Reports >

Life Sciences

>

Cardiac Implants Market Report

Cardiac Implants Market Report

First published: 21 October 2024 | Last updated: 25 May 2026 | Report Code: cardiac-implants

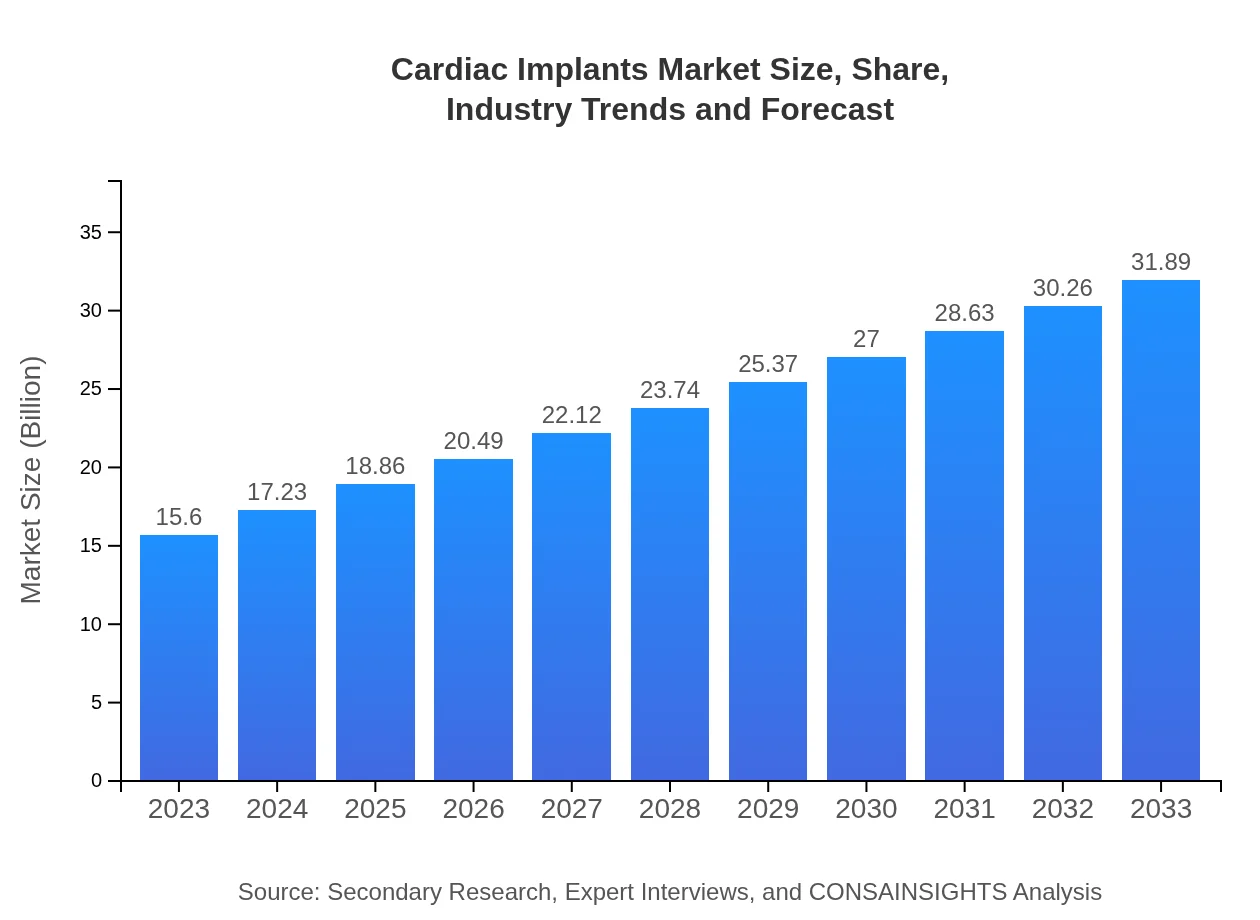

Cardiac Implants Market — USD 15.6 billion in 2023, Growing to USD 31.89B by 2033 at 7.2% CAGR

This report provides an extensive examination of the Cardiac Implants market from 2023 to 2033. It offers insights into market size, growth trends, technology advancements, product performance, and a comprehensive analysis of key regions and players in the industry.

Key Takeaways

- Global market expands from $15.60 Billion in 2023 to $31.89 Billion in 2033, reflecting a 7.2% CAGR over 2023 to 2033.

- North America is largest regional market, while no single fastest-growing region is stated because regional CAGR differences remain within 0.15 percentage points.

- Europe grows from $4.96 Billion in 2023 to $10.15 Billion in 2033, supported by aging populations and advanced healthcare infrastructure.

- Asia Pacific's market rises from $2.86 Billion in 2023 to $5.85 Billion in 2033 amid rising disease prevalence and expanding care access.

- Key product categories include pacemakers, ICDs, stents, and heart valves, with major participants such as Medtronic and Edwards Lifesciences.

Cardiac Implants Market Report — Executive Summary

North America remains largest market by forecast-period value, while no single fastest-growing region is stated because top regional growth rates are separated by less than 0.15 percentage points. The cardiac implants market demonstrates steady expansion driven by demographic shifts, rising incidence of cardiovascular conditions, and technological advancement in device design. Market value increases from $15.60 Billion in 2023 to $31.89 Billion by 2033 at a 7.2% CAGR for 2023 to 2033. Growth is supported by higher healthcare spending, improved diagnostic rates, and investment in minimally invasive procedures. Major segments encompass pacemakers, implantable cardioverter defibrillators (ICDs), stents, and heart valves across hospitals, specialty clinics, and home care settings. Regional dynamics show North America as the largest market, while other regions register notable increases in absolute value. Leading firms such as Medtronic, Abbott Laboratories, Boston Scientific, Johnson & Johnson (DePuy Synthes), and Edwards Lifesciences are central to competitive innovation and market activity. Regulatory approvals, partnerships, and an emphasis on remote monitoring and patient management are key trends influencing adoption and future product development.

Key Growth Drivers

- Aging populations and higher prevalence of cardiac disorders increasing demand for implantable devices.

- Technological improvements in device safety and longevity encouraging broader clinical adoption.

- Rising healthcare expenditure and improved reimbursement frameworks supporting market expansion.

- Greater awareness and diagnostic screening leading to earlier detection and treatment of heart conditions.

- Increased investments and collaborations among established manufacturers and research institutions.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $15.60 Billion |

| CAGR (2023-2033) | 7.2% |

| 2033 Market Size | $31.89 Billion |

| Top Companies | Medtronic , Abbott Laboratories, Boston Scientific, Johnson & Johnson (DePuy Synthes), Edwards Lifesciences |

| Published Date | 21 October 2024 |

| Last Modified Date | 25 May 2026 |

Cardiac Implants Market Overview

Customize Cardiac Implants Market Report market research report

- ✔ Get in-depth analysis of Cardiac Implants market size, growth, and forecasts.

- ✔ Understand Cardiac Implants's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Cardiac Implants

What is the Market Size & CAGR of Cardiac Implants Market Report market in 2023?

Cardiac Implants Industry Analysis

Cardiac Implants Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Cardiac Implants Market Report Market Analysis Report by Region

Europe Cardiac Implants Market Report:

Europe grows from $4.96 Billion in 2023 to $10.15 Billion in 2033. Growth reflects aging populations, well-developed clinical networks, and ongoing investment in medical device innovation and regulatory approvals supporting advanced therapies.Asia Pacific Cardiac Implants Market Report:

Asia Pacific grows from $2.86 Billion in 2023 to $5.85 Billion in 2033. Market progress is linked to expanding access to care, rising cardiovascular disease prevalence, and increasing healthcare expenditure across emerging and developed markets.North America Cardiac Implants Market Report:

North America is largest regional market, rising from $5.5 Billion in 2023 to $11.24 Billion in 2033. Regional expansion is fueled by established healthcare infrastructure, strong reimbursement systems, and early uptake of advanced implantable cardiac therapies.South America Cardiac Implants Market Report:

Latin America grows from $1.51 Billion in 2023 to $3.08 Billion in 2033. Demand is supported by improving healthcare access, greater awareness of cardiovascular conditions, and gradual adoption of implantable device technologies.Middle East & Africa Cardiac Implants Market Report:

Middle East and Africa grows from $0.77 Billion in 2023 to $1.58 Billion in 2033. Growth drivers include improving healthcare infrastructure, increased diagnostic capacity, and rising investments in medical technologies.Tell us your focus area and get a customized research report.

Research Methodology

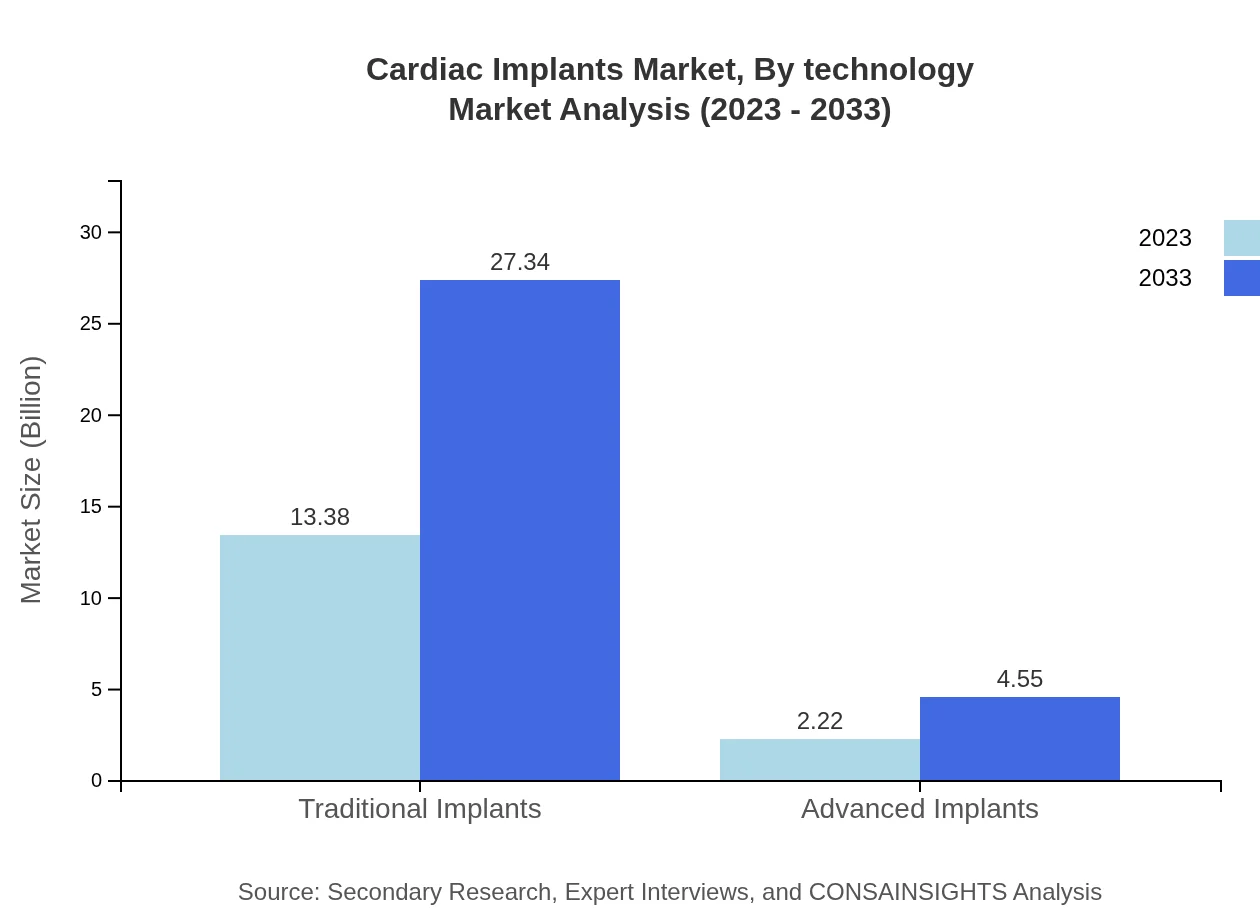

Cardiac Implants Market Analysis By Product Type

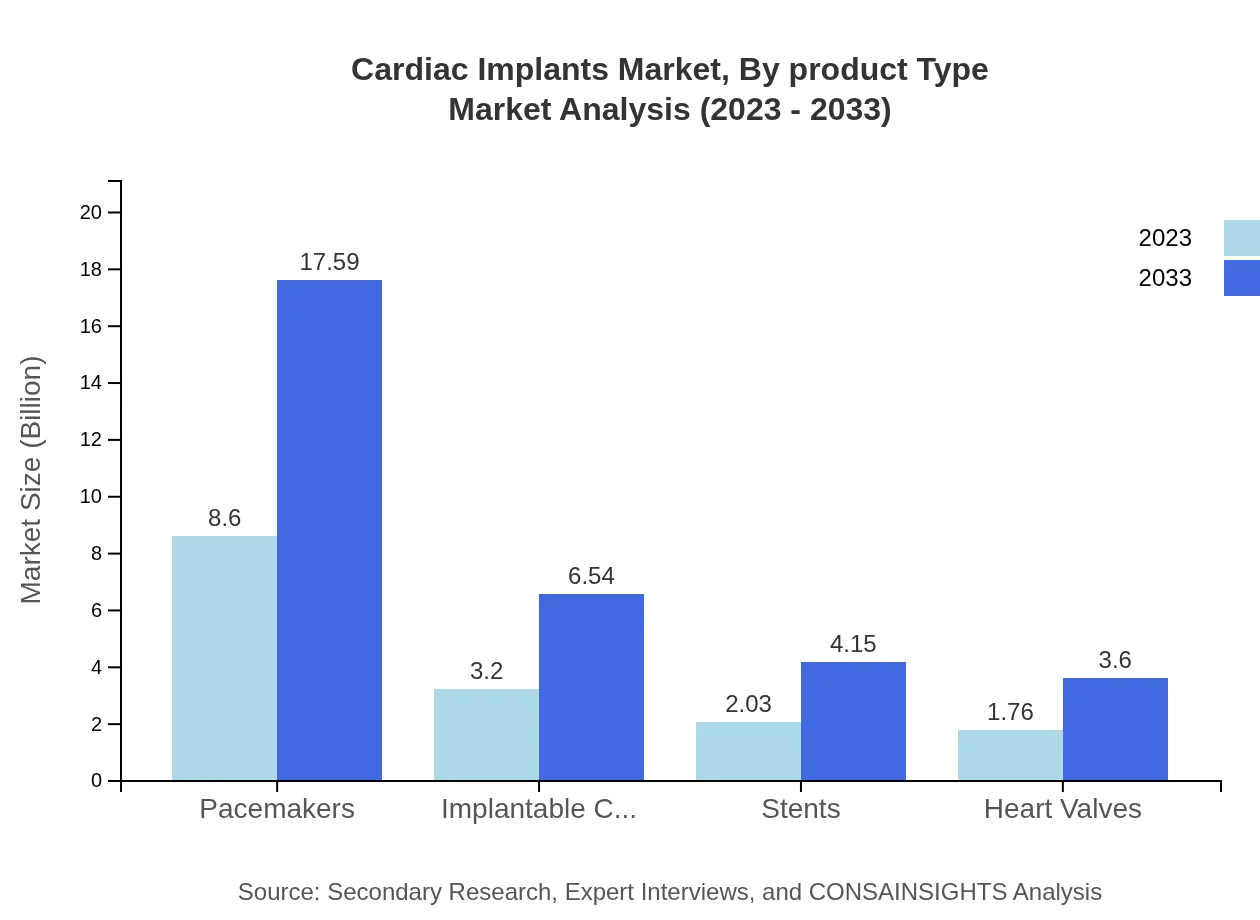

The market exhibits robust growth across various product types: Traditional implants dominate the market, accounting for $13.38 billion, expected to grow to $27.34 billion. Advanced implants are also gaining attention, increasing from $2.22 billion to $4.55 billion by 2033. Pacemakers lead in share with 55.16% in 2023, followed closely by ICDs with 20.52%.

Cardiac Implants Market Analysis By Therapy Type

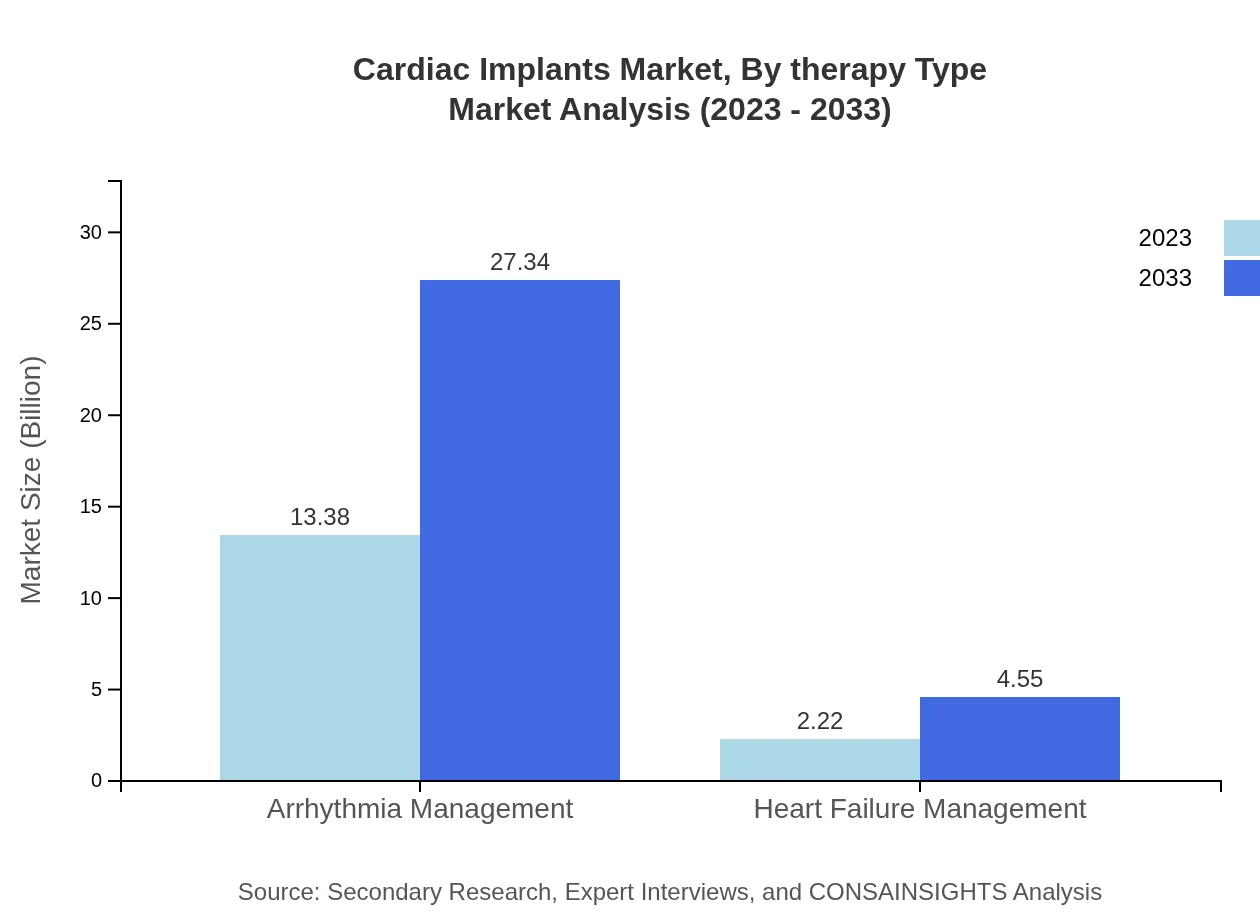

In terms of therapy type, arrhythmia management is a leading segment, commanding a significant share of 85.74% in 2023. This reflects the critical importance of rhythm stability in cardiac health management. Heart failure management also holds relevance, with expectations of growth from $2.22 billion to $4.55 billion through the forecast period.

Cardiac Implants Market Analysis By End User

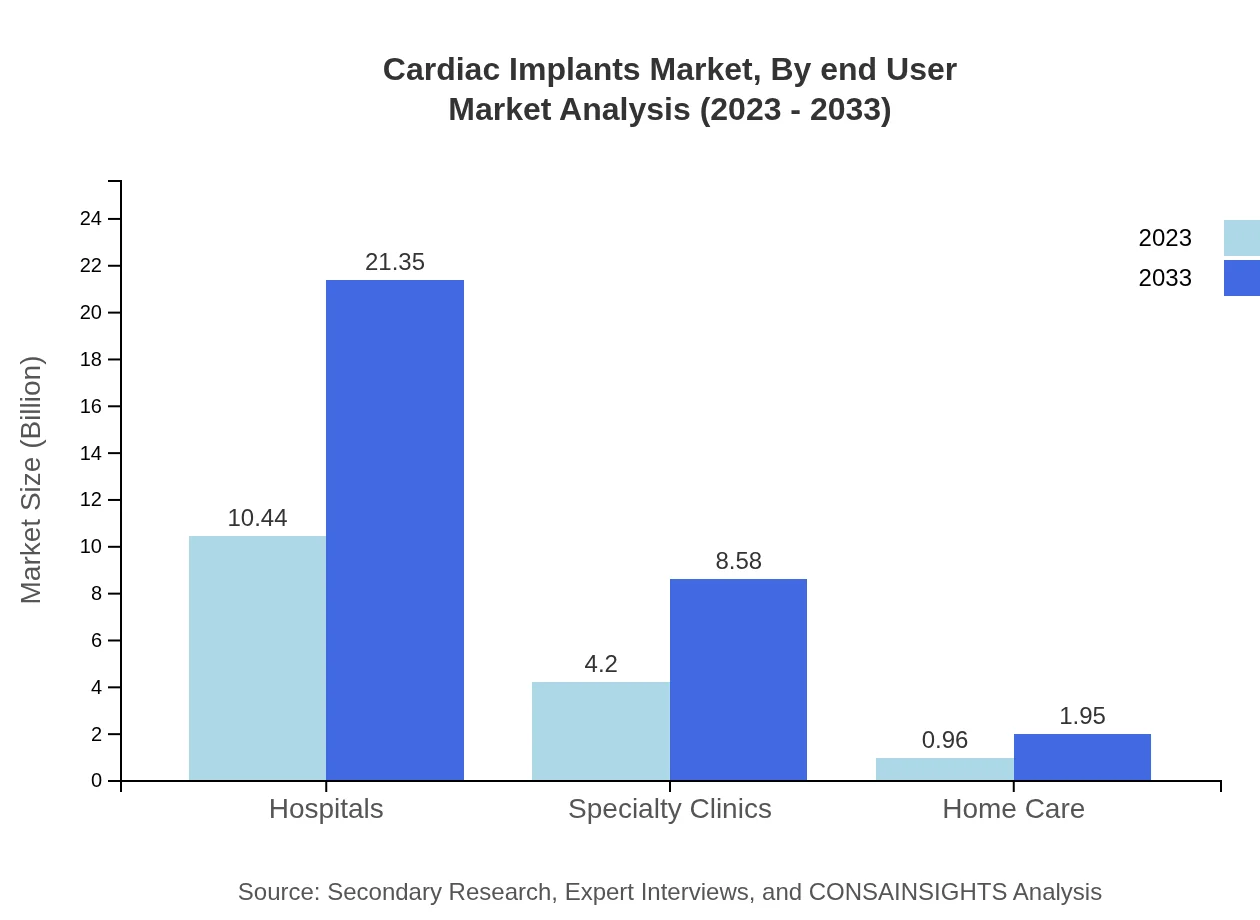

Hospitals remain the primary end-users of cardiac implants, holding a market share of 66.95% in 2023. Specialty clinics and home care segments are growing, indicating shifts towards outpatient services and patient-centered care.

Cardiac Implants Market Analysis By Technology

Technological advancements continue to shape the cardiac implants market, with innovations such as remote monitoring capabilities, minimally invasive procedures, and bioresorbable devices gaining traction. These technologies are enhancing the quality of care and patient compliance.

Cardiac Implants Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Cardiac Implants Industry

Medtronic :

A leader in the cardiac implants market, specializing in a range of devices from pacemakers to advanced heart failure management systems.Abbott Laboratories:

Known for its innovative devices, Abbott continues to advance in the field of cardiovascular care with cutting-edge technologies.Boston Scientific:

Offers a comprehensive portfolio of cardiac devices, focusing on minimally invasive therapeutic solutions.Johnson & Johnson (DePuy Synthes):

A major player in the market, providing various surgical solutions including stents and implantable devices.Edwards Lifesciences:

Specializes in heart valve technology and monitoring solutions, contributing to improved patient outcomes in cardiac care.We're grateful to work with incredible clients.

FAQs

What is the market size of the cardiac implants market in 2023?

The market size for 2023 is $15.60 Billion according to the provided data for the forecast period 2023 to 2033.

How big will the cardiac implants market be in 2033?

By 2033 the market is projected to reach $31.89 Billion, based on the specified forecast figures for 2023 to 2033.

What is CAGR of the cardiac implants market?

The compound annual growth rate (CAGR) is 7.2% for the forecast period 2023 to 2033 as provided in the input data.

Is there a single fastest Growing region in the Cardiac Implants Market Report market?

No single fastest-growing region is stated for the Cardiac Implants Market Report market because the top regional implied CAGR values are within 0.15 percentage points of each other, making the ranking too close to call reliably.

Which companies are leading in the cardiac implants market?

Top companies listed include Medtronic, Abbott Laboratories, Boston Scientific, Johnson & Johnson (DePuy Synthes), and Edwards Lifesciences.

How do product types shape the market?

Product types such as pacemakers, ICDs, stents, and heart valves form core categories that address arrhythmia and heart failure management across care settings.

What are common end users for these devices?

Primary end users include hospitals, specialty clinics, and home care environments, as indicated in the segmentation data.

Why are advancements in monitoring relevant?

Remote patient monitoring and telemedicine improve adherence and follow-up care, supporting wider device utility and integration with clinical workflows.

How is regional growth evaluated in the report?

Regional evaluation uses start and end period market values; North America is identified as the largest region while regional market region is Not specified.

Who contributed to the research methodology?

Research included primary interviews with industry experts, secondary company reports and publications, data triangulation, and expert-led trend analysis.