Military Simulator Market Report

Published Date: 03 February 2026 | Report Code: military-simulator

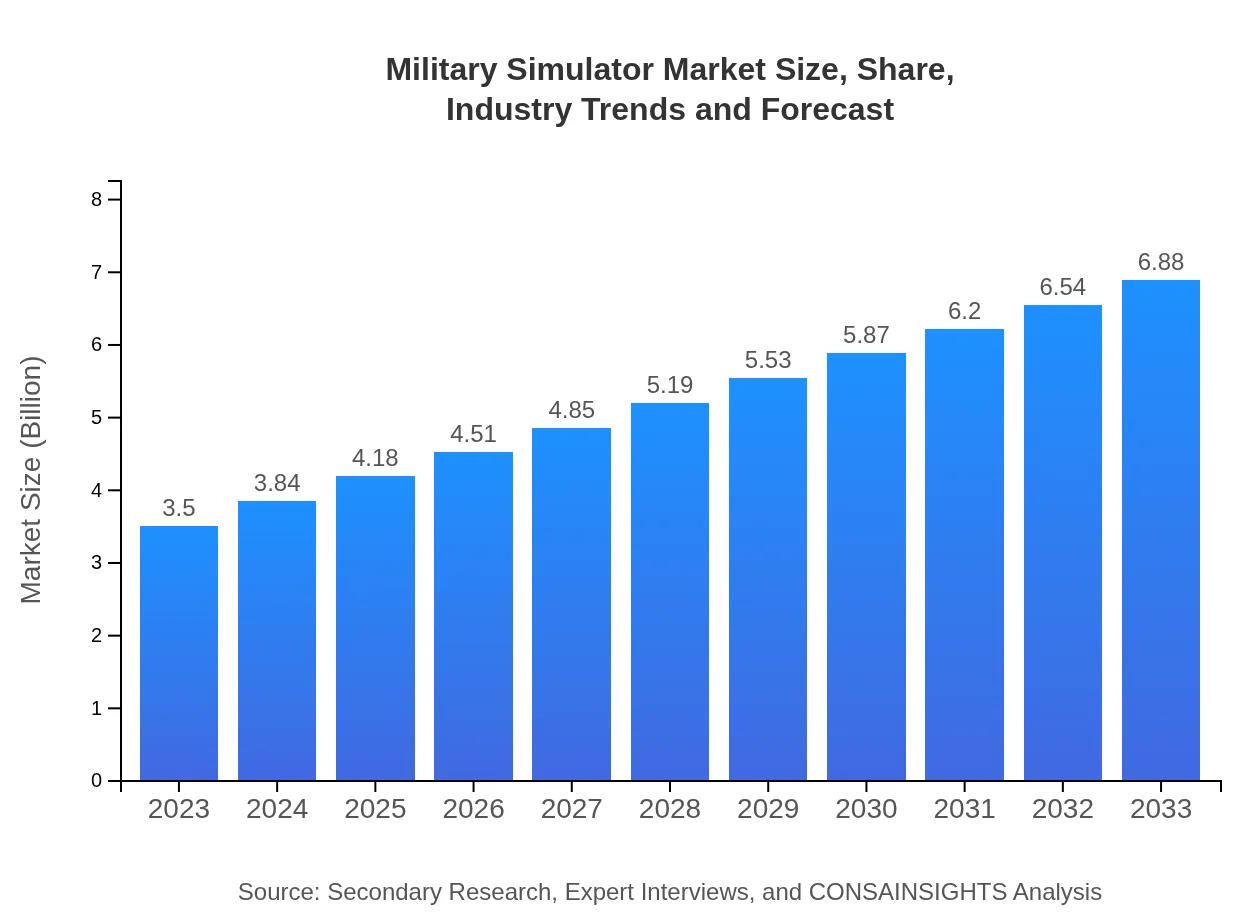

Military Simulator Market Size, Share, Industry Trends and Forecast to 2033

This report provides an in-depth analysis of the Military Simulator market, covering vital insights, market trends, and comprehensive data from 2023 to 2033, including segmentation, regional analysis, industry leaders, and future forecasts.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $3.50 Billion |

| CAGR (2023-2033) | 6.8% |

| 2033 Market Size | $6.88 Billion |

| Top Companies | Lockheed Martin, BAE Systems, Northrop Grumman, Thales Group |

| Last Modified Date | 03 February 2026 |

Military Simulator Market Overview

Customize Military Simulator Market Report market research report

- ✔ Get in-depth analysis of Military Simulator market size, growth, and forecasts.

- ✔ Understand Military Simulator's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Military Simulator

What is the Market Size & CAGR of Military Simulator market in 2023?

Military Simulator Industry Analysis

Military Simulator Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Military Simulator Market Analysis Report by Region

Europe Military Simulator Market Report:

Europe experiences a burgeoning Military Simulator market, valued at USD 1.03 billion in 2023, projected to reach USD 2.03 billion by 2033. Increasing military collaborations among NATO countries and a focus on modernizing defense capabilities are key drivers of growth in this region.Asia Pacific Military Simulator Market Report:

In 2023, the Military Simulator market in the Asia Pacific region is valued at USD 0.76 billion and is projected to reach USD 1.49 billion by 2033. The growth is attributed to increased defense spending by countries like India and China, and the rising need for advanced training methods within the rapidly changing geopolitical landscape.North America Military Simulator Market Report:

The North American market, particularly dominated by the United States, is valued at USD 1.17 billion in 2023, growing to USD 2.30 billion by 2033. The robust growth is driven by significant military investments and technological advancements in simulation training, especially in defense and homeland security sectors.South America Military Simulator Market Report:

In South America, the Military Simulator market is valued at USD 0.05 billion in 2023 and is expected to grow to USD 0.10 billion by 2033. The growth in this region is relatively slow, primarily due to lower defense budgets and limited investments in military technologies.Middle East & Africa Military Simulator Market Report:

The Middle East and Africa market is valued at USD 0.49 billion in 2023 and is expected to reach USD 0.96 billion by 2033. Growing tensions in various regions and heightened security concerns contribute to the increasing investment in military training solutions.Tell us your focus area and get a customized research report.

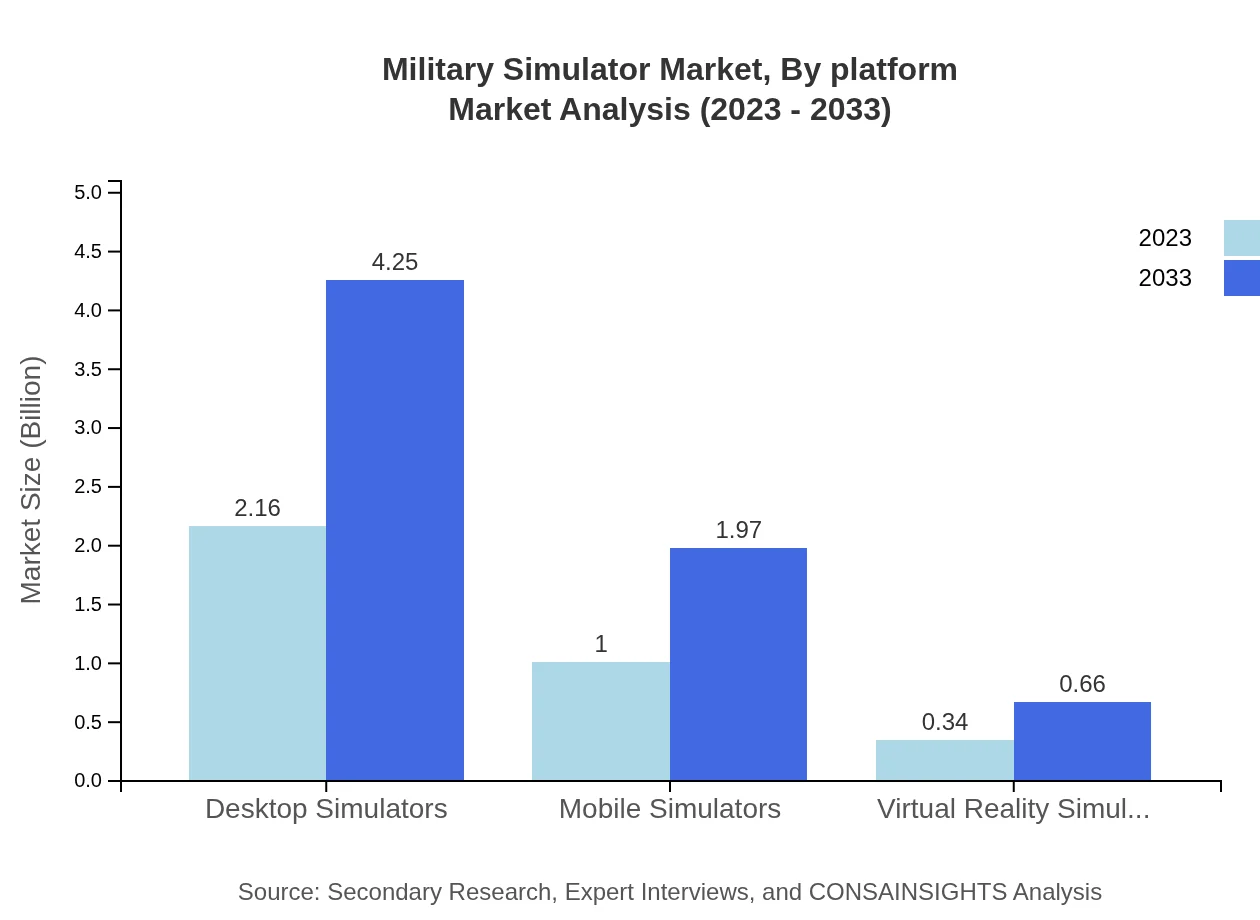

Military Simulator Market Analysis By Platform

The Military Simulator market by platform includes desktop, mobile, and virtual reality simulators. The desktop segment dominates with a market size of USD 2.16 billion in 2023, expected to grow to USD 4.25 billion by 2033. Mobile simulators, valued at USD 1.00 billion in 2023, are burgeoning due to their accessibility, while VR simulators represent a growing niche with a market size of USD 0.34 billion in 2023, rising to USD 0.66 billion by 2033.

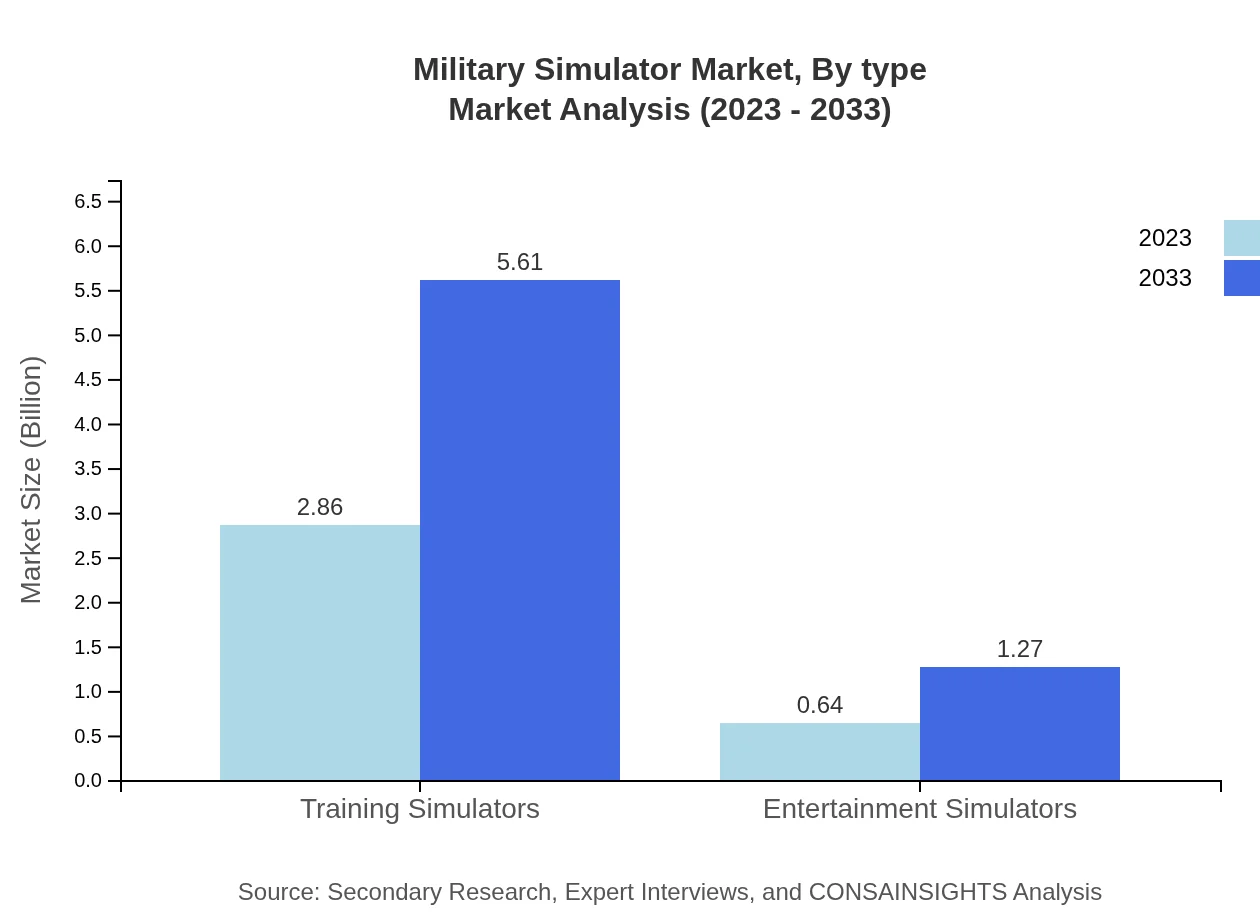

Military Simulator Market Analysis By Type

The market is segmented into training simulators and entertainment simulators, where training simulators overwhelmingly lead with a size of USD 2.86 billion in 2023 and a projected growth to USD 5.61 billion by 2033. Entertainment simulators, while smaller with a market size of USD 0.64 billion in 2023, show promising growth potential as they enhance public understanding and engagement with military capabilities.

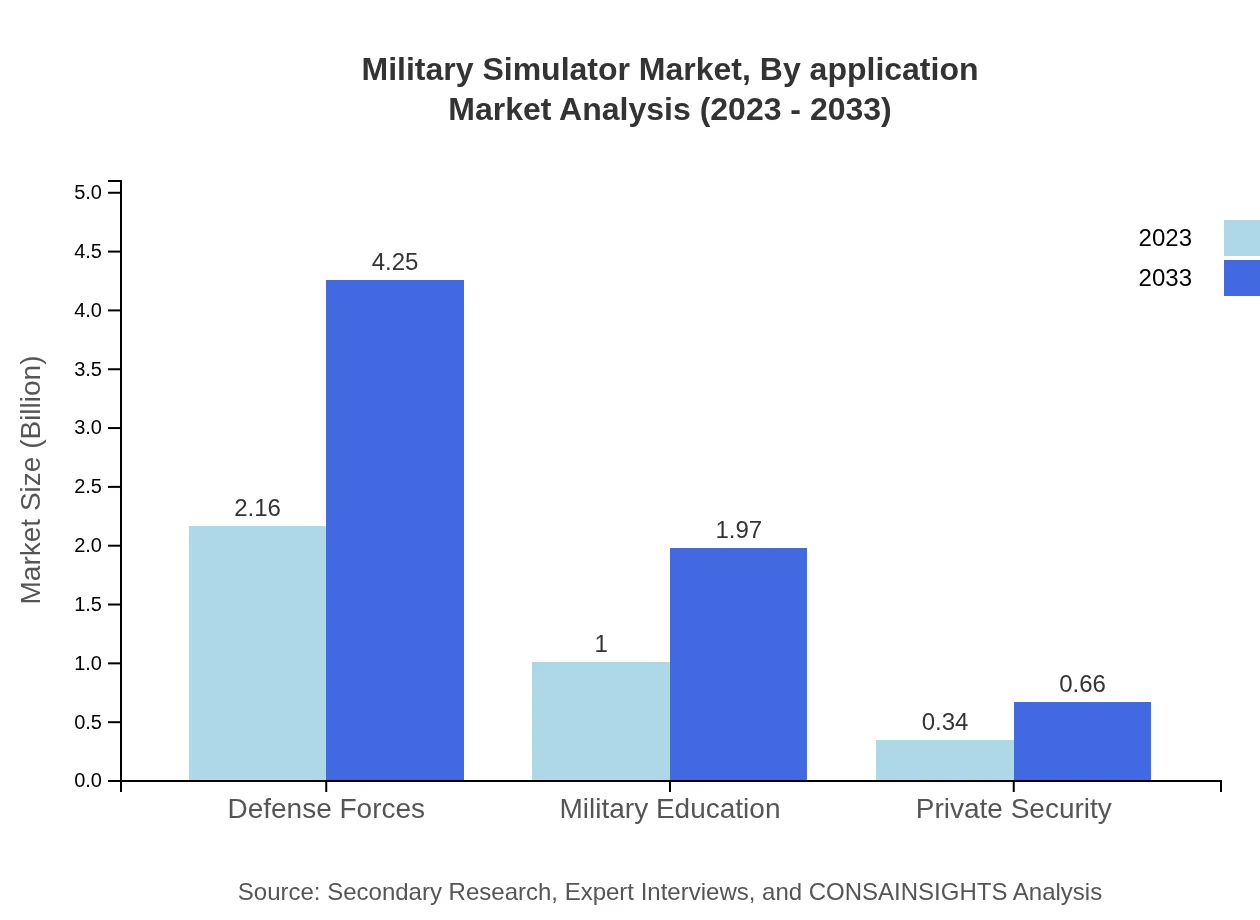

Military Simulator Market Analysis By Application

The application of Military Simulators spans defense forces, military education, and private security. The defense forces segment holds a market size of USD 2.16 billion in 2023, while military education is significant, valued at USD 1.00 billion, indicating the critical role of simulators in effective training programs.

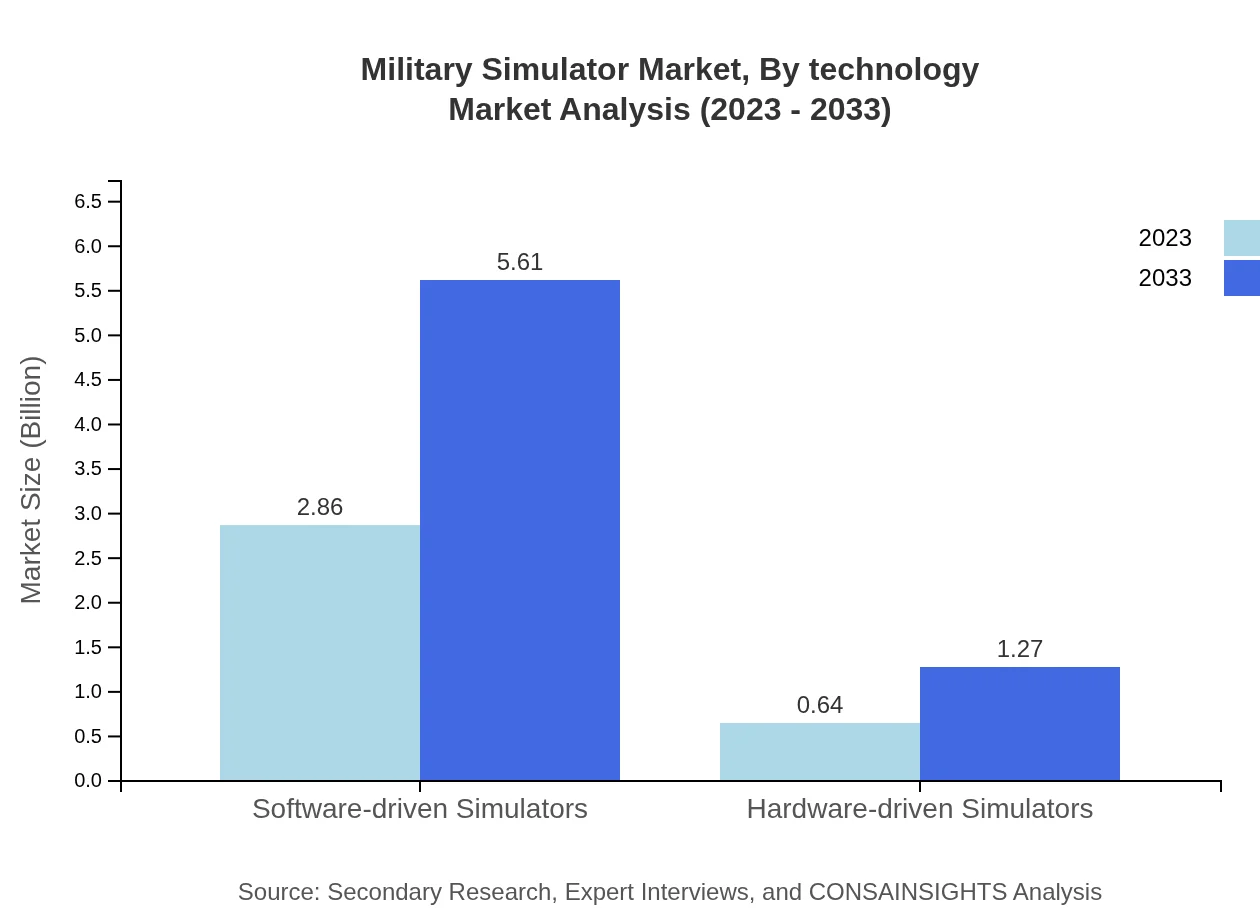

Military Simulator Market Analysis By Technology

Technology segmentation covers software-driven and hardware-driven simulators. The software-driven segment holds a substantial market share, valued at USD 2.86 billion in 2023, growing to USD 5.61 billion by 2033. Hardware-driven simulators are smaller but essential, valued at USD 0.64 billion in 2023, with anticipated growth as technology continues to integrate with simulation training.

Military Simulator Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Military Simulator Industry

Lockheed Martin:

Lockheed Martin specializes in advanced simulation solutions, providing military organizations with cutting-edge training systems that enhance operational readiness and performance.BAE Systems:

BAE Systems offers a range of military training solutions, including simulation technologies that support defense forces with innovative training and operational support.Northrop Grumman:

Northrop Grumman develops advanced simulation capabilities for military applications, focusing on creating realistic environments for training and mission rehearsal.Thales Group:

Thales Group provides simulation solutions that integrate immersive technologies for effective military training, contributing to operational excellence.We're grateful to work with incredible clients.

FAQs

What is the market size of military Simulator?

The military simulator market is projected to reach approximately $3.5 billion by 2033, growing at a CAGR of 6.8% from its current size. This growth reflects advancements in technology and increased demand for training solutions.

What are the key market players or companies in this military Simulator industry?

Major players in the military simulator market include established defense contractors and technology companies, focusing on developing innovative simulation solutions. These include companies specializing in software and hardware integrations essential for military training applications.

What are the primary factors driving the growth in the military Simulator industry?

Key drivers for growth in the military simulator industry include technological advancements, increased defense budgets globally, and a shift towards incorporating immersive training solutions, such as virtual and augmented reality simulations in defense training.

Which region is the fastest Growing in the military Simulator?

The fastest-growing region in the military simulator market is Europe, expected to grow from $1.03 billion in 2023 to $2.03 billion by 2033. This growth is driven by increasing defense expenditures and technological investments in training programs.

Does ConsaInsights provide customized market report data for the military Simulator industry?

Yes, Consainsights offers customized market report data tailored to specific user needs within the military simulator industry, enabling clients to receive specific insights, analyses, and forecasts for their strategic planning.

What deliverables can I expect from this military Simulator market research project?

Deliverables from the military simulator market research include detailed reports, market trends, competitive landscape analysis, regional insights, and forecasts, equipping clients with data for informed decision-making.

What are the market trends of military Simulator?

Current market trends in the military simulator sector highlight the rise of software-driven simulations, with training simulators dominating market share. Moreover, the adoption of mobile and virtual reality technologies is becoming increasingly prominent.