High Performance Insulation Materials Market Report

Published Date: 22 January 2026 | Report Code: high-performance-insulation-materials

High Performance Insulation Materials Market Size, Share, Industry Trends and Forecast to 2033

This report provides a comprehensive analysis of the high-performance insulation materials market, offering insights into market size, growth trends, technological advancements, and competitive landscape for the forecast period from 2023 to 2033.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

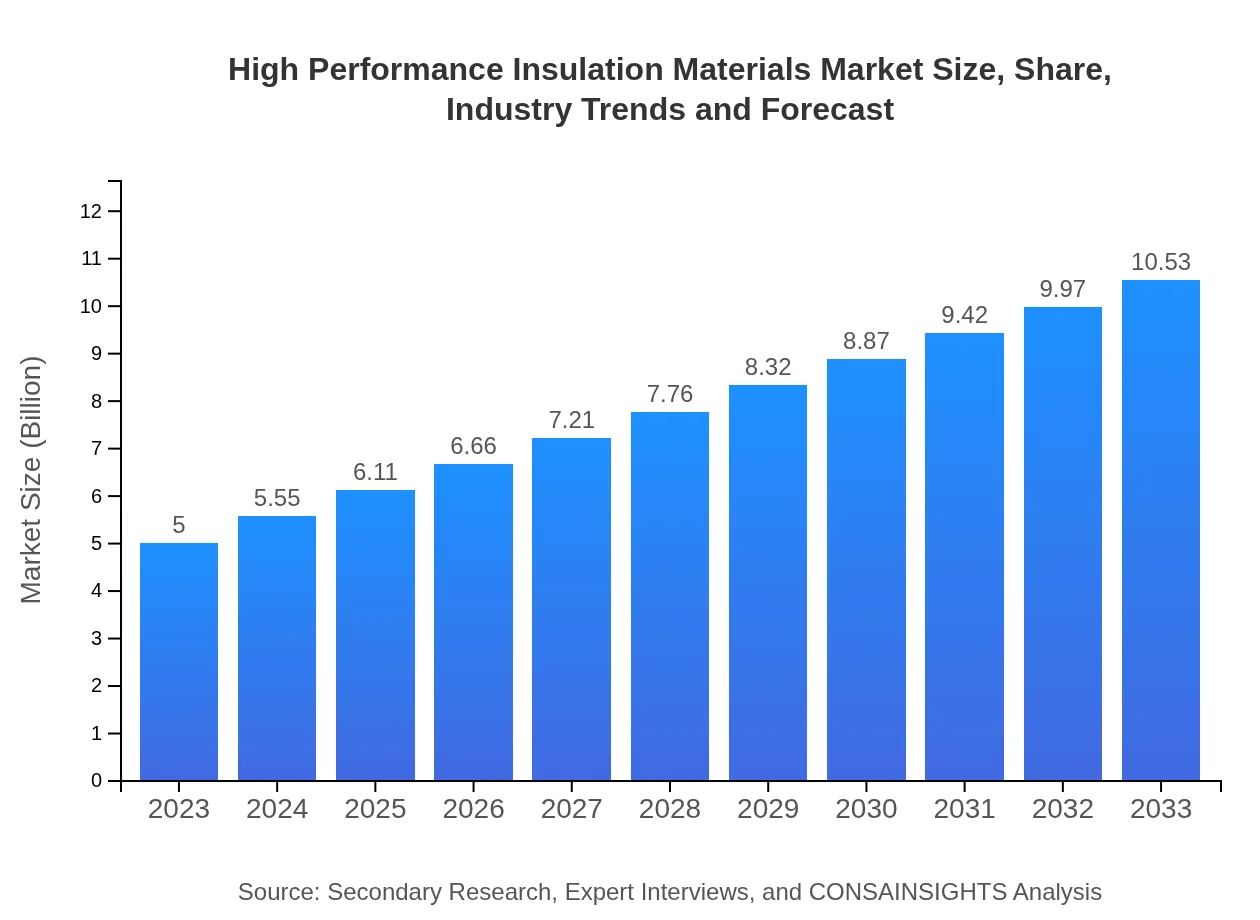

| 2023 Market Size | $5.00 Billion |

| CAGR (2023-2033) | 7.5% |

| 2033 Market Size | $10.53 Billion |

| Top Companies | Owens Corning, Rockwool International A/S, BASF SE, Johns Manville |

| Last Modified Date | 22 January 2026 |

High Performance Insulation Materials Market Overview

Customize High Performance Insulation Materials Market Report market research report

- ✔ Get in-depth analysis of High Performance Insulation Materials market size, growth, and forecasts.

- ✔ Understand High Performance Insulation Materials's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in High Performance Insulation Materials

What is the Market Size & CAGR of High Performance Insulation Materials market in 2023?

High Performance Insulation Materials Industry Analysis

High Performance Insulation Materials Market Segmentation and Scope

Tell us your focus area and get a customized research report.

High Performance Insulation Materials Market Analysis Report by Region

Europe High Performance Insulation Materials Market Report:

The European market is anticipated to grow from $1.64 billion in 2023 to $3.44 billion by 2033, driven by stringent energy efficiency standards and a rising trend towards sustainable building practices, supported by government policies incentivizing the use of high-performance insulation.Asia Pacific High Performance Insulation Materials Market Report:

In the Asia Pacific region, the market for high-performance insulation materials is anticipated to grow from $0.94 billion in 2023 to approximately $1.98 billion by 2033. This expansion is attributed to rapid industrialization and increasing construction activities in countries like China and India, coupled with heightened government initiatives towards energy-efficient buildings.North America High Performance Insulation Materials Market Report:

In North America, the market is projected to grow from $1.71 billion in 2023 to $3.60 billion by 2033. Regulations promoting energy conservation, along with advancements in insulation technology, are boosting demand, making it a significant player in the high-performance insulation materials market.South America High Performance Insulation Materials Market Report:

The South American market is expected to increase from $0.36 billion in 2023 to $0.76 billion by 2033. Brazil and Argentina are primary contributors to this growth, largely due to urbanization trends and increased focus on sustainable development practices.Middle East & Africa High Performance Insulation Materials Market Report:

In the Middle East and Africa, the market size is forecasted to rise from $0.35 billion in 2023 to $0.73 billion by 2033. Growing energy costs and increasing construction activities within the region emphasize the adoption of high-performance insulation materials.Tell us your focus area and get a customized research report.

High Performance Insulation Materials Market Analysis By Material Type

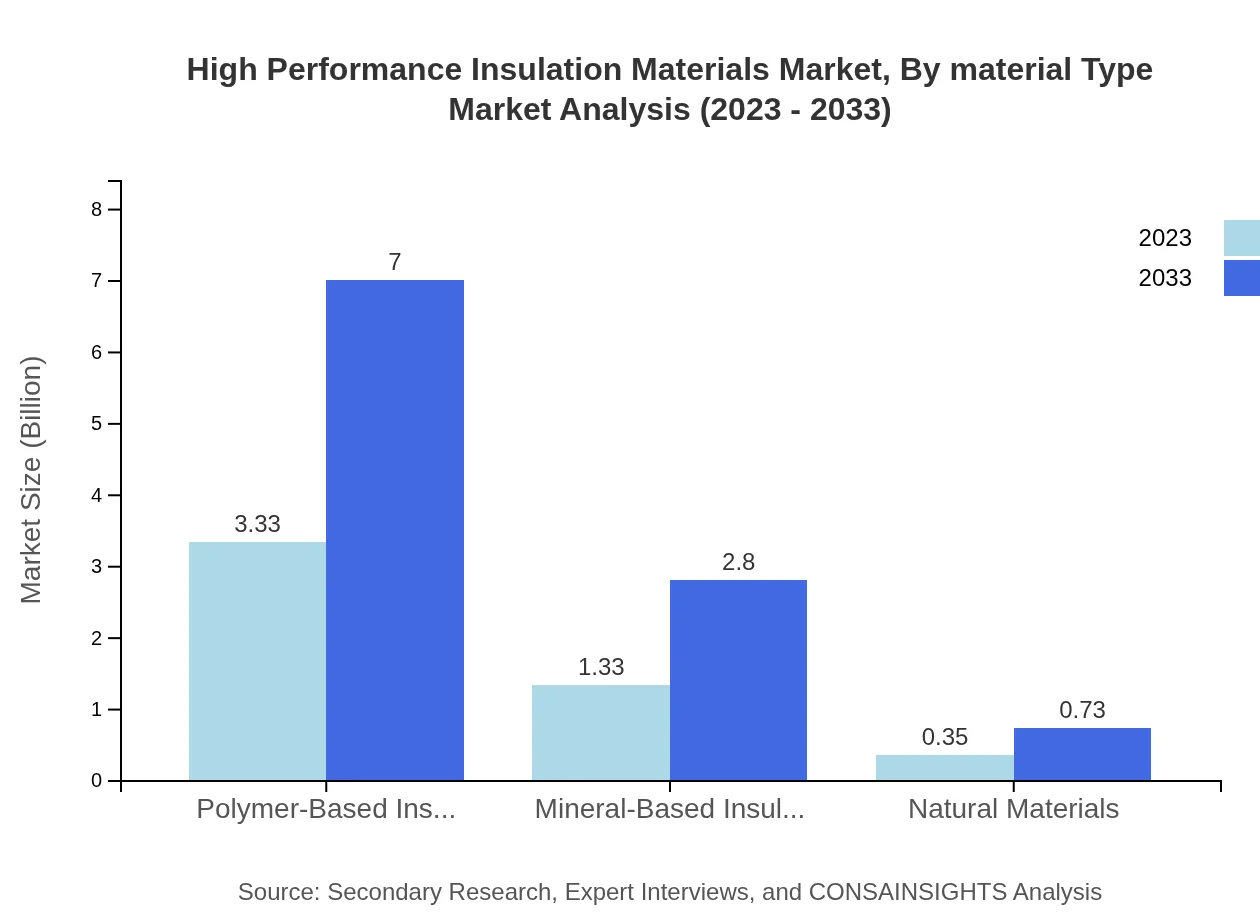

The market segmentation by material type illustrates that polymer-based insulation, accounting for $3.33 billion in 2023, will significantly grow to $7.00 billion by 2033, representing a dominant share of 66.53%. Mineral-based and natural materials also play vital roles, with mineral-based insulation expected to grow from $1.33 billion to $2.80 billion during the same period, capturing a 26.56% market share.

High Performance Insulation Materials Market Analysis By Application

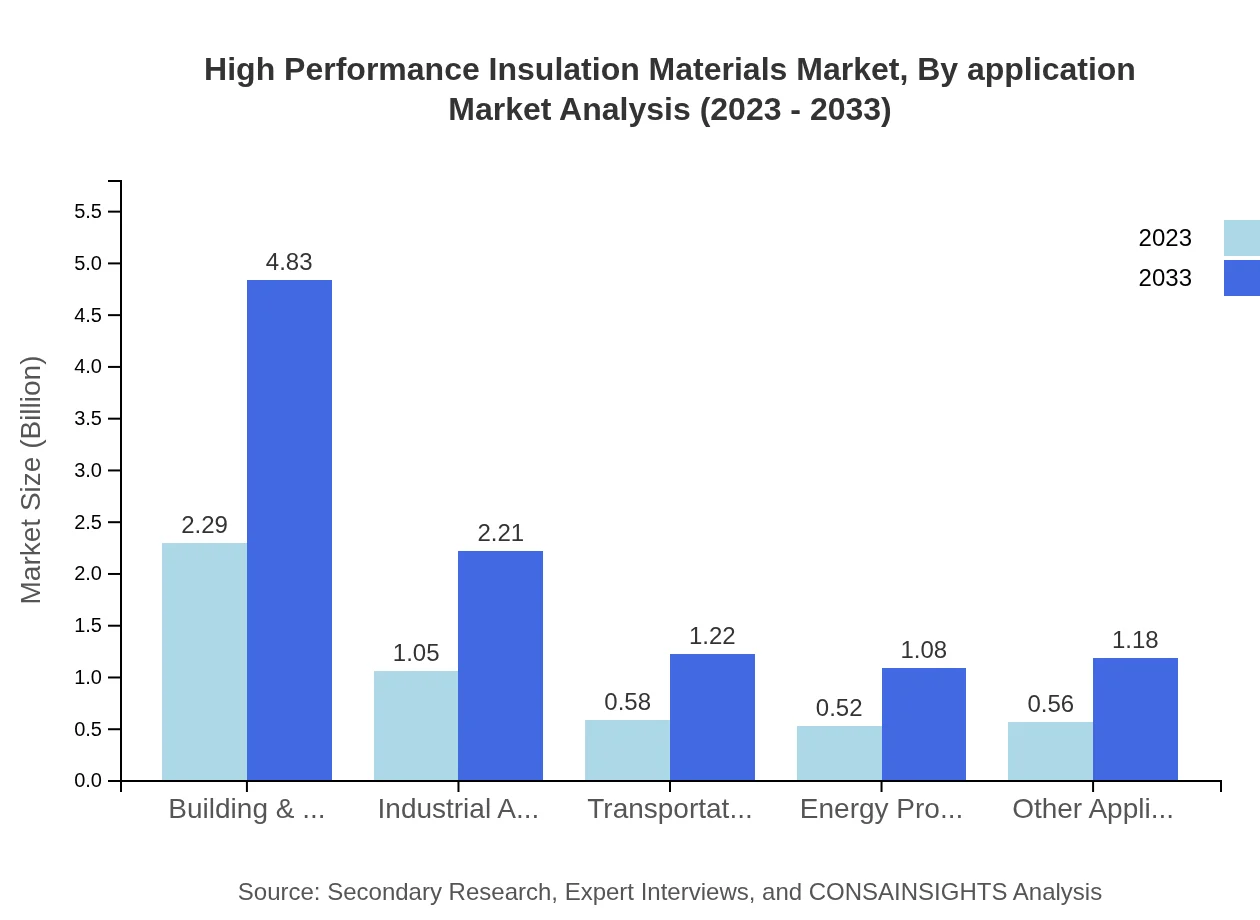

Building & construction leads the applications segment, valued at $2.29 billion in 2023, growing to $4.83 billion by 2033, translating to a consistent 45.89% market share. Other applications like industrial (from $1.05 billion to $2.21 billion) and energy production (from $0.52 billion to $1.08 billion) are also expanding.

High Performance Insulation Materials Market Analysis By End User Industry

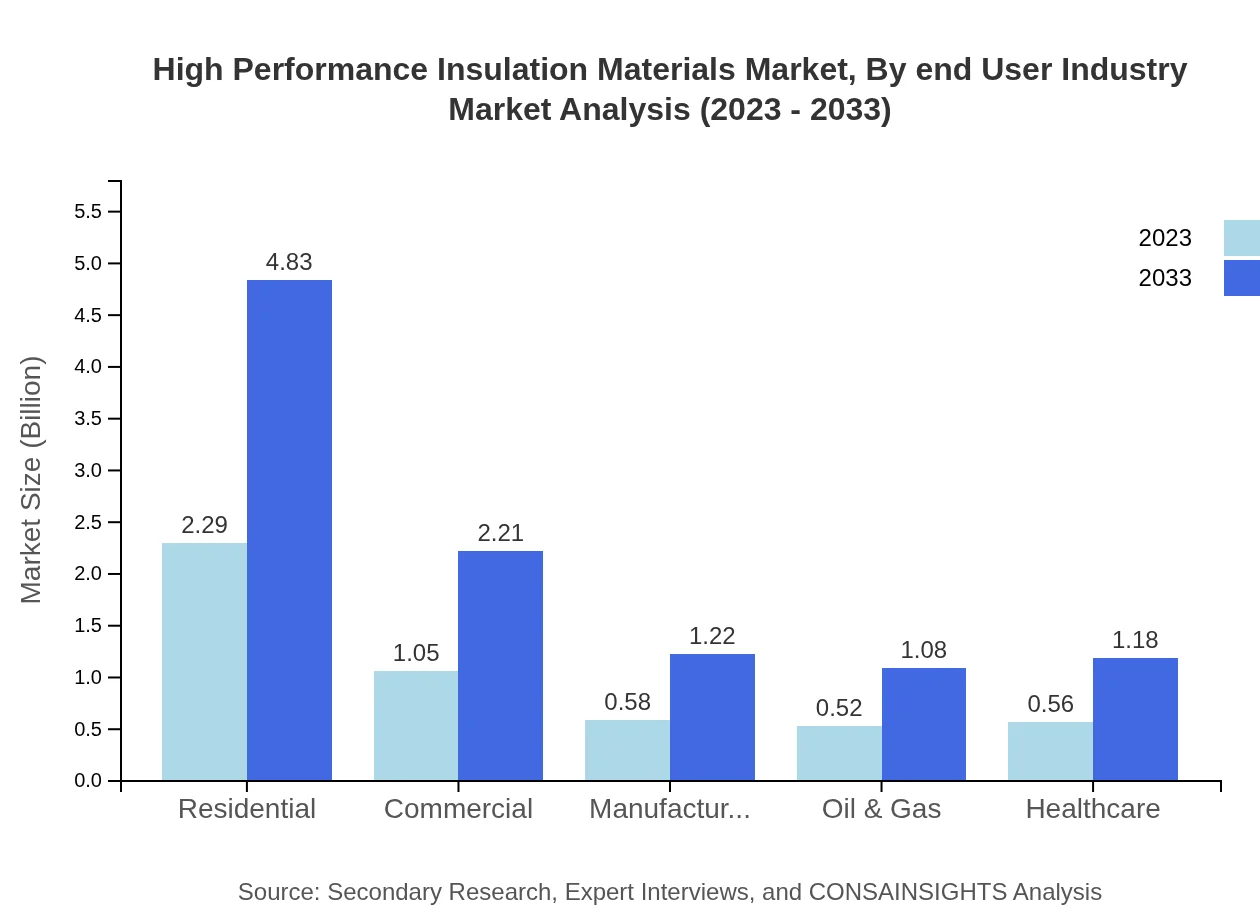

The residential sector is projected to see robust growth, rising from $2.29 billion in 2023 to approximately $4.83 billion in 2033, maintaining a significant share of 45.89%. Commercial and industrial segments are also poised for growth, particularly in energy-intensive applications such as manufacturing and oil & gas sectors.

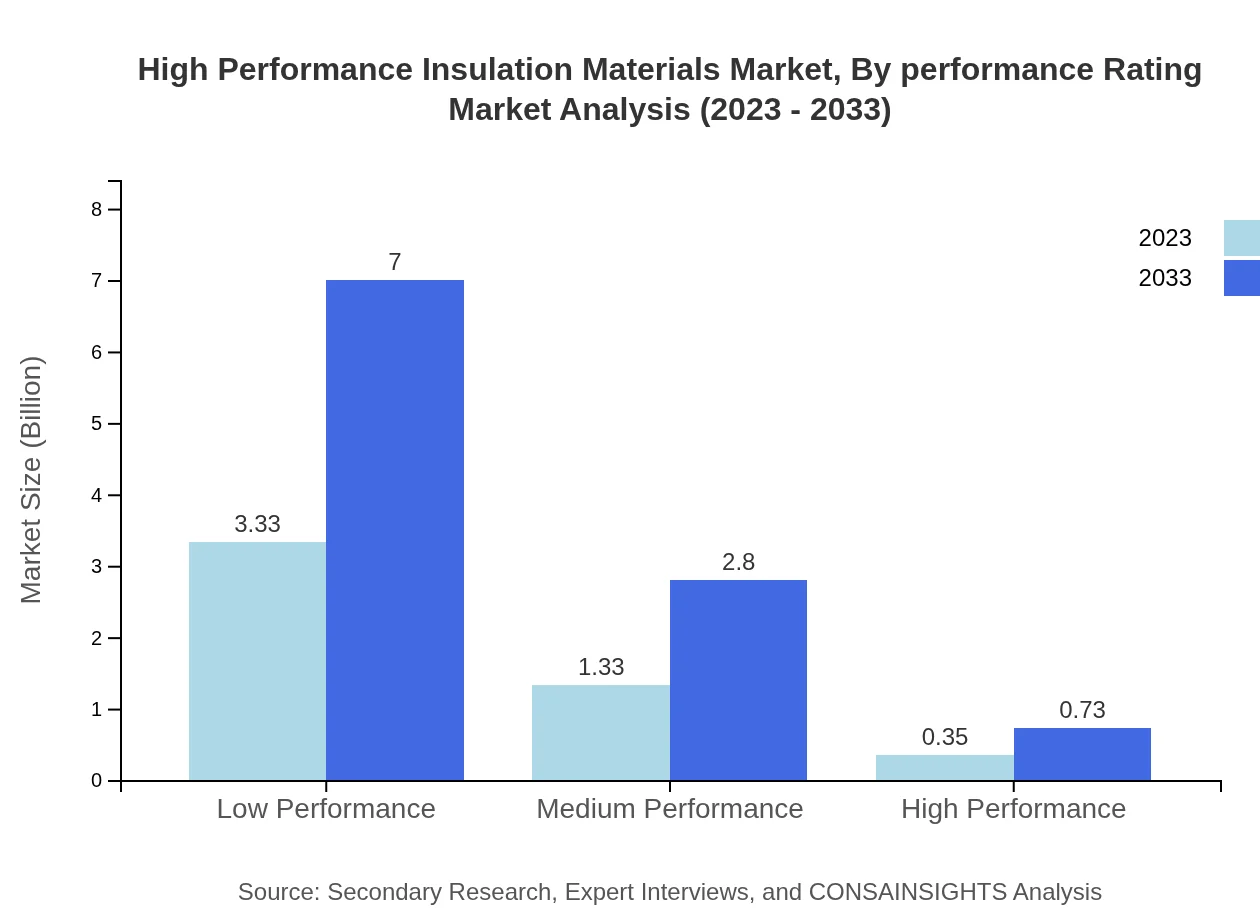

High Performance Insulation Materials Market Analysis By Performance Rating

When analyzing performance ratings, low-performance insulation materials dominate the market at $3.33 billion in 2023, reaching $7.00 billion by 2033. Medium performance follows with notable significance while high-performance materials, despite their smaller share of 6.91%, are gaining traction with increasing demand for energy-efficient solutions.

High Performance Insulation Materials Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in High Performance Insulation Materials Industry

Owens Corning:

Owens Corning is a global leader in the production of insulation and roofing materials, recognized for its innovative glass fiber insulation solutions that enhance energy efficiency in residential and commercial buildings.Rockwool International A/S:

Rockwool specializes in mineral wool insulation, providing effective thermal, acoustic, and fire insulation products that cater to construction and industrial needs, driving sustainable building practices.BASF SE:

BASF SE is a prominent chemical multinational that produces insulation materials, focusing on innovation and improving energy efficiency throughout the building construction lifecycle.Johns Manville:

Johns Manville manufactures high-performance insulation products, including fiberglass insulation, recognized for its sustainable manufacturing practices and extensive product range catering to various applications.We're grateful to work with incredible clients.

FAQs

What is the market size of high Performance Insulation Materials?

The global market size for high-performance insulation materials is projected to reach $5 billion by 2033, growing at a CAGR of 7.5% from its 2023 valuation of $5 billion.

What are the key market players or companies in this high Performance Insulation Materials industry?

Key players in the high-performance insulation materials market include major manufacturers such as Owens Corning, Rockwool Group, and Kingspan Group, among others, driving innovation and competition within the industry.

What are the primary factors driving the growth in the high Performance Insulation Materials industry?

Factors driving growth include increased energy efficiency regulations, rising construction activities, and greater awareness of environmental sustainability, making high-performance insulation materials a preferred choice.

Which region is the fastest Growing in the high Performance Insulation Materials?

The fastest-growing region for high-performance insulation materials is North America, with its market size expected to grow from $1.71 billion in 2023 to $3.60 billion by 2033.

Does ConsaInsights provide customized market report data for the high Performance Insulation Materials industry?

Yes, ConsaInsights offers customized market report data tailored to client specifications within the high-performance insulation materials industry, ensuring relevant and actionable insights.

What deliverables can I expect from this high Performance Insulation Materials market research project?

Expect comprehensive deliverables including detailed market analysis, growth forecasts, competitive landscape findings, and segmentation insights, tailored to inform strategic decision-making.

What are the market trends of high Performance Insulation Materials?

Current trends include a shift towards sustainable materials, innovations in insulation technology, and growing demand in residential and commercial segments, influencing market dynamics.