Reports >

Life Sciences

>

Hematology Analyzers Market Report

Hematology Analyzers Market Report

Published Date: 31 January 2026 | Report Code: hematology-analyzers

Hematology Analyzers Market Size, Share, Industry Trends and Forecast to 2033

This report provides an in-depth analysis of the Hematology Analyzers market, focusing on market trends, forecasts, and industry dynamics from 2023 to 2033. It offers insights into market sizes, key segments, regional performances, and the competitive landscape.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

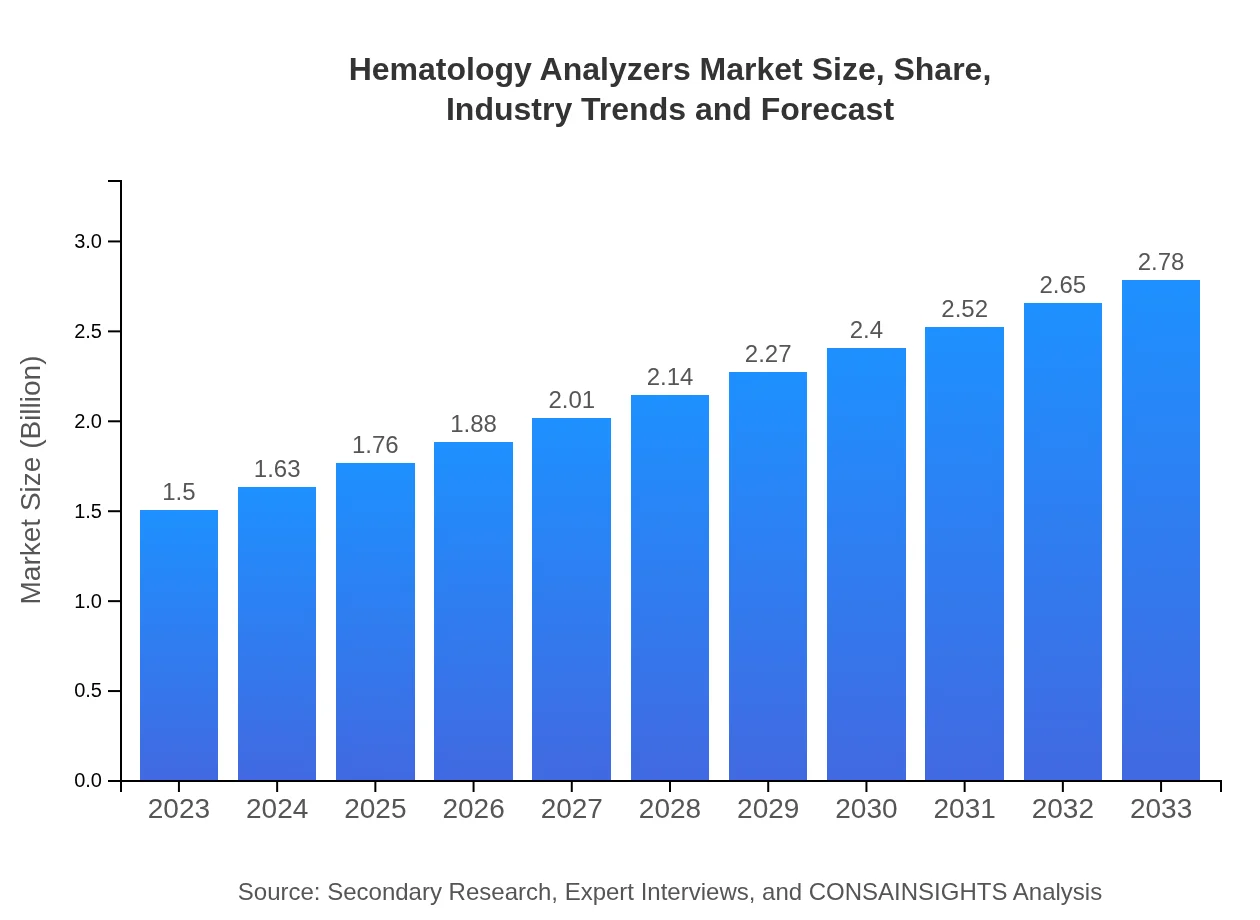

| 2023 Market Size | $1.50 Billion |

| CAGR (2023-2033) | 6.2% |

| 2033 Market Size | $2.78 Billion |

| Top Companies | Abbott Laboratories, Roche Diagnostics, Beckman Coulter, Sysmex Corporation, Mindray Medical International Limited |

| Last Modified Date | 31 January 2026 |

Hematology Analyzers Market Overview

Customize Hematology Analyzers Market Report market research report

- ✔ Get in-depth analysis of Hematology Analyzers market size, growth, and forecasts.

- ✔ Understand Hematology Analyzers's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Hematology Analyzers

What is the Market Size & CAGR of Hematology Analyzers market in 2023?

Hematology Analyzers Industry Analysis

Hematology Analyzers Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Hematology Analyzers Market Analysis Report by Region

Europe Hematology Analyzers Market Report:

In Europe, the Hematology Analyzers market is expected to grow from $0.46 billion in 2023 to $0.85 billion by 2033. Key drivers include stringent regulations regarding healthcare standards and increasing investments in laboratory equipment, with countries like Germany and the UK leading in market share.Asia Pacific Hematology Analyzers Market Report:

In the Asia-Pacific region, the Hematology Analyzers market is projected to grow from $0.29 billion in 2023 to $0.54 billion by 2033, driven by increasing healthcare investments, improving healthcare infrastructure, and rising incidences of blood disorders within the region. Countries like China and India are key markets due to their large population base and rising demand for medical services.North America Hematology Analyzers Market Report:

North America stands as the largest market, anticipated to rise from $0.50 billion in 2023 to $0.93 billion by 2033. The market's growth in this region is spurred by advanced healthcare infrastructure, high adoption rates of new technologies, and rising awareness about the diagnostics of hematological diseases.South America Hematology Analyzers Market Report:

The South American market is expected to increase from $0.04 billion in 2023 to $0.07 billion by 2033. The growth is attributed to the rising demand for improved healthcare systems in countries like Brazil and Argentina, addressing the need for efficient diagnostic processes in hospitals.Middle East & Africa Hematology Analyzers Market Report:

The Middle East and Africa market is projected to move from $0.21 billion in 2023 to $0.39 billion by 2033, benefitting from the expansion of healthcare facilities, increasing awareness of diagnostic procedures, and a gradual shift towards advanced medical technologies.Tell us your focus area and get a customized research report.

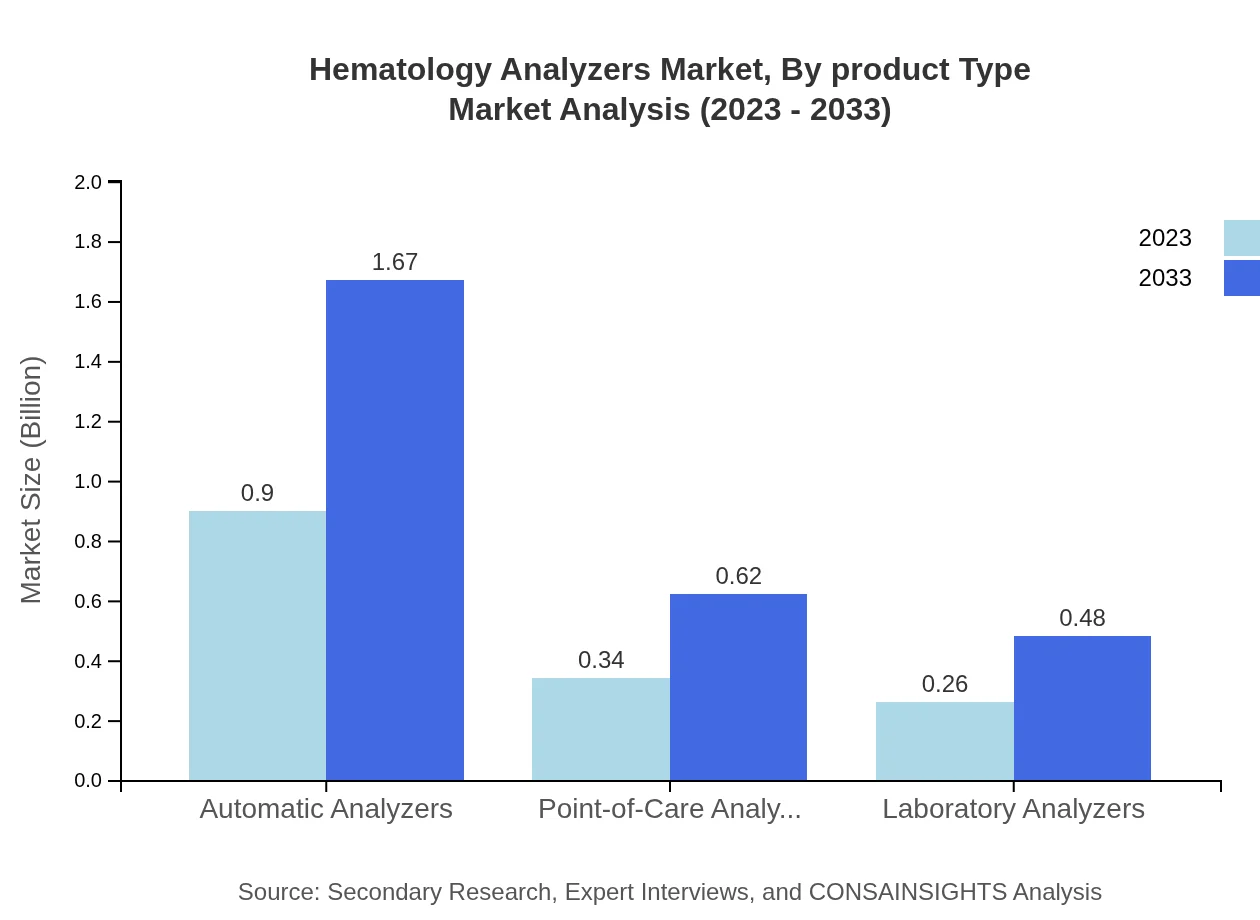

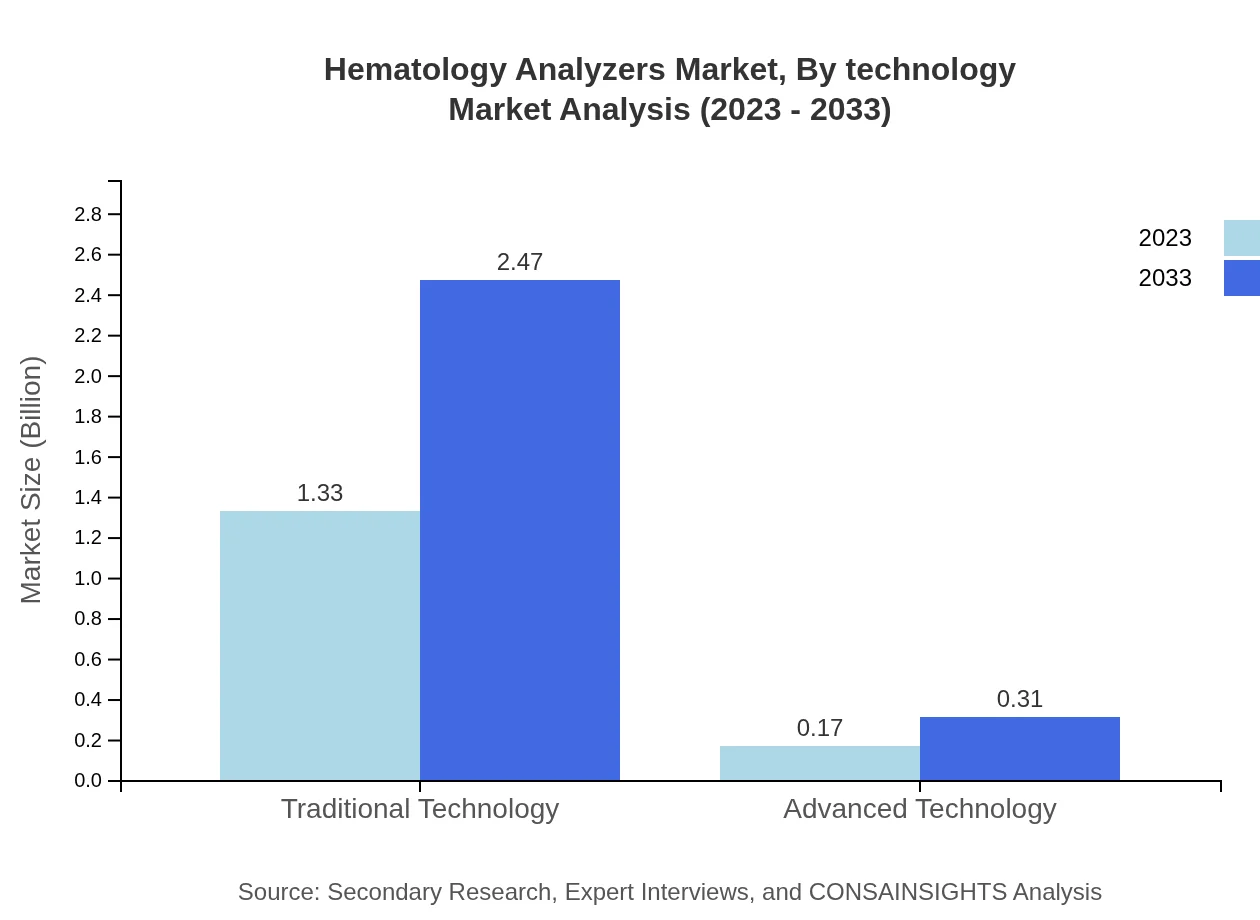

Hematology Analyzers Market Analysis By Product Type

The market is segmented into Traditional Technology and Advanced Technology. Traditional Analyzers hold a dominant share, expected to generate $1.33 billion in 2023, growing to $2.47 billion by 2033. Advanced Analyzers represent a growing segment with $0.17 billion in 2023, projected to reach $0.31 billion by 2033, supported by innovations in precision and speed.

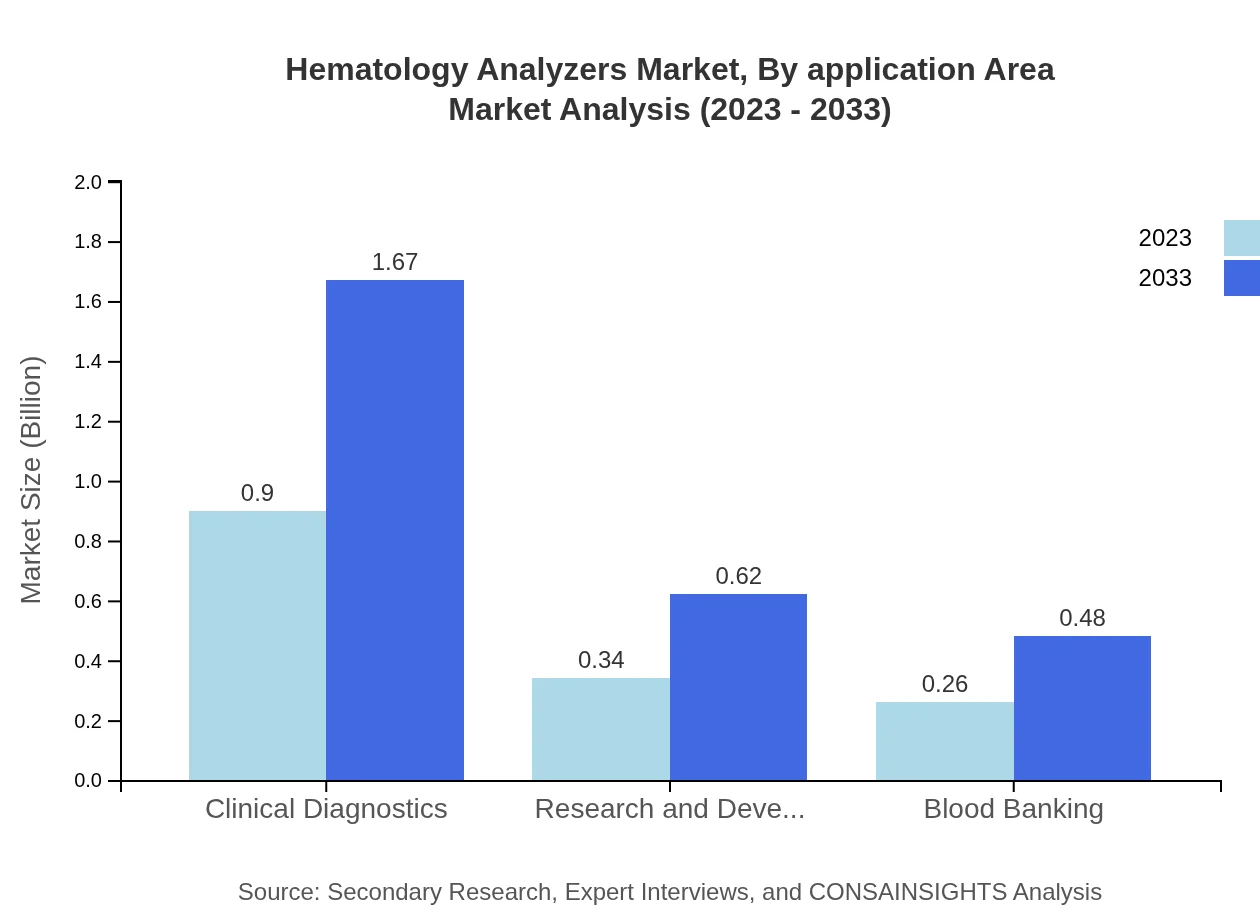

Hematology Analyzers Market Analysis By Application Area

Key applications include Clinical Diagnostics, Research and Development, and Blood Banking. Clinical Diagnostics is the leading segment, with projected growth from $0.90 billion in 2023 to $1.67 billion by 2033. Research and Development, valued at $0.34 billion in 2023, is forecasted to increase to $0.62 billion, reflecting growing R&D activities in healthcare.

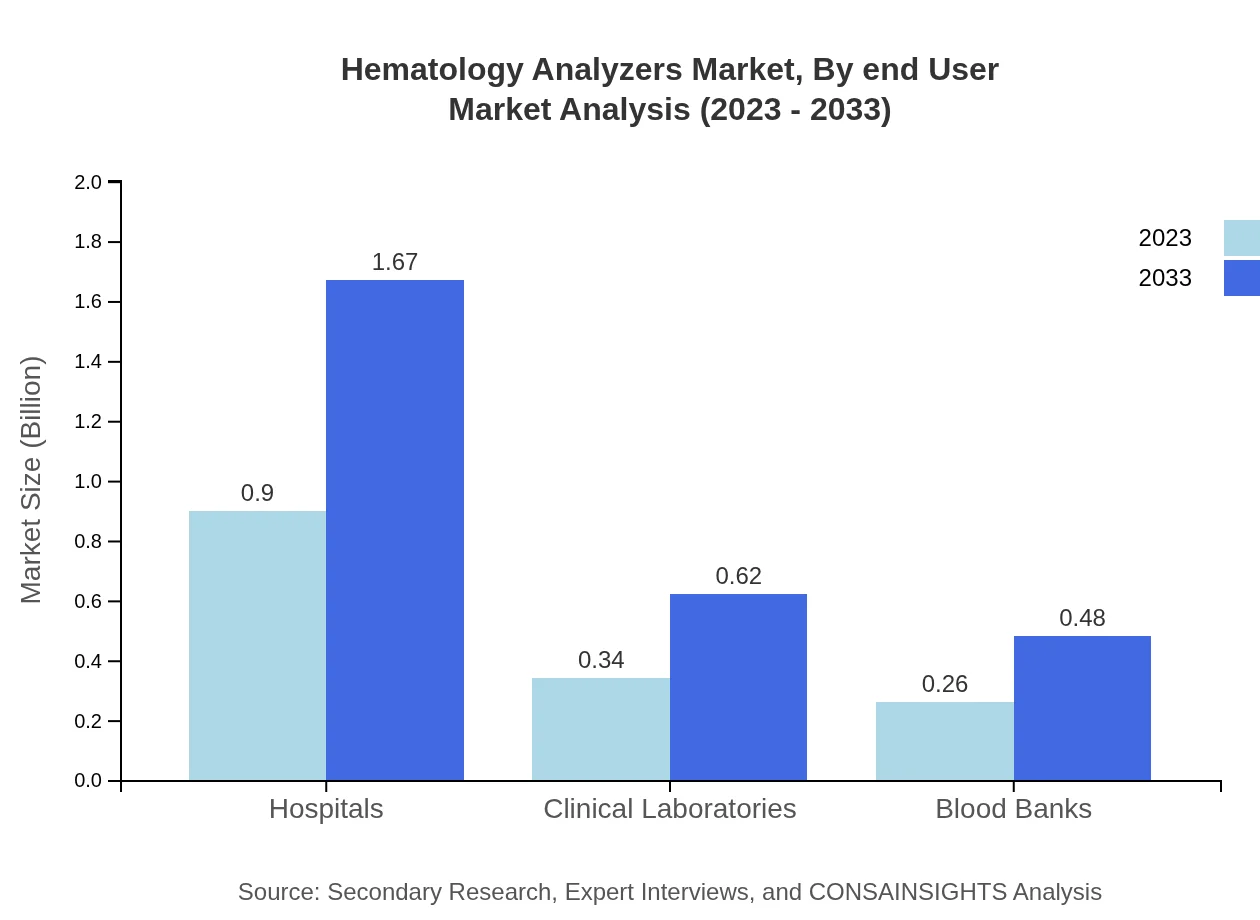

Hematology Analyzers Market Analysis By End User

Hospitals are the primary end-users of hematology analyzers, with a market valuation rising from $0.90 billion in 2023 to $1.67 billion by 2033. Clinical laboratories and blood banks follow, showcasing significant market shares that reflect their reliance on effective diagnostic tools.

Hematology Analyzers Market Analysis By Technology

Hematology analyzers utilize automatic and manual technologies. Automatic analyzers dominate, projected to maintain a market size of $0.90 billion in 2023 and growing to $1.67 billion by 2033. Point-of-care technologies are also gaining traction, increasing in relevance for rapid testing capabilities.

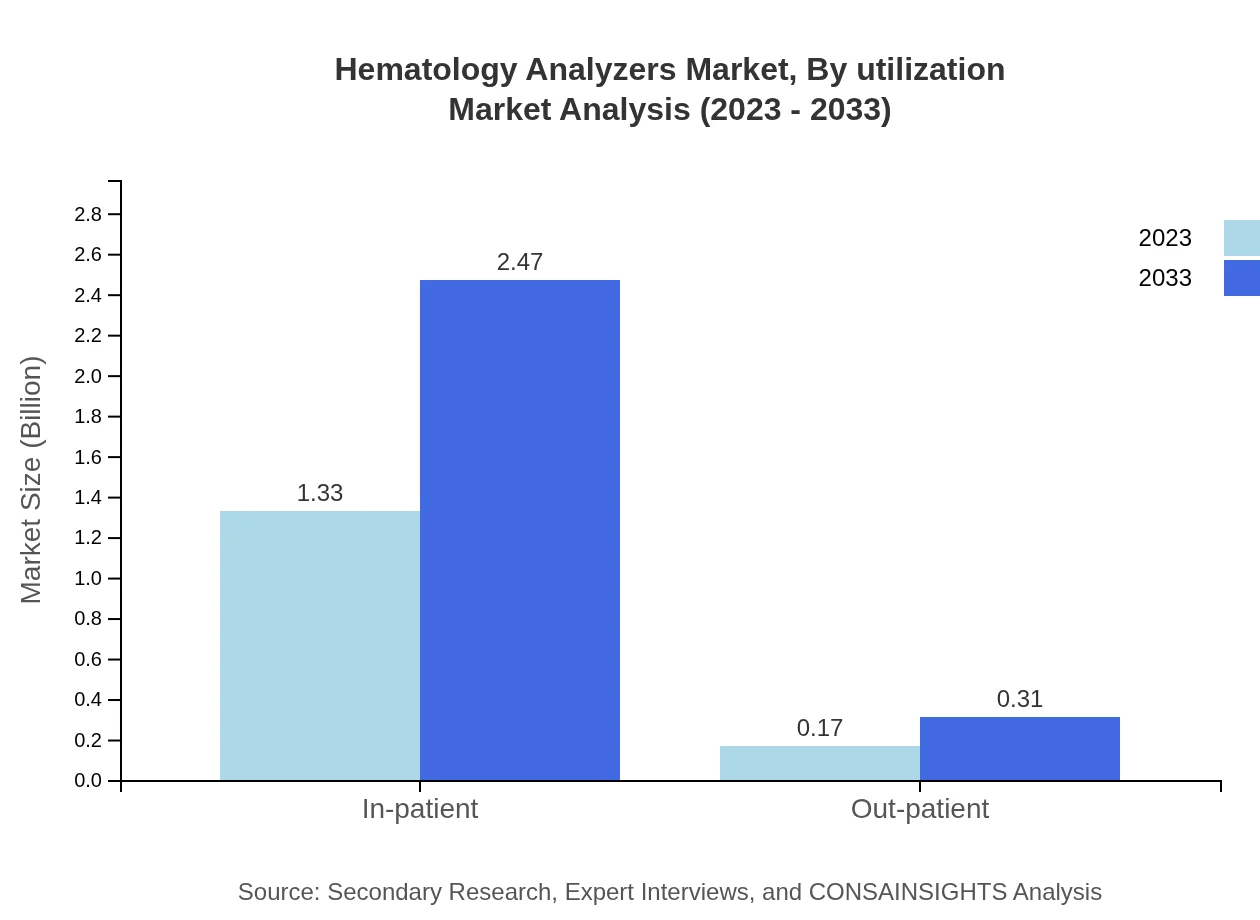

Hematology Analyzers Market Analysis By Utilization

The market utilization analysis reveals a clear distinction between inpatient and outpatient services. Inpatient services currently lead the market with $1.33 billion in 2023, expanding to $2.47 billion by 2033. Outpatient services, though smaller, are set for growth due to increasing medical check-ups and preventive healthcare approaches.

Hematology Analyzers Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Hematology Analyzers Industry

Abbott Laboratories:

Abbott is a global healthcare company that develops technologies in diagnostics, including hematology analyzers used in hospitals and laboratories to enhance clinical decision-making.Roche Diagnostics:

Roche Diagnostics offers innovative hematology solutions, known for their performance, accuracy, and range that caters to various laboratory needs in hematological diagnostics.Beckman Coulter:

Beckman Coulter is well-established in the hematology analyzer market, providing a range of automated analyzers for clinical laboratories, focusing on efficiency and data management.Sysmex Corporation:

Sysmex is a leading player in hematology diagnostics, dedicated to developing advanced analyzers and reagents, catering to the evolving healthcare demands globally.Mindray Medical International Limited:

Mindray specializes in medical devices and offers a comprehensive range of hematology analyzers designed for accuracy and efficiency in testing blood samples.We're grateful to work with incredible clients.

FAQs

What is the market size of hematology Analyzers?

The global hematology analyzers market is valued at approximately $1.5 Billion in 2023 and is projected to grow at a CAGR of 6.2%, reaching significant growth by 2033.

What are the key market players or companies in the hematology Analyzers industry?

Major players in the hematology analyzers market include Abbot Laboratories, Siemens Healthineers, Beckman Coulter, and Roche Diagnostics, which dominate through innovation and extensive product portfolios.

What are the primary factors driving the growth in the hematology Analyzers industry?

Key growth drivers in the hematology analyzers industry include technological advancements, increased prevalence of blood disorders, and rising demand for rapid diagnostic techniques in healthcare.

Which region is the fastest Growing in the hematology Analyzers?

The Asia Pacific region is the fastest-growing market for hematology analyzers, with substantial growth expected from $0.29 billion in 2023 to $0.54 billion by 2033.

Does ConsaInsights provide customized market report data for the hematology Analyzers industry?

Yes, ConsaInsights offers customized market report data tailored to specific needs, allowing clients to focus on particular segments and regions within the hematology analyzers market.

What deliverables can I expect from this hematology Analyzers market research project?

Typical deliverables from a hematology-analyzers market research project include market size analysis, growth forecasts, company profiles, competitor analysis, and regional market assessments.

What are the market trends of hematology Analyzers?

Current trends include a shift towards automatic analyzers, an increase in point-of-care testing, and advancements in clinical diagnostics, with traditional technology still holding the largest market share.