Cellular Concrete Market Report

Published Date: 22 January 2026 | Report Code: cellular-concrete

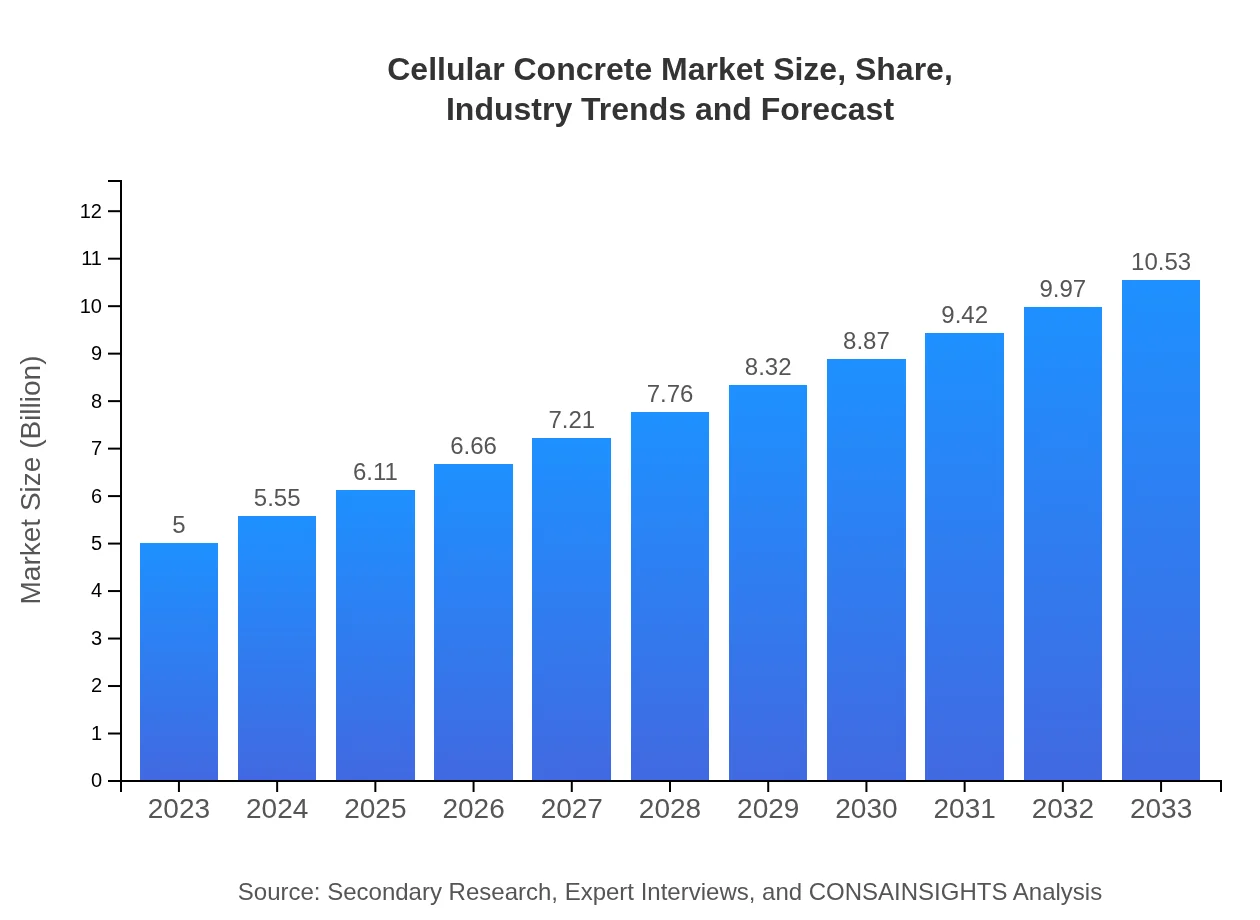

Cellular Concrete Market Size, Share, Industry Trends and Forecast to 2033

This report provides an in-depth analysis of the Cellular Concrete market, focusing on various segments, regional insights, technological advancements, and forecasts from 2023 to 2033.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.00 Billion |

| CAGR (2023-2033) | 7.5% |

| 2033 Market Size | $10.53 Billion |

| Top Companies | Aercon, Xella Group, Hebel, H+H International A/S |

| Last Modified Date | 22 January 2026 |

Cellular Concrete Market Overview

Customize Cellular Concrete Market Report market research report

- ✔ Get in-depth analysis of Cellular Concrete market size, growth, and forecasts.

- ✔ Understand Cellular Concrete's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Cellular Concrete

What is the Market Size & CAGR of Cellular Concrete market in 2023?

Cellular Concrete Industry Analysis

Cellular Concrete Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Cellular Concrete Market Analysis Report by Region

Europe Cellular Concrete Market Report:

The European Cellular Concrete market is projected to grow from $1.52 billion in 2023 to $3.19 billion by 2033. Europe is witnessing significant demand for Cellular Concrete driven by stringent regulations on building materials, and a pronounced trend towards sustainability and reducing the carbon footprint in construction.Asia Pacific Cellular Concrete Market Report:

In 2023, the Asia Pacific Cellular Concrete market is valued at approximately $0.96 billion, with a projected growth to $2.03 billion by 2033. The growth is driven by rapid urbanization, increased construction activity, and infrastructure development in countries like India and China. Additionally, governmental initiatives promoting green building technologies are further boosting the market’s expansion.North America Cellular Concrete Market Report:

North America hosts the largest market for Cellular Concrete, with a valuation of around $1.64 billion in 2023, growing to $3.46 billion by 2033. The demand is spurred due to increasing infrastructure investments and a strong shift towards sustainable building materials, coupled with rigorous codes and regulations pertaining to energy efficiency.South America Cellular Concrete Market Report:

The South American market for Cellular Concrete was estimated at $0.43 billion in 2023 and is expected to reach $0.89 billion by 2033. The market is gaining momentum with increasing investments in infrastructure projects and urban development initiatives focused on affordable housing, which emphasizes the need for lightweight construction materials.Middle East & Africa Cellular Concrete Market Report:

In the Middle East and Africa, the market is anticipated to increase from $0.45 billion in 2023 to $0.95 billion by 2033. Expanding infrastructural projects due to urbanization and economic development, particularly in the UAE and South Africa, along with an increasing focus on energy-efficient construction practices, are key factors bolstering the market.Tell us your focus area and get a customized research report.

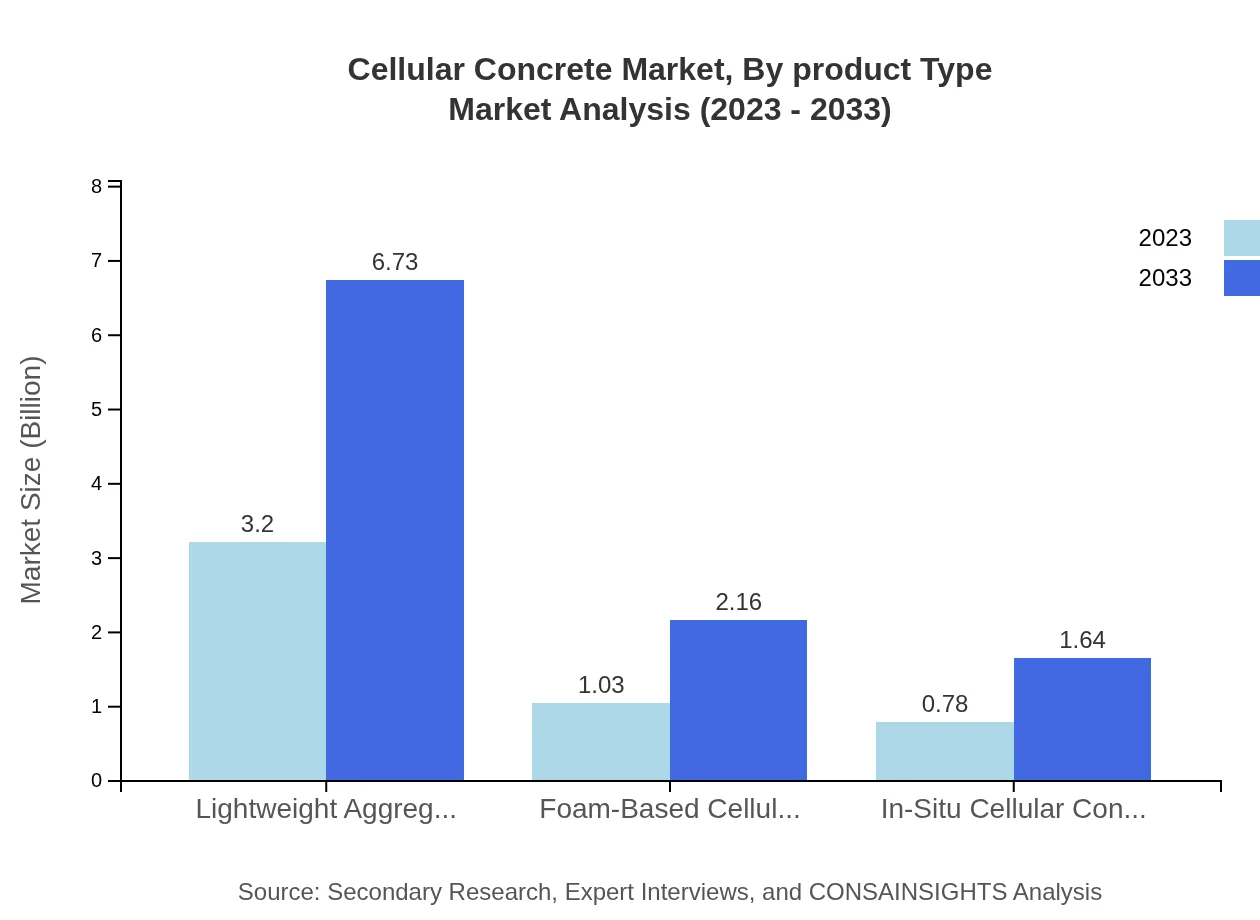

Cellular Concrete Market Analysis By Product Type

The product types of Cellular Concrete include Lightweight Aggregates, Foam-Based Cellular Concrete, and In-Situ Cellular Concrete. Among these, Lightweight Aggregate is expected to dominate the market due to its extensive use in various applications, accounting for approximately 63.91% of the market share, with an estimated market size of $3.20 billion in 2023, escalating to $6.73 billion by 2033.

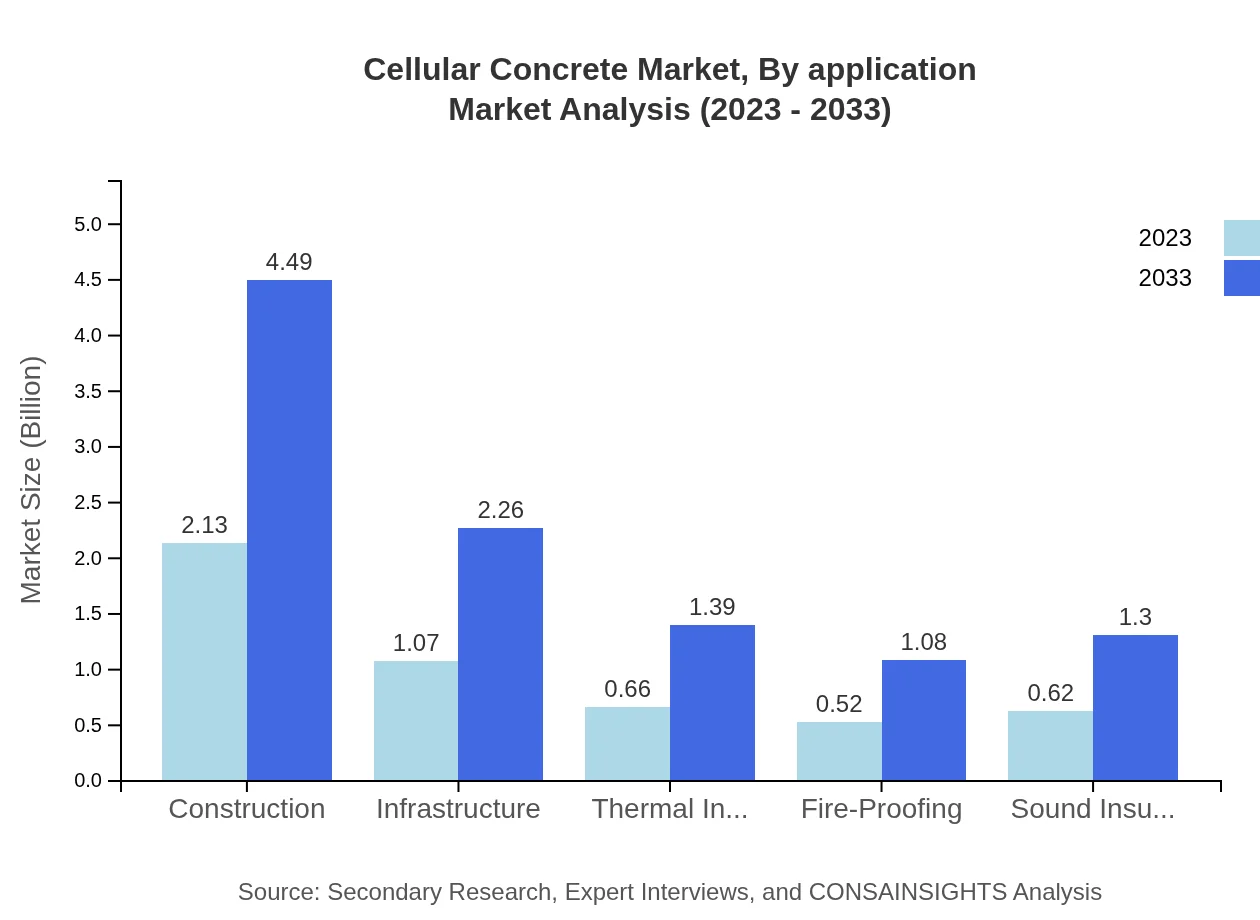

Cellular Concrete Market Analysis By Application

The applications of Cellular Concrete encompass construction, thermal insulation, fire-proofing, and sound insulation. The construction segment holds the largest share at 42.62%, contributing significantly to market value due to increased investments in infrastructural projects. By 2033, the construction application segment is projected to grow from $2.13 billion in 2023 to $4.49 billion.

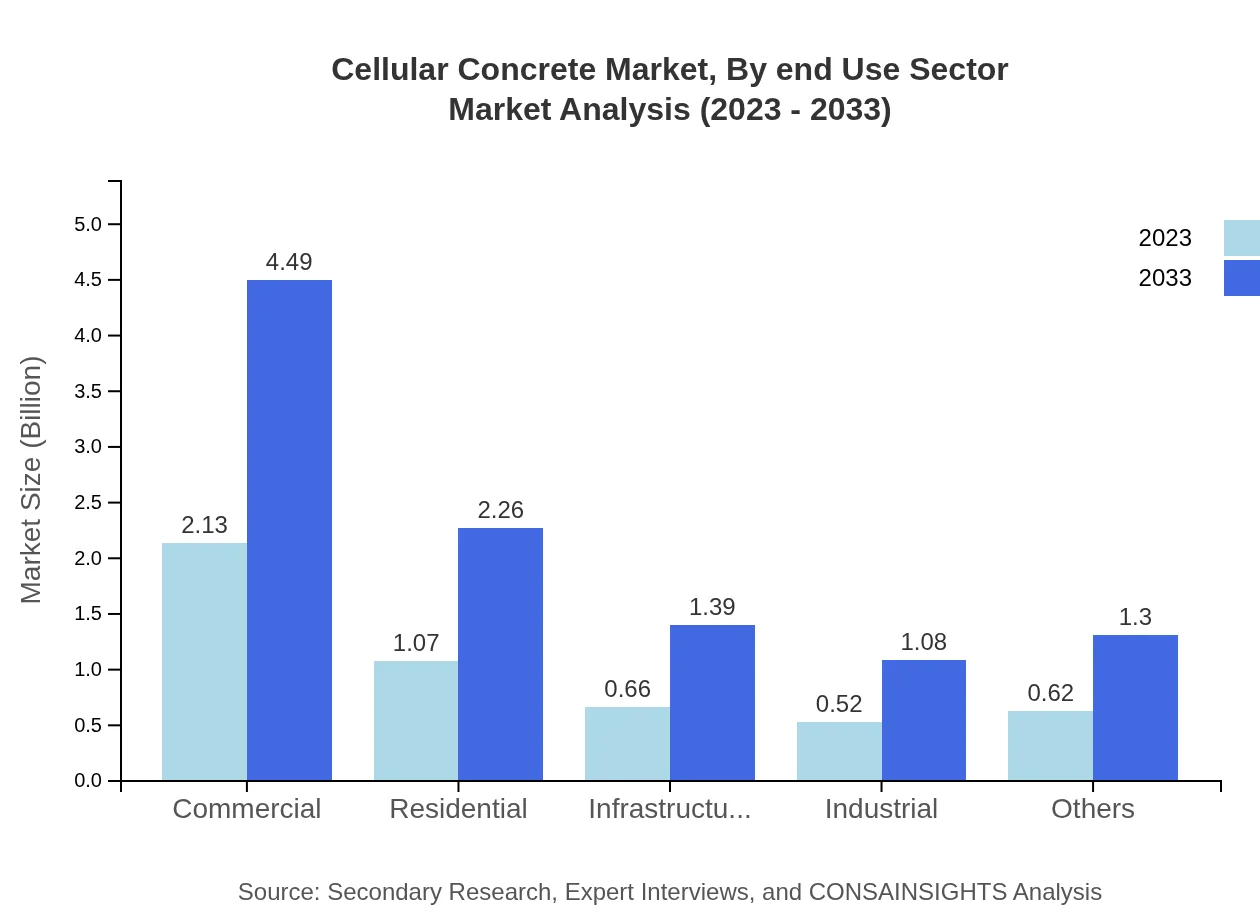

Cellular Concrete Market Analysis By End Use Sector

By end-use sector, the primary markets for Cellular Concrete include commercial, residential, industrial, and infrastructure development. The commercial sector holds a substantial share at 42.62%, with an expected market size of $2.13 billion in 2023, which is projected to grow to $4.49 billion by 2033, driven by urbanization and the need for commercial spaces.

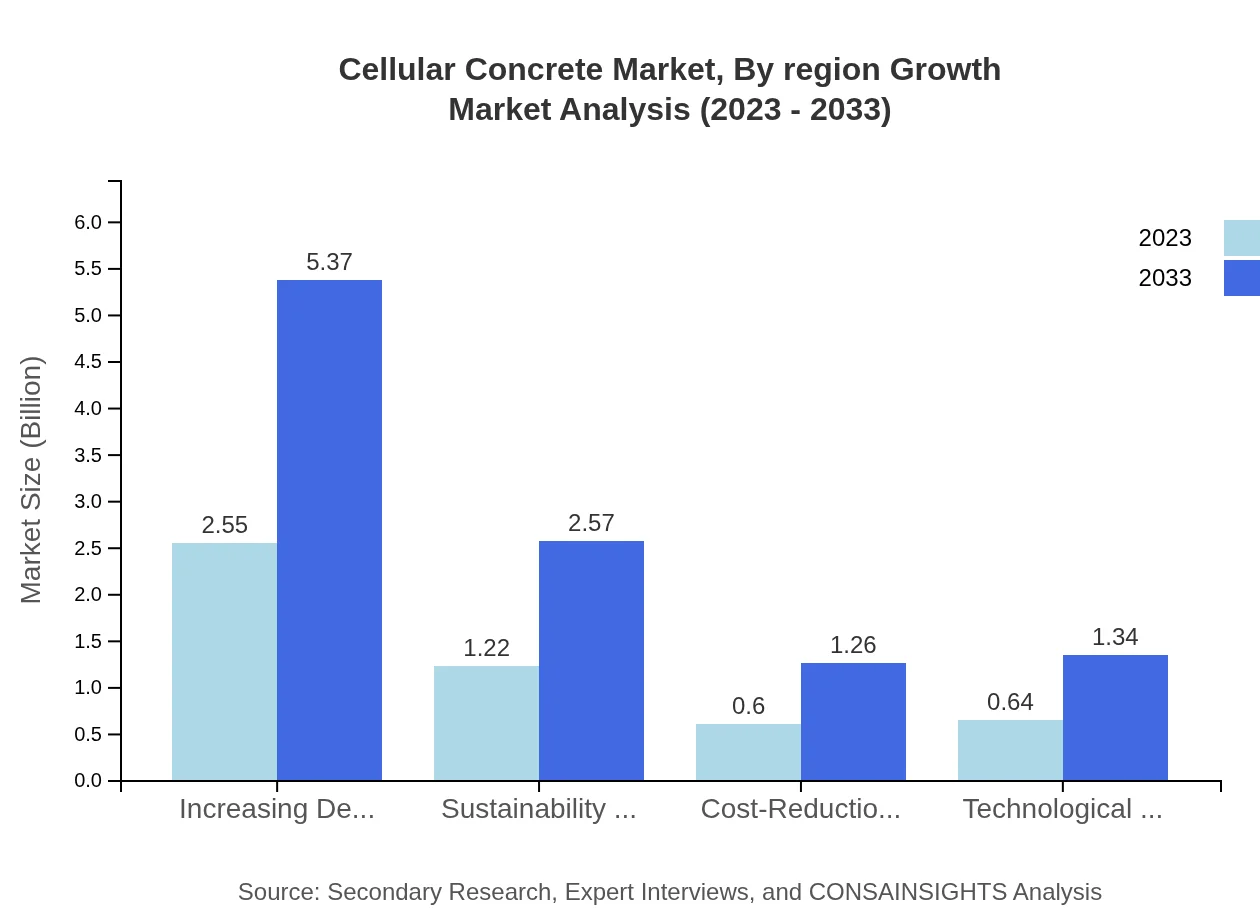

Cellular Concrete Market Analysis By Region Growth

Key growth factors for the Cellular Concrete market include the increasing demand for lightweight materials, technological advancements in production, and sustainability trends in construction. These factors are expected to facilitate substantial market growth, with the demand for lightweight materials alone projected to capture a market share of 50.98% by 2033, growing from $2.55 billion in 2023 to $5.37 billion.

Cellular Concrete Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Cellular Concrete Industry

Aercon:

Aercon is a leading manufacturer of autoclaved aerated concrete (AAC) products, known for its innovative lightweight concrete solutions and commitment to sustainable building practices.Xella Group:

Xella Group is another prominent player in the market, offering a diverse range of AAC products and focusing on eco-friendly construction solutions that meet rigorous international standards.Hebel:

Hebel, a subsidiary of the CSR Group, specializes in AAC blocks and panels, providing significant contributions to the construction industry's shift towards lightweight materials.H+H International A/S:

H+H International A/S is known for its sustainable and energy-efficient construction materials, particularly in the cellular concrete space, championing innovative production techniques.We're grateful to work with incredible clients.

FAQs

What is the market size of cellular Concrete?

The global cellular concrete market is projected to reach approximately $5 billion by 2033, growing at a CAGR of 7.5%. This expansion reflects increasing applications in various construction sectors.

What are the key market players or companies in the cellular Concrete industry?

Several prominent players dominate the cellular concrete market, including major construction firms and suppliers of lightweight materials. Their innovative products drive market competition and set industry standards.

What are the primary factors driving the growth in the cellular concrete industry?

Key growth drivers include rising demand for lightweight materials and sustainability trends in construction. Additionally, technological advancements in production methods are enhancing material performance and application versatility.

Which region is the fastest Growing in the cellular concrete market?

The Asia Pacific region is anticipated to witness significant growth, with market size increasing from $0.96 billion in 2023 to $2.03 billion by 2033, fueled by rapid urbanization and infrastructure development.

Does ConsaInsights provide customized market report data for the cellular concrete industry?

Yes, ConsaInsights offers tailored market reports that adapt to specific client needs, ensuring detailed insights into the cellular concrete industry, including market trends and competitive analyses.

What deliverables can I expect from this cellular concrete market research project?

Expect comprehensive reports featuring market size data, growth forecasts, regional breakdowns, and detailed analyses of key segments and trends within the cellular concrete industry.

What are the market trends of cellular concrete?

Influential trends include the increasing demand for cost-effective and lightweight construction materials, advancements in green building initiatives, and a competitive focus on improving material durability and sustainability.