Ceramic Matrix Composites Market Report

Published Date: 02 February 2026 | Report Code: ceramic-matrix-composites

Ceramic Matrix Composites Market Size, Share, Industry Trends and Forecast to 2033

This report provides an in-depth analysis of the Ceramic Matrix Composites market, focusing on market trends, size, CAGR, industry insights, regional performances, and future forecasts for the period of 2023 to 2033.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

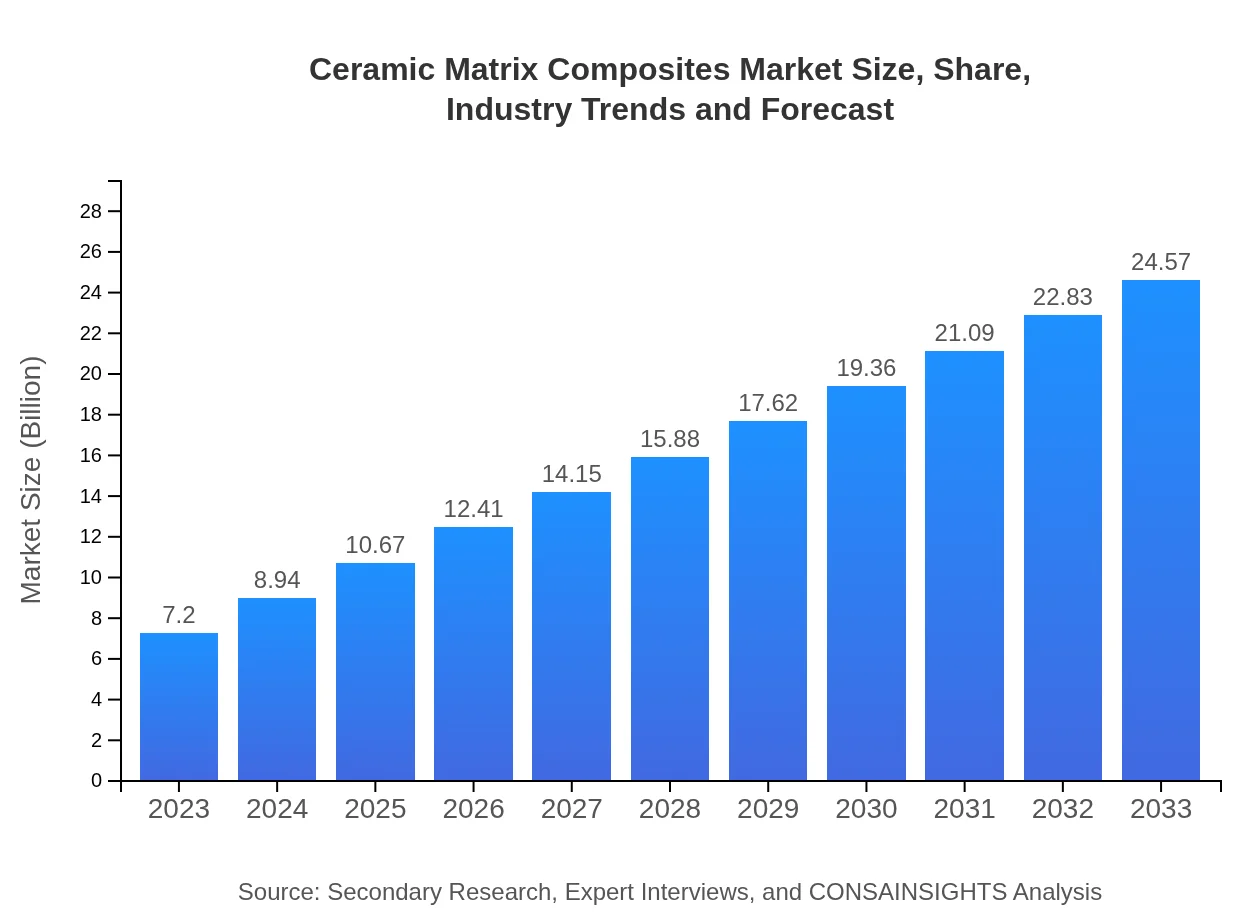

| 2023 Market Size | $7.20 Billion |

| CAGR (2023-2033) | 12.5% |

| 2033 Market Size | $24.57 Billion |

| Top Companies | Hexcel Corporation, Toshiba Corporation, Advanced Ceramic Fibers (ACFs), General Electric (GE) |

| Last Modified Date | 02 February 2026 |

Ceramic Matrix Composites Market Overview

Customize Ceramic Matrix Composites Market Report market research report

- ✔ Get in-depth analysis of Ceramic Matrix Composites market size, growth, and forecasts.

- ✔ Understand Ceramic Matrix Composites's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Ceramic Matrix Composites

What is the Market Size & CAGR of Ceramic Matrix Composites market in 2023?

Ceramic Matrix Composites Industry Analysis

Ceramic Matrix Composites Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Ceramic Matrix Composites Market Analysis Report by Region

Europe Ceramic Matrix Composites Market Report:

The European market is anticipated to grow from approximately $1.91 billion in 2023 to $6.52 billion by 2033. Driven by tight regulations on emissions and the push for lightweight materials in aerospace and automotive industries, Europe is at the forefront of adopting ceramic matrix composites for various applications.Asia Pacific Ceramic Matrix Composites Market Report:

The Asia Pacific region is projected to witness significant growth, with the market expanding from $1.43 billion in 2023 to $4.90 billion by 2033. This growth can be attributed to rising industrialization, increased defense expenditure, and a booming automotive sector, particularly in countries like China and Japan, which are focusing on advanced materials for technological enhancement.North America Ceramic Matrix Composites Market Report:

North America, holding the largest market share, is set to increase from $2.75 billion in 2023 to $9.40 billion by 2033. This region’s market growth is propelled by the strong presence of key aerospace and defense players, increasing use in automotive applications, and significant government investments in advanced manufacturing technologies.South America Ceramic Matrix Composites Market Report:

In South America, the market is expected to grow from $0.43 billion in 2023 to $1.45 billion by 2033. The slow but steady growth is driven by the expanding aerospace and energy sectors, with Brazil leading the demand for CMCs due to its focus on renewable energy technologies and aircraft manufacturing.Middle East & Africa Ceramic Matrix Composites Market Report:

The market in the Middle East and Africa is projected to grow from $0.67 billion in 2023 to $2.30 billion by 2033. This growth is driven by increasing investments in the aerospace sector and emerging renewable energy projects, which are beginning to adopt CMC materials.Tell us your focus area and get a customized research report.

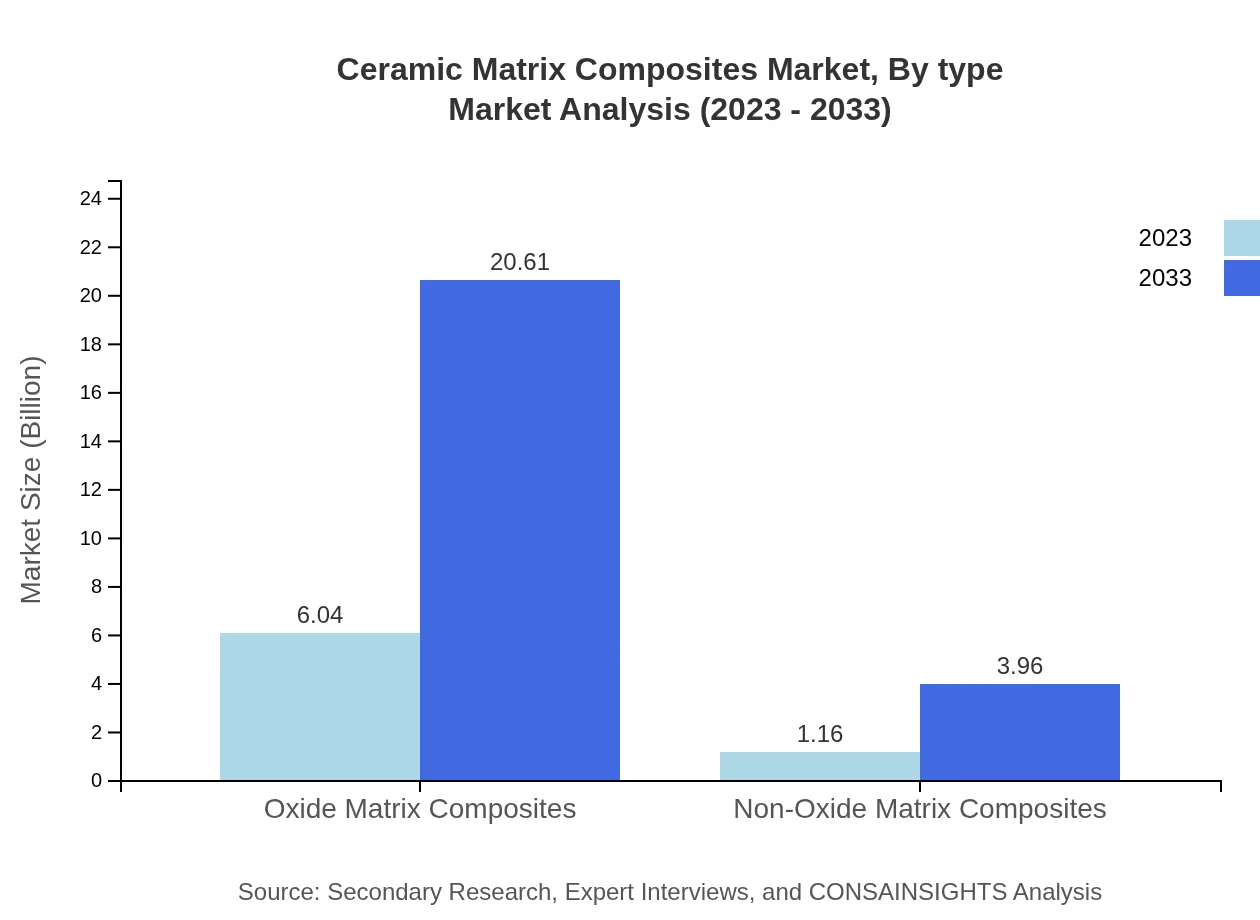

Ceramic Matrix Composites Market Analysis By Type

The ceramic matrix composites market is segmented into Oxide Matrix Composites and Non-Oxide Matrix Composites. Oxide Matrix Composites dominate the market, with a significant market size of $6.04 billion in 2023, projected to reach $20.61 billion by 2033, holding an 83.89% market share. Non-Oxide Matrix Composites, while smaller, are also critical, growing from $1.16 billion to $3.96 billion during the same period, maintaining a 16.11% market share.

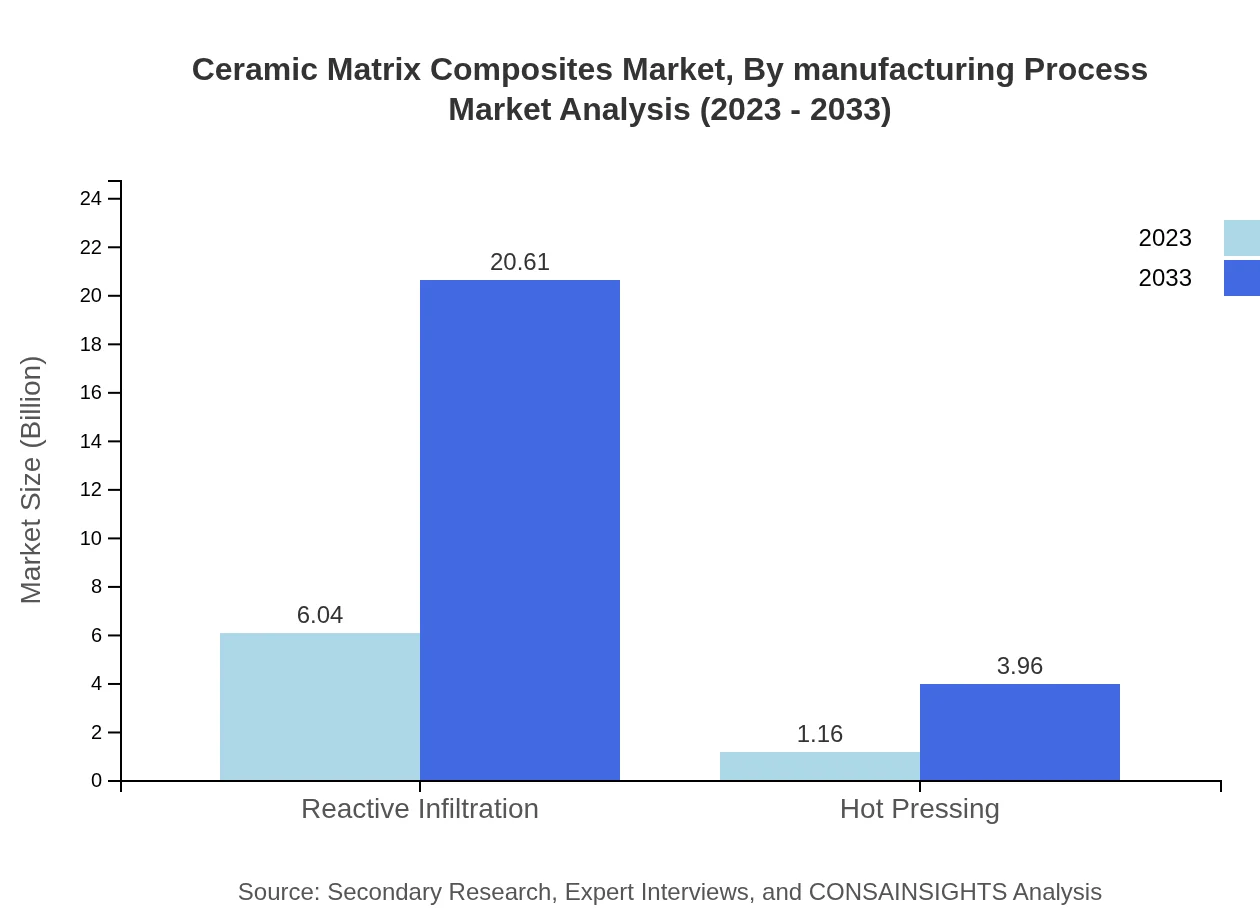

Ceramic Matrix Composites Market Analysis By Manufacturing Process

Manufacturing processes of Ceramic Matrix Composites include Reactive Infiltration and Hot Pressing. Reactive Infiltration benefits from its scalability and efficiency, with a market size of $6.04 billion in 2023 expected to rise to $20.61 billion by 2033. Hot Pressing is essential for producing Non-Oxide Matrix CMCs, growing from $1.16 billion to $3.96 billion.

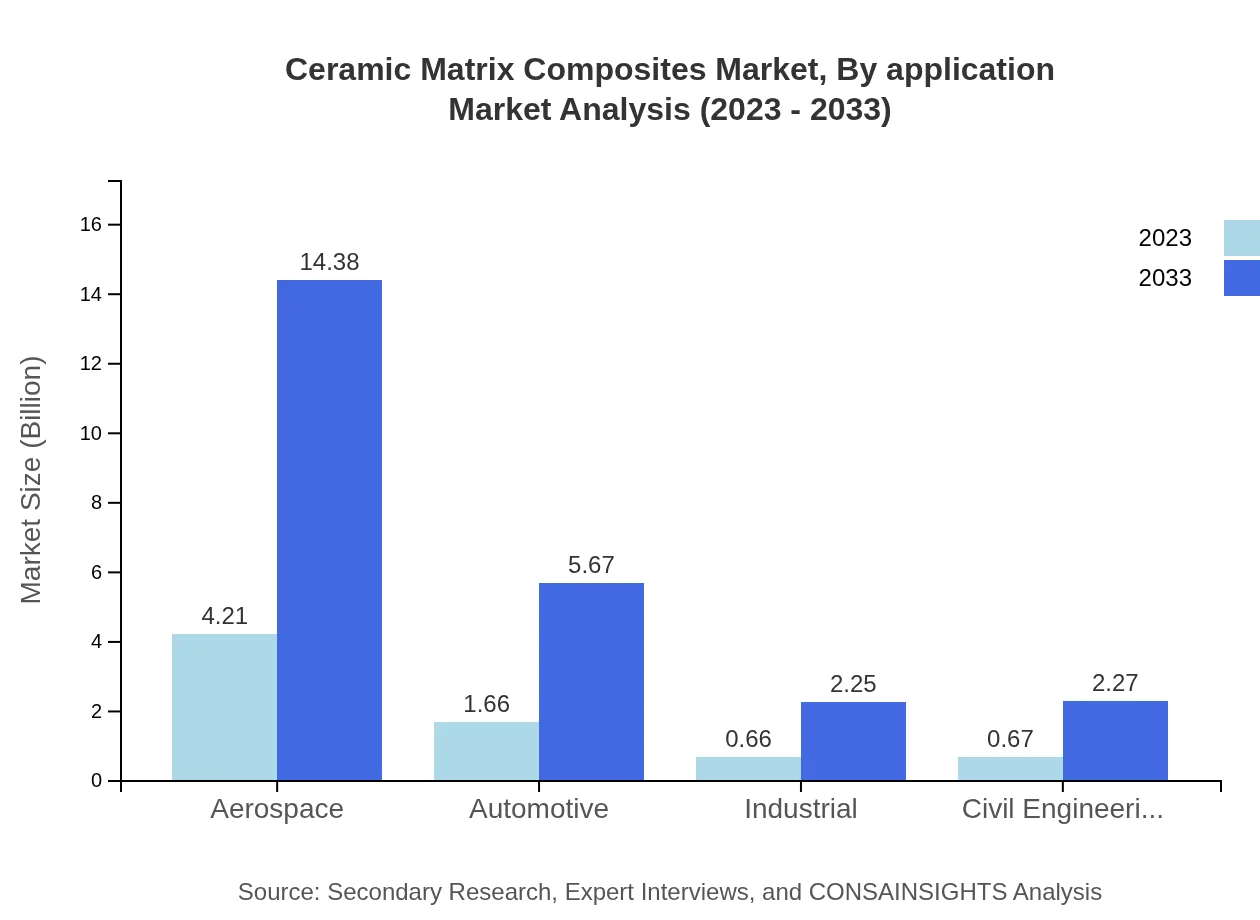

Ceramic Matrix Composites Market Analysis By Application

The applications of CMCs span various industries, most notably Aerospace and Defense, manufacturing $4.21 billion in 2023, with an expected increase to $14.38 billion. Other applications include Automotive, Electronics, and Telecommunications, reflecting diverse use cases and market potential.

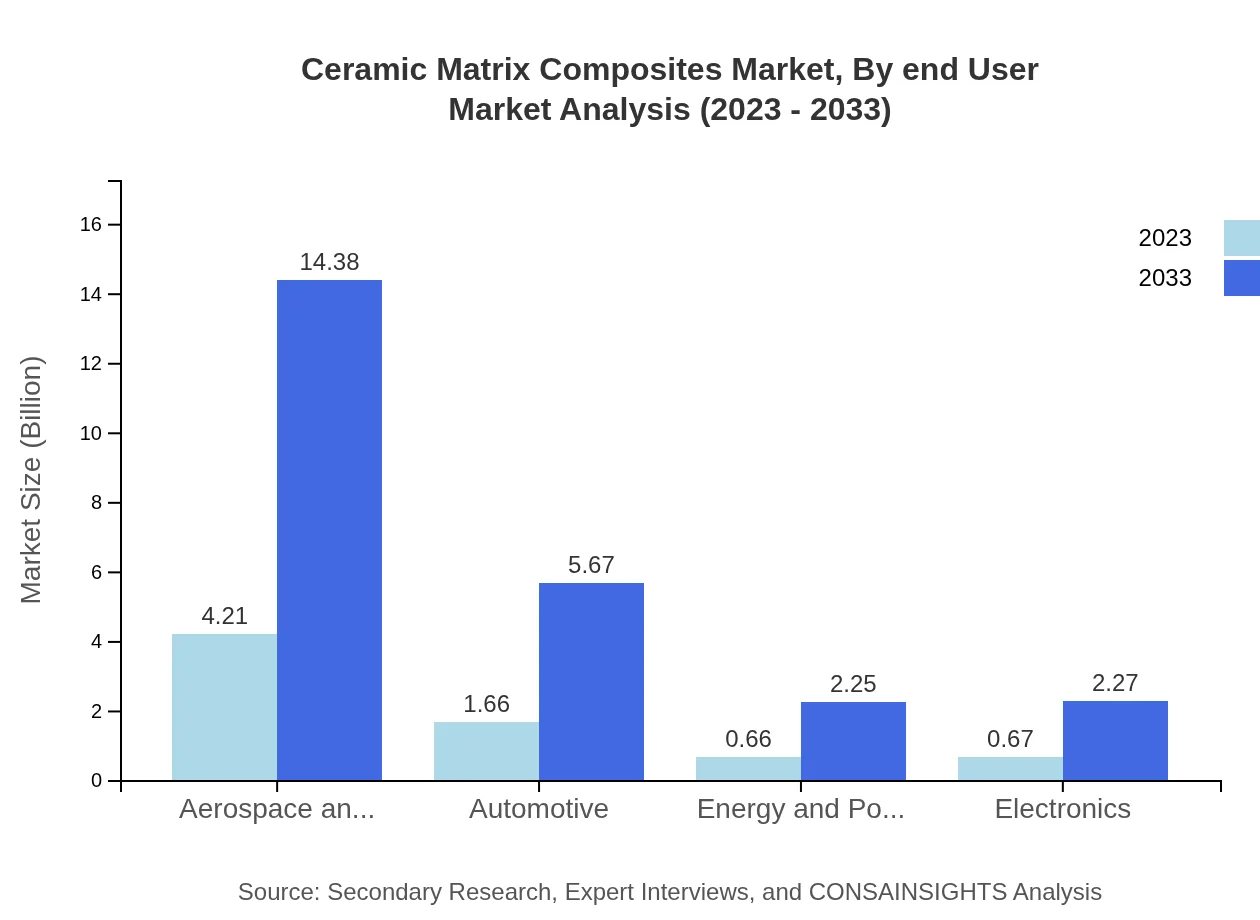

Ceramic Matrix Composites Market Analysis By End User

End-user industries of CMCs encompass Aerospace, Automotive, Medical, and Energy sectors. The Aerospace industry leads with significant demand, projected to maintain 58.52% market share, while growing applications in Automotive are seeing a rise from $1.66 billion to $5.67 billion.

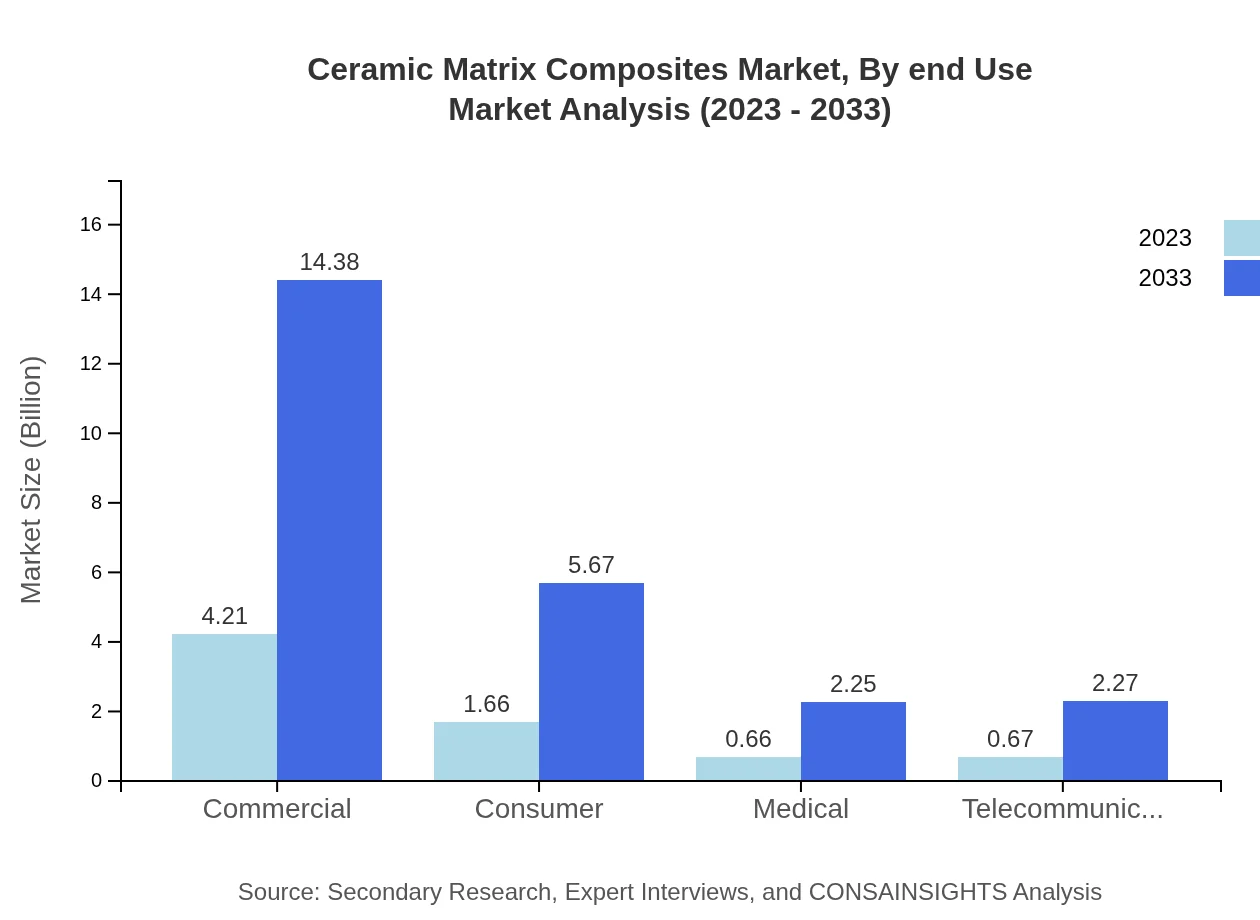

Ceramic Matrix Composites Market Analysis By End Use

End-use applications include Industrial, Civil Engineering, and Defense among others. The market for Industrial applications is projected to expand substantially, demonstrating the diverse range of opportunities available for manufacturers in the CMC segment.

Ceramic Matrix Composites Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Ceramic Matrix Composites Industry

Hexcel Corporation:

Hexcel specializes in manufacturing advanced composites for aerospace and other applications, contributing significantly with their innovative composite solutions.Toshiba Corporation:

A leader in advanced materials, Toshiba's CMC products are widely utilized in industries requiring high thermal resistance and durability.Advanced Ceramic Fibers (ACFs):

ACFs is known for producing specialized advanced ceramic materials that enhance thermal and structural performance in aerospace applications.General Electric (GE):

GE plays a pivotal role in the aerospace industry, advancing the use of CMCs in turbine applications, contributing to improved fuel efficiency and reduced emissions.We're grateful to work with incredible clients.

FAQs

What is the market size of Ceramic Matrix Composites?

The global Ceramic Matrix Composites market is projected to reach approximately $7.2 billion by 2033, growing at a CAGR of 12.5% from its current valuation.

What are the key market players or companies in the Ceramic Matrix Composites industry?

Key players in the Ceramic Matrix Composites market include major companies such as GE Aviation, Rolls-Royce, and Airbus, which are recognized for their innovative applications in aerospace and defense sectors.

What are the primary factors driving the growth in the Ceramic Matrix Composites industry?

The growth in the Ceramic Matrix Composites industry is driven by the increasing demand for high-performance materials in aerospace, automotive, and energy applications, coupled with advancements in manufacturing technologies.

Which region is the fastest Growing in the Ceramic Matrix Composites?

The North American region is poised to be the fastest-growing market for Ceramic Matrix Composites, with an anticipated market increase from $2.75 billion in 2023 to $9.40 billion by 2033.

Does ConsaInsights provide customized market report data for the Ceramic Matrix Composites industry?

Yes, ConsaInsights offers customized market report data for the Ceramic Matrix Composites industry tailored to specific requirements, ensuring clients receive the most relevant insights.

What deliverables can I expect from this Ceramic Matrix Composites market research project?

From this market research project, expect comprehensive reports containing market size, forecasts, segment analyses, regional insights, and competitive assessments to guide strategic decision-making.

What are the market trends of Ceramic Matrix Composites?

Current trends in the Ceramic Matrix Composites market include a shift towards sustainable materials, increasing applications in energy and telecommunications, and advancements in processing technologies.