Lipid Disorder Treatment Market Report

Published Date: 31 January 2026 | Report Code: lipid-disorder-treatment

Lipid Disorder Treatment Market Size, Share, Industry Trends and Forecast to 2033

This report provides a comprehensive analysis of the Lipid Disorder Treatment market, including insights on market trends, size, and forecasts from 2023 to 2033. It explores various segments, regional dynamics, and the competitive landscape within this growing industry.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

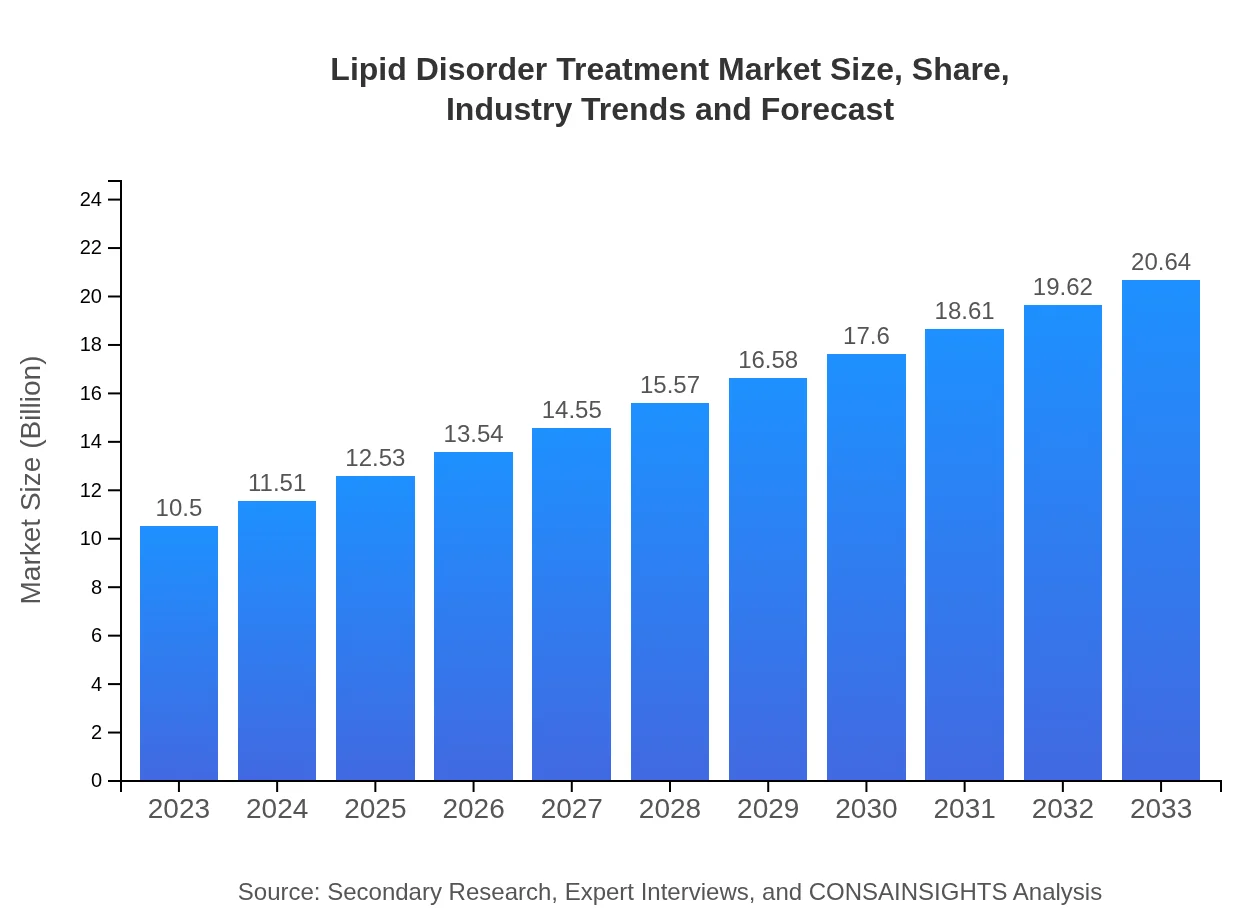

| 2023 Market Size | $10.50 Billion |

| CAGR (2023-2033) | 6.8% |

| 2033 Market Size | $20.64 Billion |

| Top Companies | Pfizer Inc., Amgen Inc., Sanofi, Merck & Co. |

| Last Modified Date | 31 January 2026 |

Lipid Disorder Treatment Market Overview

Customize Lipid Disorder Treatment Market Report market research report

- ✔ Get in-depth analysis of Lipid Disorder Treatment market size, growth, and forecasts.

- ✔ Understand Lipid Disorder Treatment's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Lipid Disorder Treatment

What is the Market Size & CAGR of Lipid Disorder Treatment market in 2023?

Lipid Disorder Treatment Industry Analysis

Lipid Disorder Treatment Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Lipid Disorder Treatment Market Analysis Report by Region

Europe Lipid Disorder Treatment Market Report:

The European market for Lipid Disorder Treatment is projected to grow significantly from $2.91 billion in 2023 to $5.73 billion by 2033. A strong emphasis on preventive healthcare and the availability of advanced treatment options play integral roles in this expansion, with countries such as Germany, France, and the UK leading the charge.Asia Pacific Lipid Disorder Treatment Market Report:

The Asia Pacific region is witnessing substantial growth in the Lipid Disorder Treatment market, projected to increase from $2.03 billion in 2023 to $3.99 billion by 2033. Increasing awareness about lifestyle diseases and enhancing healthcare infrastructure contribute to this growth. Countries like China and India are leading this trend due to rising patient populations and improved access to treatment.North America Lipid Disorder Treatment Market Report:

North America remains a leading market for Lipid Disorder Treatment, anticipated to grow from $3.97 billion in 2023 to $7.80 billion by 2033. This growth is driven by a greater prevalence of lipid disorders, substantial healthcare expenditure, and the presence of key pharmaceutical companies that drive innovation in treatment.South America Lipid Disorder Treatment Market Report:

In South America, the Lipid Disorder Treatment market is expected to grow from $0.31 billion in 2023 to $0.60 billion by 2033. This region is benefitting from an increase in healthcare accessibility and rising incidences of cardiovascular diseases, making lipid disorder management a priority area for healthcare providers.Middle East & Africa Lipid Disorder Treatment Market Report:

In the Middle East and Africa, the market is estimated to grow from $1.28 billion in 2023 to $2.51 billion by 2033. Factors such as rising healthcare investments, increasing awareness of lipid disorders, and improvements in the healthcare system drive growth in this region.Tell us your focus area and get a customized research report.

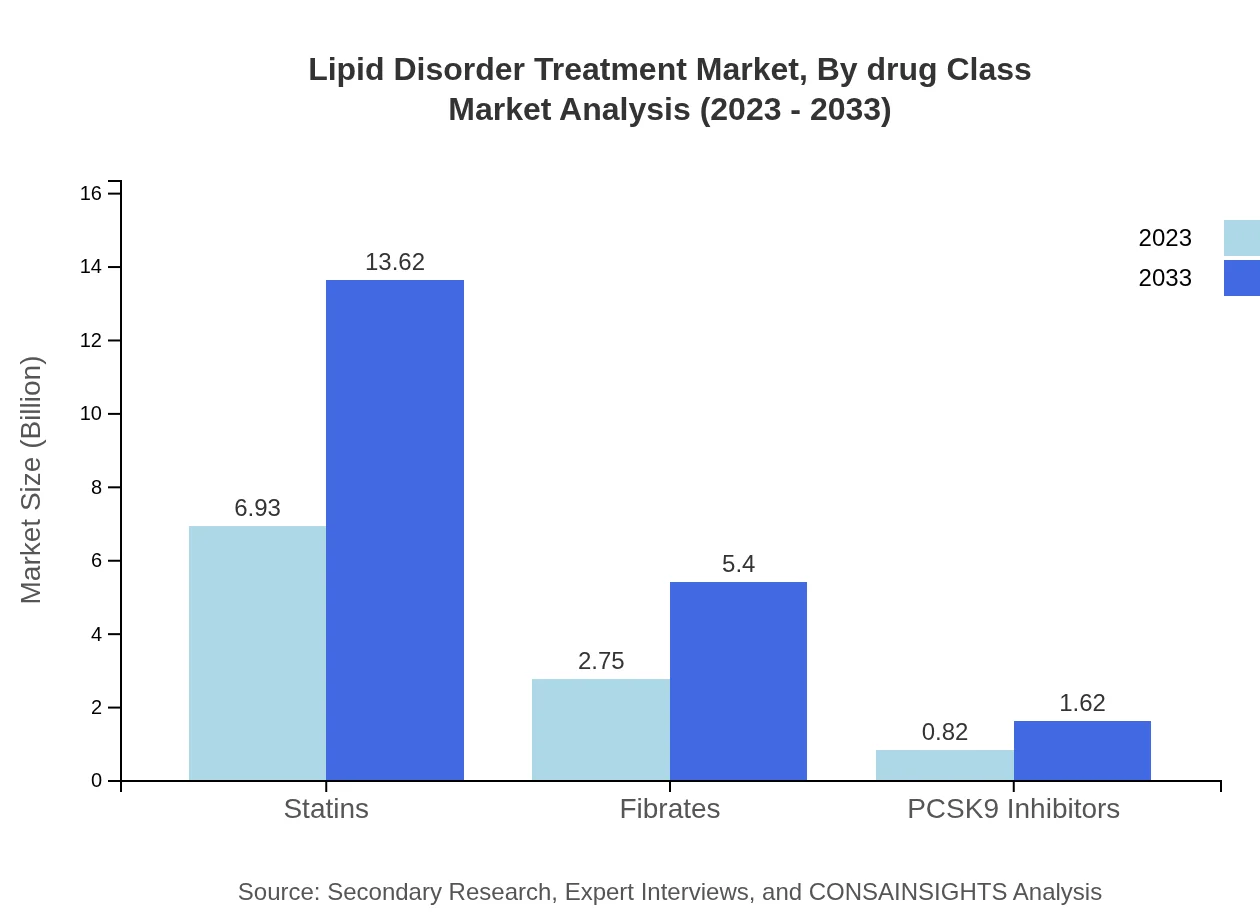

Lipid Disorder Treatment Market Analysis By Drug Class

The Lipid Disorder Treatment market by drug class is largely led by Statins, which hold a market size of $6.93 billion in 2023, projected to grow to $13.62 billion by 2033. Other classes like fibrates and PCSK9 inhibitors follow, constituting an essential part of the treatment strategy.

Lipid Disorder Treatment Market Analysis By Indication

Global Lipid Disorder Treatment Market, By Indication Market Analysis (2023 - 2033)

Indications such as Hyperlipidemia and Atherosclerosis dominate the market, with Hyperlipidemia accounting for $6.93 billion in 2023, expected to reach $13.62 billion by 2033. Other indications represent a growing niche, driving the diversification of treatments provided.

Lipid Disorder Treatment Market Analysis By Formulation

Global Lipid Disorder Treatment Market, By Formulation Market Analysis (2023 - 2033)

Formulations primarily include Tablets, which dominate the market with a size of $6.93 billion in 2023 and a projected growth to $13.62 billion by 2033. Injections and oral solutions, although smaller segments, are also witnessing incremental growth.

Lipid Disorder Treatment Market Analysis By Distribution Channel

Global Lipid Disorder Treatment Market, By Distribution Channel Market Analysis (2023 - 2033)

Hospital Pharmacies account for a significant market share of 65.98% in the Lipid Disorder Treatment landscape, projected to maintain that share into 2033. Retail pharmacies and online pharmacies are also growing, reflecting changes in consumer purchasing behaviors.

Lipid Disorder Treatment Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Lipid Disorder Treatment Industry

Pfizer Inc.:

A global powerhouse known for its innovative statins, Pfizer is a leader in the Lipid Disorder Treatment market, continually investing in R&D and expanding its portfolio.Amgen Inc.:

Renowned for its PCSK9 inhibitors, Amgen significantly contributes to the market by addressing high cholesterol levels in patients, showcasing its dedication to improving therapeutic options.Sanofi:

A key player in the Lipid Disorder Treatment sector, Sanofi develops various lipid-lowering therapies and focuses on expanding its global presence.Merck & Co.:

Merck is known for its extensive research in lipidology and produces several essential drugs that help manage lipid disorders, enhancing patient outcomes.We're grateful to work with incredible clients.

FAQs

What is the market size of lipid Disorder Treatment?

The lipid-disorder-treatment market is estimated to reach approximately $10.5 billion by 2033, growing steadily at a CAGR of 6.8% during the forecast period. This growth is driven by increasing awareness and prevalence of lipid-related disorders globally.

What are the key market players or companies in this lipid Disorder Treatment industry?

Key players in the lipid-disorder-treatment market include major pharmaceutical companies, biotechnology firms, and specialty medication providers. These companies are pivotal in research and development, contributing significantly to innovations and market expansion.

What are the primary factors driving the growth in the lipid Disorder Treatment industry?

Growth in the lipid-disorder-treatment market is primarily driven by rising incidences of hyperlipidemia, increased aging population, and advancements in drug formulations. Additionally, heightened patient awareness and enhanced healthcare accessibility are significant contributors.

Which region is the fastest Growing in the lipid Disorder Treatment?

The North America region is the fastest-growing market for lipid-disorder-treatment, projected to grow from $3.97 billion in 2023 to $7.80 billion by 2033. Europe and Asia Pacific follow closely, indicating healthy market expansion.

Does ConsaInsights provide customized market report data for the lipid Disorder Treatment industry?

Yes, Consainsights offers customized market report data tailored to specific needs within the lipid-disorder-treatment industry, ensuring comprehensive insights that address unique client requirements and market dynamics.

What deliverables can I expect from this lipid Disorder Treatment market research project?

From the lipid-disorder-treatment market research project, clients can expect detailed market analysis, segmentation insights, competitive landscapes, regional data, and forecasts covering the period up to 2033, along with strategic recommendations.

What are the market trends of lipid Disorder Treatment?

Key trends in the lipid-disorder-treatment market include the rise of personalized medicine, increased focus on preventive healthcare, and the growing adoption of telemedicine services. These trends indicate a shift towards more patient-centric approaches in lipid disorder management.