBM Watson Health:

IBM Watson Health utilizes AI-driven analytics to enhance the insights gained from cancer registries, supporting healthcare providers in delivering optimal patient care.Allscripts Healthcare Solutions:

Allscripts delivers interoperable cancer registry software that supports data sharing and compliance with health regulations.We're grateful to work with incredible clients.

FAQs

What is the market size of cancer Registry Software?

The global Cancer Registry Software market is valued at approximately $2.5 billion in 2023, with a projected CAGR of 7.8%. By 2033, it is expected to grow significantly, highlighting the increasing demand for cancer data management solutions.

What are the key market players or companies in this cancer Registry Software industry?

Key players in the Cancer Registry Software industry include leading tech firms specializing in healthcare IT, software developers focusing on data management, and companies providing tailored solutions for healthcare providers and research institutions.

What are the primary factors driving the growth in the cancer Registry Software industry?

The growth in the Cancer Registry Software market is primarily fueled by increasing cancer prevalence, rising emphasis on efficient data management, advancements in technology like AI, and government initiatives promoting cancer research and prevention.

Which region is the fastest Growing in the cancer Registry Software?

In the Cancer Registry Software market, North America shows the fastest growth, expected to rise from $0.91 billion in 2023 to $1.98 billion by 2033. Europe and the Asia Pacific regions also exhibit significant growth potential.

Does ConsaInsights provide customized market report data for the cancer Registry Software industry?

Yes, ConsaInsights offers customized market report data tailored to specific needs within the Cancer Registry Software industry, providing clients with detailed insights that align with their business strategies and market objectives.

What deliverables can I expect from this cancer Registry Software market research project?

From the Cancer Registry Software market research project, you can expect comprehensive reports including market size analysis, growth trends, competitive landscape, regional insights, and detailed segment data to inform decision-making.

What are the market trends of cancer Registry Software?

Current trends in the Cancer Registry Software market include a shift towards cloud-based solutions, integration of data analytics, and enhanced emphasis on interoperability standards, driven by the need for efficient cancer data management and reporting.