Neurodiagnostics Market Report

Published Date: 31 January 2026 | Report Code: neurodiagnostics

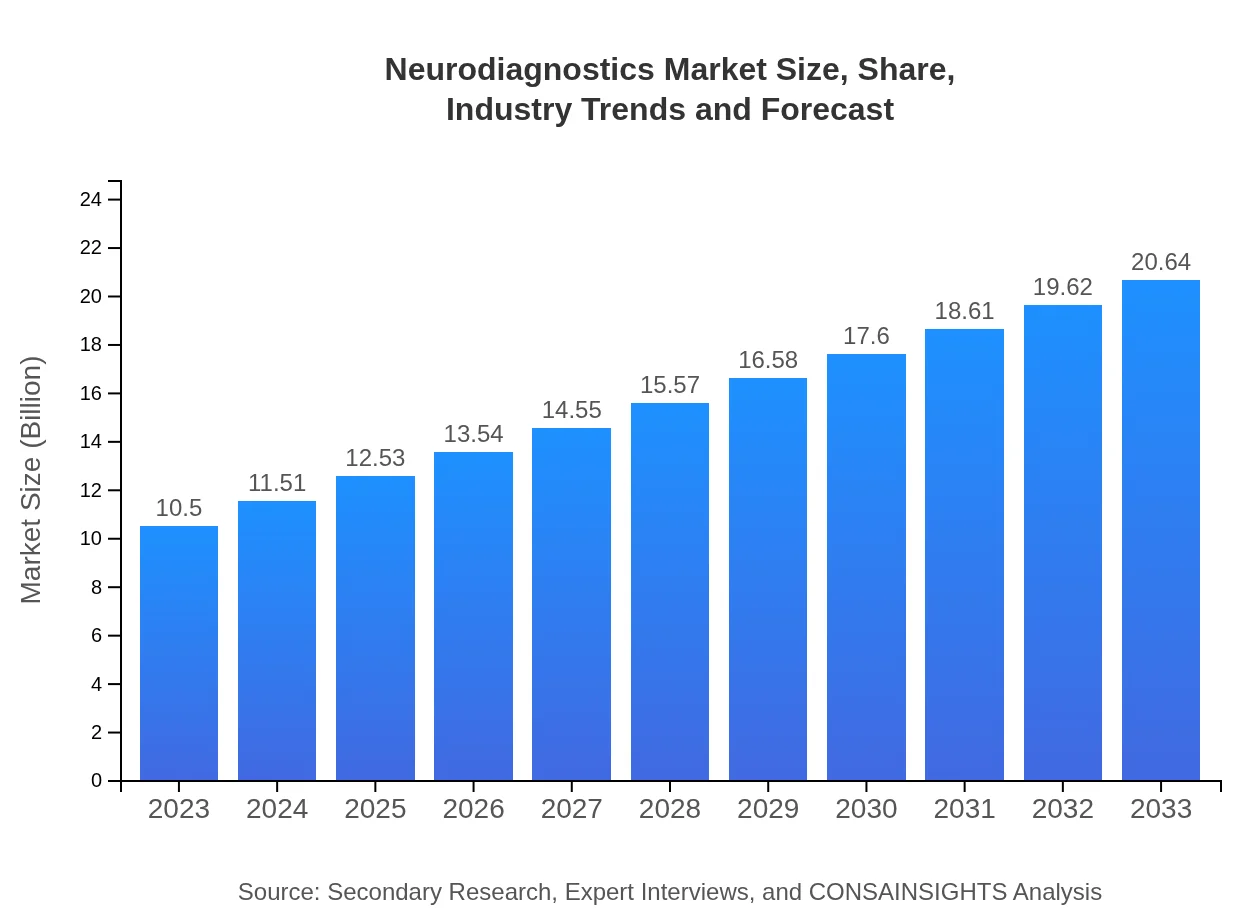

Neurodiagnostics Market Size, Share, Industry Trends and Forecast to 2033

This report provides a comprehensive analysis of the Neurodiagnostics market, covering insights on market size, trends, regional performance, and forecasts through 2033. It aims to equip stakeholders with vital information for informed decision-making.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $10.50 Billion |

| CAGR (2023-2033) | 6.8% |

| 2033 Market Size | $20.64 Billion |

| Top Companies | Medtronic , Philips Healthcare, Natus Medical, GE Healthcare, Siemens Healthineers |

| Last Modified Date | 31 January 2026 |

Neurodiagnostics Market Overview

Customize Neurodiagnostics Market Report market research report

- ✔ Get in-depth analysis of Neurodiagnostics market size, growth, and forecasts.

- ✔ Understand Neurodiagnostics's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Neurodiagnostics

What is the Market Size & CAGR of Neurodiagnostics market in 2033?

Neurodiagnostics Industry Analysis

Neurodiagnostics Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Neurodiagnostics Market Analysis Report by Region

Europe Neurodiagnostics Market Report:

Europe's Neurodiagnostics market is projected to grow from $3.43 billion in 2023 to $6.74 billion by 2033. This region benefits from a robust regulatory environment that stimulates innovation and ensures safety in neurodiagnostic procedures. Furthermore, collaborations between research institutions and healthcare providers are enhancing the development of cutting-edge diagnostic technologies, driving market demand significantly.Asia Pacific Neurodiagnostics Market Report:

The Asia Pacific region shows promising growth potential in the Neurodiagnostics market, projected to increase from $1.80 billion in 2023 to $3.54 billion by 2033. Factors such as increasing healthcare investments, growing prevalence of neurological disorders, and rising awareness about neurodiagnostic technologies contribute to this trend. Additionally, emerging markets like India and China are setting substantial growth benchmarks by augmenting healthcare infrastructure and accessibility.North America Neurodiagnostics Market Report:

North America holds a dominant position in the Neurodiagnostics market, with the market size expected to rise from $3.71 billion in 2023 to $7.29 billion by 2033. The region benefits from advanced healthcare infrastructure, significant R&D investments, and a high prevalence of neurological disorders. The extensive presence of major market players and an increasing number of approved neurodiagnostic devices further solidify its position in the global market.South America Neurodiagnostics Market Report:

In South America, the Neurodiagnostics market is anticipated to double, growing from $0.36 billion in 2023 to $0.71 billion by 2033. The growth is primarily driven by increased government funding for healthcare initiatives and collaborations with international organizations aimed at improving diagnostic services across the region. Nevertheless, challenges such as limited healthcare budgets can hinder exponential growth.Middle East & Africa Neurodiagnostics Market Report:

The Middle East and Africa Neurodiagnostics market is forecasted to grow from $1.20 billion in 2023 to $2.36 billion by 2033. This growth is supported by increasing investments in healthcare infrastructure, awareness campaigns regarding neurological disorders, and demand for advanced medical devices. However, political instability and economic challenges in certain areas could impact growth rates in the region.Tell us your focus area and get a customized research report.

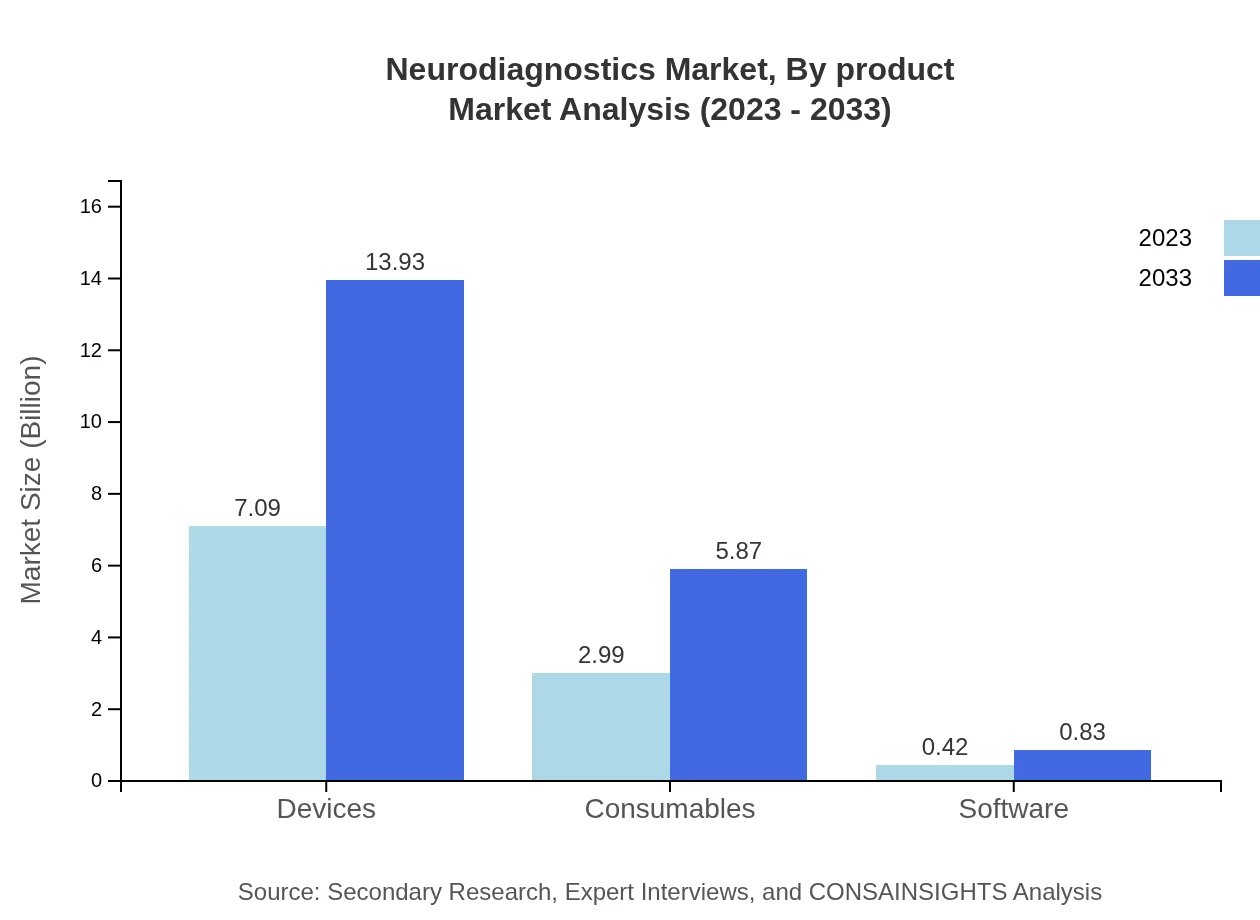

Neurodiagnostics Market Analysis By Product

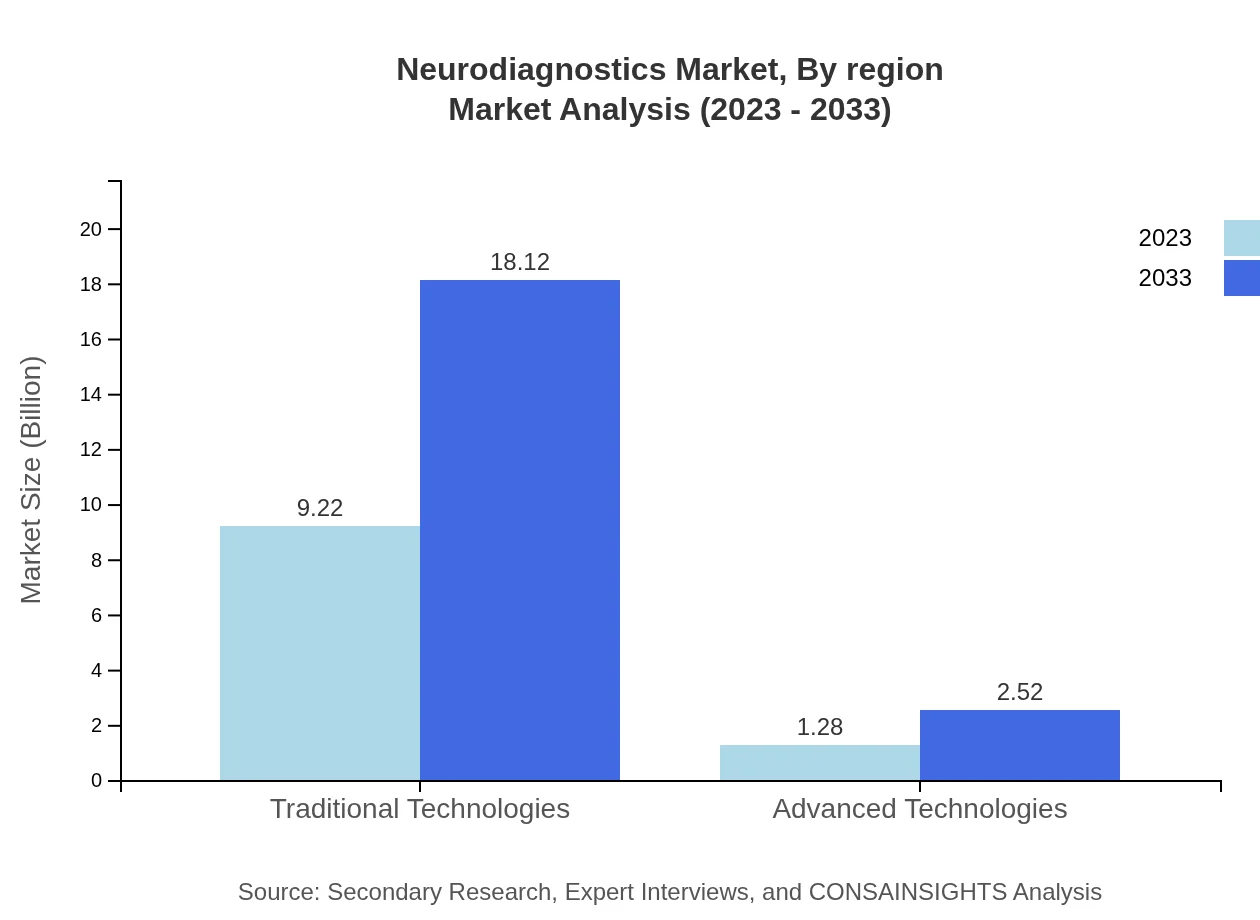

The Neurodiagnostics market by product categories includes traditional and advanced technologies, along with devices, consumables, and software segments. In 2023, traditional technologies stood at $9.22 billion, expected to grow to $18.12 billion by 2033, representing 87.8% of the market share throughout the forecast period. Advanced technologies, though currently smaller at $1.28 billion, are anticipated to grow to $2.52 billion, capturing 12.2% share by 2033, showcasing a trend towards innovation and modern diagnostic solutions. Devices remain the largest segment with $7.09 billion in 2023 and $13.93 billion by 2033, emphasizing the significance of reliable and efficient diagnostic tools across healthcare settings.

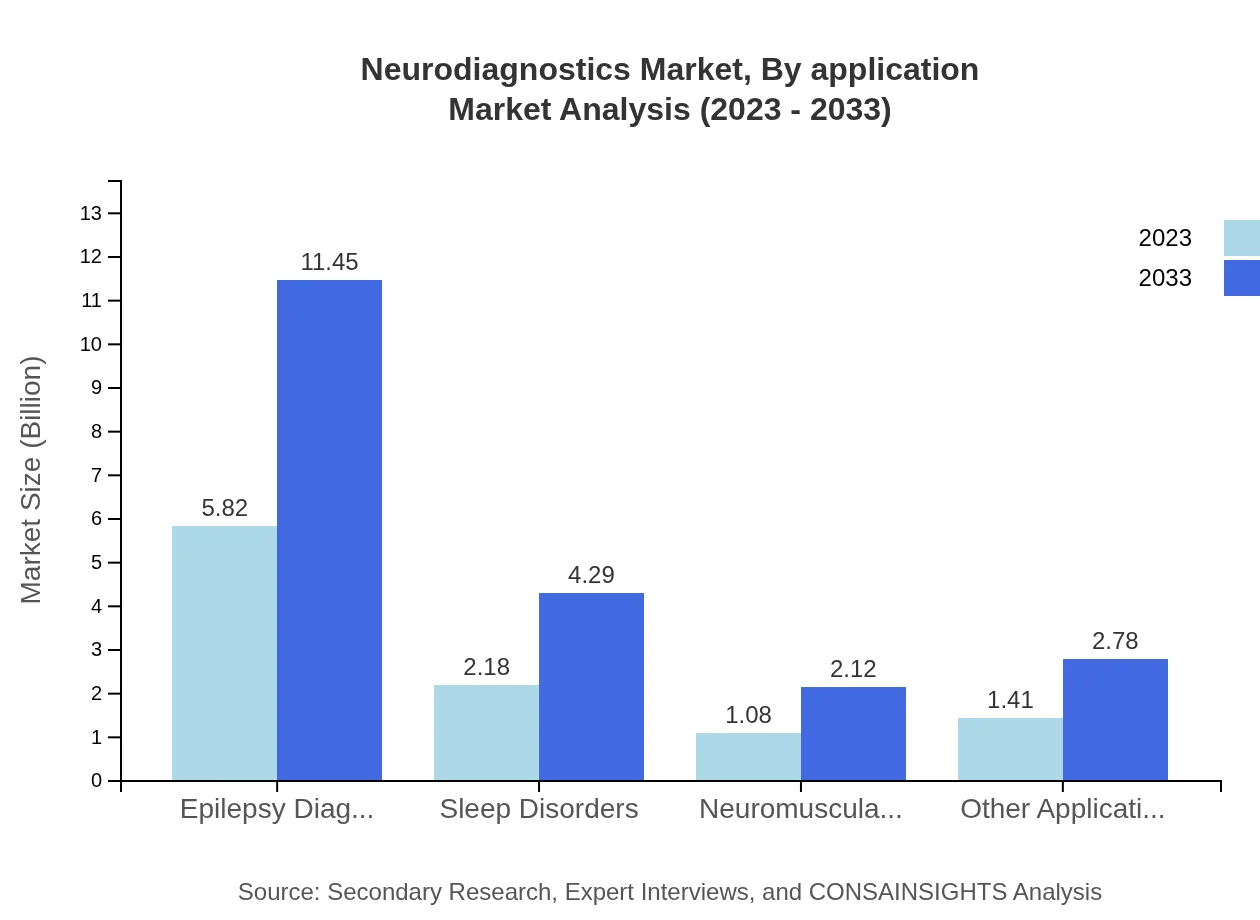

Neurodiagnostics Market Analysis By Application

Application-wise, the Neurodiagnostics market is heavily centered around epilepsy diagnosis, contributing significantly to market size. In 2023, epilepsy diagnosis accounted for $5.82 billion, projected to increase to $11.45 billion by 2033, representing a substantial 55.46% share. Other applications, such as sleep disorders ($2.18 billion to $4.29 billion), neuromuscular disorders ($1.08 billion to $2.12 billion), and additional applications ($1.41 billion to $2.78 billion) indicate that a diverse range of neurological conditions is driving demand for diagnostic solutions.

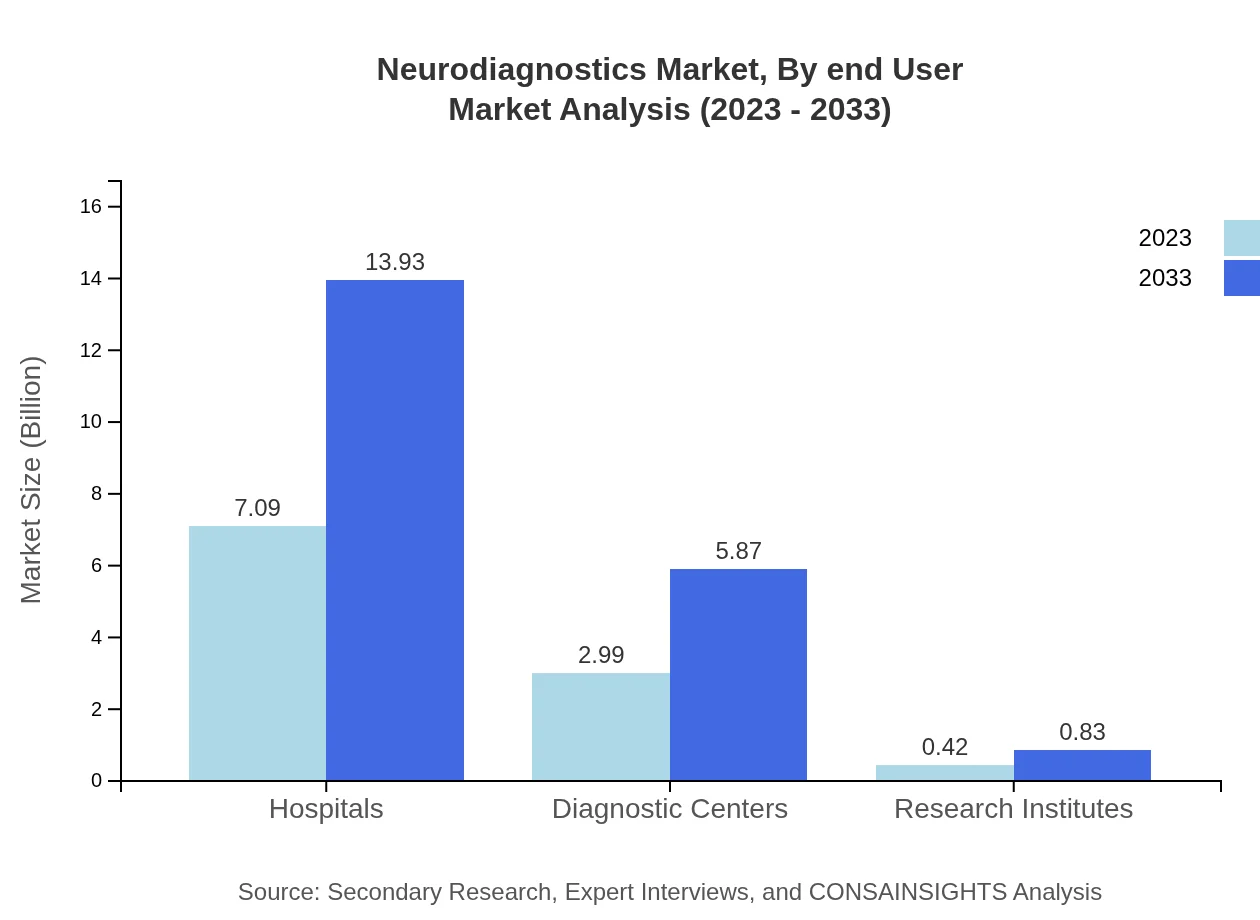

Neurodiagnostics Market Analysis By End User

The market segmentation by end-users includes hospitals, diagnostic centers, and research institutes. Hospitals dominate by contributing $7.09 billion in 2023, forecasted to reach $13.93 billion by 2033, capturing a 67.51% market share. Diagnostic centers and research institutes, though smaller in comparison, exhibit significant growth potential as awareness and utilization of neurodiagnostic services grow, marking $2.99 billion to $5.87 billion and $0.42 billion to $0.83 billion, respectively.

Neurodiagnostics Market Analysis By Region

The Neurodiagnostics market can be further segmented by technology. Traditional technologies utilize time-tested methods that dominate the market, with a size of $9.22 billion in 2023 expected to rise to $18.12 billion by 2033, representing sustained market strength. Advanced technologies, representing innovative solutions, also capture a small yet growing segment, expanding from $1.28 billion in 2023 to $2.52 billion by 2033. This highlights an industry shift towards technological advancements and improved diagnostic capabilities.

Neurodiagnostics Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Neurodiagnostics Industry

Medtronic :

Medtronic is a leading medical device company that offers a wide range of neurodiagnostic solutions, including advanced neurostimulation devices aimed at treating neurological disorders.Philips Healthcare:

Philips Healthcare specializes in diagnostic imaging systems and neurology-related solutions, significantly contributing to the neurodiagnostics market with innovative products.Natus Medical:

Natus Medical focuses on newborn care, neurology, and sleep diagnostics, providing essential neurodiagnostic equipment to ensure comprehensive patient care.GE Healthcare:

GE Healthcare provides advanced imaging technologies and solutions for neurological diagnostics, enhancing diagnostic accuracy and supporting strategic healthcare decisions.Siemens Healthineers:

Siemens Healthineers develops innovations in imaging and diagnostics, significantly contributing to the advancements in the Neurodiagnostics market.We're grateful to work with incredible clients.

FAQs

What is the market size of neurodiagnostics?

The neurodiagnostics market is currently valued at approximately $10.5 billion in 2023 and is projected to grow at a CAGR of 6.8%, reaching significant growth by 2033.

What are the key market players or companies in the neurodiagnostics industry?

Key players in the neurodiagnostics market include major companies such as Siemens Healthineers, Philips, GE Healthcare, and Medtronic, all contributing to technological advancements and product offerings in this sector.

What are the primary factors driving the growth in the neurodiagnostics industry?

The growth of the neurodiagnostics industry is driven by an increase in neurological disorders, advancements in diagnostic technologies, a growing geriatric population, and rising awareness of mental health.

Which region is the fastest Growing in the neurodiagnostics?

Europe is currently the fastest-growing region in the neurodiagnostics market, expected to expand from $3.43 billion in 2023 to $6.74 billion by 2033, highlighting significant growth opportunities.

Does ConsaInsights provide customized market report data for the neurodiagnostics industry?

Yes, ConsaInsights offers customized market report data tailored to the specific needs of clients in the neurodiagnostics industry, providing insights and analyses as per client requirements.

What deliverables can I expect from this neurodiagnostics market research project?

Deliverables from the neurodiagnostics market research project typically include comprehensive market reports, trend analysis, competitive landscape evaluations, and actionable insights focused on growth opportunities.

What are the market trends of neurodiagnostics?

Current trends in neurodiagnostics include the integration of AI in diagnostics, a shift towards personalized medicine, and increased demand for portable devices, enhancing efficiency and accessibility in healthcare.