Data Center Accelerator Market Report

Published Date: 31 January 2026 | Report Code: data-center-accelerator

Data Center Accelerator Market Size, Share, Industry Trends and Forecast to 2033

This report provides an in-depth analysis of the Data Center Accelerator market, offering insights into its growth trajectory, key drivers, market size, and future forecasts from 2023 to 2033, along with detailed regional and segment analyses.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

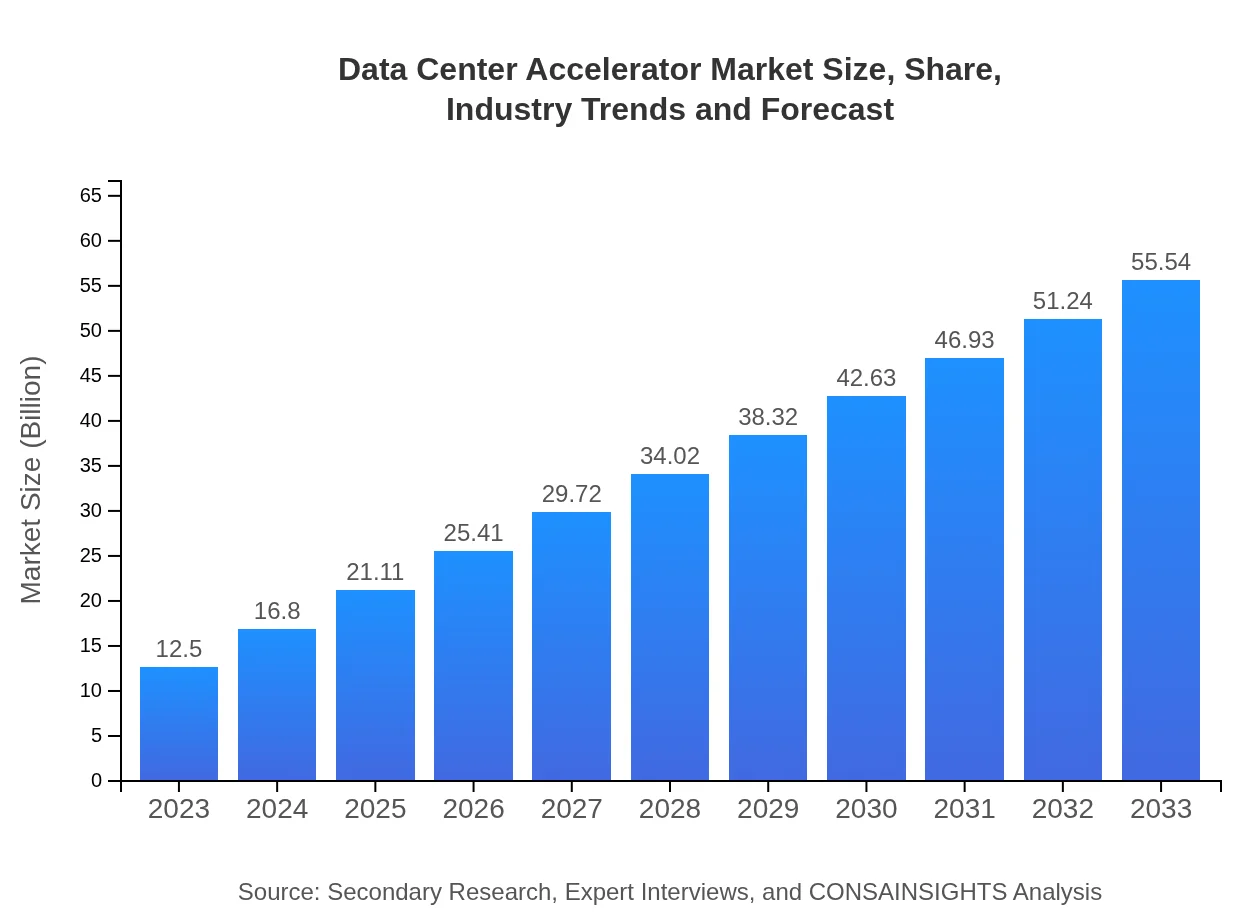

| 2023 Market Size | $12.50 Billion |

| CAGR (2023-2033) | 15.3% |

| 2033 Market Size | $55.54 Billion |

| Top Companies | NVIDIA Corporation, Intel Corporation, Advanced Micro Devices, Inc. (AMD), Amazon Web Services (AWS), Google Cloud |

| Last Modified Date | 31 January 2026 |

Data Center Accelerator Market Overview

Customize Data Center Accelerator Market Report market research report

- ✔ Get in-depth analysis of Data Center Accelerator market size, growth, and forecasts.

- ✔ Understand Data Center Accelerator's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Data Center Accelerator

What is the Market Size & CAGR of the Data Center Accelerator market in 2033?

Data Center Accelerator Industry Analysis

Data Center Accelerator Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Data Center Accelerator Market Analysis Report by Region

Europe Data Center Accelerator Market Report:

The European market is projected to grow significantly from $3.04 billion in 2023 to $13.50 billion by 2033. Increased demand for compliance and data regulation compliance as well as the European Union's push for a digitalized economy boost the investment in data center solutions in this region.Asia Pacific Data Center Accelerator Market Report:

The Asia-Pacific region is forecasted to showcase robust growth with the market expected to reach $11.47 billion by 2033, compared to $2.58 billion in 2023. Factors such as rapid digital transformation, increasing cloud computing adoption, and enhanced investments in data centre infrastructure propel market growth in this region.North America Data Center Accelerator Market Report:

North America continues to dominate the Data Center Accelerator market, anticipated to expand from $4.68 billion in 2023 to $20.80 billion by 2033. Key drivers include the presence of major technology companies, a strong focus on advanced technology adoption, and a drive for data center optimization among American enterprises.South America Data Center Accelerator Market Report:

In South America, the market is expected to grow from $1.03 billion in 2023 to $4.58 billion by 2033, reflecting a compound growth driven by the digitization of businesses and investments in the healthcare and financial services sectors which demand high-performance computing.Middle East & Africa Data Center Accelerator Market Report:

In the Middle East and Africa, the Data Center Accelerator market is expected to grow from $1.17 billion in 2023 to $5.20 billion by 2033. This growth can be attributed to increasing technological advancements in the region, the growing importance of data centers for the business continuity in emerging economies, and investment in enhancing IT infrastructure.Tell us your focus area and get a customized research report.

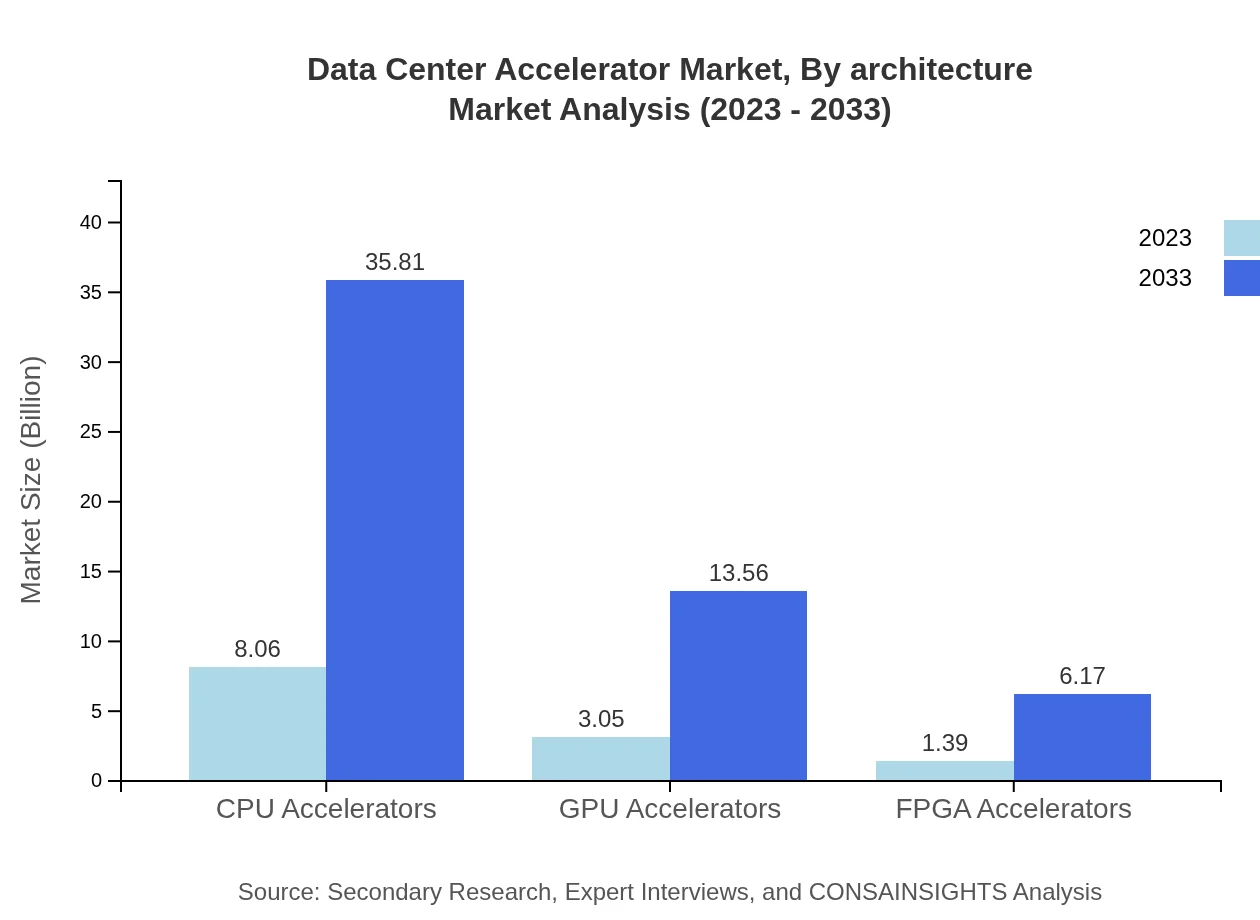

Data Center Accelerator Market Analysis By Architecture

The architecture segment includes key types such as ASIC (Application-Specific Integrated Circuits), which dominate the market due to their high performance for specific applications, especially in AI and machine learning. FPGAs (Field-Programmable Gate Arrays) offer programmability advantages, allowing users to optimize performance according to workload changes, whereas GPUs (Graphics Processing Units) are favored for parallel processing capabilities across various applications such as data analytics and video rendering, marking their significance in this growing sector.

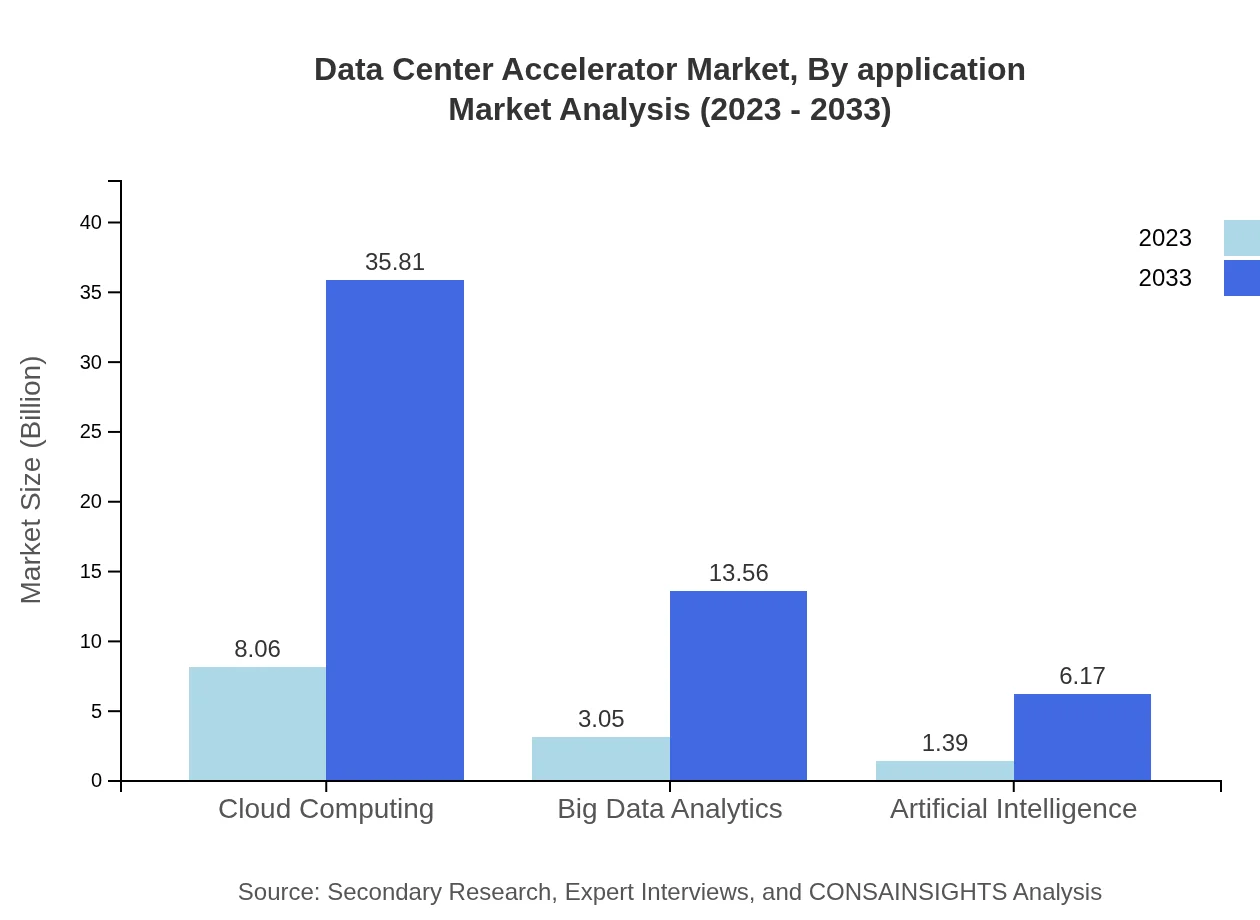

Data Center Accelerator Market Analysis By Application

Applications such as Cloud Computing, Big Data Analytics, and AI are at the forefront, driving market growth. Cloud Computing holds a significant market share, as businesses increasingly migrate to sustainable cloud solutions that enhance operational efficiency and lower costs. Big Data Analytics is crucial, with organizations leveraging high-performance computing to derive actionable insights from vast data sets. AI applications are multiplying, and the need for accelerators to enhance machine learning workloads underpins their critical role within this segment.

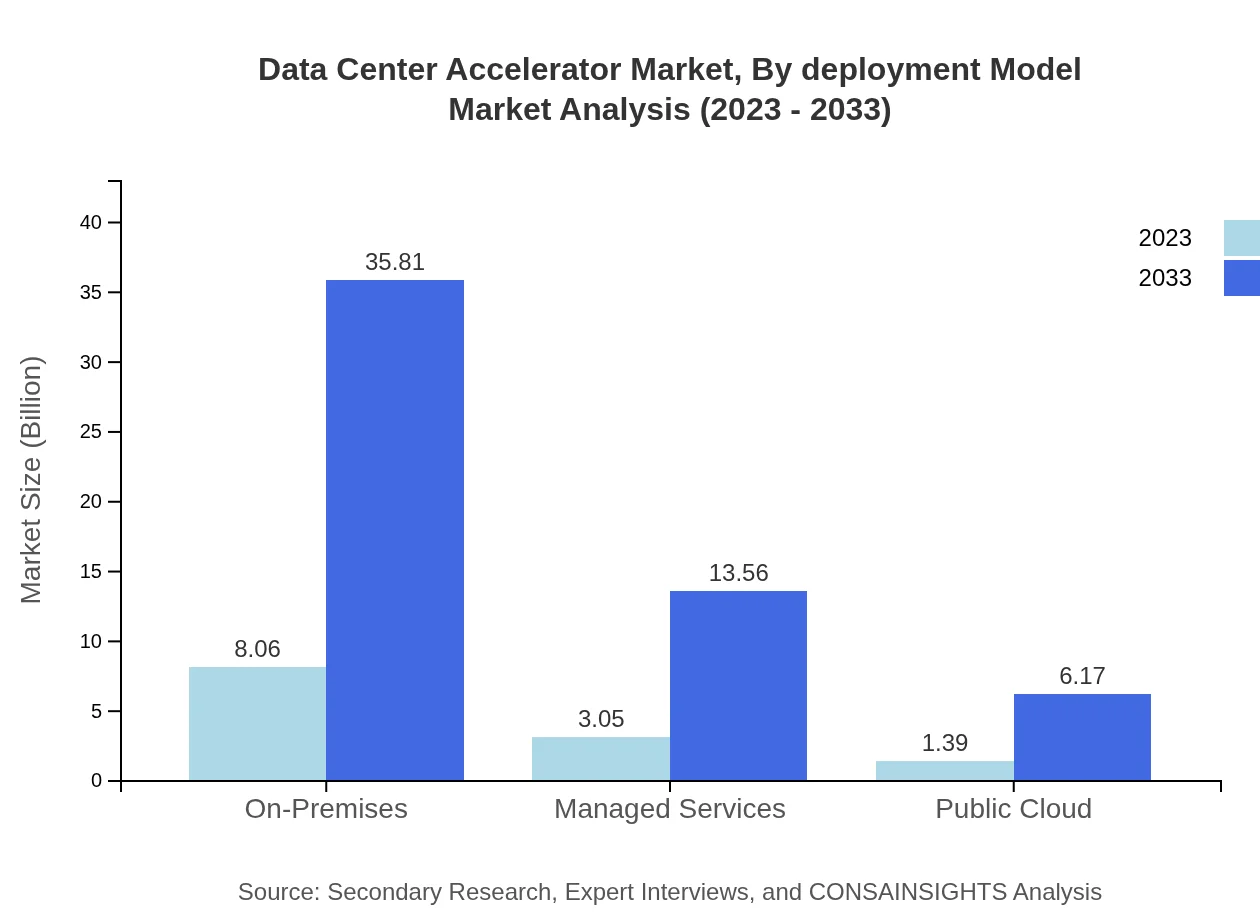

Data Center Accelerator Market Analysis By Deployment Model

The deployment model segment highlights the choice between On-Premises solutions and Managed Services. On-Premises models provide organizations complete control over their infrastructure and data, which is essential for highly regulated industries. However, Managed Services gain traction, offering flexibility and scalability without the heavy upfront costs associated with traditional setups, especially necessary for small to medium businesses.

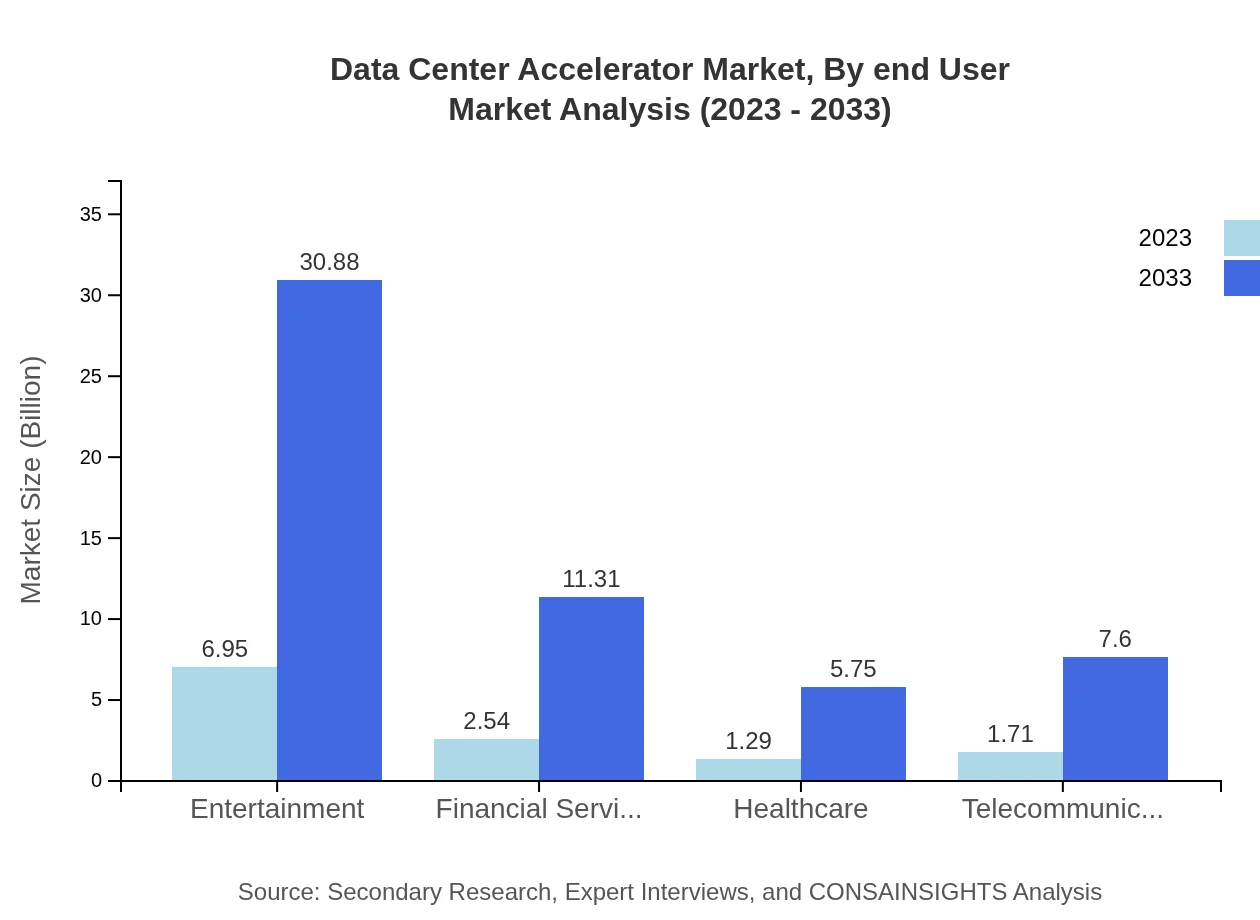

Data Center Accelerator Market Analysis By End User

End-user industries like Financial Services, Healthcare, Telecommunications, and Entertainment heavily rely on advanced data processing capabilities. Financial Services demand high-frequency data processing and security, Healthcare requires efficient large data storage and retrieval for patient information, Telecommunications seek low-latency solutions for service improvements, while Entertainment focuses on high-performance computing demands for content creation and distribution. These needs drive segment-specific innovativeness and investment in newer technologies.

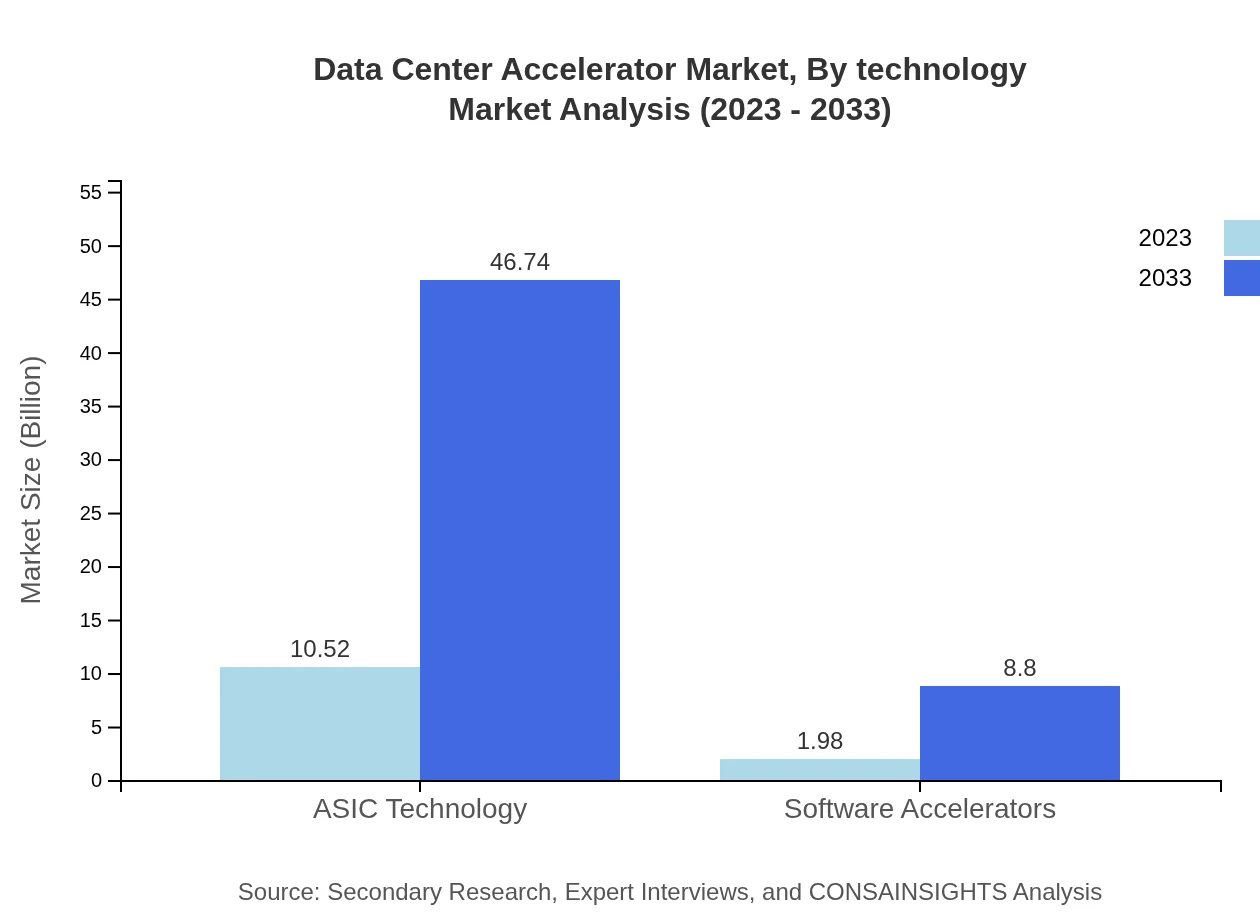

Data Center Accelerator Market Analysis By Technology

Innovations in technology segment, such as cloud technologies, AI enhancements in processing capabilities, and simplified integration systems, are crucial to the growth of the Data Center Accelerator market. Organizations benefit from emerging technologies improving processing times and reducing costs. The advent of software accelerators in combining hardware capabilities with software solutions enhances efficiency and meet modern use cases, enabling organizations to remain competitive.

Data Center Accelerator Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Data Center Accelerator Industry

NVIDIA Corporation:

NVIDIA is a global leader in the development of GPU accelerators that provide advanced computing performance for gaming, AI, and data analytics applications.Intel Corporation:

Intel is renowned for its processors and accelerator technologies, playing a significant role in Data Center performance enhancements through its range of AI and FPGA solutions.Advanced Micro Devices, Inc. (AMD):

AMD specializes in high-performance computing, including server-grade processors and GPU accelerators that advance cloud computing and data center capabilities.Amazon Web Services (AWS):

AWS is a major player in the cloud computing market, providing data center infrastructure and integrated solutions that leverage data-center accelerators for improved performance.Google Cloud:

Google Cloud provides innovative solutions that incorporate accelerators within its data centers to serve demanding workloads in machine learning and analytics.We're grateful to work with incredible clients.

FAQs

What is the market size of data Center Accelerator?

The global Data Center Accelerator market is projected to reach approximately $12.5 billion by 2033, growing from $4.68 billion in 2023, with a CAGR of 15.3%. This robust growth indicates a strong demand for advanced computing capabilities in data centers.

What are the key market players or companies in this data Center Accelerator industry?

Key players in the Data Center Accelerator industry include major tech corporations focused on optimizing computing performance. These may encompass companies like NVIDIA, AMD, Intel, and various cloud service providers that integrate accelerators into their offerings to enhance efficiency.

What are the primary factors driving the growth in the data Center Accelerator industry?

Growth in the Data Center Accelerator industry is primarily driven by the increasing demand for high-performance computing, expansion of AI applications, the rise of cloud services, and the necessity for efficient data processing across industries such as finance, healthcare, and telecommunications.

Which region is the fastest Growing in the data Center Accelerator?

The fastest-growing region in the Data Center Accelerator market is North America, expected to grow from $4.68 billion in 2023 to $20.80 billion by 2033. Following closely, Europe and Asia Pacific also show significant growth, indicating widespread adoption across these markets.

Does ConsaInsights provide customized market report data for the data Center Accelerator industry?

Yes, ConsaInsights offers customized market reports tailored to specific needs within the Data Center Accelerator sector, enabling stakeholders to obtain detailed insights into niche segments, geographical trends, and competitive analysis to support strategic decision-making.

What deliverables can I expect from this data Center Accelerator market research project?

From the Data Center Accelerator market research project, you can expect comprehensive reports detailing market size, growth forecasts, competitive landscape, segment analysis, and regional insights, as well as strategic recommendations for navigating the evolving market landscape.

What are the market trends of data Center Accelerator?

Trends in the Data Center Accelerator market include increasing investment in AI and machine learning capabilities, a surge in demand for cloud computing services, and advancements in accelerator technology. Growing reliance on big data analytics is also significantly influencing market dynamics.