Non Hodgkin Lymphoma Diagnostics Market Report

Published Date: 31 January 2026 | Report Code: non-hodgkin-lymphoma-diagnostics

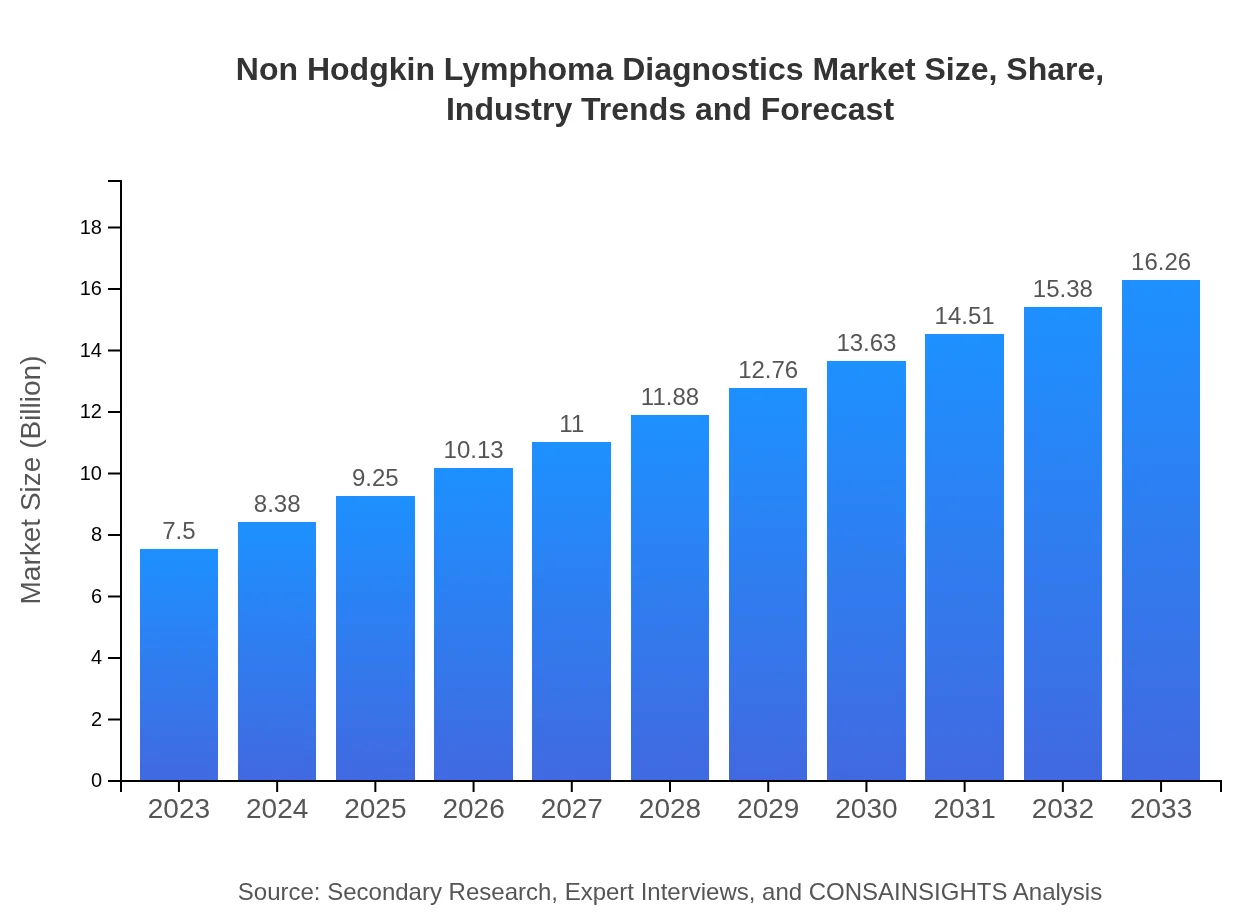

Non Hodgkin Lymphoma Diagnostics Market Size, Share, Industry Trends and Forecast to 2033

This report provides a comprehensive analysis of the Non Hodgkin Lymphoma diagnostics market from 2023 to 2033, highlighting market size, trends, technological advancements, and regional insights to guide stakeholders in strategic decision-making.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $7.50 Billion |

| CAGR (2023-2033) | 7.8% |

| 2033 Market Size | $16.26 Billion |

| Top Companies | Roche Diagnostics, Abbott Laboratories, Siemens Healthineers, Thermo Fisher Scientific, GE Healthcare |

| Last Modified Date | 31 January 2026 |

Non Hodgkin Lymphoma Diagnostics Market Overview

Customize Non Hodgkin Lymphoma Diagnostics Market Report market research report

- ✔ Get in-depth analysis of Non Hodgkin Lymphoma Diagnostics market size, growth, and forecasts.

- ✔ Understand Non Hodgkin Lymphoma Diagnostics's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Non Hodgkin Lymphoma Diagnostics

What is the Market Size & CAGR of Non Hodgkin Lymphoma Diagnostics market in 2033?

Non Hodgkin Lymphoma Diagnostics Industry Analysis

Non Hodgkin Lymphoma Diagnostics Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Non Hodgkin Lymphoma Diagnostics Market Analysis Report by Region

Europe Non Hodgkin Lymphoma Diagnostics Market Report:

Europe's market is expected to expand from $2.49 billion in 2023 to $5.40 billion by 2033, supported by extensive research efforts, heightened disease awareness, and a strong regulatory framework for novel diagnostics.Asia Pacific Non Hodgkin Lymphoma Diagnostics Market Report:

In the Asia-Pacific region, the Non Hodgkin Lymphoma diagnostics market is expected to grow from $1.25 billion in 2023 to $2.72 billion by 2033, driven by increasing adoption of advanced diagnostic techniques and rising NHL prevalence. Economic growth and enhanced healthcare infrastructure play pivotal roles in expanding market access.North America Non Hodgkin Lymphoma Diagnostics Market Report:

North America holds the largest share of the market, projected to increase from $2.64 billion in 2023 to $5.72 billion by 2033. Factors such as advanced healthcare systems, increased awareness, and higher treatment costs contribute to this robust growth.South America Non Hodgkin Lymphoma Diagnostics Market Report:

The South American market is anticipated to grow from $0.54 billion in 2023 to $1.17 billion in 2033, as the demand for improved healthcare services rises. The growing focus on cancer awareness and early diagnosis is fostering market growth.Middle East & Africa Non Hodgkin Lymphoma Diagnostics Market Report:

In the Middle East and Africa, the market is set to grow from $0.58 billion in 2023 to $1.25 billion by 2033, driven by improvements in healthcare access and increasing investments in oncology diagnostics.Tell us your focus area and get a customized research report.

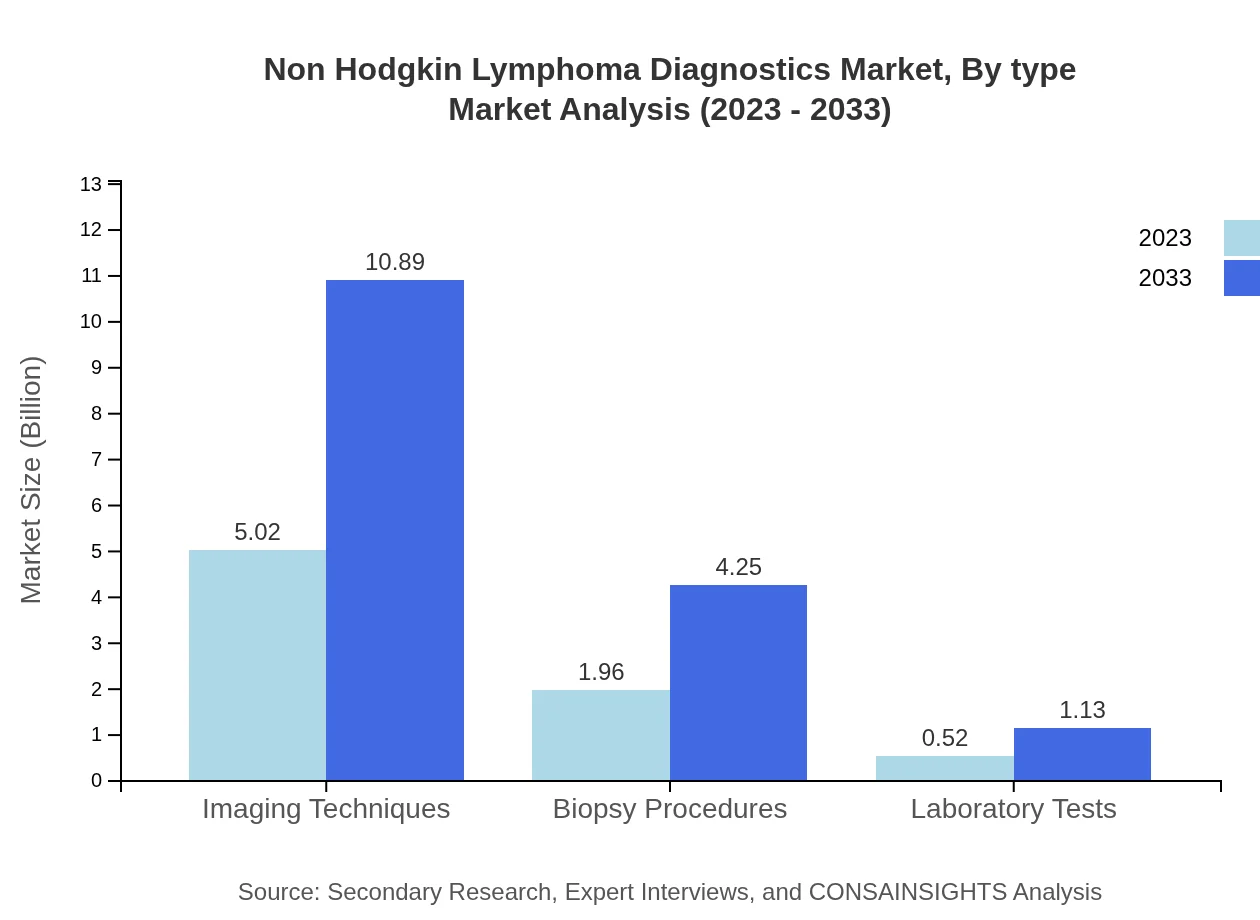

Non Hodgkin Lymphoma Diagnostics Market Analysis By Type

The Non Hodgkin Lymphoma Diagnostics market by type includes Imaging Techniques, Biopsy Procedures, and Laboratory Tests. Imaging Techniques dominate the market, representing $5.02 billion in 2023, forecasted to increase to $10.89 billion by 2033. Biopsy Procedures account for $1.96 billion in 2023, rising to $4.25 billion, while Laboratory Tests contribute $0.52 billion, projected to reach $1.13 billion by 2033.

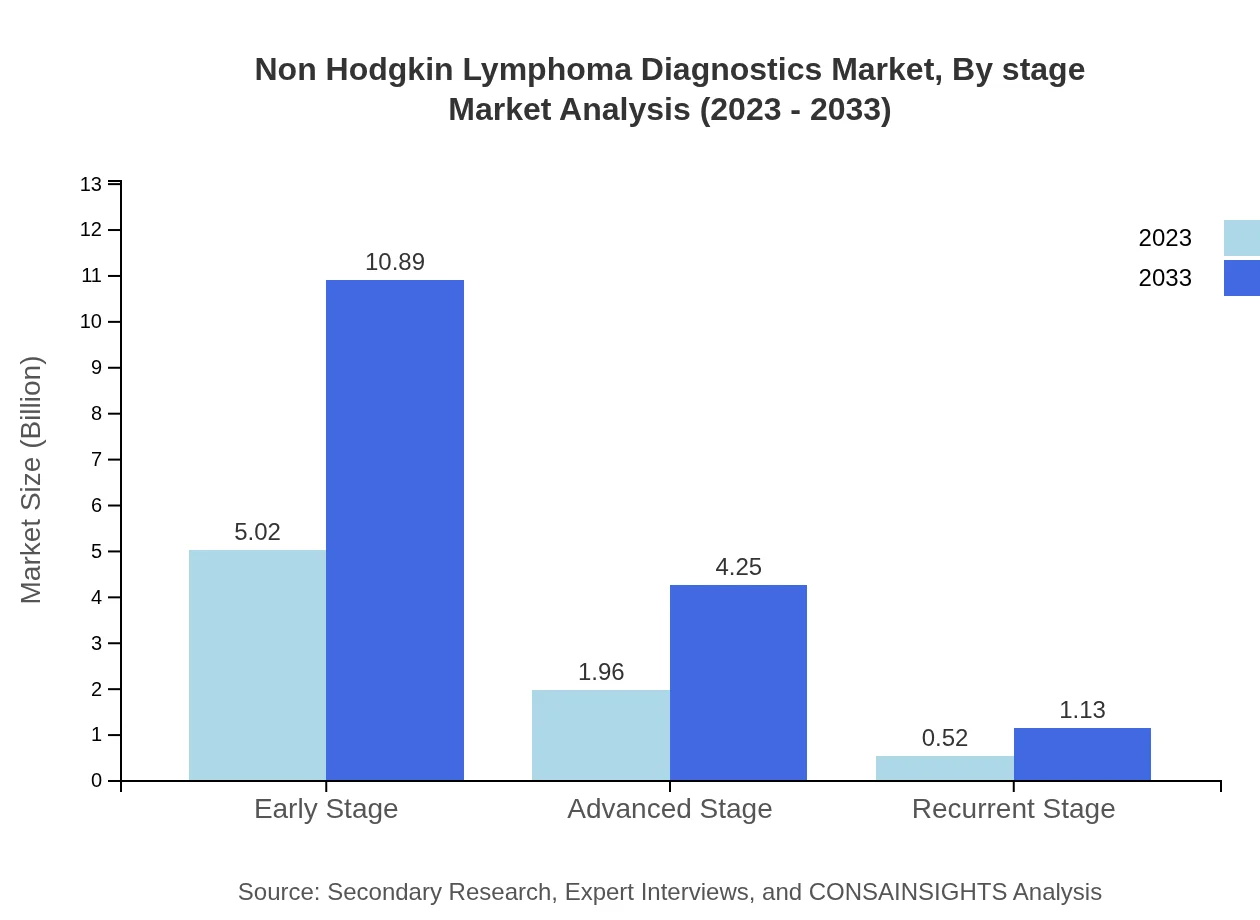

Non Hodgkin Lymphoma Diagnostics Market Analysis By Stage

The market is segmented by Disease Stage into Early Stage, Advanced Stage, and Recurrent Stage diagnostics. Early Stage diagnostics lead the segment, valued at $5.02 billion in 2023, escalating to $10.89 billion by 2033. Advanced and Recurrent Stage diagnostics represent $1.96 billion and $0.52 billion respectively in 2023, with projections of $4.25 billion and $1.13 billion by 2033.

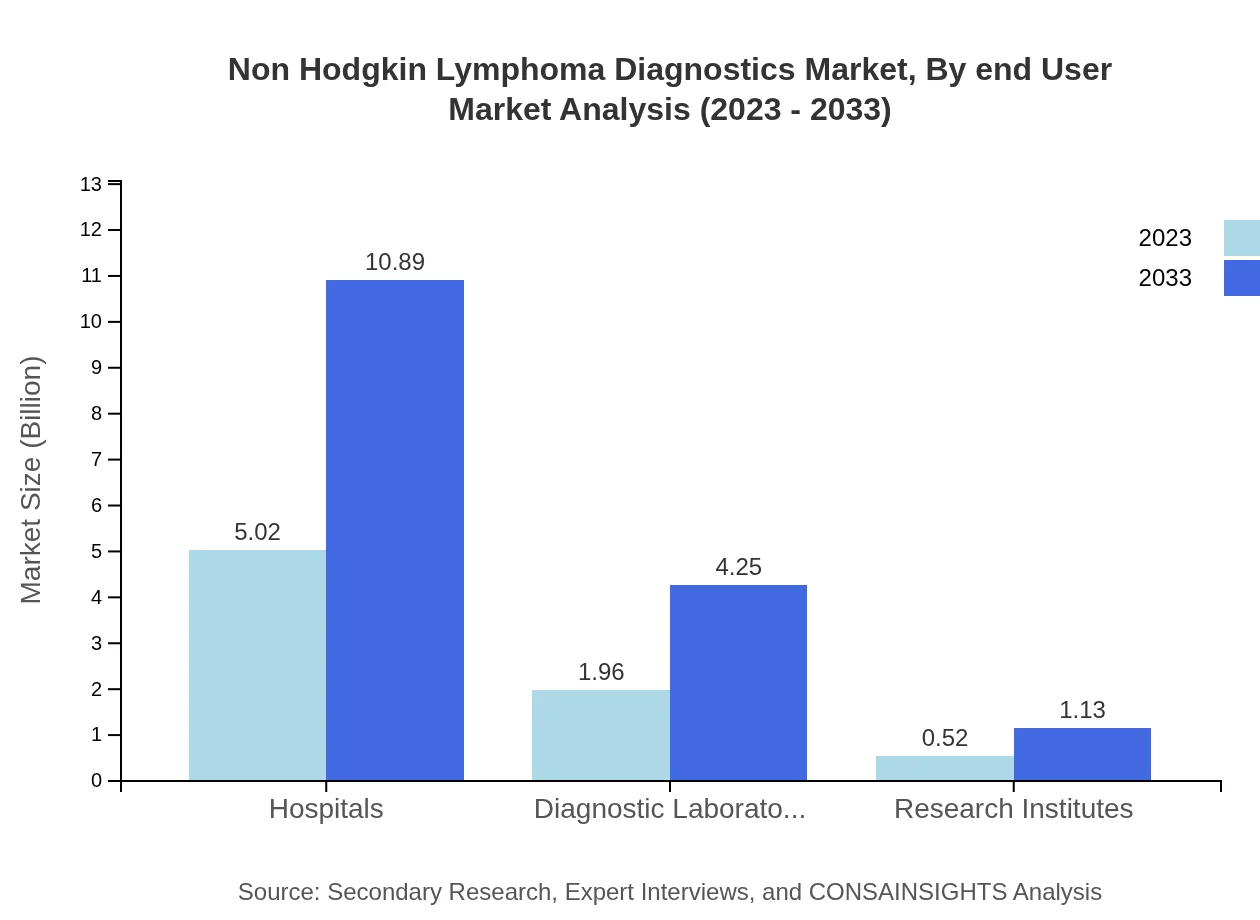

Non Hodgkin Lymphoma Diagnostics Market Analysis By End User

The end-user segment includes Hospitals, Diagnostic Laboratories, and Research Institutes. Hospitals hold the largest market share at $5.02 billion in 2023, increasing to $10.89 billion by 2033. Diagnostic Laboratories are valued at $1.96 billion, projected to grow to $4.25 billion, while Research Institutes contribute $0.52 billion, expected to reach $1.13 billion.

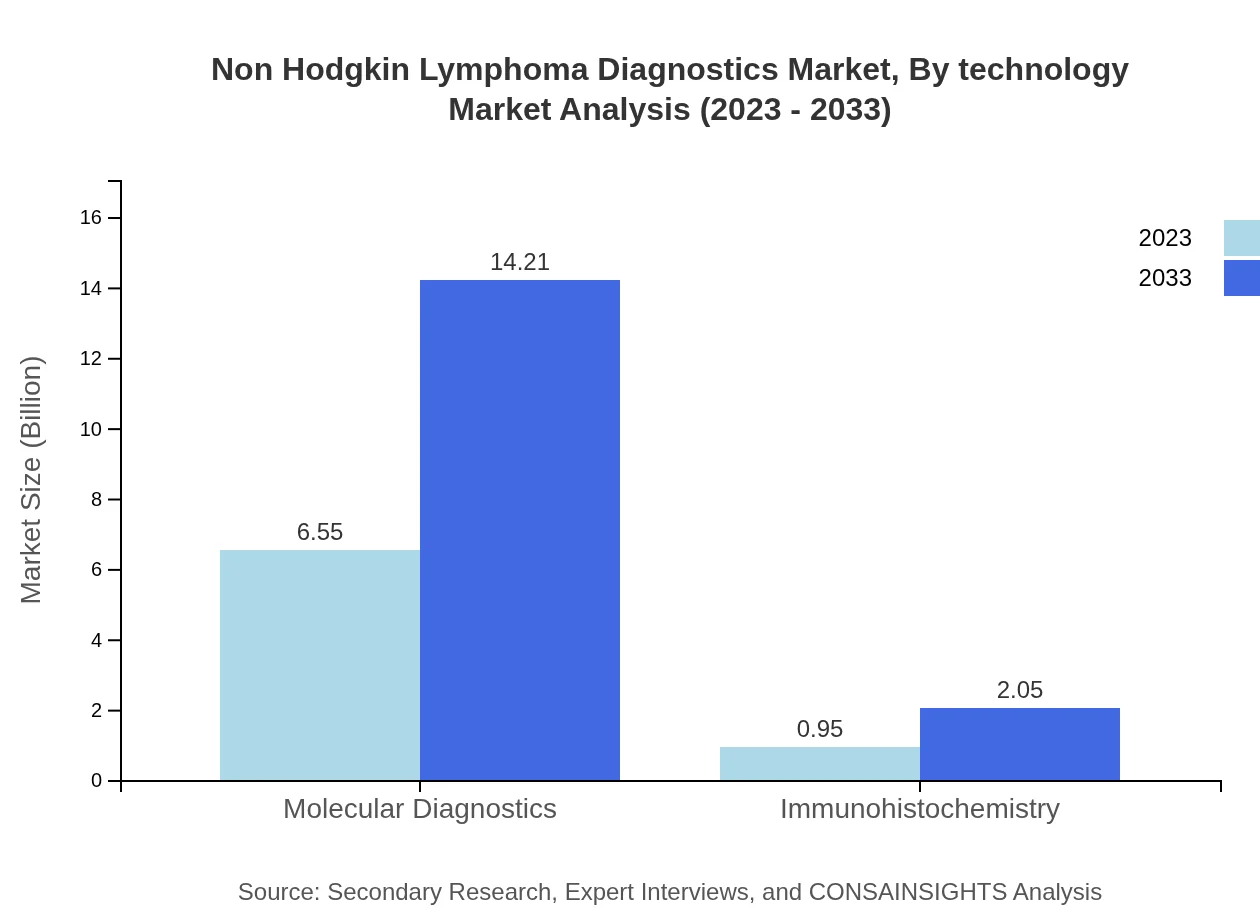

Non Hodgkin Lymphoma Diagnostics Market Analysis By Technology

Innovations in technology significantly influence the market, particularly in Molecular Diagnostics and Imaging Techniques. Molecular Diagnostics, valued at $6.55 billion in 2023, is forecasted to reach $14.21 billion by 2033, while Imaging Techniques, currently valued at $5.02 billion, is expected to grow in line with advancements in imaging technologies.

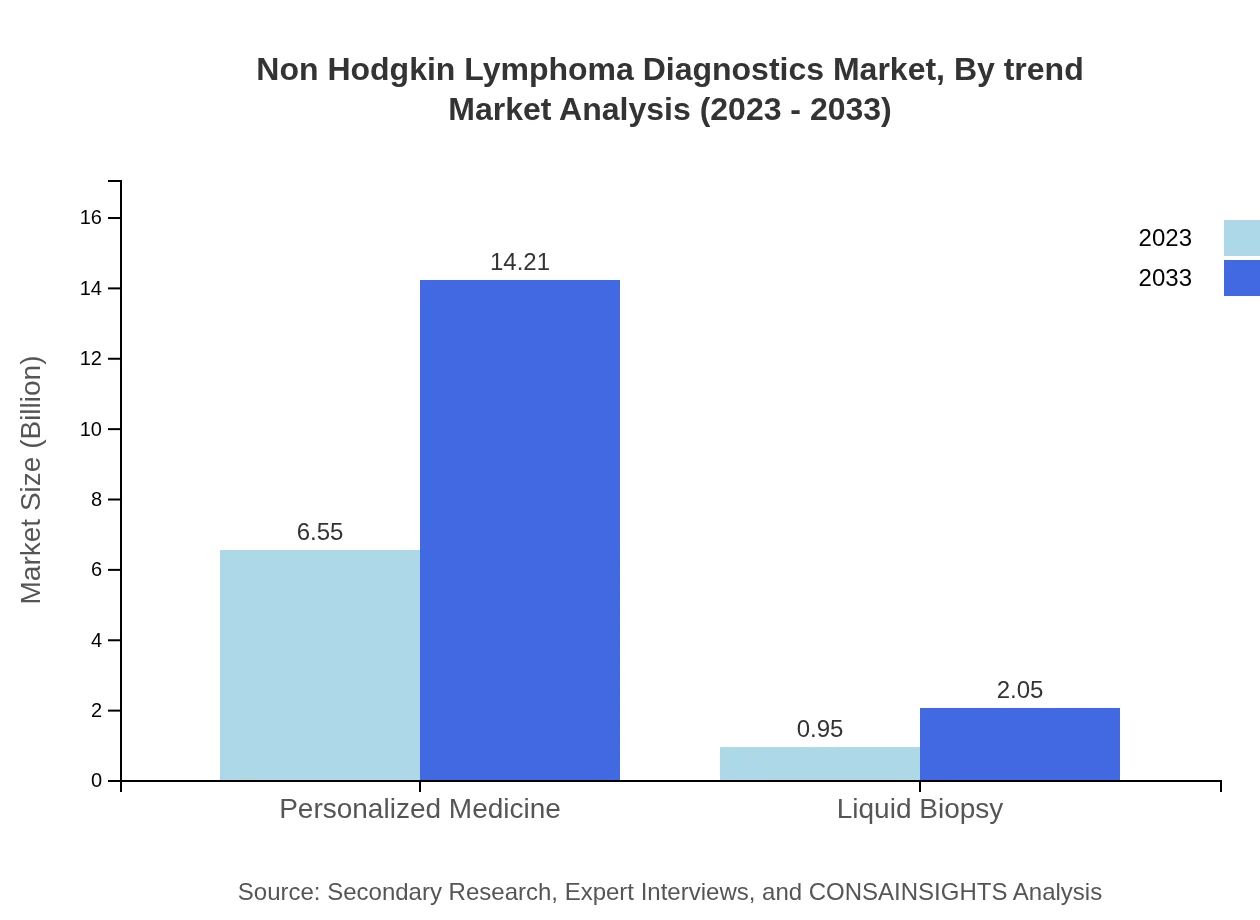

Non Hodgkin Lymphoma Diagnostics Market Analysis By Trend

Current trends in the Non Hodgkin Lymphoma diagnostics market include a shift towards personalized medicine, heightened investment in R&D for diagnostic tools, and integration of artificial intelligence for improved diagnostic accuracy. This trend is expected to bolster market growth significantly by 2033.

Non Hodgkin Lymphoma Diagnostics Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Non Hodgkin Lymphoma Diagnostics Industry

Roche Diagnostics:

A leader in molecular diagnostics, Roche focuses on advanced diagnostic solutions, enhancing the availability and effectiveness of NHL diagnostics through innovative technologies.Abbott Laboratories:

Abbott specializes in laboratory tests and imaging technologies, providing comprehensive diagnostic solutions targeting Non Hodgkin Lymphoma and facilitating early detection.Siemens Healthineers:

Siemens develops cutting-edge imaging technologies, crucial for Non Hodgkin Lymphoma diagnostics, ensuring precise imaging that aids in thorough disease understanding.Thermo Fisher Scientific:

Thermo Fisher is instrumental in providing laboratory tests and molecular diagnostics, driving advancements in the detection and monitoring of NHL.GE Healthcare:

With a focus on imaging and patient monitoring technologies, GE Healthcare contributes to the NHL diagnostics landscape through detailed imaging capabilities.We're grateful to work with incredible clients.

FAQs

What is the market size of Non-Hodgkin Lymphoma Diagnostics?

The Non-Hodgkin Lymphoma Diagnostics market is valued at approximately $7.5 billion in 2023, with a strong compound annual growth rate (CAGR) of 7.8% projected through 2033.

What are the key market players or companies in the Non-Hodgkin Lymphoma Diagnostics industry?

Key players in the Non-Hodgkin Lymphoma Diagnostics market include established diagnostic laboratories, biotechnology firms, and pharmaceutical companies that specialize in lymphoma treatment and research. These entities continuously innovate to improve diagnostic capabilities.

What are the primary factors driving the growth in the Non-Hodgkin Lymphoma Diagnostics industry?

Growth drivers include increasing lymphoma incidence rates, advancements in imaging and molecular diagnostic technologies, growing awareness and funding for cancer research, and the demand for personalized medicine solutions catered to specific patient needs.

Which region is the fastest Growing in the Non-Hodgkin Lymphoma Diagnostics?

The Asia Pacific region showcases the fastest growth potential in the Non-Hodgkin Lymphoma Diagnostics market, expected to expand from $1.25 billion in 2023 to $2.72 billion by 2033, indicating significant market opportunities.

Does ConsaInsights provide customized market report data for the Non-Hodgkin Lymphoma Diagnostics industry?

Yes, ConsaInsights offers tailored market report data for the Non-Hodgkin Lymphoma Diagnostics sector, allowing stakeholders to obtain specific insights and analysis that align with their unique business objectives.

What deliverables can I expect from this Non-Hodgkin Lymphoma Diagnostics market research project?

Expect comprehensive market analysis reports, including segmentation insights, competitive landscape assessments, growth forecasts, and region-specific data tailored to your research needs in the Non-Hodgkin Lymphoma Diagnostics market.

What are the market trends of Non-Hodgkin Lymphoma Diagnostics?

Current trends include the rising adoption of imaging techniques contributing 66.96% market share, advancements in molecular diagnostics leading the market, and growth in personalized medicine practices, reflecting shifts towards targeted therapeutic approaches.