Dry Eye Disease Market Report

Published Date: 31 January 2026 | Report Code: dry-eye-disease

Dry Eye Disease Market Size, Share, Industry Trends and Forecast to 2033

This report provides a comprehensive analysis of the Dry Eye Disease market, covering key insights, market trends, and forecasts for the period 2023 to 2033. It includes in-depth market segmentation, regional analyses, and an overview of major players in the industry.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

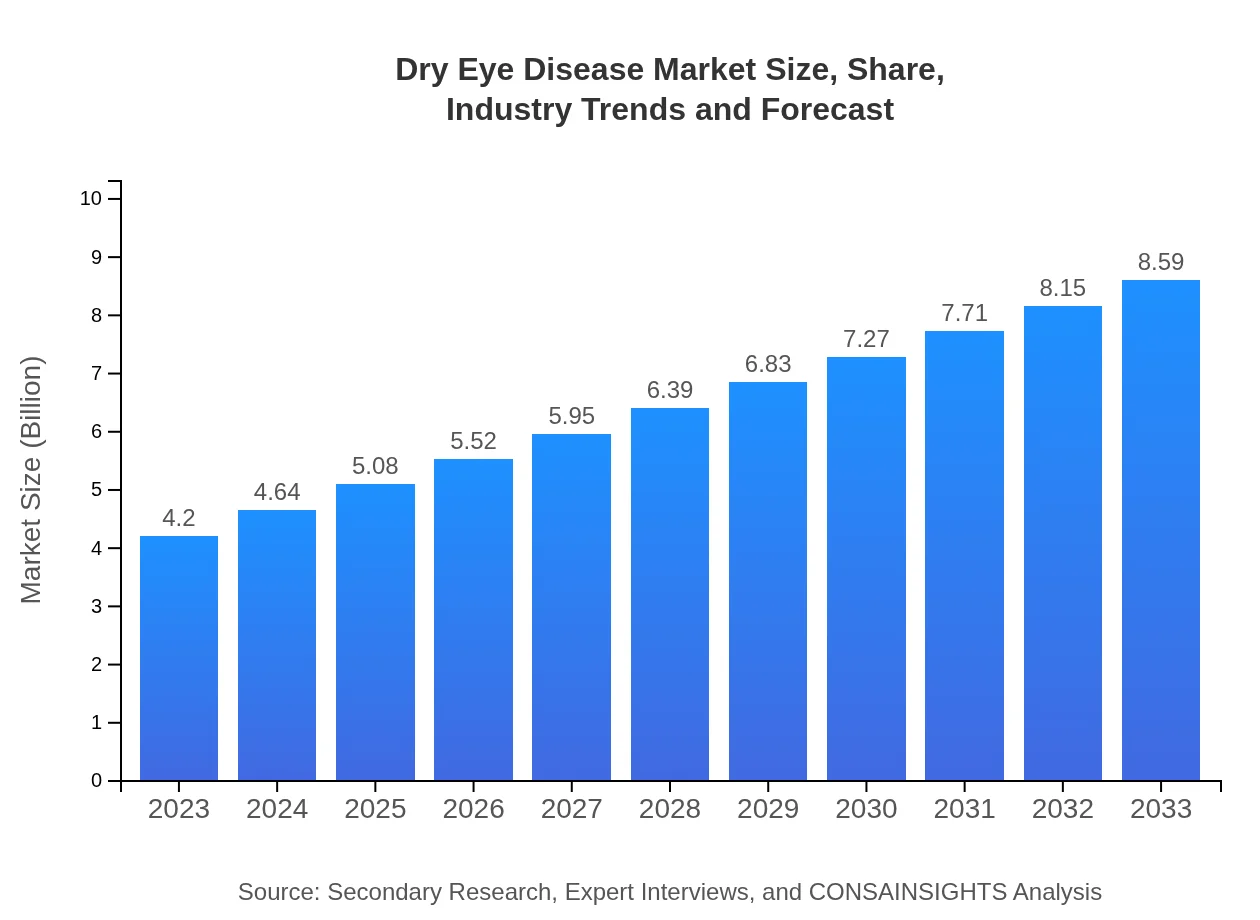

| 2023 Market Size | $4.20 Billion |

| CAGR (2023-2033) | 7.2% |

| 2033 Market Size | $8.59 Billion |

| Top Companies | Allergan, Inc., Santen Pharmaceutical Co., Ltd., Novartis AG, Bausch Health Companies Inc. |

| Last Modified Date | 31 January 2026 |

Dry Eye Disease Market Overview

Customize Dry Eye Disease Market Report market research report

- ✔ Get in-depth analysis of Dry Eye Disease market size, growth, and forecasts.

- ✔ Understand Dry Eye Disease's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Dry Eye Disease

What is the Market Size & CAGR of Dry Eye Disease market in 2023?

Dry Eye Disease Industry Analysis

Dry Eye Disease Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Dry Eye Disease Market Analysis Report by Region

Europe Dry Eye Disease Market Report:

The European market is expected to expand from USD 1.10 billion in 2023 to USD 2.24 billion by 2033. Factors such as stringent regulatory frameworks and increased collaboration between healthcare entities and pharmaceutical companies contribute positively to growth in this region.Asia Pacific Dry Eye Disease Market Report:

The Asia Pacific region is projected to witness substantial growth, with the market expected to grow from USD 0.88 billion in 2023 to USD 1.79 billion in 2033. This region's growth is fueled by an increasing population, rising awareness of eye health, and advancements in treatment modalities.North America Dry Eye Disease Market Report:

North America remains a leader in the Dry Eye Disease market, with projections indicating market growth from USD 1.47 billion in 2023 to USD 3.01 billion by 2033. This growth is driven by advanced healthcare infrastructure, high treatment awareness, and a robust pipeline of innovative treatments.South America Dry Eye Disease Market Report:

In South America, the Dry Eye Disease market is anticipated to increase from USD 0.42 billion in 2023 to USD 0.85 billion in 2033. The surge can be attributed to growing healthcare access, rising disposable incomes, and increasing prevalence of eye disorders.Middle East & Africa Dry Eye Disease Market Report:

The Middle East and Africa market, though smaller, is still anticipated to grow from USD 0.34 billion in 2023 to USD 0.69 billion by 2033. This growth is driven by increasing healthcare investment and rising awareness about eye health-related issues.Tell us your focus area and get a customized research report.

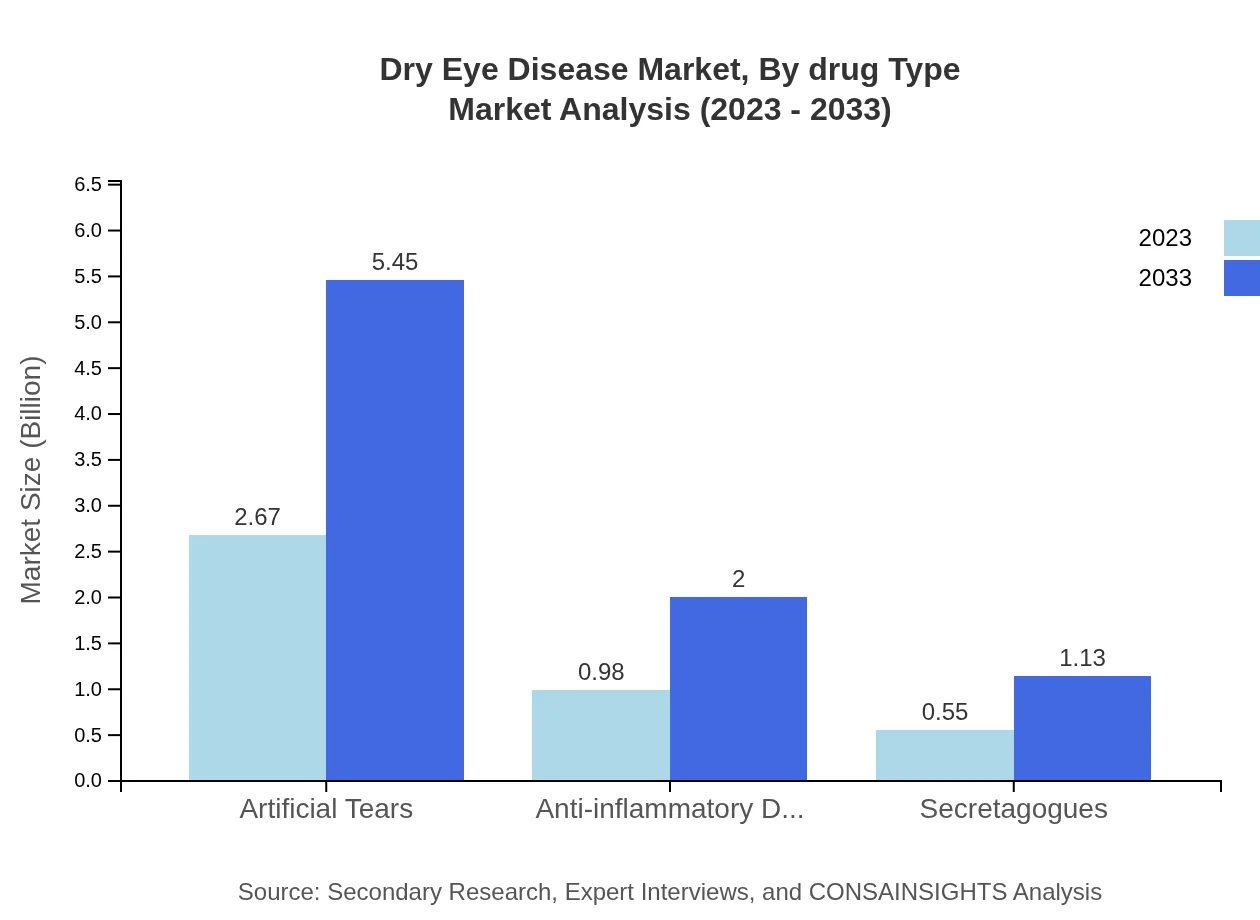

Dry Eye Disease Market Analysis By Drug Type

By drug type, Artificial Tears dominate the market, with a size of USD 2.67 billion in 2023, expected to rise to USD 5.45 billion by 2033. Anti-inflammatory Drugs hold the second position, projected to grow from USD 0.98 billion to USD 2.00 billion in the same period.

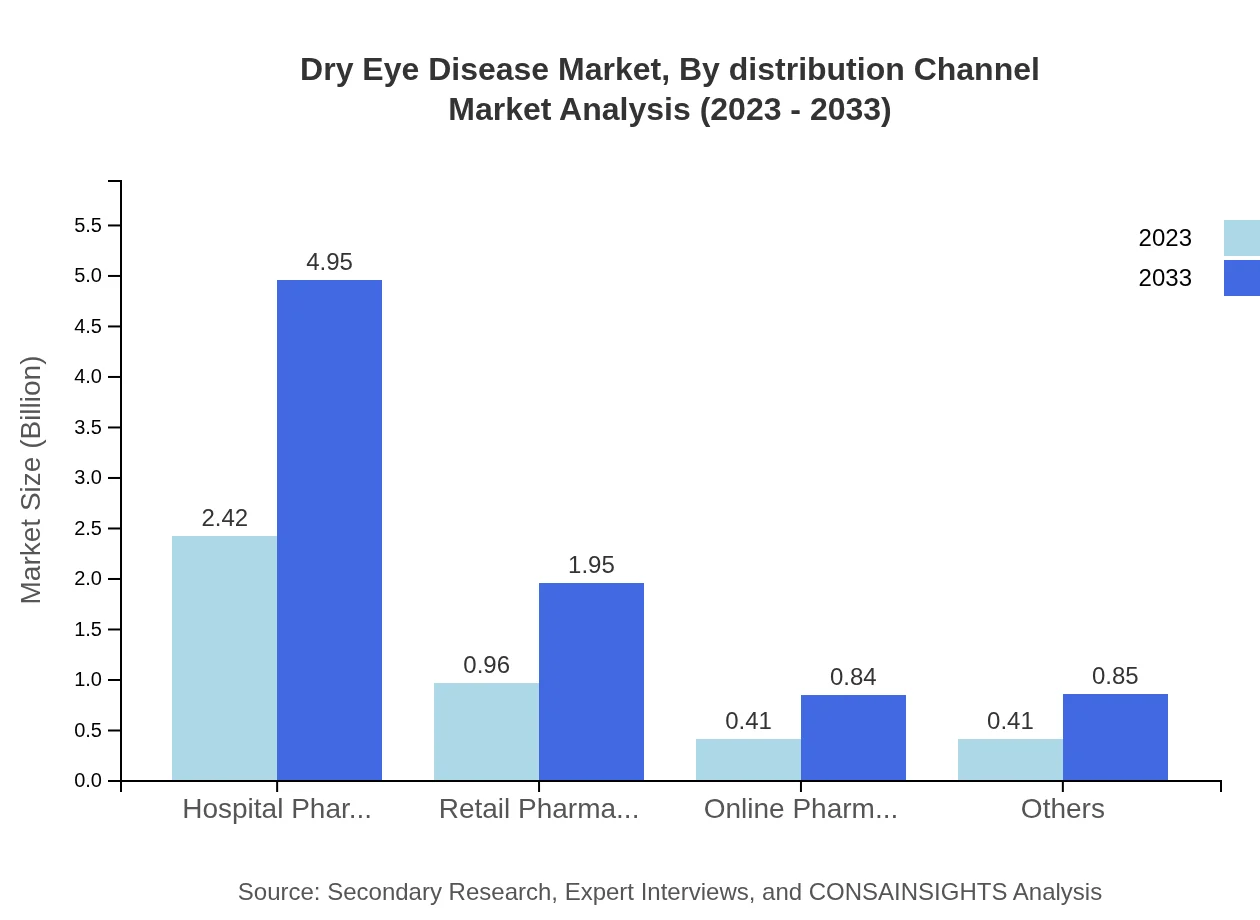

Dry Eye Disease Market Analysis By Distribution Channel

Hospital Pharmacies account for the largest share, commanding market sizes of USD 2.42 billion in 2023 and expected to reach USD 4.95 billion by 2033. Retail Pharmacies also contribute significantly with projected growth from USD 0.96 billion to USD 1.95 billion.

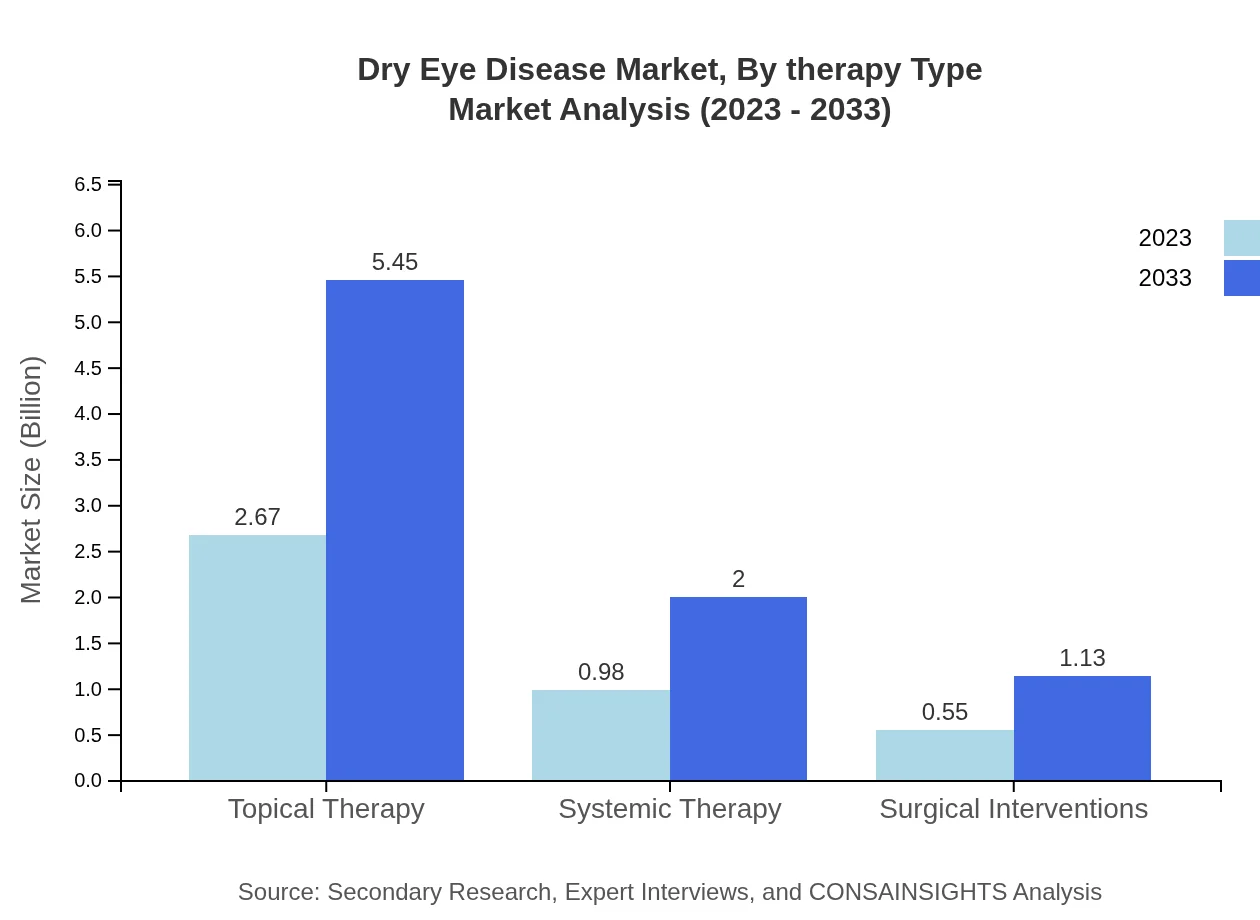

Dry Eye Disease Market Analysis By Therapy Type

Topical Therapy leads the segment with a market size of USD 2.67 billion in 2023, rising to USD 5.45 billion by 2033, highlighting the focus on localized treatment options. Systemic Therapy follows, increasing from USD 0.98 billion to USD 2.00 billion during the forecast period.

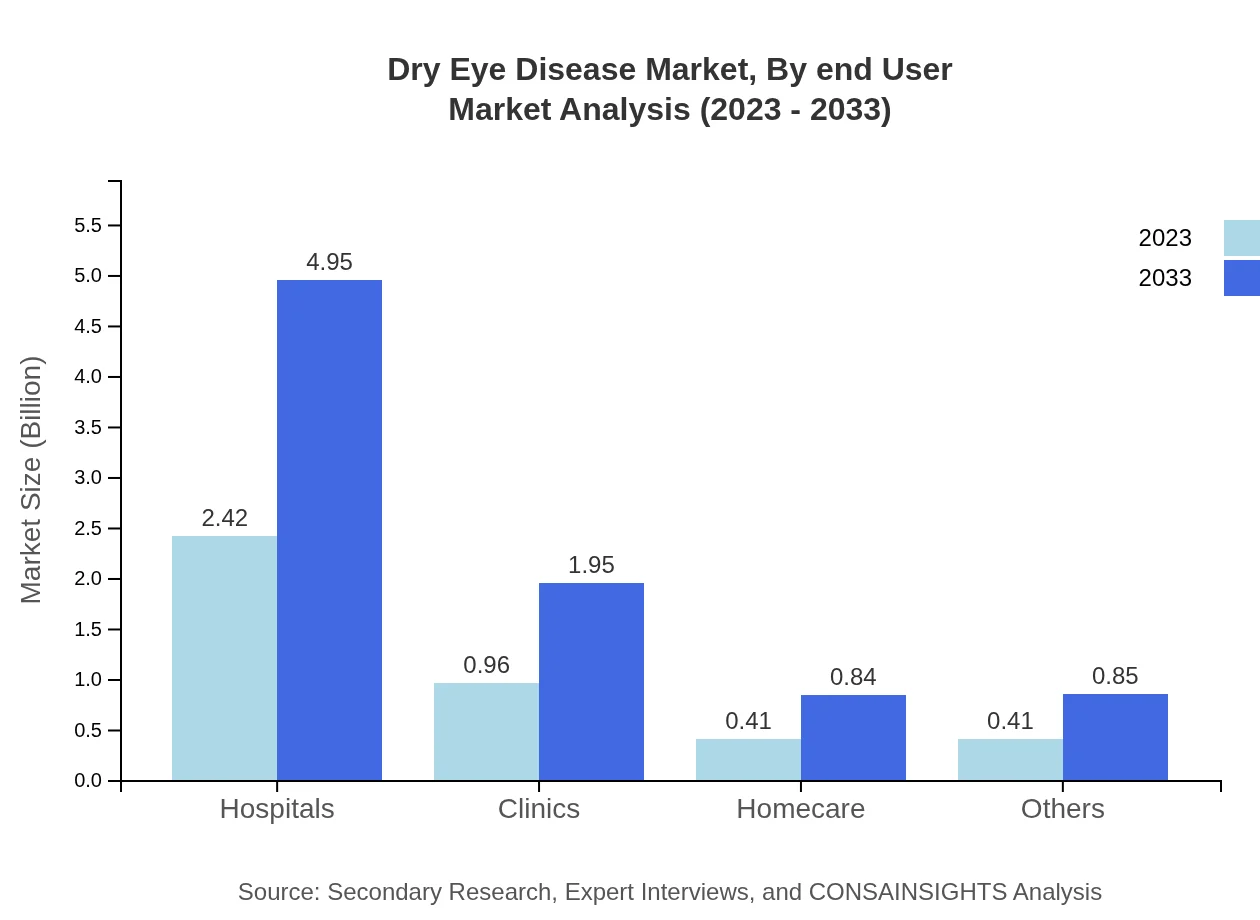

Dry Eye Disease Market Analysis By End User

The market by end-user shows Hospitals as the major player, with a market size projected to expand from USD 2.42 billion in 2023 to USD 4.95 billion by 2033, reflecting the demand for comprehensive care facilities in managing DED.

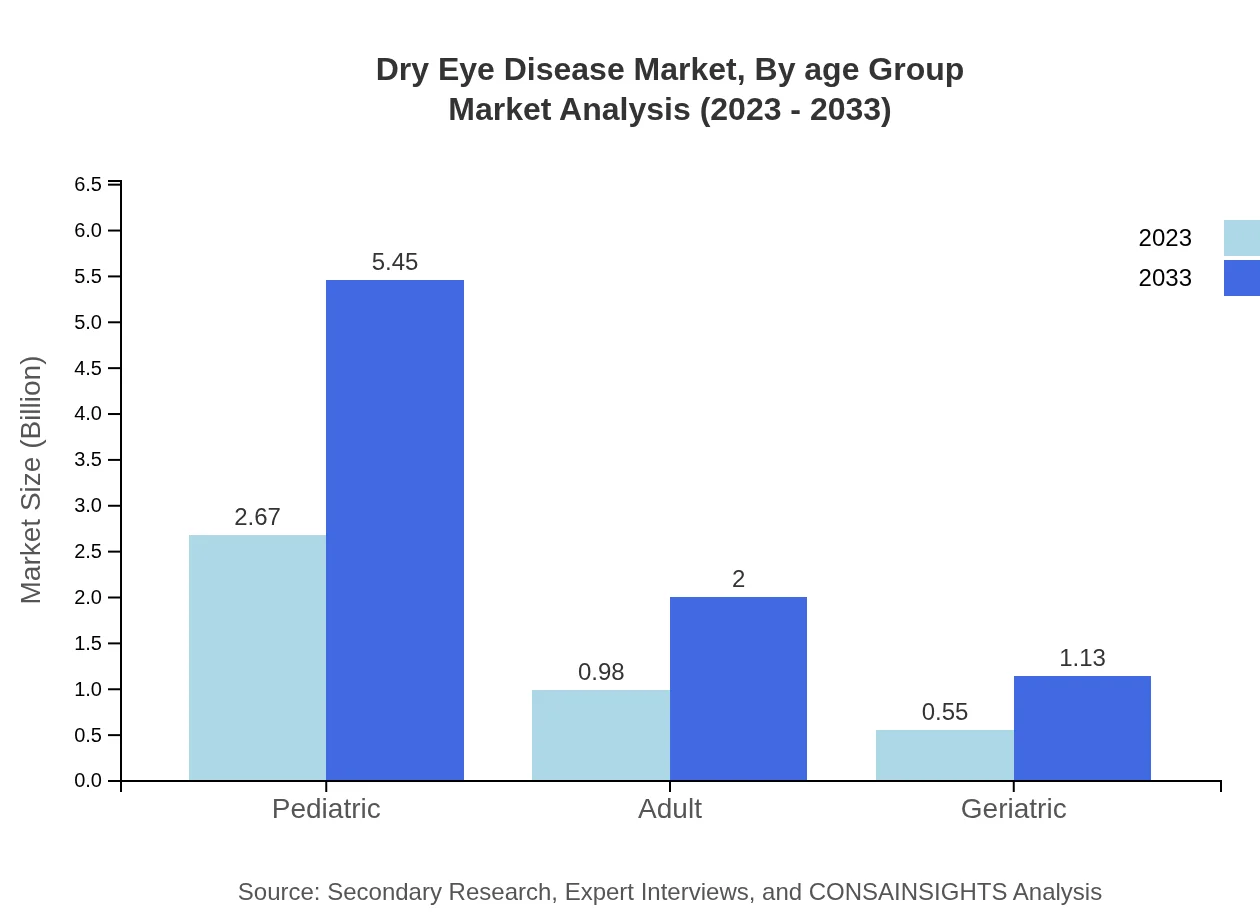

Dry Eye Disease Market Analysis By Age Group

The Pediatric segment leads in market share, with a size of USD 2.67 billion in 2023, growing to USD 5.45 billion by 2033, highlighting the essential considerations for younger patients. Adult and Geriatric groups follow, with respective projections showing a significant increase, meeting their unique ocular health needs.

Dry Eye Disease Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Dry Eye Disease Industry

Allergan, Inc.:

Known for its extensive portfolio of eye care products, Allergan leads in the development of innovative therapeutics for Dry Eye Disease, including Restasis.Santen Pharmaceutical Co., Ltd.:

A prominent player focusing on developing and marketing ophthalmic products, Santen is recognized for its expertise in Dry Eye Disease treatments.Novartis AG:

With a commitment to ophthalmology, Novartis invests significantly in research and development to bring novel solutions for those suffering from Dry Eye Disease.Bausch Health Companies Inc.:

Bausch Health is a global leader in eye health products, offering a range of therapies aimed at improving ocular surface health and managing Dry Eye Disease.We're grateful to work with incredible clients.

FAQs

What is the market size of dry Eye Disease?

The dry eye disease market is projected to reach a size of $4.2 billion by 2033, growing at a CAGR of 7.2%. This growth reflects increasing awareness, rising patient populations, and advancements in treatment options.

What are the key market players or companies in this dry Eye Disease industry?

Key market players in the dry eye disease industry include major pharmaceutical companies. They are investing in innovative therapies and are engaged in strategic partnerships to enhance product offerings and strengthen their market position.

What are the primary factors driving the growth in the dry Eye Disease industry?

The primary factors driving growth in the dry eye disease market include an increase in the aging population, higher prevalence rates, advancements in treatment solutions, and growing awareness about eye health which collectively enhance the demand for effective therapies.

Which region is the fastest Growing in the dry Eye Disease?

The fastest-growing region in the dry eye disease market is North America, which is projected to reach $3.01 billion by 2033. This growth is fueled by increasing healthcare spending and awareness about eye diseases in the region.

Does ConsaInsights provide customized market report data for the dry Eye Disease industry?

Yes, ConsaInsights offers customized market report data for the dry eye disease industry, allowing clients to gain tailored insights that align with specific business needs, ensuring relevant and actionable market intelligence.

What deliverables can I expect from this dry Eye Disease market research project?

From this market research project, you can expect comprehensive deliverables including detailed market analysis, competitive landscape insights, trend evaluations, and forecasts segmented by regions and product types for strategic planning.

What are the market trends of dry Eye Disease?

Current market trends in dry eye disease include a surge in demand for artificial tears and topical therapies. There is also a growing trend towards personalized medicine and integrated healthcare approaches to enhance patient outcomes.