Reports >

Manufacturing And Construction

>

Inverter Market Report

Inverter Market Report

Published Date: 22 January 2026 | Report Code: inverter

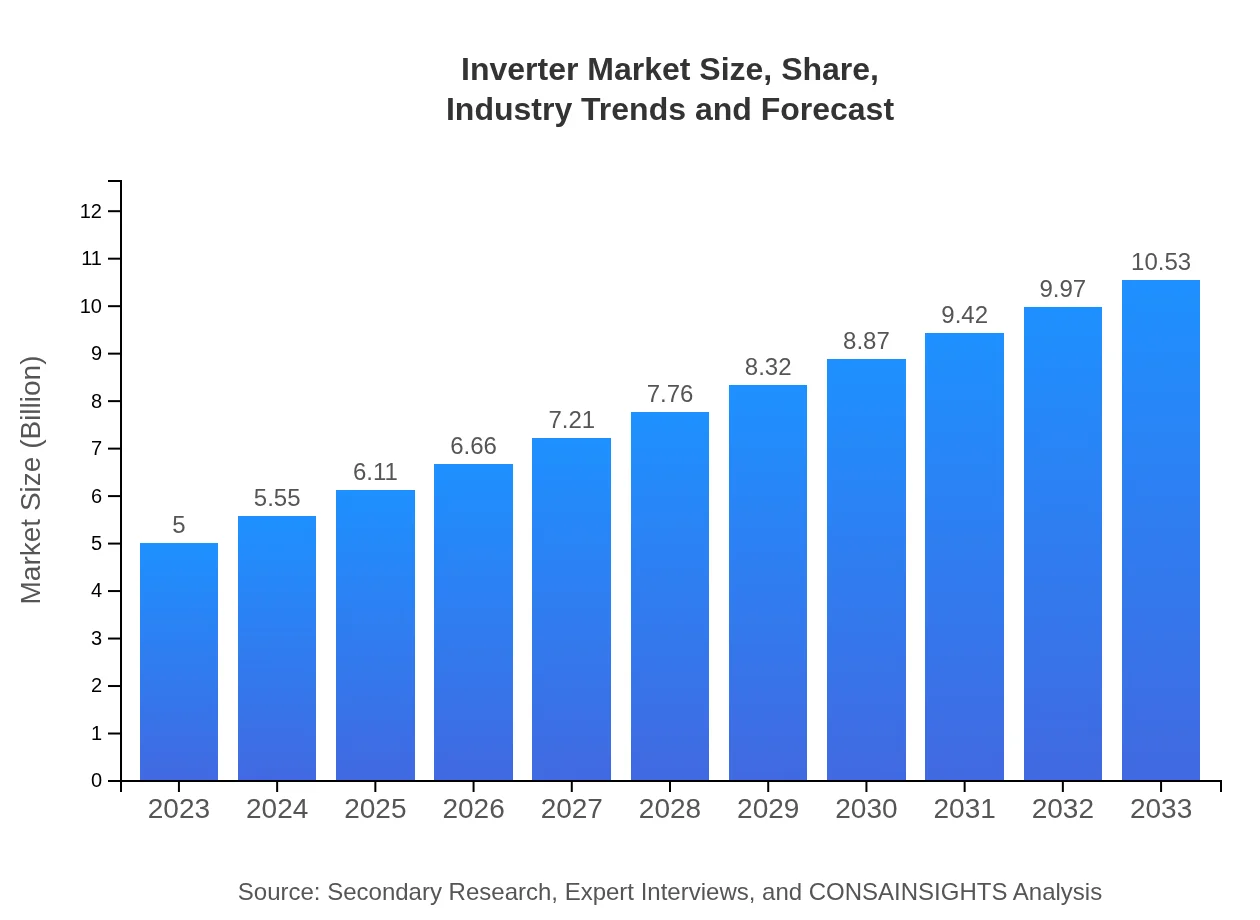

Inverter Market Size, Share, Industry Trends and Forecast to 2033

This report provides a comprehensive analysis of the inverter market, covering market size, trends, segmentation, and growth forecasts from 2023 to 2033. It includes insights into various regional markets and key players driving innovation and growth in the industry.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.00 Billion |

| CAGR (2023-2033) | 7.5% |

| 2033 Market Size | $10.53 Billion |

| Top Companies | SMA Solar Technology, Fronius International, SolarEdge Technologies, ABB Ltd., Enphase Energy |

| Last Modified Date | 22 January 2026 |

Inverter Market Overview

Customize Inverter Market Report market research report

- ✔ Get in-depth analysis of Inverter market size, growth, and forecasts.

- ✔ Understand Inverter's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Inverter

What is the Market Size & CAGR of Inverter market in 2023?

Inverter Industry Analysis

Inverter Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Inverter Market Analysis Report by Region

Europe Inverter Market Report:

In Europe, the inverter market is expected to rise from $1.69 billion in 2023 to $3.57 billion by 2033. The implementation of renewable energy directives and substantial investments into smart grid technologies are major contributors to this rapid growth.Asia Pacific Inverter Market Report:

In the Asia Pacific region, the inverter market is projected to grow significantly from $0.88 billion in 2023 to $1.85 billion by 2033. This growth is driven by rapid urbanization, increasing energy demands, and supportive government policies promoting renewable energy installations.North America Inverter Market Report:

The North American market is projected to grow from $1.79 billion in 2023 to $3.77 billion by 2033. Strong federal incentives and state-level support for renewable energy projects significantly influence market dynamics in this region.South America Inverter Market Report:

The South American inverter market is expected to expand from $0.14 billion in 2023 to $0.30 billion by 2033. The demand for inverter solutions in photovoltaic installations is rising, spurred by increasing awareness of energy efficiency and renewable energy benefits.Middle East & Africa Inverter Market Report:

The inverter market in the Middle East and Africa is forecasted to grow from $0.49 billion in 2023 to $1.03 billion by 2033. Increased investment in infrastructure and the growth of renewable energy projects are key drivers in this region.Tell us your focus area and get a customized research report.

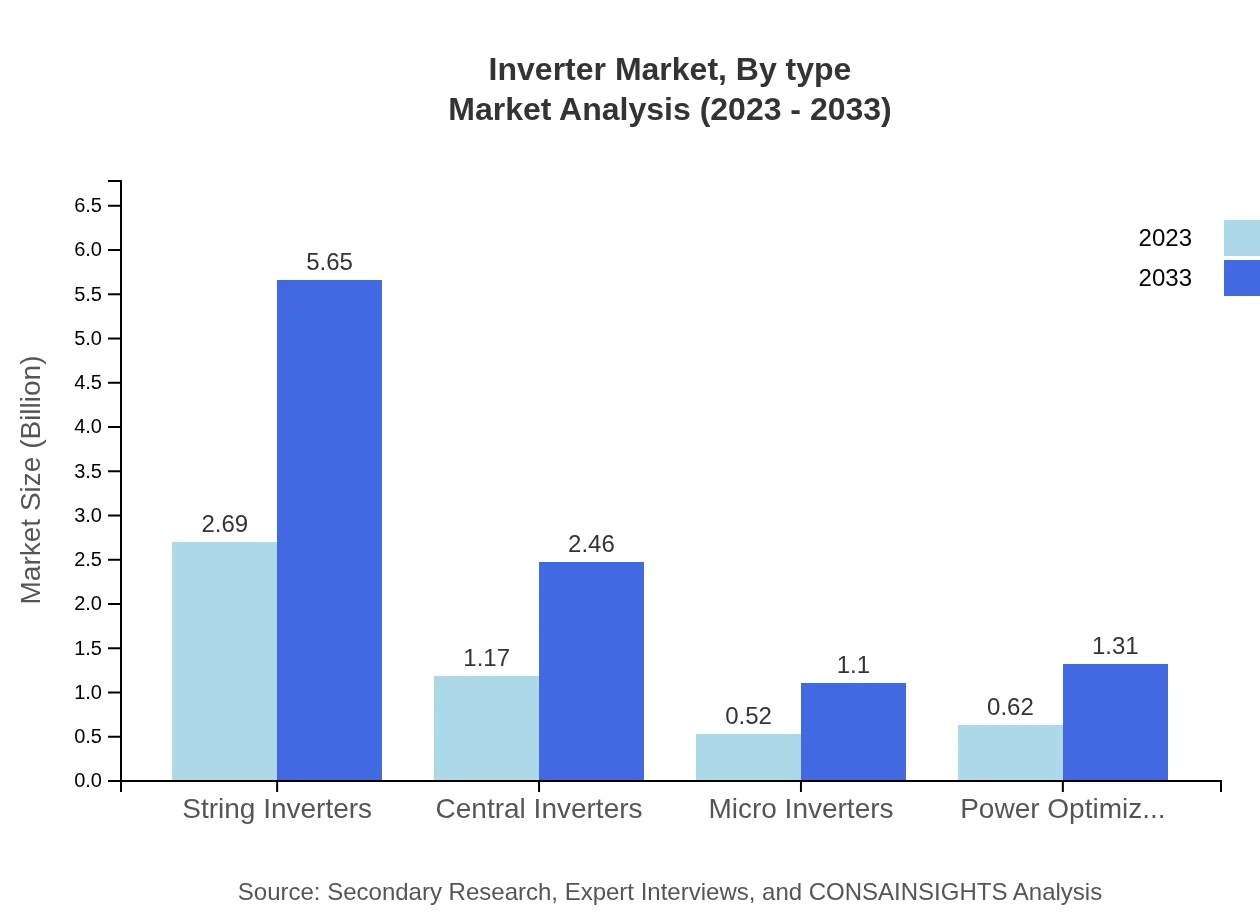

Inverter Market Analysis By Type

The inverter market is segmented by type into String Inverters, Central Inverters, Micro Inverters, and Power Optimizers: - **String Inverters**: Dominating the market with a size of $2.69 billion in 2023 and expected to reach $5.65 billion in 2033. They hold a share of 53.71%. - **Central Inverters**: Estimated size of $1.17 billion in 2023, growing to $2.46 billion in 2033 with a market share of 23.41%. - **Micro Inverters**: Their market size is projected from $0.52 billion in 2023 to $1.10 billion in 2033, maintaining a share of 10.42%. - **Power Optimizers**: Expecting growth from $0.62 billion in 2023 to $1.31 billion by 2033, with a share of 12.46%.

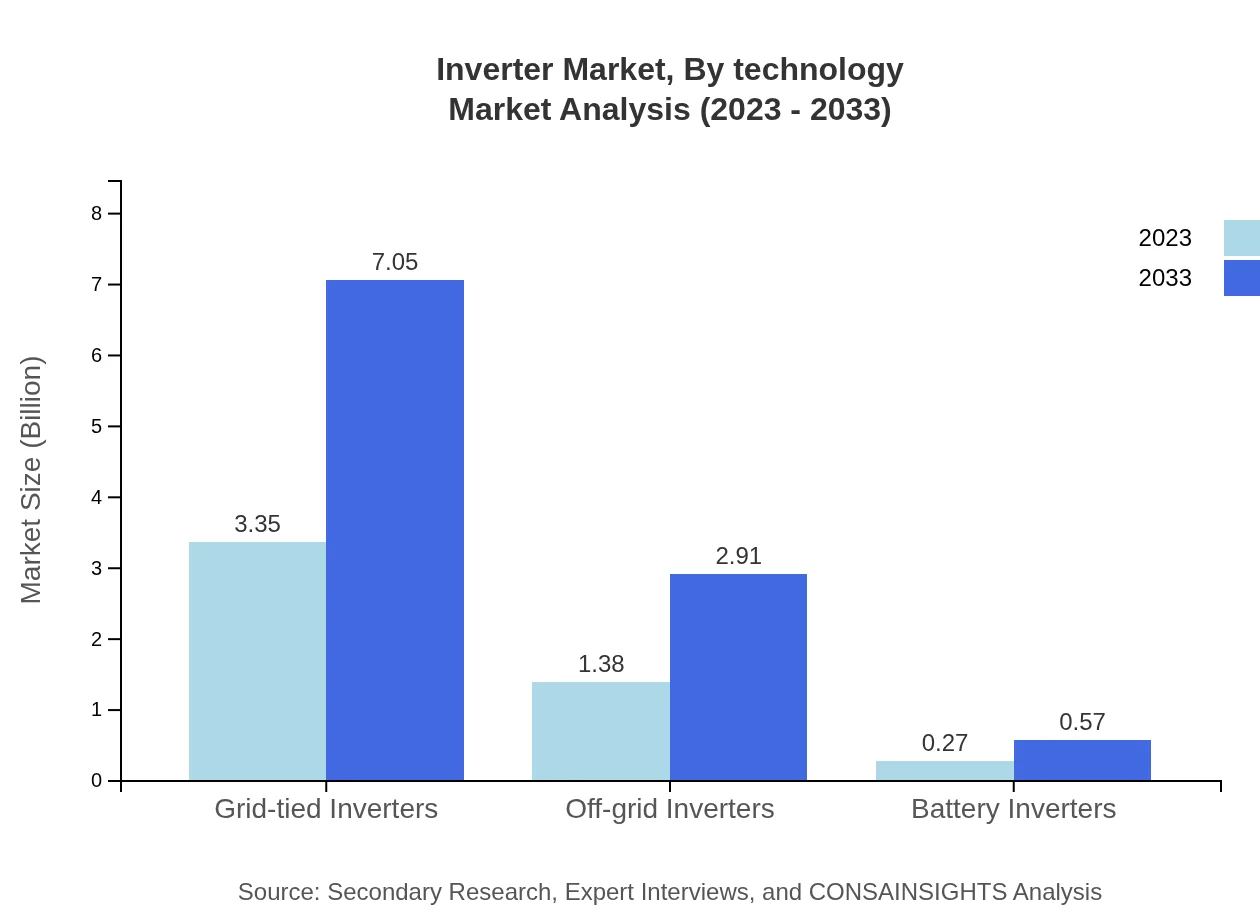

Inverter Market Analysis By Technology

The market is also segmented into: - **Grid-tied Inverters**: Leading with a size of $3.35 billion in 2023 and anticipated to grow to $7.05 billion in 2033, holding a share of 67.01%. - **Off-grid Inverters**: Expected to expand from $1.38 billion in 2023 to $2.91 billion in 2033, accounting for 27.62% of the market. - **Battery Inverters**: Set to increase from $0.27 billion in 2023 to $0.57 billion in 2033, maintaining a market share of 5.37%.

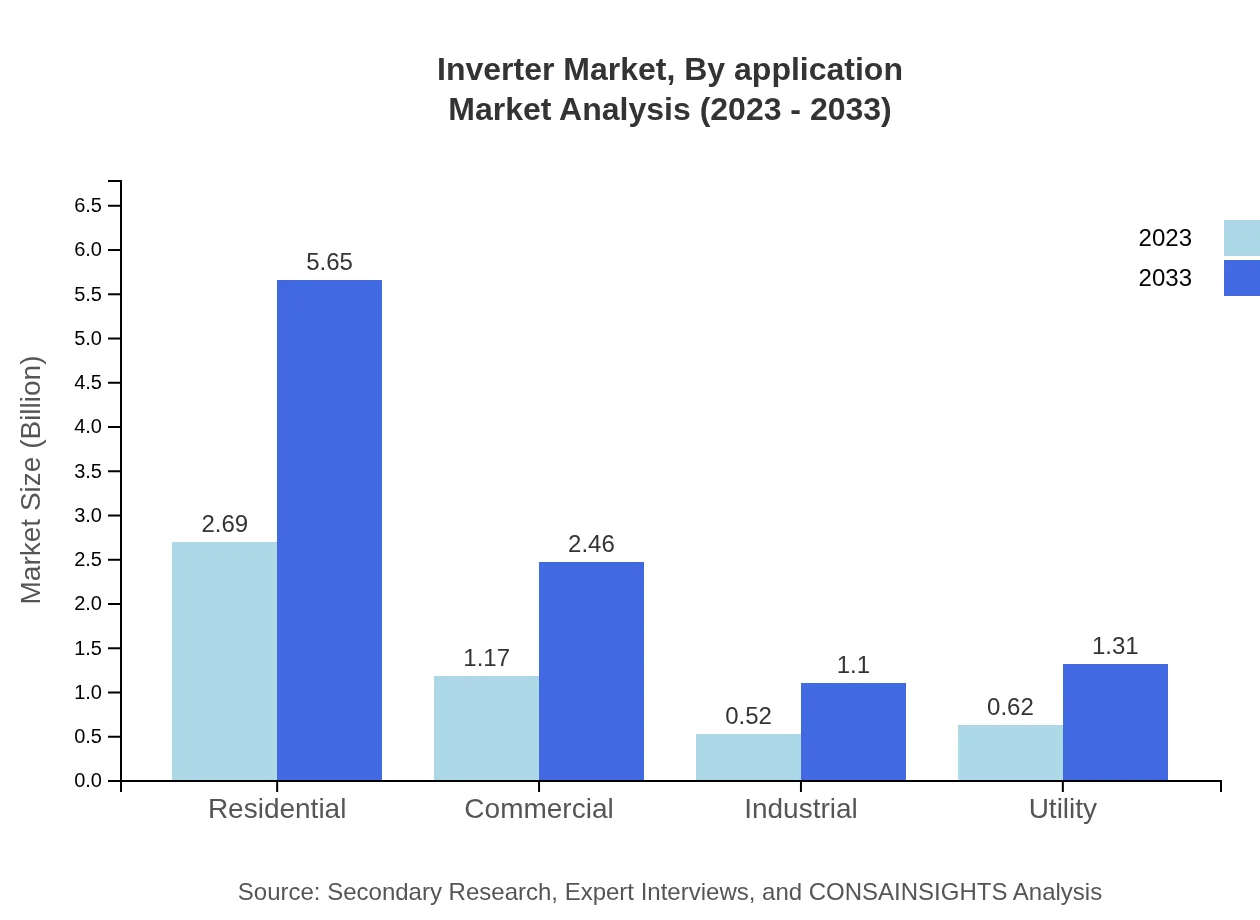

Inverter Market Analysis By Application

Applications of inverters include: - **Residential**: Projected to expand from $2.69 billion in 2023 to $5.65 billion by 2033, with a share of 53.71%. - **Commercial**: Size expected to grow from $1.17 billion in 2023 to $2.46 billion in 2033, holding 23.41% of the market. - **Industrial**: Anticipated growth from $0.52 billion in 2023 to $1.10 billion in 2033, sustaining a market share of 10.42%. - **Utility**: Expected to grow from $0.62 billion in 2023 to $1.31 billion by 2033, capturing 12.46% of the market.

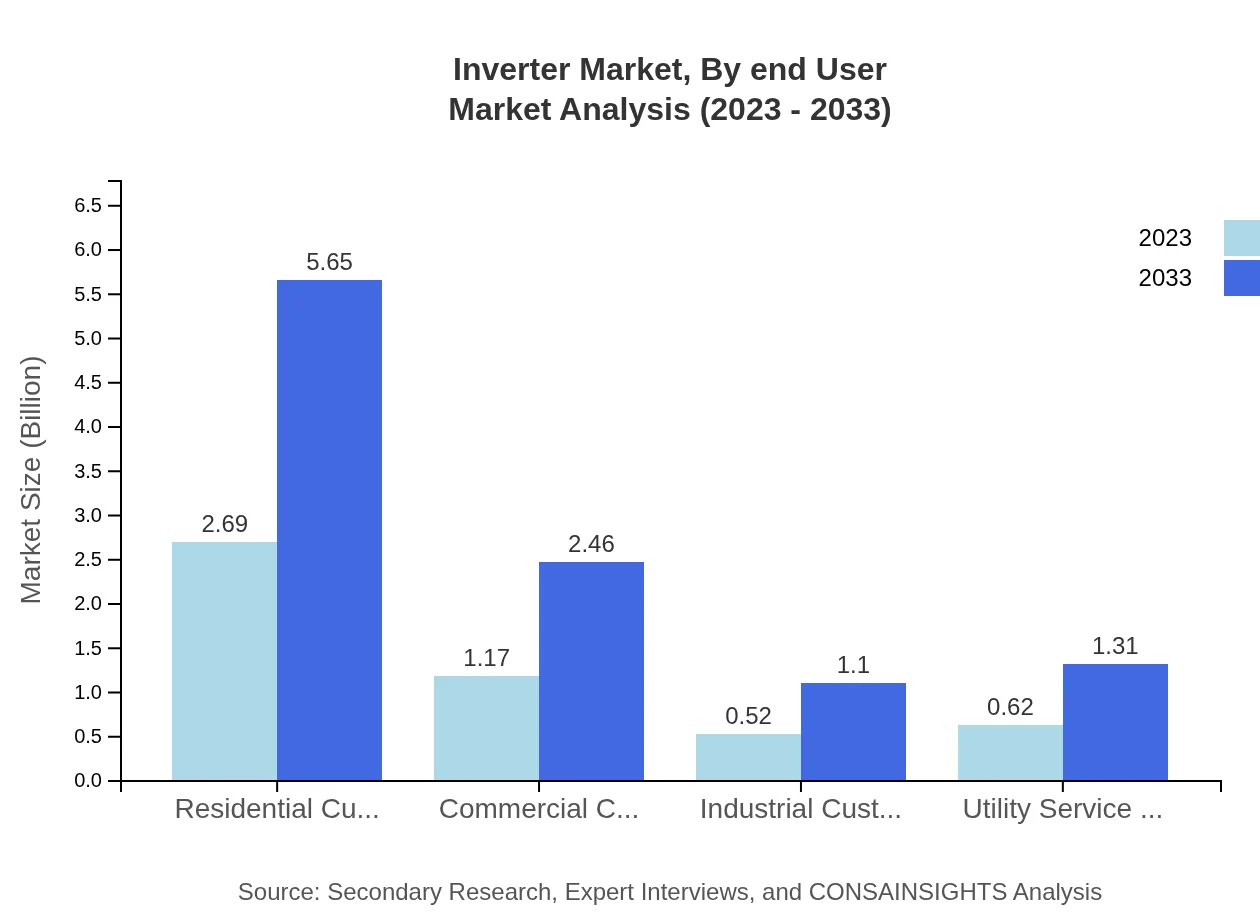

Inverter Market Analysis By End User

Inverter market segmentation by end-user includes: - **Residential Customers**: Market size anticipated to increase from $2.69 billion in 2023 to $5.65 billion by 2033, representing 53.71% share. - **Commercial Customers**: Expected growth from $1.17 billion in 2023 to $2.46 billion in 2033, holding 23.41% of the market. - **Industrial Customers**: Projected increase from $0.52 billion in 2023 to $1.10 billion by 2033, maintaining a share of 10.42%. - **Utility Service Providers**: Expected to grow from $0.62 billion in 2023 to $1.31 billion in 2033, with a share of 12.46%.

Inverter Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Inverter Industry

SMA Solar Technology:

SMA is a global leader in photovoltaic inverters, specializing in developing innovative energy solutions that optimize solar energy generation.Fronius International:

Fronius is known for its cutting-edge inverter technology offering high efficiency and reliable services, fostering sustainability through solar energy.SolarEdge Technologies:

Specializing in smart inverter technology, SolarEdge offers innovative power optimization solutions that enhance energy harvesting in solar products.ABB Ltd.:

ABB delivers a wide range of inverter solutions with advanced technology aimed at increasing efficiency in the power and industrial markets.Enphase Energy:

Known for manufacturing micro-inverters, Enphase focuses on energy management solutions that provide reliable performance in solar applications.We're grateful to work with incredible clients.

FAQs

What is the market size of inverters?

The global inverter market, valued at $5 billion in 2023, is projected to grow at a CAGR of 7.5% reaching approximately $11 billion by 2033. This growth reflects increasing adoption of renewable energy technologies and advancements in inverter technology.

What are the key market players or companies in the inverter industry?

Key market players in the inverter industry include major companies like SMA Solar Technology AG, ABB Ltd., Schneider Electric, Enphase Energy, and Huawei Technologies Co., Ltd. These companies lead the market through innovation and comprehensive product offerings.

What are the primary factors driving the growth in the inverter industry?

The growth in the inverter industry is primarily driven by the rising demand for renewable energy sources, government incentives for solar energy adoption, the need for energy storage solutions, and advancements in inverter technologies, increasing system efficiency and reliability.

Which region is the fastest Growing in the inverter market?

The forecast shows that Europe is the fastest-growing region for inverters, with the market expanding from $1.69 billion in 2023 to $3.57 billion by 2033. Asia Pacific also shows significant growth, increasing from $0.88 billion to $1.85 billion in the same period.

Does ConsaInsights provide customized market report data for the inverter industry?

Yes, ConsaInsights offers customized market reports to suit specific client needs in the inverter industry. Clients can request tailored analysis focusing on particular segments, geographies, or trends to gain unique insights and competitive advantages.

What deliverables can I expect from this inverter market research project?

Deliverables from the inverter market research project include comprehensive market analysis reports, data on market size and projections, evaluations of competitive landscapes, and insights into regional trends, along with specific segment analyses tailored to client requirements.

What are the market trends of inverters?

Current market trends in inverters include the shift towards more efficient grid-tied and off-grid systems, increased adoption of battery inverters, growing integration of smart technology, and the expansion of micro inverter applications in residential settings.