Reports >

Chemicals And Materials

>

Polyphenylene Market Report

Polyphenylene Market Report

Published Date: 02 February 2026 | Report Code: polyphenylene

Polyphenylene Market Size, Share, Industry Trends and Forecast to 2033

This report offers a comprehensive analysis of the Polyphenylene market from 2023 to 2033, detailing key trends, market size, segmentation, and regional insights. It aims to provide stakeholders with valuable data for strategic planning and investment decisions.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

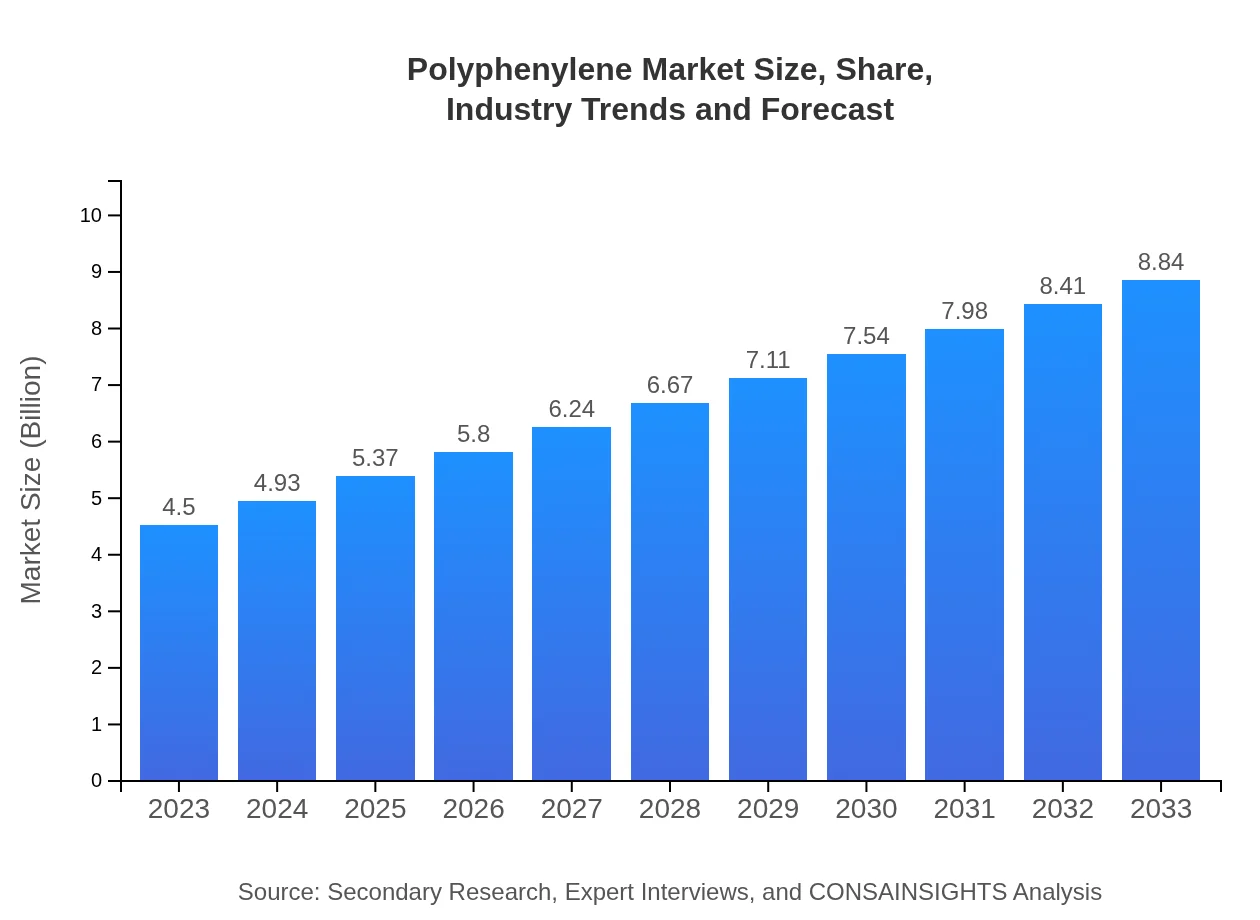

| 2023 Market Size | $4.50 Billion |

| CAGR (2023-2033) | 6.8% |

| 2033 Market Size | $8.84 Billion |

| Top Companies | Solvay, BASF, Kraton Corporation, Sabic |

| Last Modified Date | 02 February 2026 |

Polyphenylene Market Overview

Customize Polyphenylene Market Report market research report

- ✔ Get in-depth analysis of Polyphenylene market size, growth, and forecasts.

- ✔ Understand Polyphenylene's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Polyphenylene

What is the Market Size & CAGR of Polyphenylene market in 2023?

Polyphenylene Industry Analysis

Polyphenylene Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Polyphenylene Market Analysis Report by Region

Europe Polyphenylene Market Report:

Europe's market for Polyphenylene is estimated at $1.41 billion in 2023, growing to $2.77 billion by 2033. Increased environmental regulations and a significant focus on sustainability practices are driving innovations and investments in this region.Asia Pacific Polyphenylene Market Report:

The Asia Pacific region held a market size of $0.78 billion in 2023, projected to grow to $1.53 billion by 2033, driven by rapid industrialization and growing automotive sectors in countries like China and India. Increased investments in research and development for high-performance materials are further fueling this growth.North America Polyphenylene Market Report:

North America, with a market size of $1.67 billion in 2023, is forecasted to reach $3.28 billion by 2033. The region is bolstered by technological advancements and robust research activities in plastics, especially in high-performance applications in automotive and aerospace.South America Polyphenylene Market Report:

In South America, the Polyphenylene market is expected to grow from $0.16 billion in 2023 to $0.31 billion by 2033. This growth is attributed to rising infrastructure development and increased demand in automotive and electronics sectors, despite slower economic recovery compared to other regions.Middle East & Africa Polyphenylene Market Report:

The Middle East and Africa region is projected to grow from $0.48 billion in 2023 to $0.95 billion by 2033, aided by developing industrial sectors and increasing investments in high-performance material technologies.Tell us your focus area and get a customized research report.

Polyphenylene Market Analysis By Type

The Polyphenylene market is mainly dominated by Polyphenylene Dioxide (PPD), which is anticipated to grow from $2.83 billion in 2023 to $5.56 billion by 2033, capturing a market share of 62.84%. Polyphenylene Hydride (PPH) follows, with a growth from $1.30 billion to $2.56 billion, holding 28.99% of the market share, while Polyphenylene Sulfide (PPS) is expected to grow from $0.37 billion to $0.72 billion, constituting 8.17%.

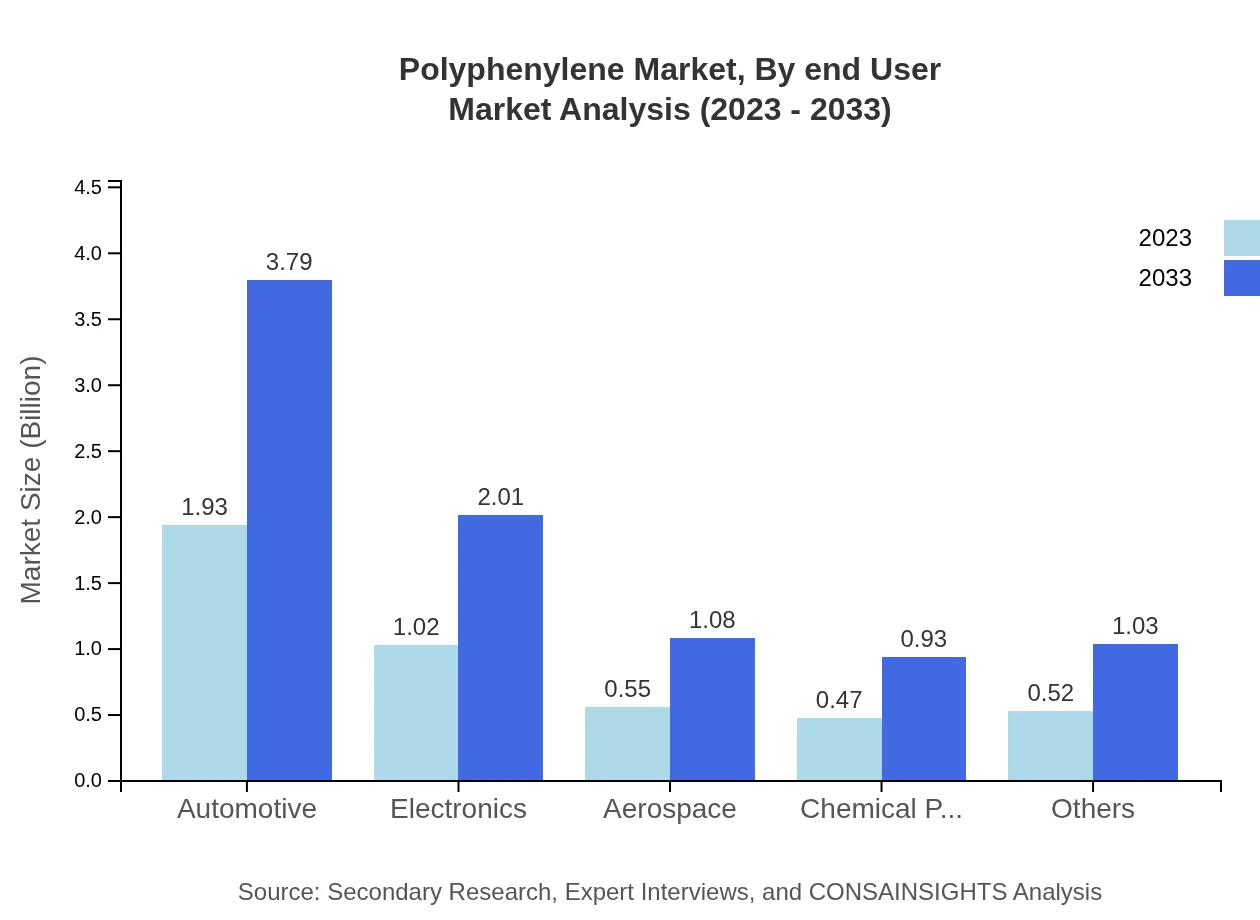

Polyphenylene Market Analysis By End User

The automotive sector is a primary end-user, dominating the market with a size of $1.93 billion in 2023, projected to expand to $3.79 billion, comprising 42.9% of the share. The electronics sector represents $1.02 billion, with an expected rise to $2.01 billion, accounting for 22.71%. Additionally, aerospace and chemical processing represent significant contributions with respective shares of 10.48% and 12.25%.

Polyphenylene Market Analysis By Application

Applications of Polyphenylene span across automotive parts, aerospace components, electronics, and films. The automotive segment alone signifies substantial growth, expected to reach $3.79 billion by 2033, representing 42.9% of total application share. High-performance parts and engineering plastics also play critical roles in the market dynamics.

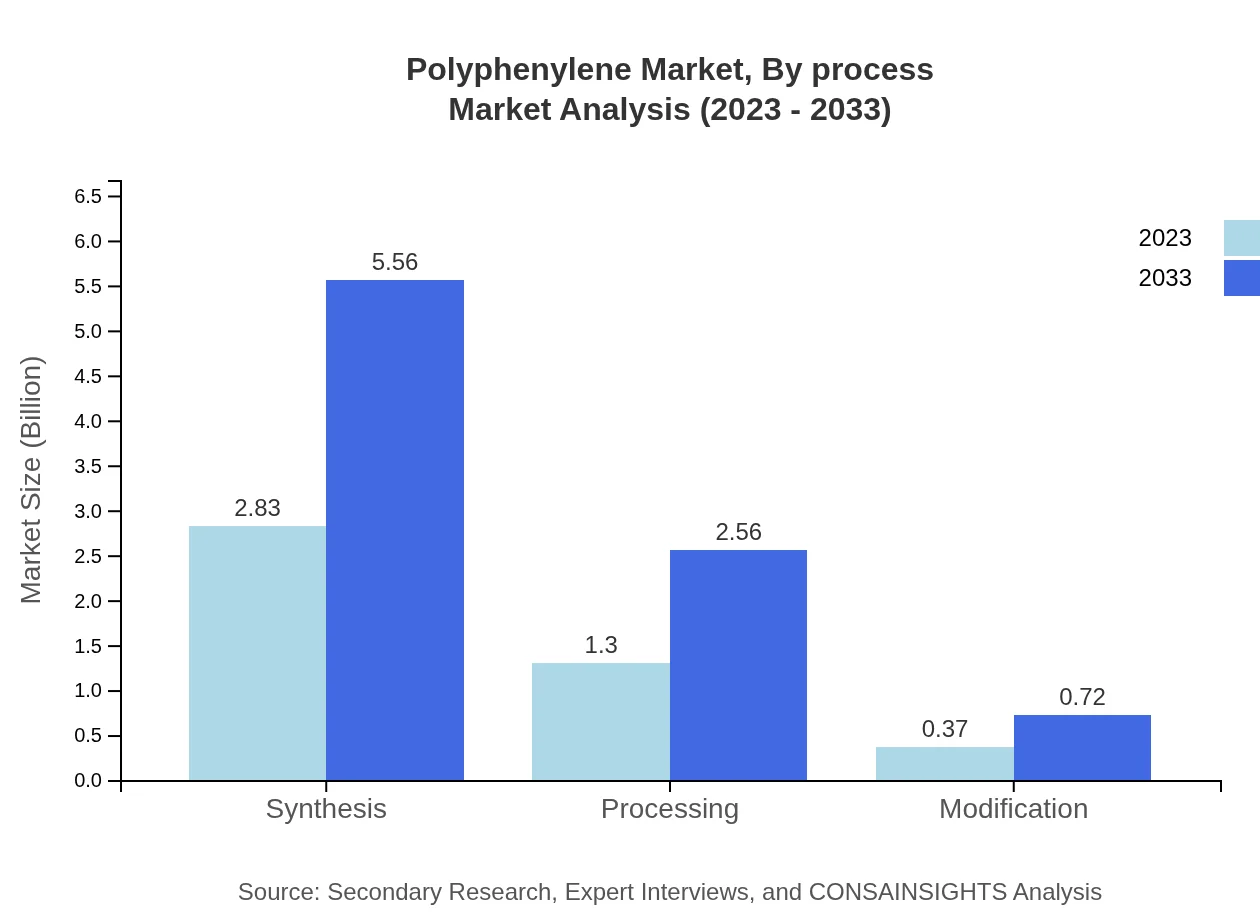

Polyphenylene Market Analysis By Process

The processes include synthesis, processing, and modification, with significant growth in synthesis and processing segments. Synthesis holds a leading share with a market size of $2.83 billion in 2023, expected to grow to $5.56 billion by 2033. Processing reflects robust demand as well, expanding from $1.30 billion to $2.56 billion, showcasing the increasing need for sophisticated Polyphenylene processing techniques.

Polyphenylene Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Polyphenylene Industry

Solvay:

A global leader in advanced materials, Solvay specializes in producing high-performance polymers, including Polyphenylene products. The company significantly emphasizes sustainability and technological advancement.BASF:

BASF is a major player in the chemical industry, known for its comprehensive range of materials, including Polyphenylene variants. The company's focus on innovative material solutions drives growth in multiple end-user markets.Kraton Corporation:

Kraton specializes in sustainable advanced polymers and additives, contributing to the Polyphenylene market through innovative and eco-friendly products.Sabic:

As a diversified global supplier, Sabic offers a variety of Polyphenylene products and is committed to research and development, heavily investing in innovative solutions for high-performance applications.We're grateful to work with incredible clients.

FAQs

What is the market size of polyphenylene?

The polyphenylene market is valued at approximately $4.5 billion in 2023, with a projected growth rate of 6.8% CAGR, forecasted to reach significant dimensions by 2033.

What are the key market players or companies in this polyphenylene industry?

Key players in the polyphenylene market include leading chemical manufacturers and polymers producers, though specific names weren't captured, they play vital roles in driving innovation and supply.

What are the primary factors driving the growth in the polyphenylene industry?

Key growth drivers for the polyphenylene market include increasing demand in the automotive and aerospace sectors, advancements in electronics, and the growing need for high-performance materials.

Which region is the fastest Growing in the polyphenylene?

The fastest-growing region for polyphenylene is North America, with its market expected to expand from $1.67 billion in 2023 to $3.28 billion by 2033.

Does ConsaInsights provide customized market report data for the polyphenylene industry?

Yes, ConsaInsights offers tailored market report data for the polyphenylene industry, catering to specific client needs and insights.

What deliverables can I expect from this polyphenylene market research project?

Deliverables include comprehensive reports detailing market size, forecasts, trends, segmentation analysis, key players, and strategic insights.

What are the market trends of polyphenylene?

Current trends in the polyphenylene market include an increasing shift towards sustainable materials, enhanced processing technologies, and the growth of high-performance applications across various industries.