Infectious Disease Diagnostics Market Report

First published: 08 October 2024 | Last updated: 25 May 2026 | Report Code: infectious-disease-diagnostics

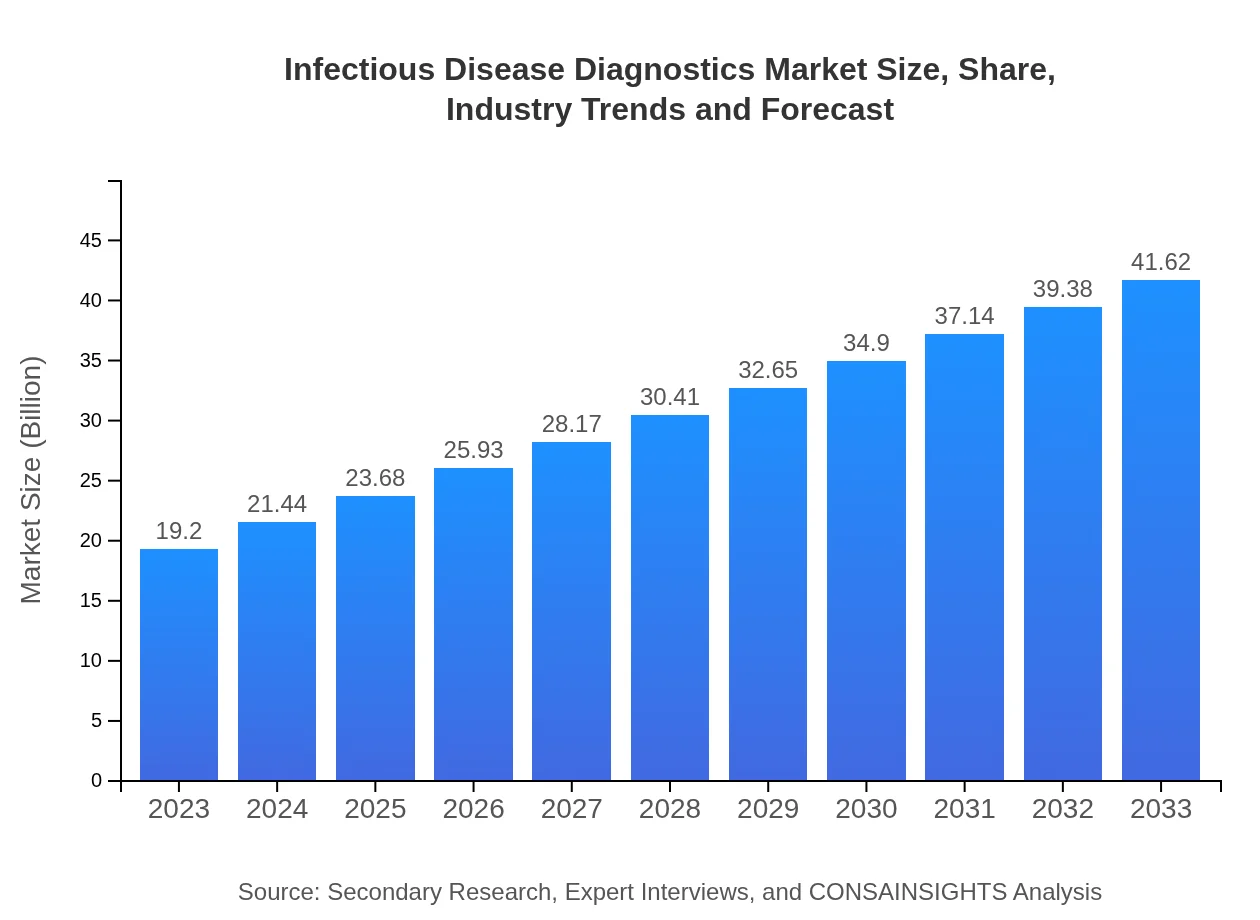

Infectious Disease Diagnostics Market — USD 19.2 billion in 2023, Growing to USD 41.62B by 2033 at 7.8% CAGR

This report provides a comprehensive analysis of the Infectious Disease Diagnostics market, including market size, growth forecasts, industry trends, and key player insights from 2023 to 2033.

Key Takeaways

- Global market value rises from $19.20 Billion in 2023 to $41.62 Billion in 2033 at a 7.8% CAGR.

- North America is largest regional market, while no single fastest-growing region is stated because regional CAGR differences remain within 0.15 percentage points.

- Europe expands from $5.45 Billion in 2023 to $11.82 Billion in 2033; Asia Pacific grows from $3.91 Billion to $8.49 Billion.

- Market structure includes molecular, serology, and antigen test types plus technologies like Nucleic Acid Technology and Immunodiagnostics.

- Leading firms named include Roche Diagnostics, Abbott Laboratories, Thermo Fisher Scientific, and Siemens Healthineers.

Infectious Disease Diagnostics Market Report — Executive Summary

North America remains largest market by forecast-period value, while no single fastest-growing region is stated because top regional growth rates are separated by less than 0.15 percentage points. This report maps the Infectious Disease Diagnostics market from 2023 to 2033, reporting a rise from $19.20 Billion to $41.62 Billion at a 7.8% CAGR. Growth is supported by accelerating adoption of advanced testing approaches, increased investment in diagnostic infrastructure, and demand for rapid, accurate detection. The analysis covers test types (molecular, serology, antigen), technologies (Nucleic Acid Technology, Immunodiagnostics, Microbiology Culture), end users, and distribution channels. Regional profiles quantify shifts across North America, Europe, Asia Pacific, Latin America, and Middle East and Africa, while competitive coverage highlights players such as Roche Diagnostics, Abbott Laboratories, Thermo Fisher Scientific, and Siemens Healthineers. The research synthesizes primary expert interviews and secondary sources to validate trends and market sizing, offering actionable insights for stakeholders evaluating product development, market entry, and partnership strategies.

Key Growth Drivers

- Rising demand for fast and precise diagnostic tests fuels adoption of molecular and antigen-based technologies.

- Continued investment in laboratory capacity and point-of-care solutions expands service availability across care settings.

- Technological advances in Nucleic Acid Technology and immunodiagnostics enhance sensitivity and throughput of testing.

- Increased public health focus and surveillance programs drive procurement and deployment of infectious disease diagnostics.

- Wider use of online and direct sales channels improves market access and distribution efficiency.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $19.20 Billion |

| CAGR (2023-2033) | 7.8% |

| 2033 Market Size | $41.62 Billion |

| Top Companies | Roche Diagnostics, Abbott Laboratories, Thermo Fisher Scientific, Siemens Healthineers |

| Published Date | 08 October 2024 |

| Last Modified Date | 25 May 2026 |

Infectious Disease Diagnostics Market Overview

Customize Infectious Disease Diagnostics Market Report market research report

- ✔ Get in-depth analysis of Infectious Disease Diagnostics market size, growth, and forecasts.

- ✔ Understand Infectious Disease Diagnostics's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Infectious Disease Diagnostics

What is the Market Size & CAGR of Infectious Disease Diagnostics Market Report market in 2023?

Infectious Disease Diagnostics Industry Analysis

Infectious Disease Diagnostics Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Infectious Disease Diagnostics Market Report Market Analysis Report by Region

Europe Infectious Disease Diagnostics Market Report:

Europe grows from $5.45 Billion in 2023 to $11.82 Billion in 2033. Expansion is supported by modernization of diagnostic services, emphasis on surveillance programs, and uptake of immunodiagnostics and molecular testing technologies.Asia Pacific Infectious Disease Diagnostics Market Report:

Asia Pacific grows from $3.91 Billion in 2023 to $8.49 Billion in 2033. Growth drivers include expanding laboratory capacity, increasing access to point-of-care testing, and rising demand for rapid diagnostics across diverse healthcare settings.North America Infectious Disease Diagnostics Market Report:

North America is largest regional market, rising from $6.8 Billion in 2023 to $14.74 Billion in 2033. Regional growth reflects sustained investment in laboratory infrastructure, high adoption of molecular diagnostics, and established public health testing networks.South America Infectious Disease Diagnostics Market Report:

Latin America grows from $0.43 Billion in 2023 to $0.92 Billion in 2033. Market acceleration is linked to investments in diagnostic capabilities, greater test availability, and strengthened public health initiatives.Middle East & Africa Infectious Disease Diagnostics Market Report:

Middle East and Africa grows from $2.61 Billion in 2023 to $5.65 Billion in 2033. Growth is underpinned by scaling laboratory services, enhanced disease surveillance, and adoption of newer diagnostic technologies.Tell us your focus area and get a customized research report.

Research Methodology

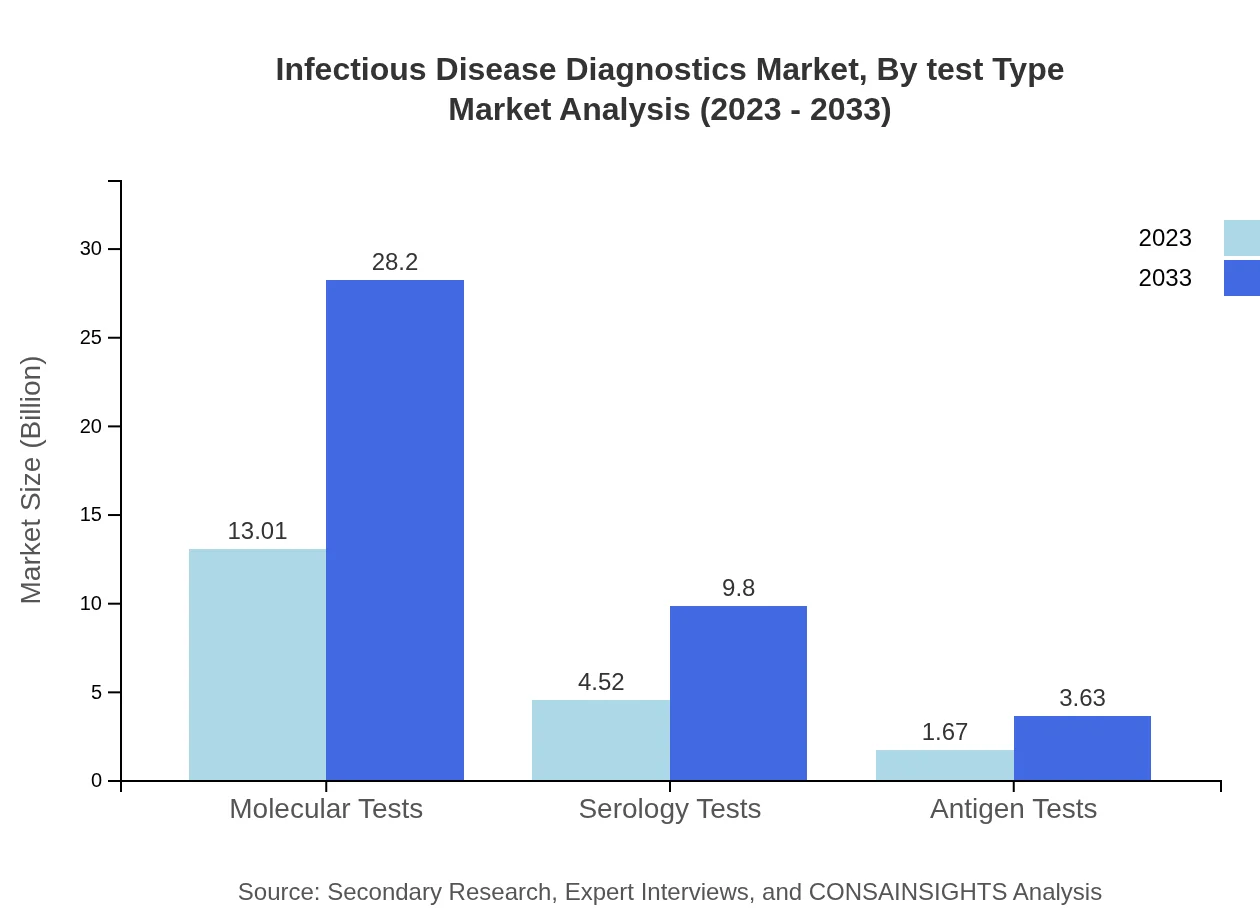

Infectious Disease Diagnostics Market Analysis By Test Type

The Infectious Disease Diagnostics Market, By Test Type, illustrates a significant emphasis on molecular tests, accounting for $13.01 billion in 2023 and forecasted to double to $28.20 billion by 2033. Serology tests will also see growth from $4.52 billion to $9.80 billion, indicating a steady reliance on both molecular diagnostics and immunoassays.

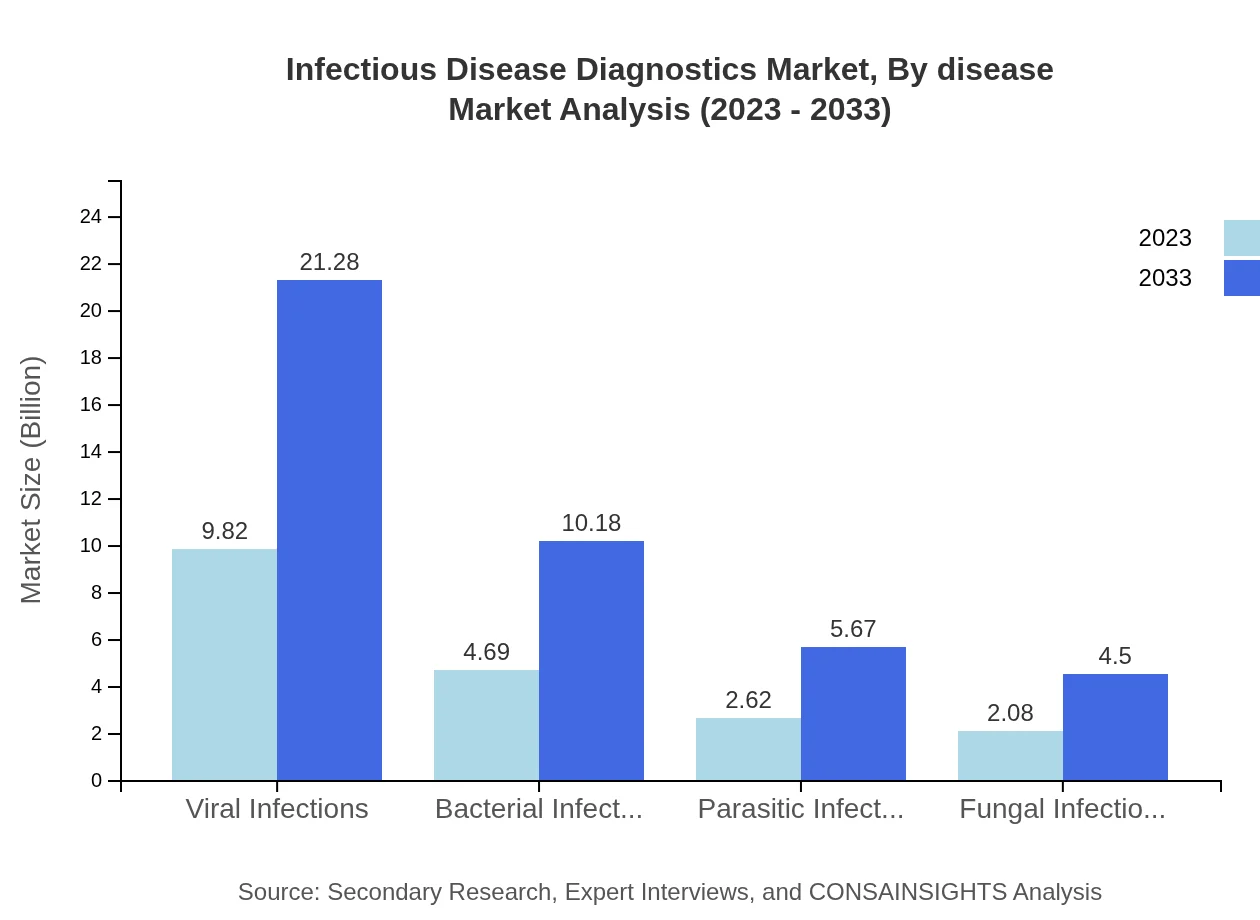

Infectious Disease Diagnostics Market Analysis By Disease

The market size for viral infections is expected to grow from $9.82 billion in 2023 to $21.28 billion by 2033. Bacterial infections and parasitic infections are predicted to follow suit, with market sizes increasing from $4.69 billion to $10.18 billion and from $2.62 billion to $5.67 billion respectively.

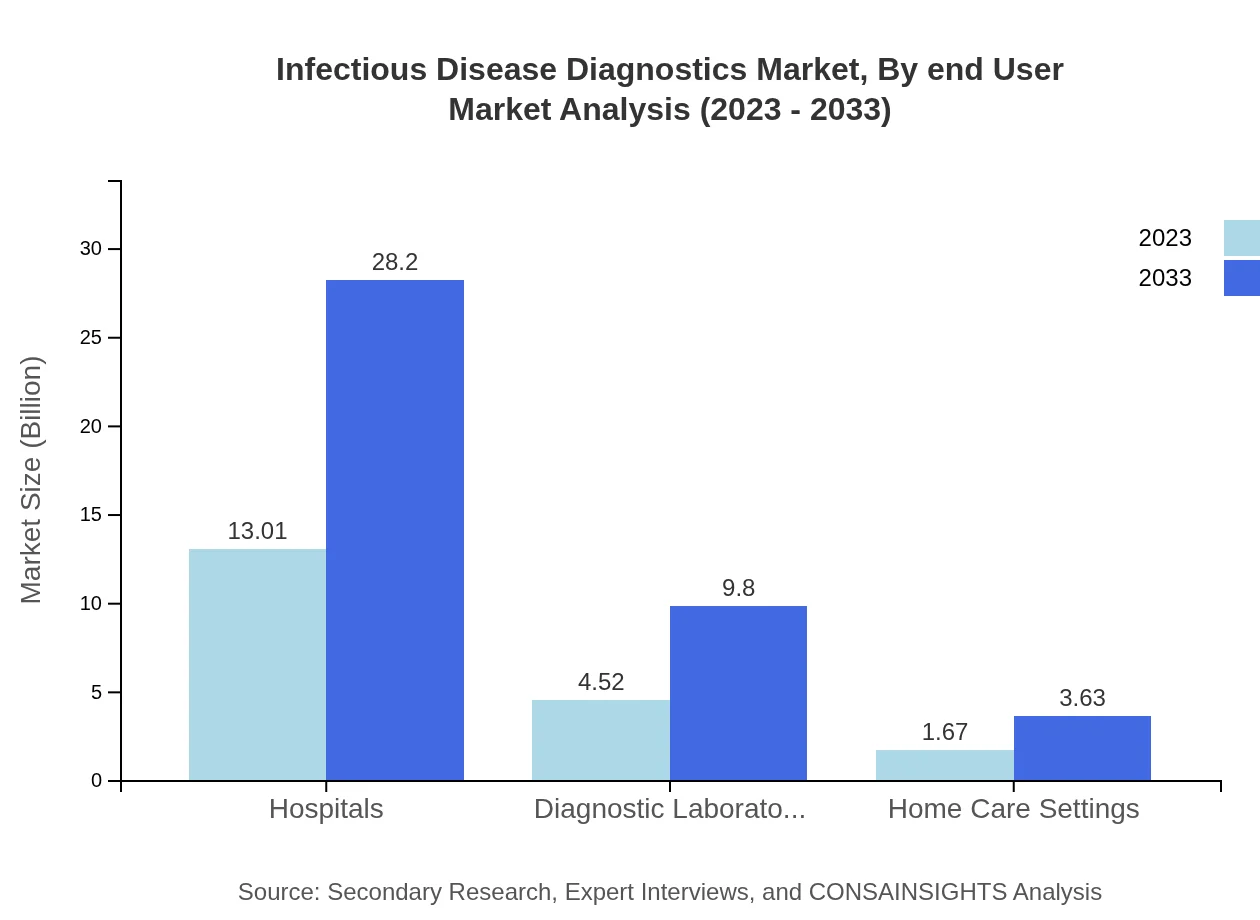

Infectious Disease Diagnostics Market Analysis By End User

Hospitals dominate the market with a size of $13.01 billion in 2023 and are projected to grow to $28.20 billion by 2033. Diagnostic laboratories are also significant players, growing from $4.52 billion to $9.80 billion, showcasing the importance of laboratory services in disease diagnostics.

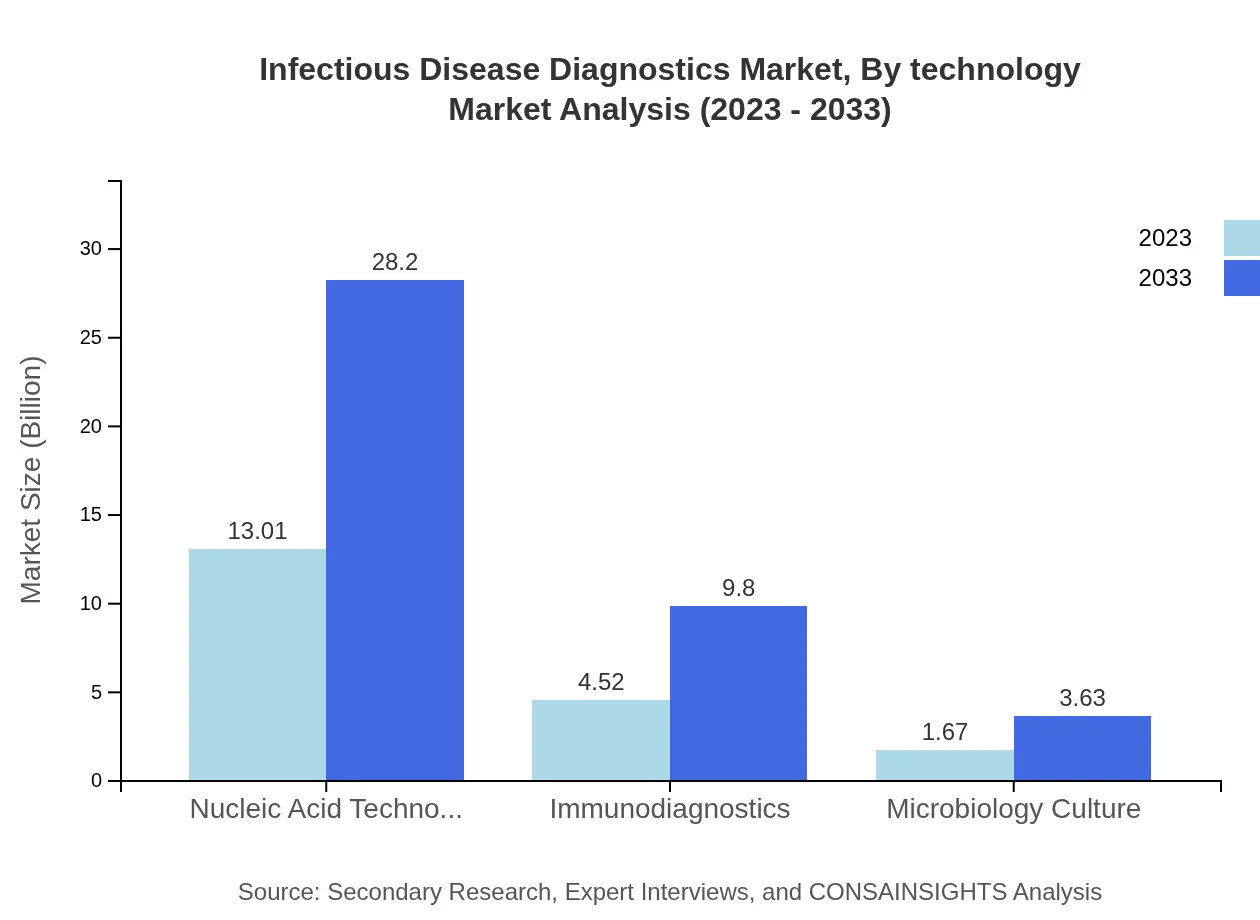

Infectious Disease Diagnostics Market Analysis By Technology

Nucleic acid technology leads the market with a size expected to rise from $13.01 billion in 2023 to $28.20 billion in 2033. Meanwhile, immunodiagnostics will significantly contribute, expanding from $4.52 billion to $9.80 billion.

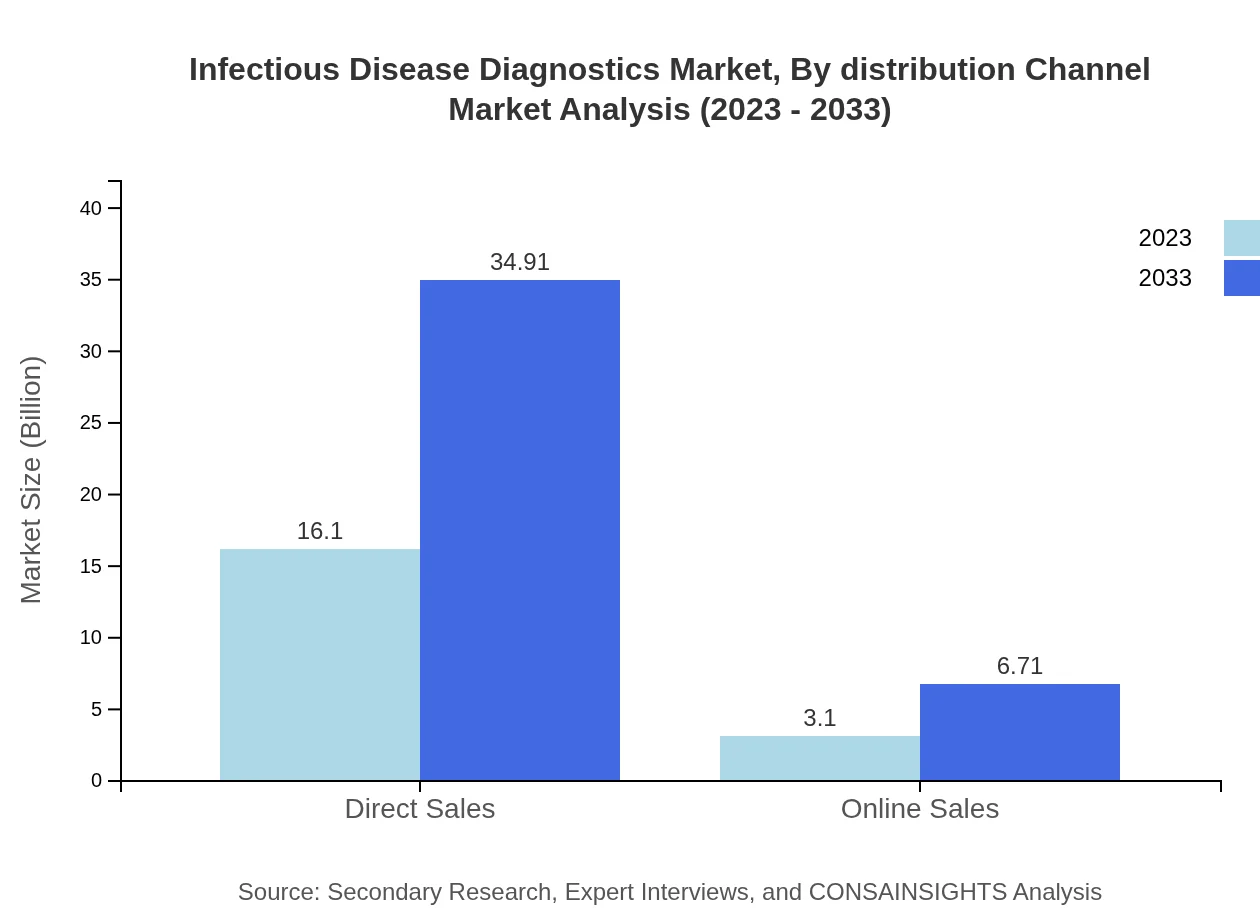

Infectious Disease Diagnostics Market Analysis By Distribution Channel

Direct sales account for a significant market share, increasing from $16.10 billion in 2023 to $34.91 billion by 2033. Online sales are also expected to climb from $3.10 billion to $6.71 billion, reflecting shifting consumer preferences towards online purchasing.

Infectious Disease Diagnostics Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Infectious Disease Diagnostics Industry

Roche Diagnostics:

A leader in diagnostic solutions, Roche offers an extensive range of tests and procedures for infectious diseases, focusing on rapid diagnostics.Abbott Laboratories:

Known for innovative diagnostic products, Abbott focuses on providing advanced molecular diagnostics and serological tests for a wide range of infectious diseases.Thermo Fisher Scientific:

Provides a broad portfolio of diagnostic solutions emphasizing advanced and comprehensive testing technologies in infectious disease diagnostics.Siemens Healthineers:

Specializes in integrated diagnostics solutions, offering an array of testing technologies and analytics for better patient outcomes.We're grateful to work with incredible clients.

FAQs

What is the market size in 2023?

The market size in 2023 is $19.20 Billion according to the report’s base-year estimate and market accounting.

How big will the market be in 2033?

By 2033 the market is projected to reach $41.62 Billion as reported for the forecast end year.

What is CAGR for the forecast period?

The compound annual growth rate for 2023 to 2033 is 7.8% as stated for the market trajectory.

Is there a single fastest Growing region in the Infectious Disease Diagnostics Market Report market?

No single fastest-growing region is stated for the Infectious Disease Diagnostics Market Report market because the top regional implied CAGR values are within 0.15 percentage points of each other, making the ranking too close to call reliably.

Why is diagnostic technology adoption increasing?

Adoption rises because advances in test accuracy, demand for rapid results, and investments in diagnostic infrastructure support broader implementation.

Who are the top companies in the market?

Top companies mentioned include Roche Diagnostics, Abbott Laboratories, Thermo Fisher Scientific, and Siemens Healthineers.

What test types are included in the segmentation?

Segmentation covers Molecular Tests, Serology Tests, and Antigen Tests as the principal test-type categories.

How are technologies categorized?

Technologies are listed as Nucleic Acid Technology, Immunodiagnostics, and Microbiology Culture in the report’s breakdown.

What end User segments are covered?

End-user segmentation includes Hospitals, Diagnostic Laboratories, and Home Care Settings across care delivery channels.

Which distribution channels are analyzed?

Distribution channels reviewed comprise Direct Sales and Online Sales as the primary routes to market.