Cellular Glass Market Report

Published Date: 02 February 2026 | Report Code: cellular-glass

Cellular Glass Market Size, Share, Industry Trends and Forecast to 2033

This report provides a comprehensive analysis of the Cellular Glass market, covering insights from 2023 to 2033. It includes market trends, segmentation, regional analysis, and forecasts, along with detailed information on key players in the industry.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

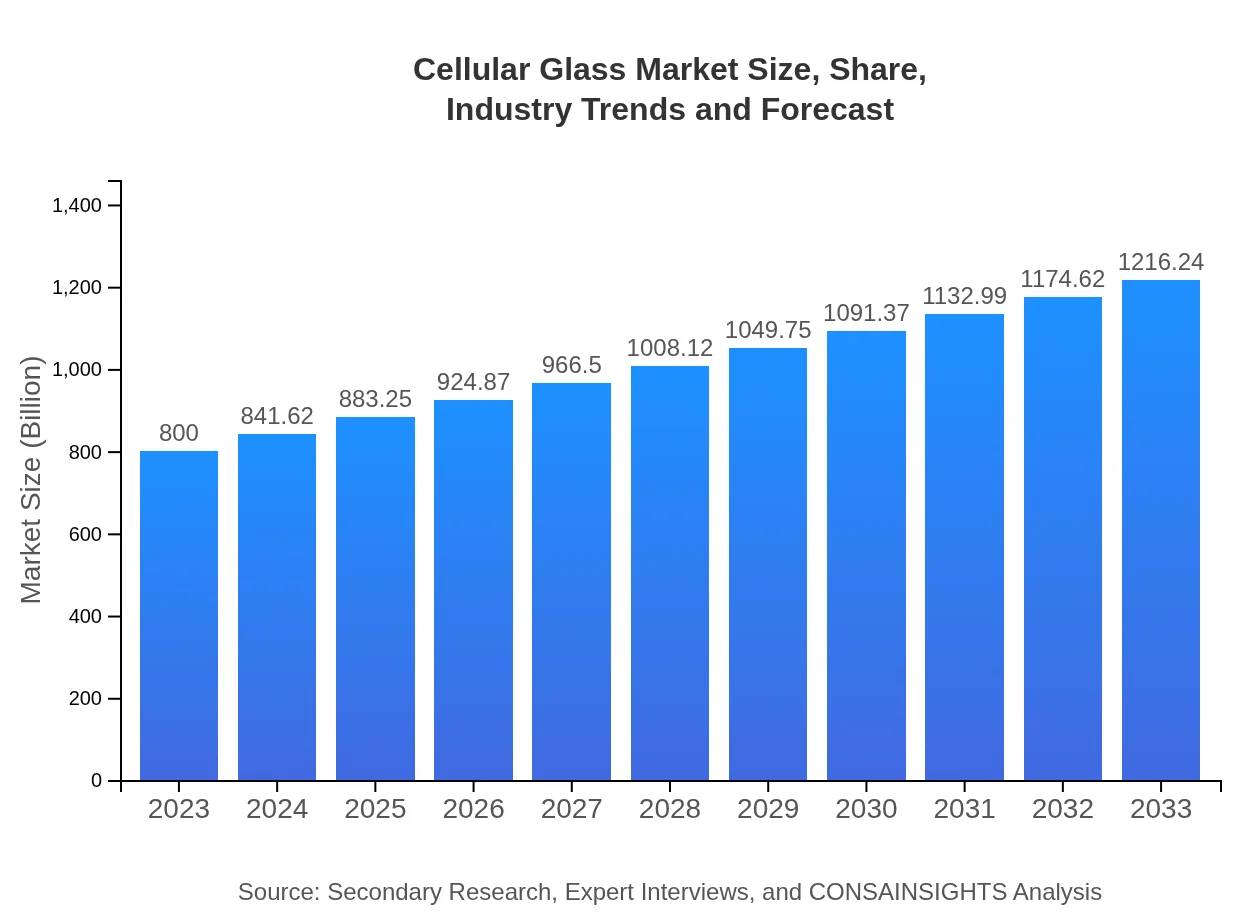

| 2023 Market Size | $800.00 Million |

| CAGR (2023-2033) | 4.2% |

| 2033 Market Size | $1216.24 Million |

| Top Companies | Owens Corning, Saint-Gobain, U.S. Gasket & Packing, Glasweld |

| Last Modified Date | 02 February 2026 |

Cellular Glass Market Overview

Customize Cellular Glass Market Report market research report

- ✔ Get in-depth analysis of Cellular Glass market size, growth, and forecasts.

- ✔ Understand Cellular Glass's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Cellular Glass

What is the Market Size & CAGR of Cellular Glass market in 2023?

Cellular Glass Industry Analysis

Cellular Glass Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Cellular Glass Market Analysis Report by Region

Europe Cellular Glass Market Report:

Europe's market is robust due to a strong focus on energy efficiency, with a market size of $207.68 million in 2023 projected to increase to $315.74 million by 2033. Initiatives toward reducing carbon footprints are driving innovation in cellular glass products.Asia Pacific Cellular Glass Market Report:

The Asia Pacific region is witnessing robust growth, with a market size of $153.76 million in 2023 and expected to reach $233.76 million by 2033. Rising construction activities and increasing investments in green buildings are propelling demand.North America Cellular Glass Market Report:

North America holds a significant share of the market, valued at $301.76 million in 2023, with expectations to grow to $458.77 million by 2033. The region's growth is fueled by stringent regulations on energy efficiency and increasing demand for high-performance building materials.South America Cellular Glass Market Report:

In South America, the market is projected to grow from $46.40 million in 2023 to $70.54 million by 2033, driven by expanding construction projects and government initiatives focused on sustainable practices.Middle East & Africa Cellular Glass Market Report:

The Middle East and Africa market is expected to see growth from $90.40 million in 2023 to $137.44 million by 2033, influenced by infrastructure development and rising demand for thermal insulation materials.Tell us your focus area and get a customized research report.

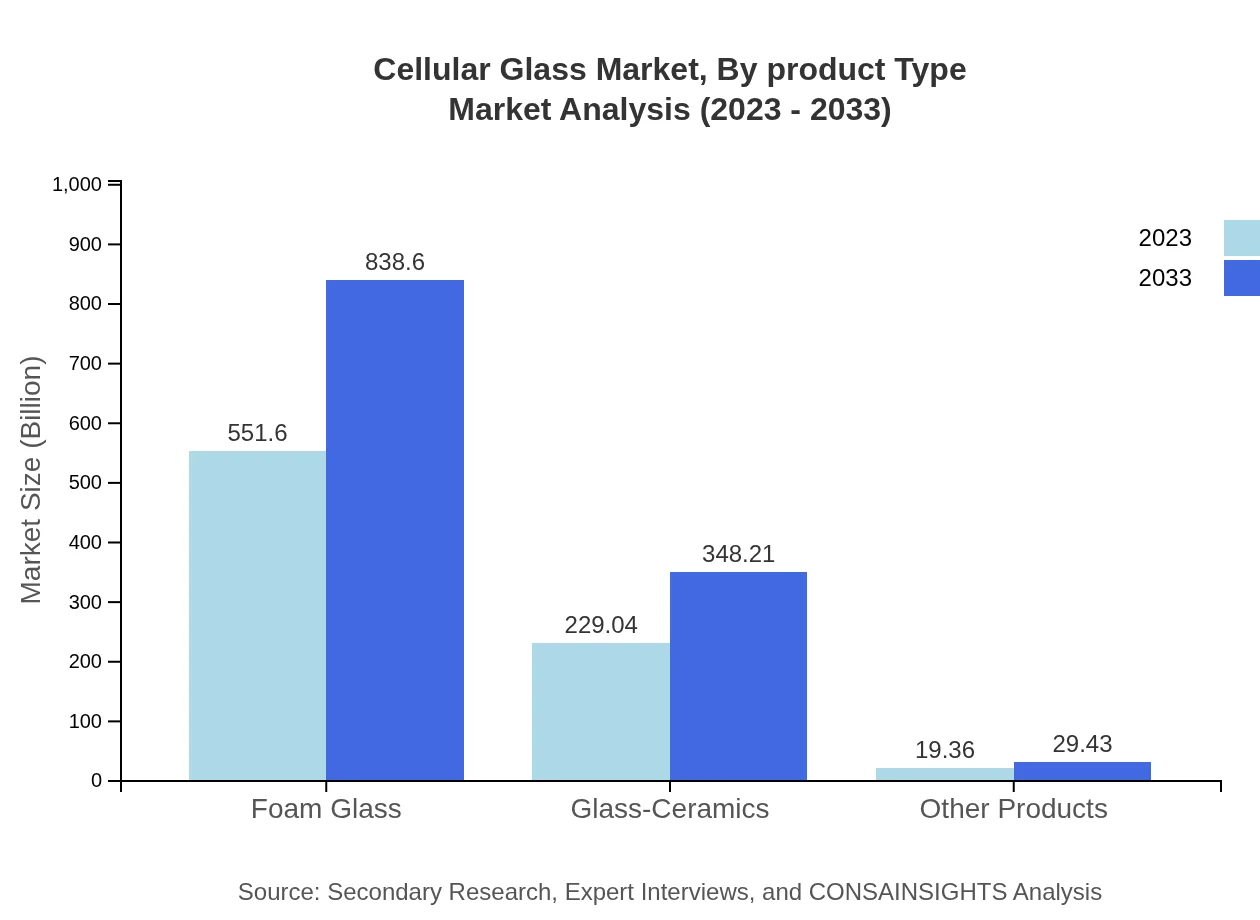

Cellular Glass Market Analysis By Product Type

The Cellular Glass market by product type includes foam glass and glass-ceramics. Foam glass leads the segment with a market size of $551.60 million in 2023, projected to grow to $838.60 million by 2033. Glass-ceramics follow with $229.04 million in 2023, expected to reach $348.21 million by 2033.

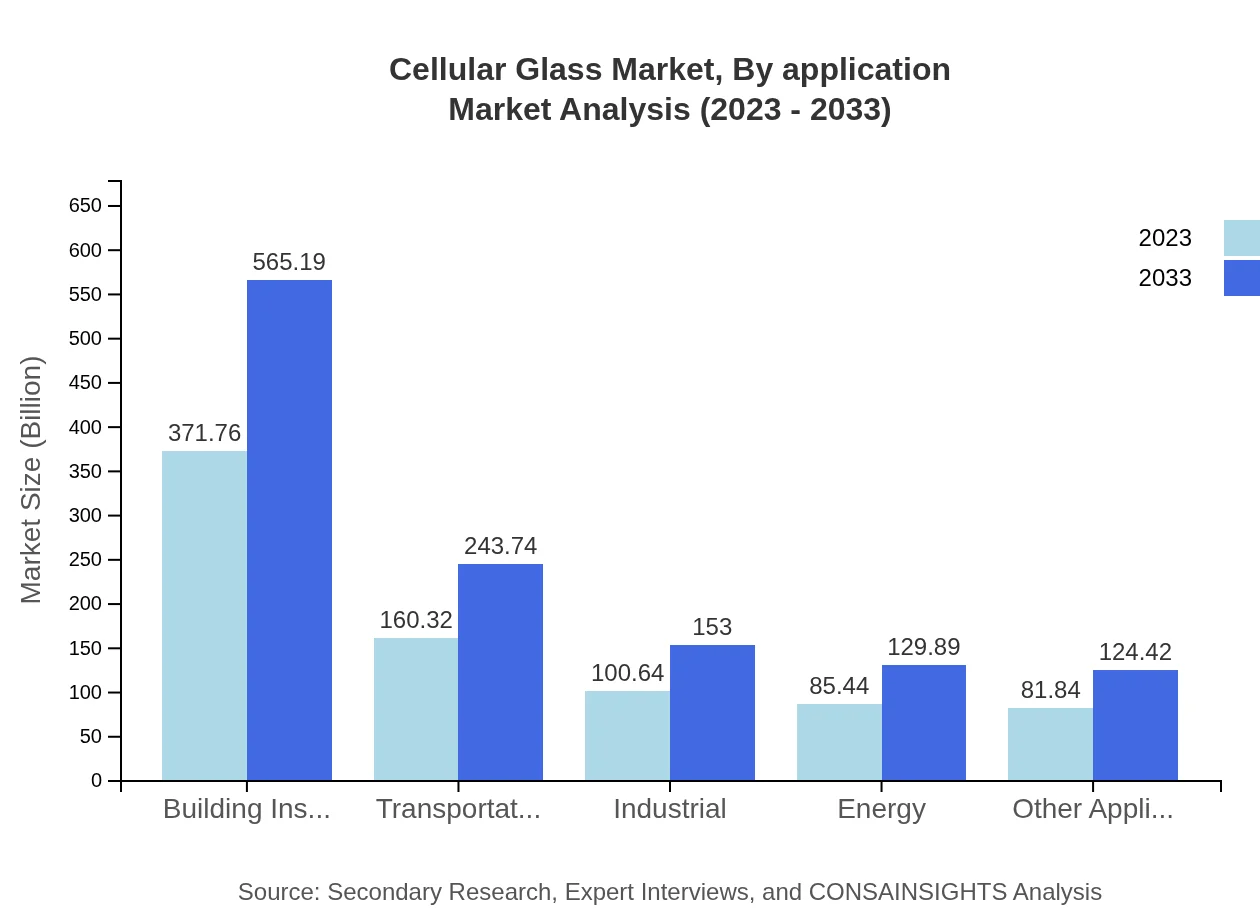

Cellular Glass Market Analysis By Application

By application, the market is led by construction and insulation, valued at $371.76 million in 2023 and anticipated to reach $565.19 million by 2033. Other significant applications include marine and automotive sectors.

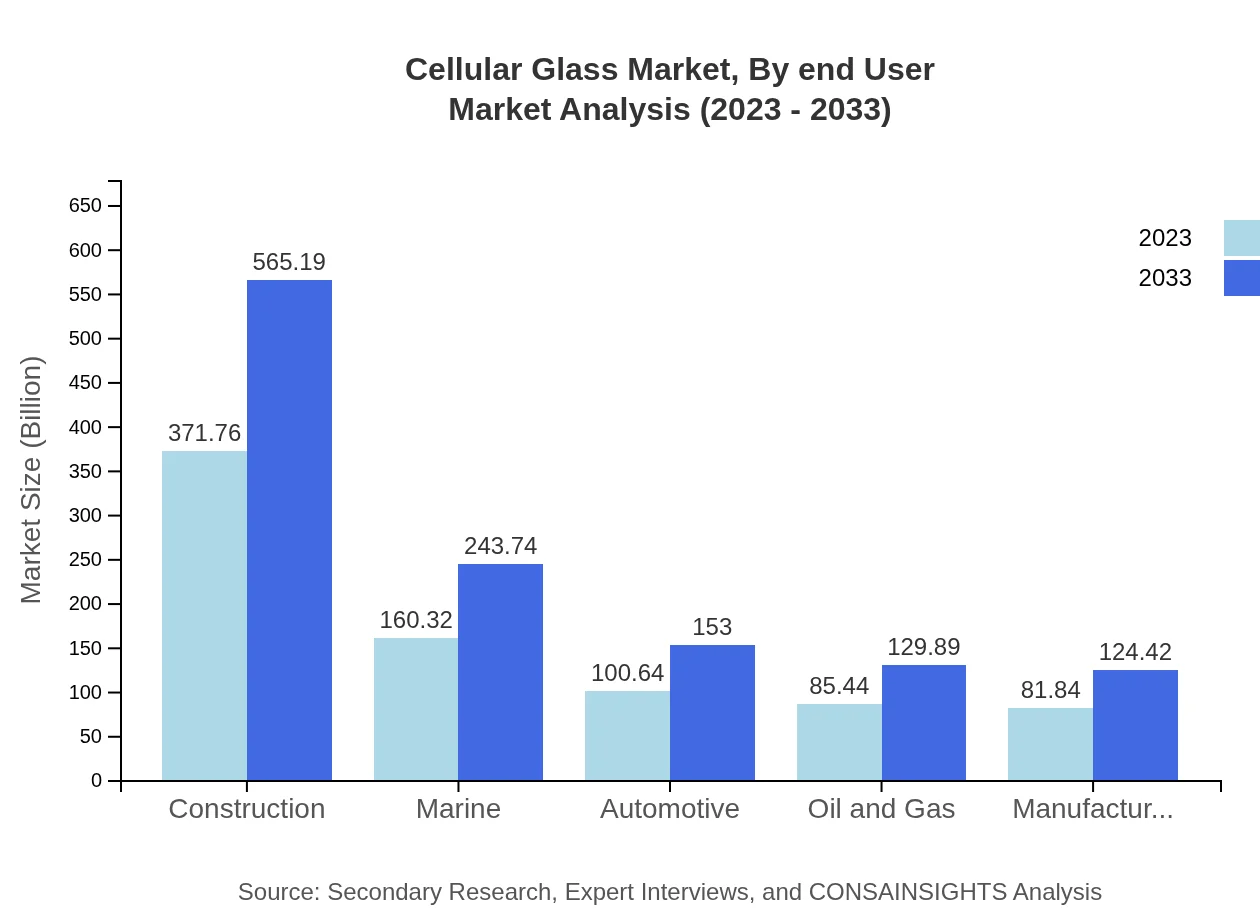

Cellular Glass Market Analysis By End User

End-users include construction, automotive, and marine industries. The construction sector holds the largest share at 46.47% in 2023, with similar shares predicted for 2033, reflecting its central role in market growth.

Cellular Glass Market Analysis By Production Techniques

Production techniques include traditional manufacturing and advanced manufacturing, where traditional methods account for a significant market share due to established processes and technologies.

Cellular Glass Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Cellular Glass Industry

Owens Corning:

A leading global producer of insulation and high-performance building materials, contributing significantly to innovations in cellular glass technology.Saint-Gobain:

Specializes in construction materials and is a prominent player in the cellular glass market, focusing on sustainable solutions.U.S. Gasket & Packing:

Provides a variety of foam glass products for insulation and fire safety, known for its advanced manufacturing capabilities.Glasweld:

An innovative company producing cellular glass products with a focus on energy efficiency and durability.We're grateful to work with incredible clients.

FAQs

What is the market size of cellular Glass?

The cellular-glass market was valued at approximately $800 million in 2023, with a projected CAGR of 4.2% over the next decade, indicating substantial growth potential in various applications and regions.

What are the key market players or companies in this cellular Glass industry?

Key players in the cellular-glass industry include leading manufacturers and suppliers actively enhancing their production capabilities and innovations to cater to the growing demand across sectors like construction and automotive.

What are the primary factors driving the growth in the cellular Glass industry?

The growth of the cellular-glass market is driven by increased construction activities, stringent energy efficiency regulations, and a growing emphasis on sustainable materials in various industries, including automotive and construction.

Which region is the fastest Growing in the cellular Glass?

The North American region is the fastest-growing market for cellular-glass, expected to rise from $301.76 million in 2023 to $458.77 million by 2033, driven by robust construction and industrial sectors.

Does ConsaInsights provide customized market report data for the cellular Glass industry?

Yes, ConsaInsights offers customized market report data tailored to specific business needs and market segments within the cellular-glass industry, ensuring relevance and accuracy.

What deliverables can I expect from this cellular Glass market research project?

Expect detailed market analysis reports, segmentation insights, competitive landscape assessments, and growth forecasts, along with tailored recommendations for market entry or expansion strategies.

What are the market trends of cellular Glass?

Key trends include the rising adoption of cellular-glass in construction for insulation, advancements in manufacturing processes, and increased focus on recycling materials to support sustainability efforts in various industries.