Mobile Phone Semiconductor Market Report

Published Date: 31 January 2026 | Report Code: mobile-phone-semiconductor

Mobile Phone Semiconductor Market Size, Share, Industry Trends and Forecast to 2033

This report presents a comprehensive analysis of the Mobile Phone Semiconductor market, focusing on crucial insights, market trends, and forecasts spanning the years 2023 to 2033, including segments and regional evaluations.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

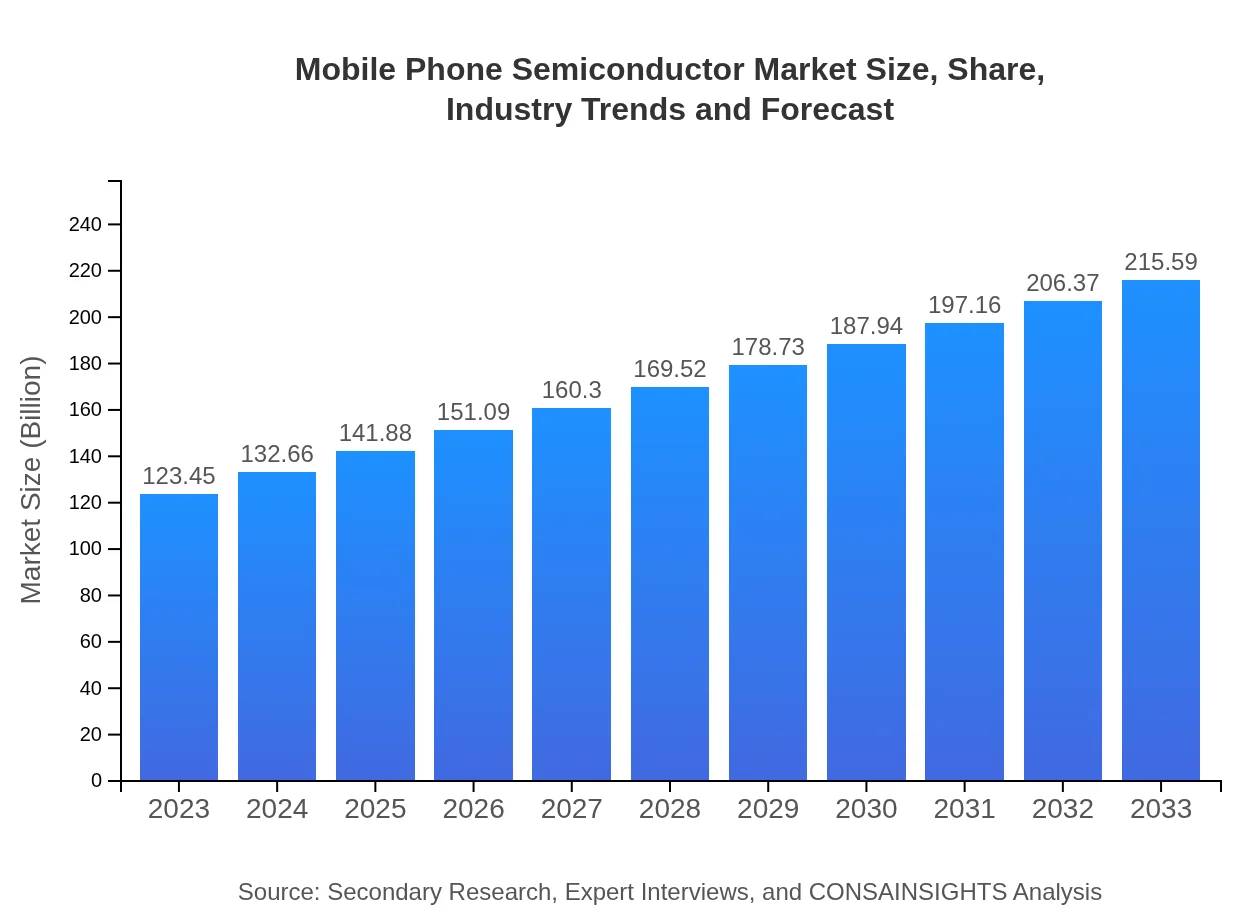

| 2023 Market Size | $123.45 Billion |

| CAGR (2023-2033) | 5.6% |

| 2033 Market Size | $215.59 Billion |

| Top Companies | Qualcomm , Samsung Electronics, Intel Corporation, MediaTek, Broadcom Inc. |

| Last Modified Date | 31 January 2026 |

Mobile Phone Semiconductor Market Overview

Customize Mobile Phone Semiconductor Market Report market research report

- ✔ Get in-depth analysis of Mobile Phone Semiconductor market size, growth, and forecasts.

- ✔ Understand Mobile Phone Semiconductor's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Mobile Phone Semiconductor

What is the Market Size & CAGR of Mobile Phone Semiconductor market in 2023?

Mobile Phone Semiconductor Industry Analysis

Mobile Phone Semiconductor Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Mobile Phone Semiconductor Market Analysis Report by Region

Europe Mobile Phone Semiconductor Market Report:

Europe's market, currently at $36.43 billion in 2023, is anticipated to grow to $63.62 billion by 2033. The region demonstrates strong regulatory frameworks promoting technological advancements and sustainability, which heavily influence semiconductor demand in mobile devices.Asia Pacific Mobile Phone Semiconductor Market Report:

The Asia-Pacific region, valued at $23.69 billion in 2023 and projected to reach $41.37 billion by 2033, leads the global market owing to the presence of major semiconductor manufacturers and smartphone producers. Growing consumer demand for advanced mobile features propels innovation and production efficiency in this region.North America Mobile Phone Semiconductor Market Report:

North America shows a market size of $40.02 billion in 2023, projected to rise to $69.89 billion by 2033. The region is characterized by a robust technology landscape, with numerous companies investing in semiconductor production and innovation to cater to the needs of high-tech markets.South America Mobile Phone Semiconductor Market Report:

In South America, the market is valued at $10.90 billion in 2023, with expectations to grow to $19.04 billion by 2033. The increasing penetration of smartphones and mobile technology adoption among consumers is boosting the semiconductor demand in this region, showcasing significant growth potential.Middle East & Africa Mobile Phone Semiconductor Market Report:

The Middle East and Africa market is relatively smaller, sized at $12.41 billion in 2023, expected to reach $21.67 billion by 2033. However, increasing smartphone adoption and investments in digital infrastructures are contributing positively towards the growth of the semiconductor market in these regions.Tell us your focus area and get a customized research report.

Mobile Phone Semiconductor Market Analysis By Technology

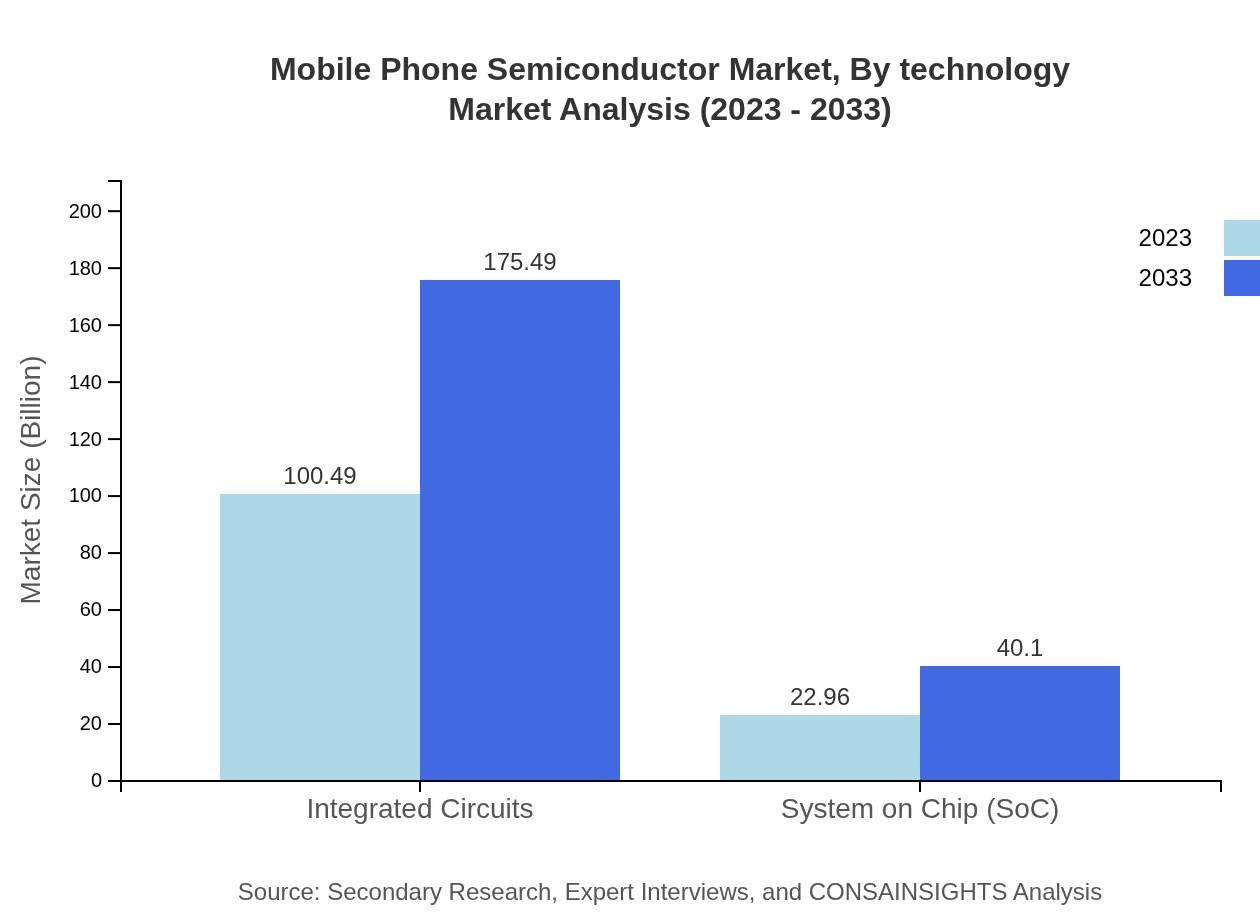

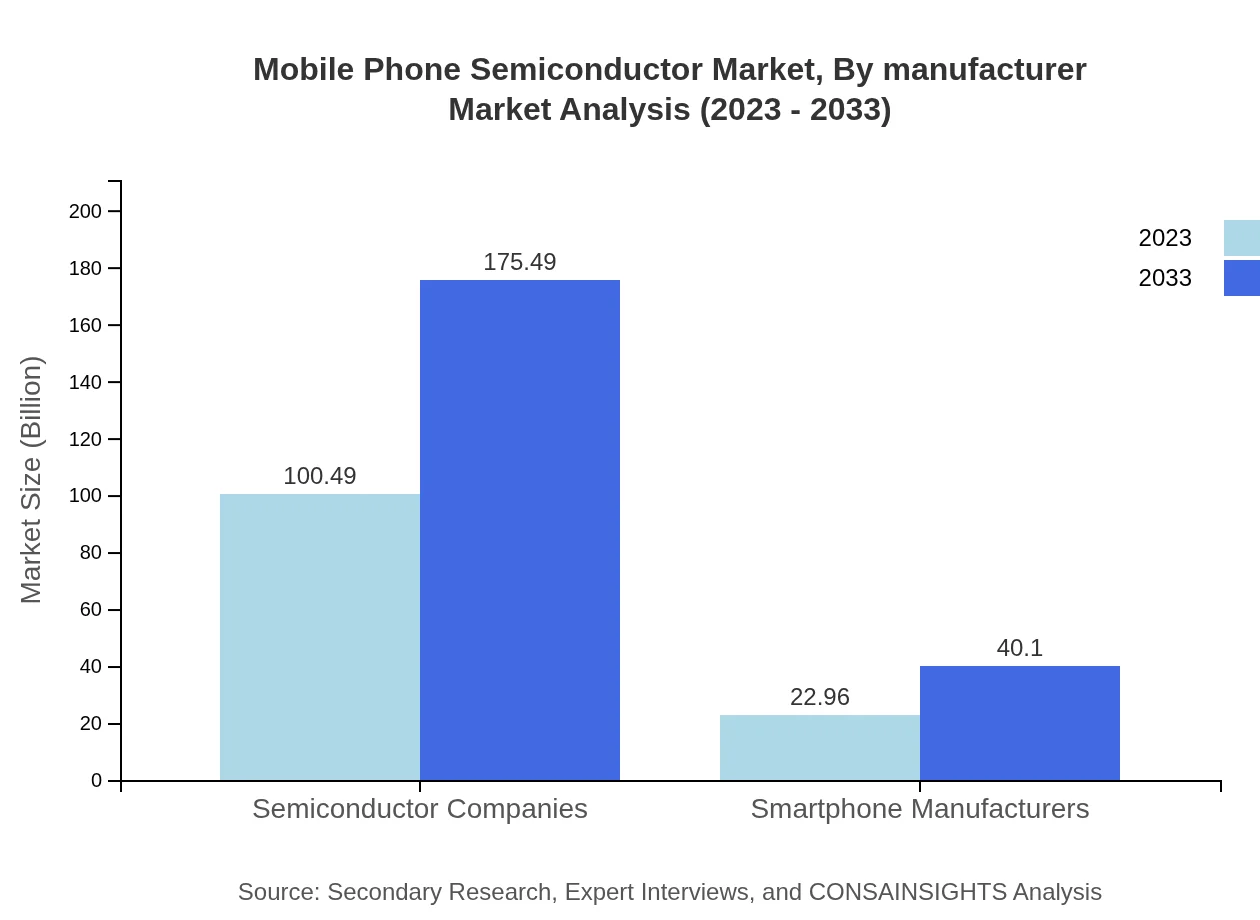

The Mobile Phone Semiconductor market, segmented by technology, reflects significant trends in integrated circuits and System on Chips (SoC). Integrated Circuits dominate the sector with a market size of $100.49 billion in 2023, rising to $175.49 billion by 2033, maintaining a dominant market share of 81.4% throughout the forecast period. SoC also shows robust growth, expected to increase from $22.96 billion in 2023 to $40.10 billion in 2033, indicating a more integrated and multifunctional semiconductor landscape.

Mobile Phone Semiconductor Market Analysis By Product Type

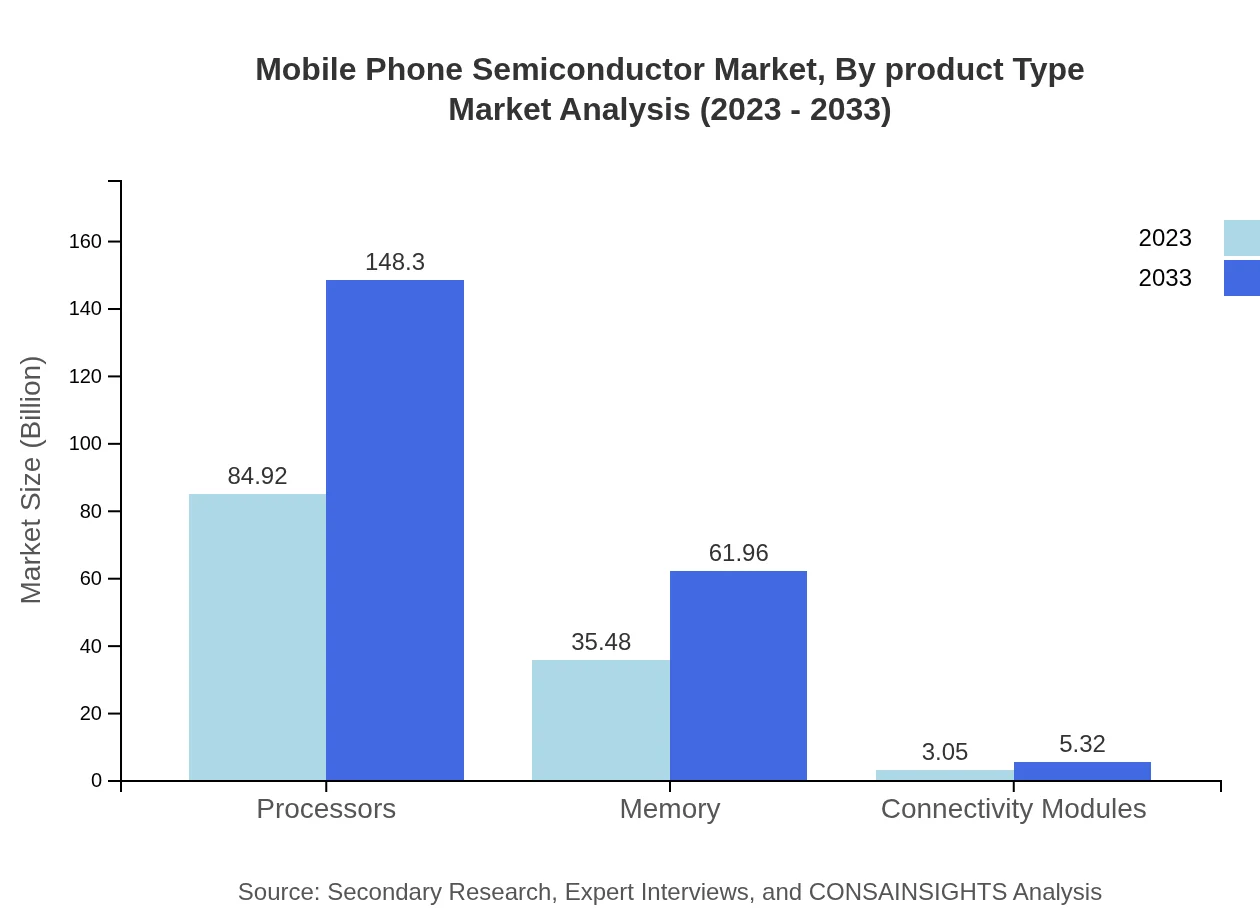

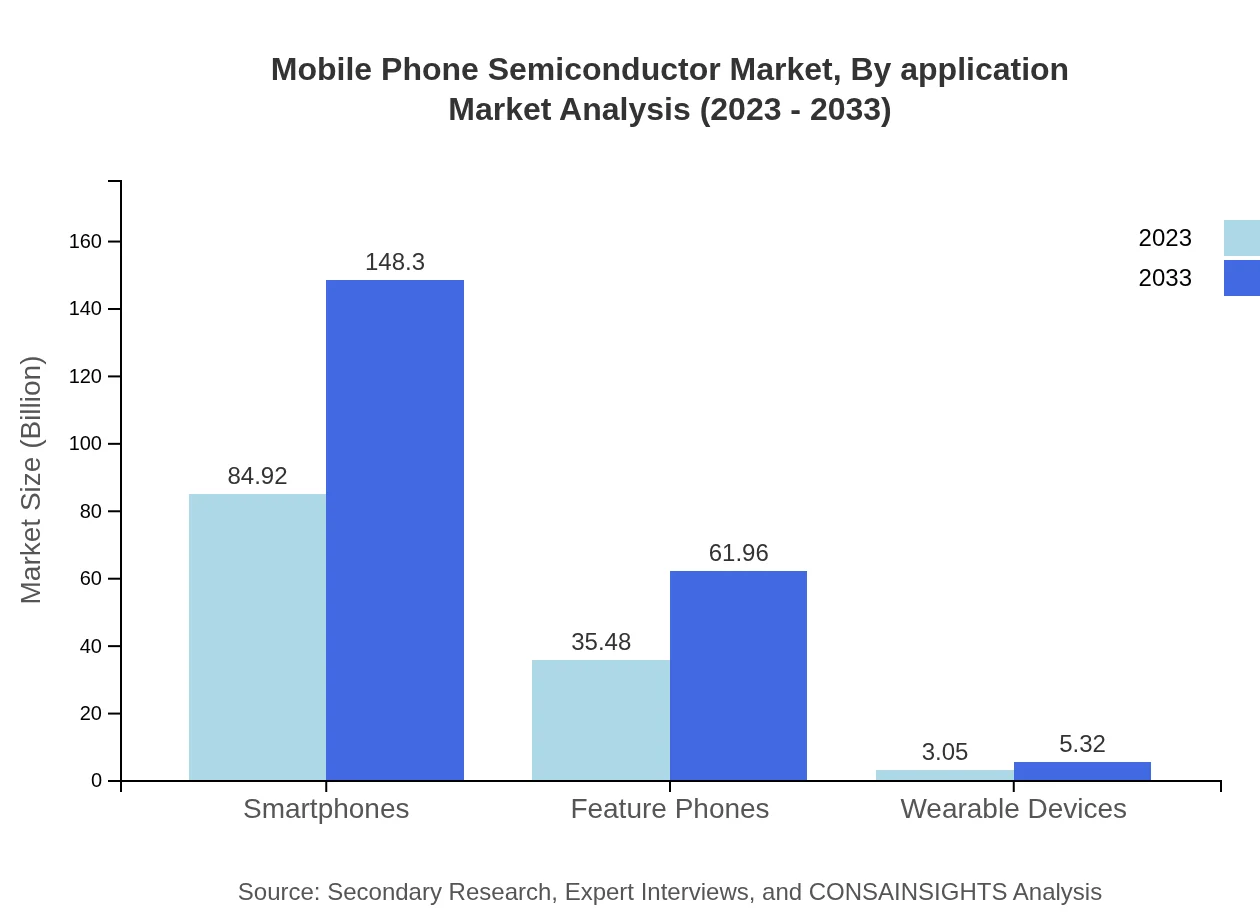

In product categories, smartphones lead the market with a size of $84.92 billion in 2023, forecasted to grow to $148.30 billion by 2033, reflecting a 68.79% market share. Feature phones and wearable devices present smaller markets but are expected to show significant growth, particularly feature phones, moving from $35.48 billion to $61.96 billion. This diversification illustrates consumer preferences shifting towards more personalized and varied mobile solutions.

Mobile Phone Semiconductor Market Analysis By Application

The application segment highlights the demand for processors and memory components, essential for the performance of mobile devices. Processors represent a substantial share of the market, projected to grow from $84.92 billion in 2023 to $148.30 billion by 2033, while memory is expected to develop from $35.48 billion to $61.96 billion over the same period. This growth emphasizes the critical role of efficient memory management and processing power in enhancing user experience.

Mobile Phone Semiconductor Market Analysis By Manufacturer

The manufacturer segment reflects the landscape dominated by global giants that continuously enhance their production capabilities and technological advancements. Leading semiconductor manufacturers are adapting to market demands with innovations in circuit design and manufacturing techniques, reinforcing their positions in the evolving mobile phone ecosystem.

Mobile Phone Semiconductor Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Mobile Phone Semiconductor Industry

Qualcomm :

Qualcomm is a leading manufacturer of mobile processors, primarily known for its Snapdragon series, which powers a majority of smartphones worldwide. Its innovations in 5G technology significantly contribute to advancements in mobile communication.Samsung Electronics:

Samsung is a key player in semiconductor manufacturing, specializing in memory chips and System on Chips essential for mobile devices. Its commitment to research and development keeps it at the forefront of the mobile technology revolution.Intel Corporation:

Intel specializes in a wide range of semiconductor technologies, particularly processors that enhance computing power and efficiency in mobile applications. Its efforts in mobile-specific designs continue to expand its footprint in the market.MediaTek:

MediaTek is known for its affordable SoCs that power smartphones across various price ranges, allowing broader access to advanced mobile technologies. Its rapid innovation cycle reflects market trends effectively.Broadcom Inc.:

Broadcom offers a comprehensive array of semiconductor solutions, including wireless communication chips critical for smartphones and IoT applications. The company's strategic acquisitions enhance its product portfolio and market reach.We're grateful to work with incredible clients.

FAQs

What is the market size of the mobile Phone Semiconductor?

The mobile phone semiconductor market is anticipated to reach a size of approximately $123.45 billion by 2033, growing at a CAGR of 5.6%. This growth reflects the increasing demand for advanced mobile technology.

What are the key market players or companies in the mobile Phone Semiconductor industry?

Key players include major semiconductor manufacturers like Qualcomm, MediaTek, Nvidia, Samsung Semiconductors, and Intel. These companies lead in technology advancements and production capabilities, shaping the industry's future.

What are the primary factors driving the growth in the mobile Phone Semiconductor industry?

Growth factors include the rising demand for smartphones, advancements in 5G technology, increased consumer electronics adoption, and innovations in mobile computing, driving semiconductor integration into mobile devices.

Which region is the fastest Growing in the mobile Phone Semiconductor?

Asia Pacific is the fastest-growing region, with the market projected to expand from $23.69 billion in 2023 to $41.37 billion by 2033, fueled by increased smartphone adoption and manufacturing capabilities.

Does ConsaInsights provide customized market report data for the mobile Phone Semiconductor industry?

Yes, ConsaInsights offers customized market report data tailored to specific client requirements in the mobile phone semiconductor sector, allowing businesses to obtain insights directly relevant to their strategies.

What deliverables can I expect from this mobile Phone Semiconductor market research project?

Expect comprehensive deliverables including detailed market analysis, trends, competitive landscape, consumer insights, and forecast data, all designed to inform strategic decisions in the mobile phone semiconductor industry.

What are the market trends of mobile Phone Semiconductor?

Current trends reflect a shift towards integrated solutions, growth in 5G technology adoption, enhanced focus on energy efficiency in semiconductors, and increasing demand for AI-enabled mobile devices.