Compound Semiconductor Market Report

Published Date: 31 January 2026 | Report Code: compound-semiconductor

Compound Semiconductor Market Size, Share, Industry Trends and Forecast to 2033

This report provides a comprehensive analysis of the Compound Semiconductor market from 2023 to 2033, covering detailed insights on market size, growth rates, regional analyses, technology trends, and competitive landscape.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

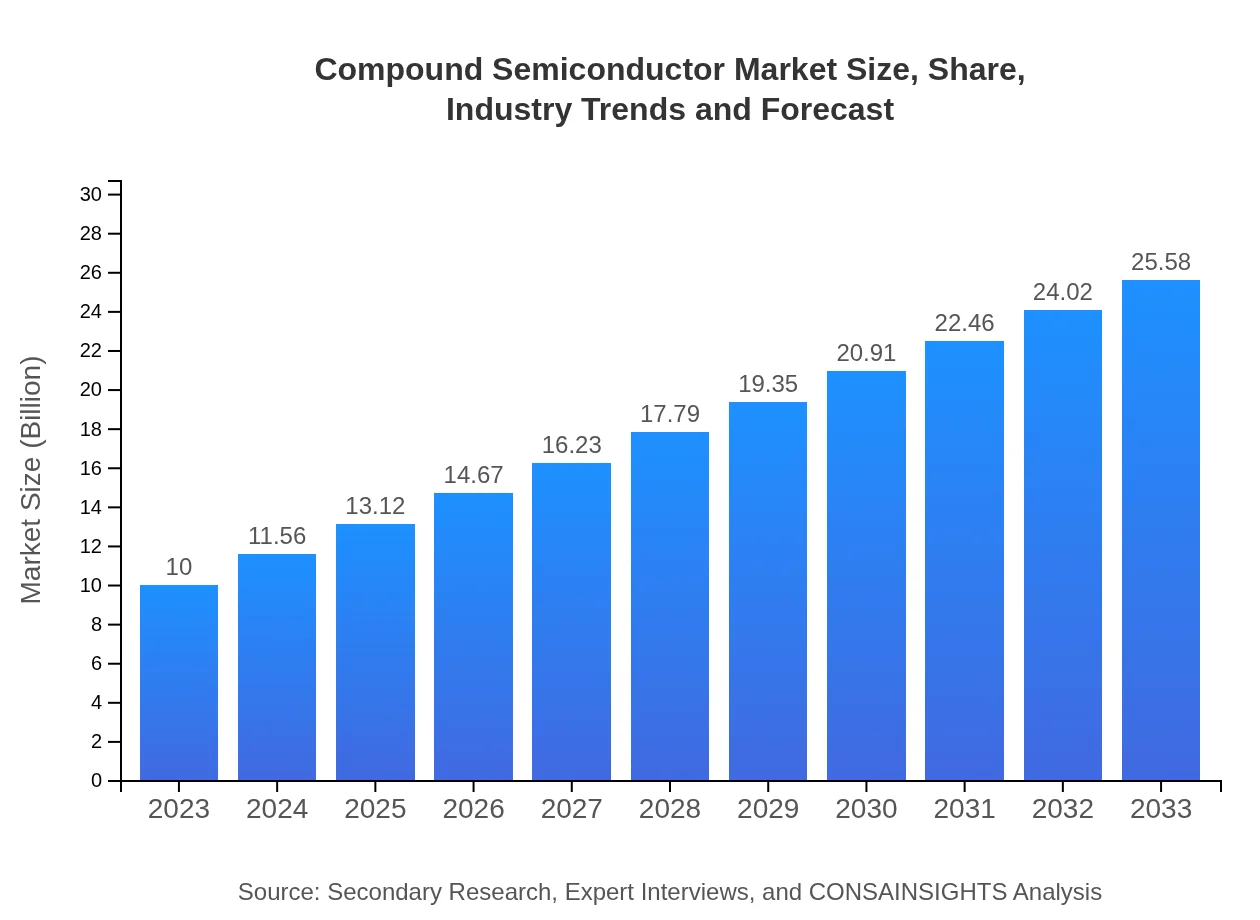

| 2023 Market Size | $10.00 Billion |

| CAGR (2023-2033) | 9.5% |

| 2033 Market Size | $25.58 Billion |

| Top Companies | Infineon Technologies AG, Cree, Inc., Qualcomm Incorporated, NXP Semiconductors N.V., Broadcom Inc. |

| Last Modified Date | 31 January 2026 |

Compound Semiconductor Market Overview

Customize Compound Semiconductor Market Report market research report

- ✔ Get in-depth analysis of Compound Semiconductor market size, growth, and forecasts.

- ✔ Understand Compound Semiconductor's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Compound Semiconductor

What is the Market Size & CAGR of Compound Semiconductor market in 2023?

Compound Semiconductor Industry Analysis

Compound Semiconductor Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Compound Semiconductor Market Analysis Report by Region

Europe Compound Semiconductor Market Report:

Europe's Compound Semiconductor market is forecasted to increase from 3.05 billion USD in 2023 to 7.81 billion USD by 2033. The region benefits from its focus on sustainability and advanced automotive technology innovations, increasingly turning to compound semiconductors for efficient power solutions and communications technologies.Asia Pacific Compound Semiconductor Market Report:

The Asia Pacific region is anticipated to grow from 1.90 billion USD in 2023 to about 4.85 billion USD by 2033, reflecting a solid growth trajectory fueled by a robust electronics manufacturing sector in countries like China, Japan, and South Korea. The demand for advanced solutions in telecommunications and consumer electronics continues to drive investments and innovations in this region.North America Compound Semiconductor Market Report:

North America, with its current market size of 3.59 billion USD in 2023, is likely to grow to 9.18 billion USD by 2033. Driven by advancements in 5G technology and electric networks, the region is characterized by strong R&D activities, significant investments, and a dense ecosystem of semiconductor manufacturers.South America Compound Semiconductor Market Report:

South America's Compound Semiconductor market is expected to expand from 0.53 billion USD in 2023 to around 1.35 billion USD by 2033. This growth is primarily attributed to the increasing adoption of smart technologies and government initiatives to promote digital transformation in key industries.Middle East & Africa Compound Semiconductor Market Report:

The Middle East and Africa's market size is projected to move from 0.93 billion USD in 2023 to 2.38 billion USD by 2033. Growth in telecommunications infrastructure and the rise of renewable energy projects are prompting further adoption of compound semiconductor technologies in this region.Tell us your focus area and get a customized research report.

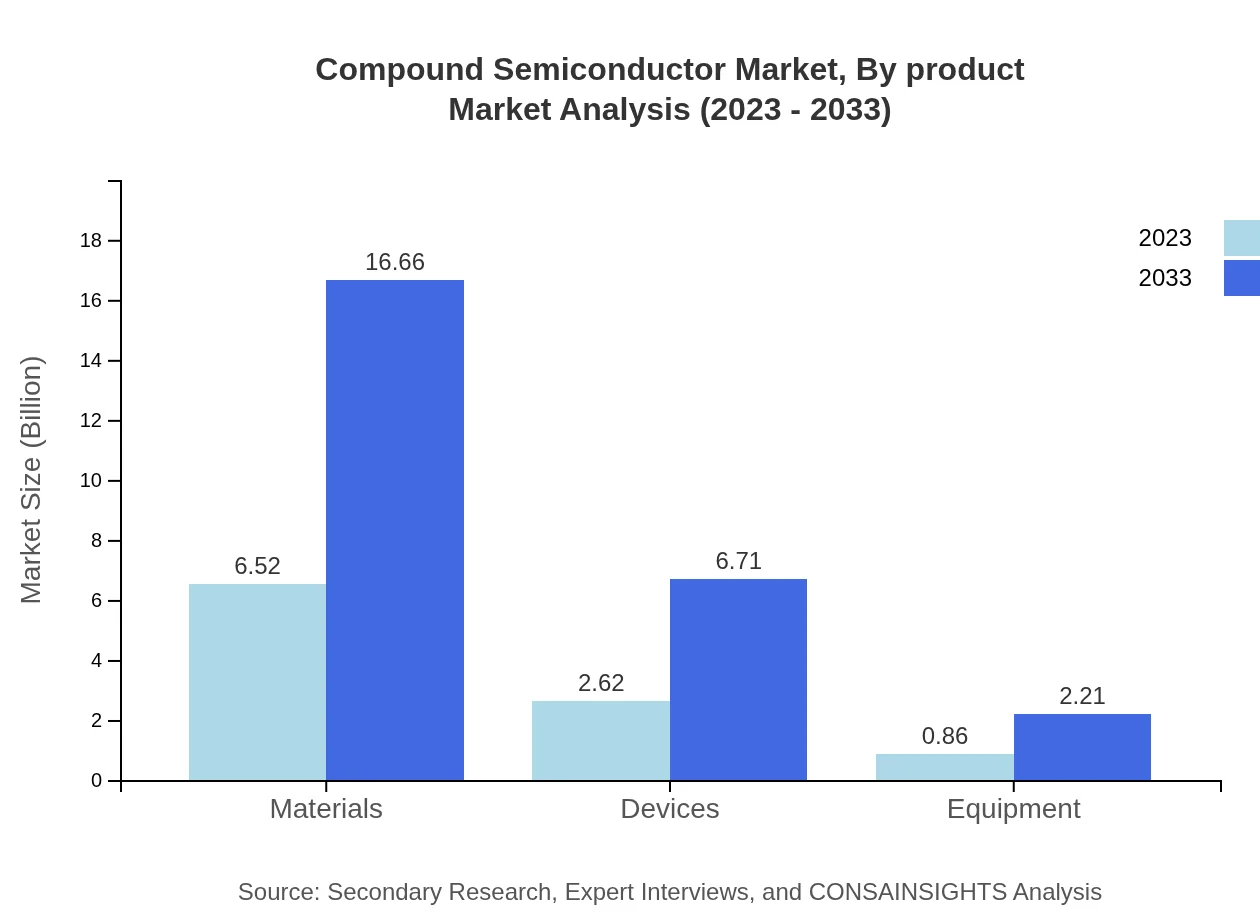

Compound Semiconductor Market Analysis By Product

The Compound Semiconductor market by product is dominated by materials, which accounted for a market size of 6.52 billion USD in 2023 with expected growth to 16.66 billion USD by 2033, achieving a share of 65.15%. Devices represent the second largest segment at 2.62 billion USD in 2023, projected to grow to 6.71 billion USD by 2033, holding a share of 26.22%. Equipment accounts for a smaller segment, growing from 0.86 billion USD in 2023 to 2.21 billion USD by 2033.

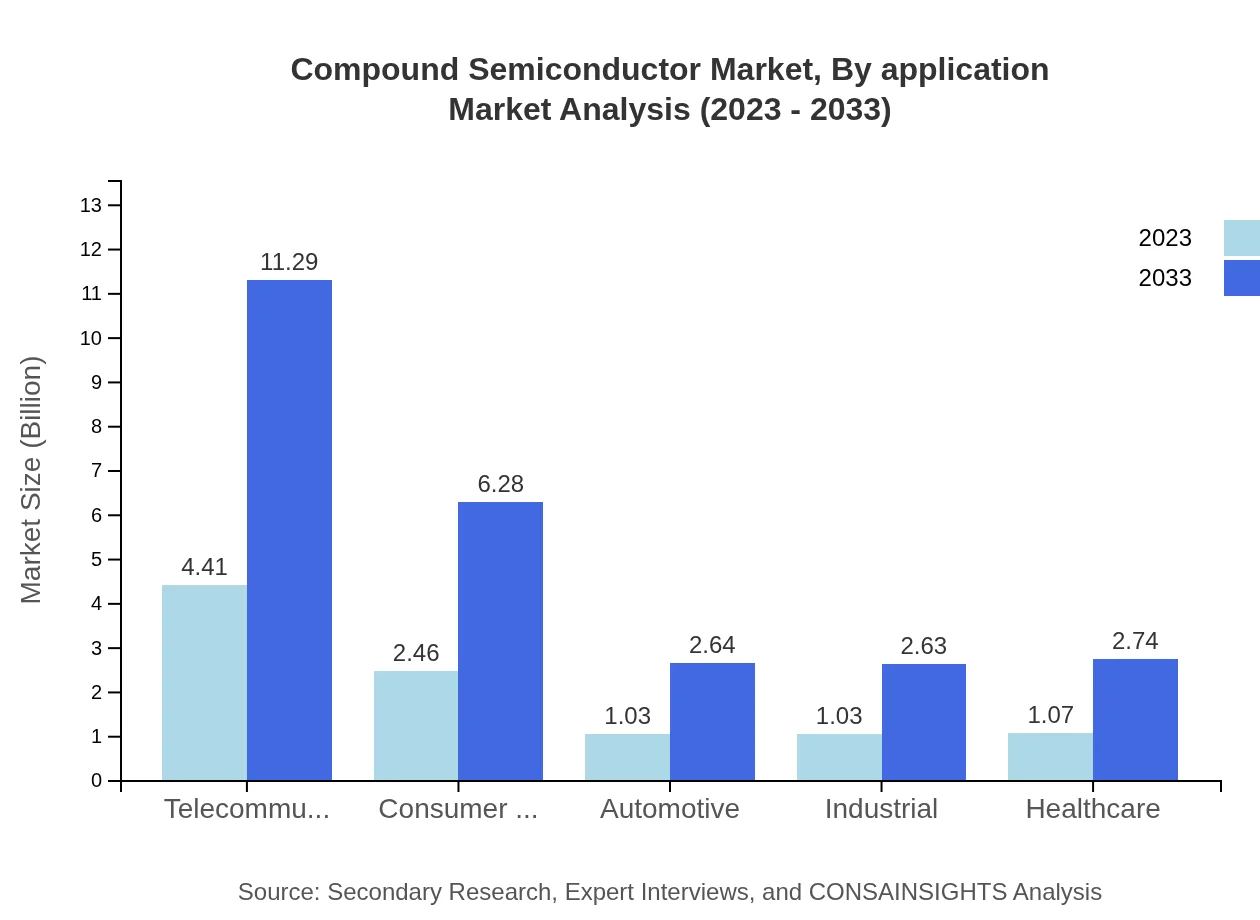

Compound Semiconductor Market Analysis By Application

Telecommunications leads the application segment with a market size of 4.41 billion USD in 2023 and is expected to reach 11.29 billion USD by 2033, capturing 44.12% market share. Consumer Electronics follows with 2.46 billion USD in 2023, growing to 6.28 billion USD by 2033. Automotive applications are progressively gaining importance, increasing from 1.03 billion USD to 2.64 billion USD in the same period.

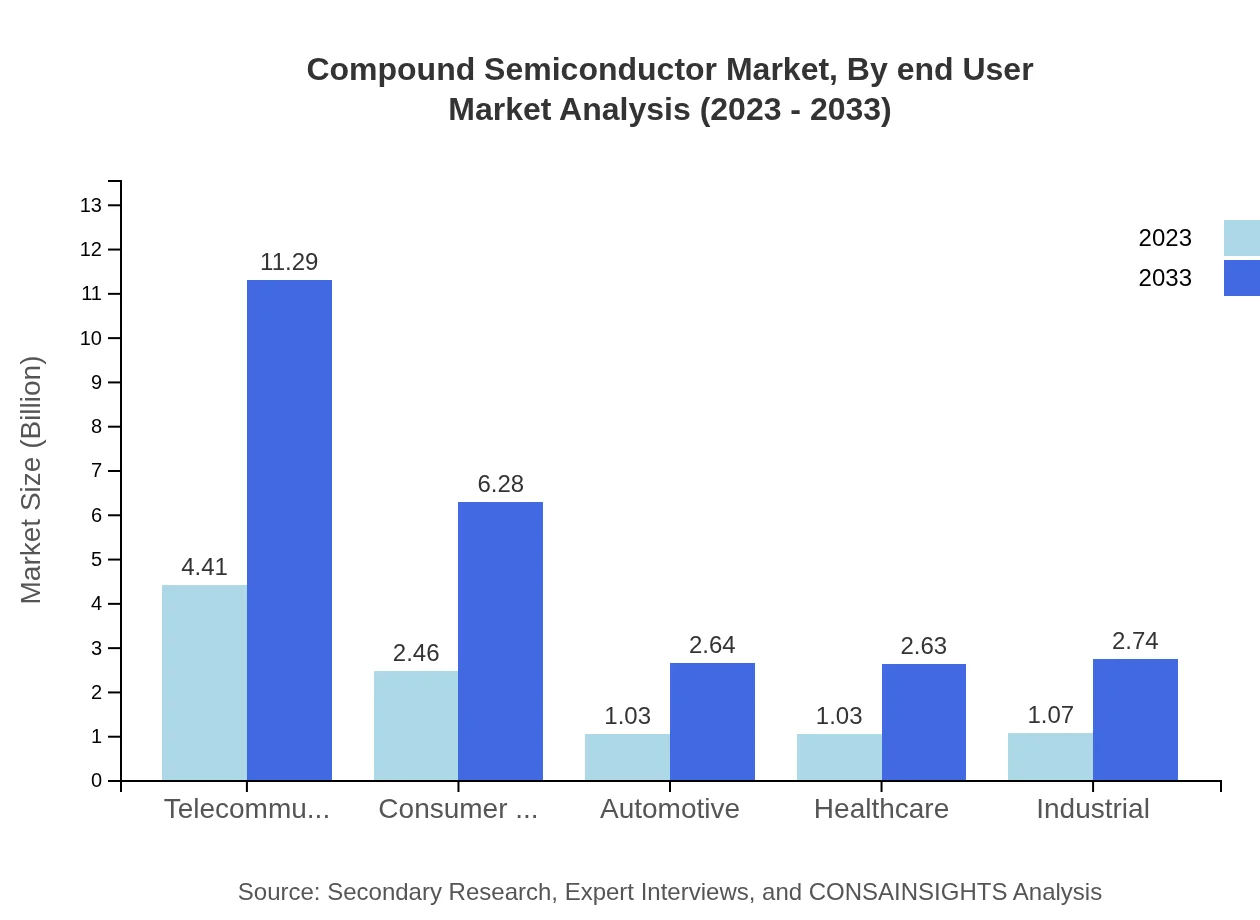

Compound Semiconductor Market Analysis By End User

The automotive sector shows a significant presence in the compound semiconductor market, with its size expected to grow from 1.03 billion USD in 2023 to 2.64 billion USD by 2033. Telecommunications continues to dominate the end-user industry, driven by the 5G deployment with an expansion from 4.41 billion USD to 11.29 billion USD, underscoring its vital role in future connectivity solutions.

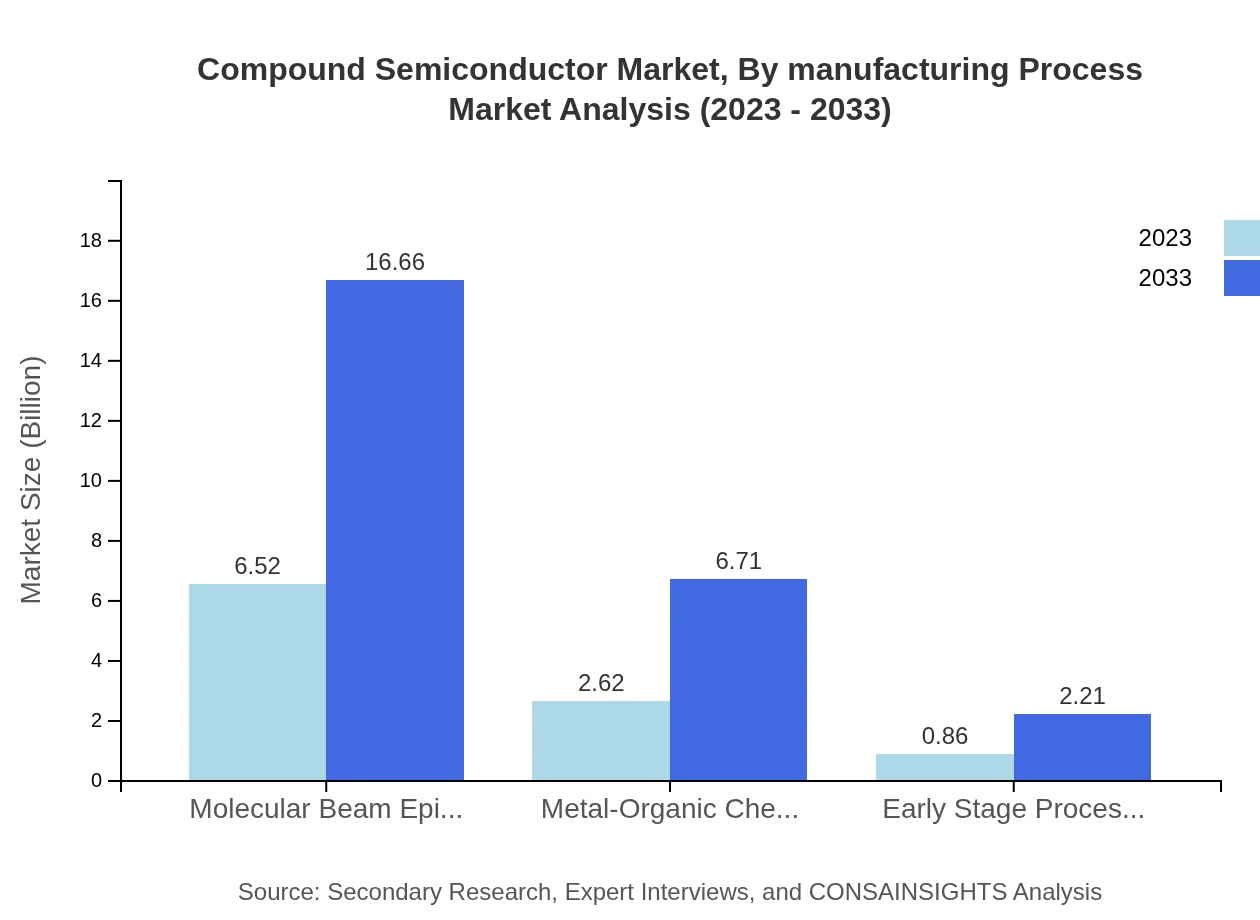

Compound Semiconductor Market Analysis By Manufacturing Process

Molecular Beam Epitaxy (MBE) remains the leading manufacturing process with a market size of 6.52 billion USD growing to 16.66 billion USD by 2033. Metal-Organic Chemical Vapor Deposition (MOCVD) follows, expected to grow from 2.62 billion USD to 6.71 billion USD over the same period, supported by the rising demand for efficient, high-quality semiconductor devices.

Compound Semiconductor Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Compound Semiconductor Industry

Infineon Technologies AG:

A major player known for its innovations in automotive solutions and industrial applications, focusing on power semiconductors.Cree, Inc.:

A leading innovator in SiC technology, important for electric vehicles and renewable energy solutions.Qualcomm Incorporated:

Renowned for semiconductor solutions in telecommunications, significantly contributing to the 5G transformation.NXP Semiconductors N.V.:

A global semiconductor leader focusing on secure connectivity solutions for automotive, IoT, and mobile sectors.Broadcom Inc.:

A key player in providing a range of semiconductor solutions, particularly in broadband and wireless applications.We're grateful to work with incredible clients.

FAQs

What is the market size of compound Semiconductor?

The compound semiconductor market was valued at $10 billion in 2023 and is projected to grow at a CAGR of 9.5%, reaching approximately $24.3 billion by 2033, indicating robust demand and expansion in various sectors.

What are the key market players or companies in the compound semiconductor industry?

Key players in the compound semiconductor industry include major corporations such as Cree, RF Micro Devices, and II-VI Incorporated, which dominate the market with their innovative technologies and extensive product portfolios.

What are the primary factors driving the growth in the compound semiconductor industry?

The growth in the compound semiconductor industry is driven by the increasing demand for high-performance electronic devices, advancements in wireless communication technologies, and the rise in applications across sectors such as automotive and consumer electronics.

Which region is the fastest Growing in the compound semiconductor?

The fastest-growing region in the compound semiconductor market is North America, with the market expanding from $3.59 billion in 2023 to $9.18 billion by 2033, fueled by technological advancements and investments in high-tech industries.

Does ConsaInsights provide customized market report data for the compound semiconductor industry?

Yes, ConsaInsights offers customized market report data tailored to your specific needs in the compound semiconductor industry, enabling you to gain detailed insights based on your unique business requirements.

What deliverables can I expect from this compound semiconductor market research project?

Deliverables include comprehensive market analysis reports, detailed segmentation data, competitive landscape assessments, and forecasts that cater specifically to your needs in the compound semiconductor industry.

What are the market trends of compound semiconductor?

Key market trends include a shift towards more efficient materials like Gallium Nitride (GaN) and Silicon Carbide (SiC), increasing investments in research and development, and a growing emphasis on renewable energy applications.