Polyvinyl Butyral Market Report

Published Date: 02 February 2026 | Report Code: polyvinyl-butyral

Polyvinyl Butyral Market Size, Share, Industry Trends and Forecast to 2033

This report provides a comprehensive analysis of the Polyvinyl Butyral market, including insights into market trends, segmentation, and regional dynamics, with forecasts from 2023 to 2033. The intention is to offer stakeholders valuable data to inform decisions and strategies.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

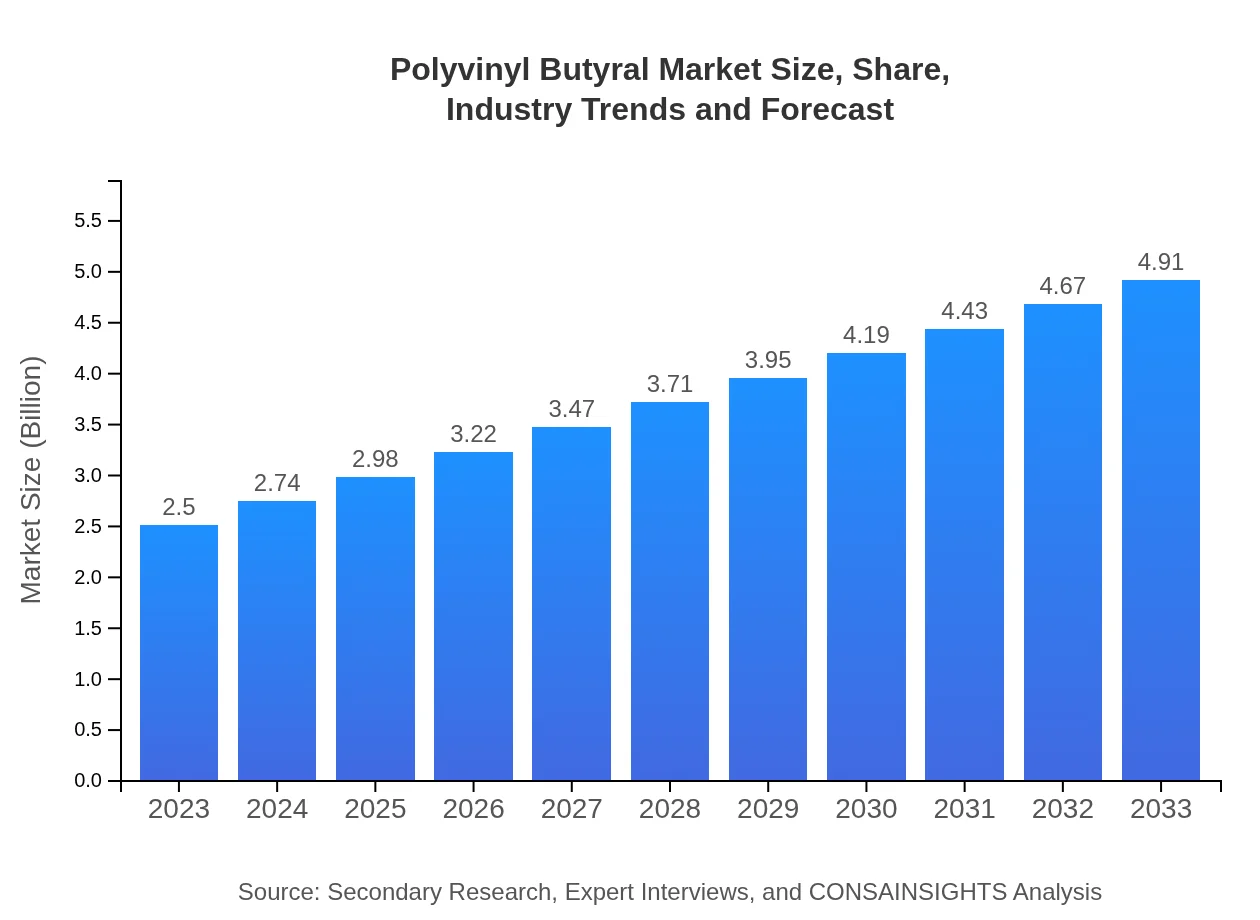

| 2023 Market Size | $2.50 Billion |

| CAGR (2023-2033) | 6.8% |

| 2033 Market Size | $4.91 Billion |

| Top Companies | Eastman Chemical Company, Kuraray Co., Ltd., Sekisui Chemicals |

| Last Modified Date | 02 February 2026 |

Polyvinyl Butyral Market Overview

Customize Polyvinyl Butyral Market Report market research report

- ✔ Get in-depth analysis of Polyvinyl Butyral market size, growth, and forecasts.

- ✔ Understand Polyvinyl Butyral's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Polyvinyl Butyral

What is the Market Size & CAGR of Polyvinyl Butyral market in 2023?

Polyvinyl Butyral Industry Analysis

Polyvinyl Butyral Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Polyvinyl Butyral Market Analysis Report by Region

Europe Polyvinyl Butyral Market Report:

The European market for Polyvinyl Butyral is set to increase from $0.68 billion in 2023 to $1.33 billion by 2033. Factors such as high automotive production levels, particularly in Germany, combined with a strong focus on green building initiatives, are major growth drivers in this region.Asia Pacific Polyvinyl Butyral Market Report:

The Asia Pacific region is anticipated to witness substantial growth in the Polyvinyl Butyral market, increasing from $0.53 billion in 2023 to $1.05 billion by 2033. This growth is driven by rising automotive production and infrastructural developments across countries like China and India, fostering a demand for safety glass.North America Polyvinyl Butyral Market Report:

North America is projected to be a significant market for Polyvinyl Butyral, growing from $0.86 billion in 2023 to $1.69 billion in 2033. The demand is primarily driven by stringent safety regulations in the automotive industry and innovations in glass manufacturing techniques, enhancing product quality.South America Polyvinyl Butyral Market Report:

In South America, the market for Polyvinyl Butyral is expected to grow moderately, with an increase from $0.16 billion in 2023 to $0.32 billion by 2033. The growth can be attributed to increased construction activities and an emerging automotive sector, although market penetration remains limited compared to other regions.Middle East & Africa Polyvinyl Butyral Market Report:

In the Middle East and Africa, the market is expected to grow from $0.26 billion in 2023 to $0.52 billion in 2033. Rapid urbanization and the need for modern construction materials are paramount in driving the demand for PVB, especially in emerging economies.Tell us your focus area and get a customized research report.

Polyvinyl Butyral Market Analysis By Type

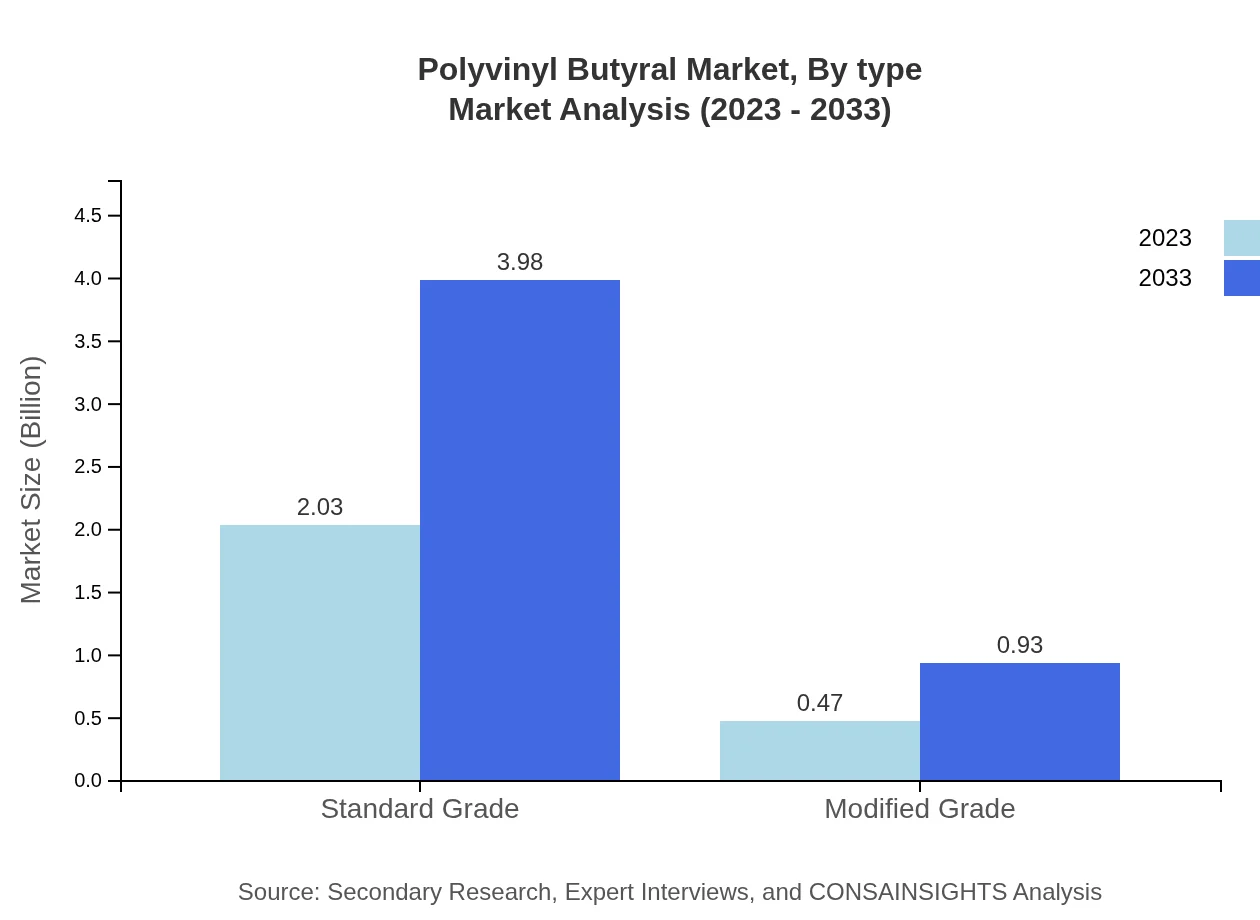

The segmentation of Polyvinyl Butyral by type shows that standard grade PVB dominates the market, expected to grow from $2.03 billion in 2023 to $3.98 billion in 2033, maintaining an 81.05% market share. The modified grade, however, is also gaining ground, projected to rise from $0.47 billion in 2023 to $0.93 billion by 2033, holding 18.95% market share.

Polyvinyl Butyral Market Analysis By Application

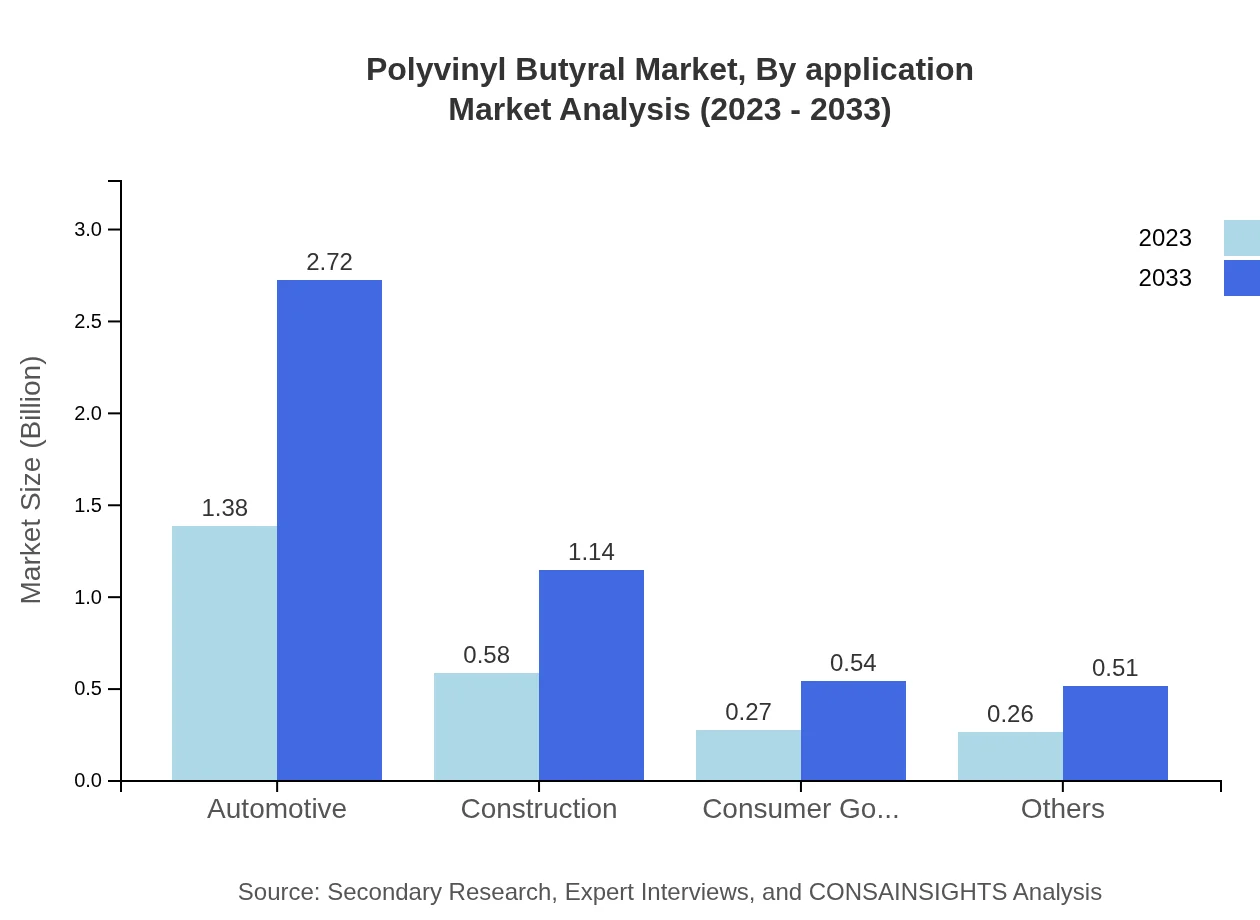

Analyzing the application segment, the automotive industry leads with a market size of $1.38 billion in 2023, expected to reach $2.72 billion in 2033, capturing 55.3% of the total market. The construction industry follows, with forecasts showing growth from $0.58 billion to $1.14 billion, representing a 23.28% share.

Polyvinyl Butyral Market Analysis By End Use Industry

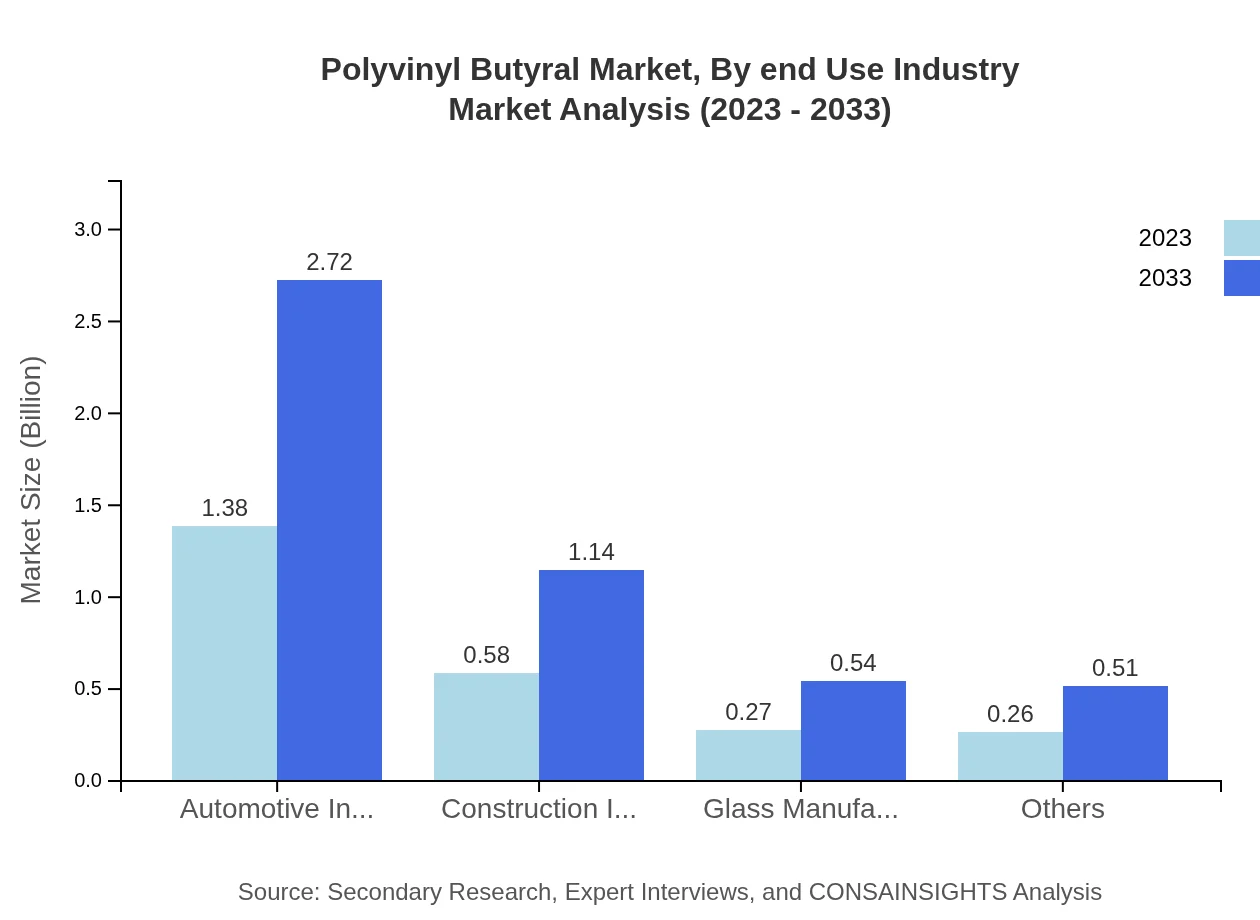

In terms of end-use industries, the automotive sector remains the largest consumer of PVB. Alongside this, the construction industry also accounts for a notable portion due to an increase in glass usage in building facades, which is expected to rise significantly.

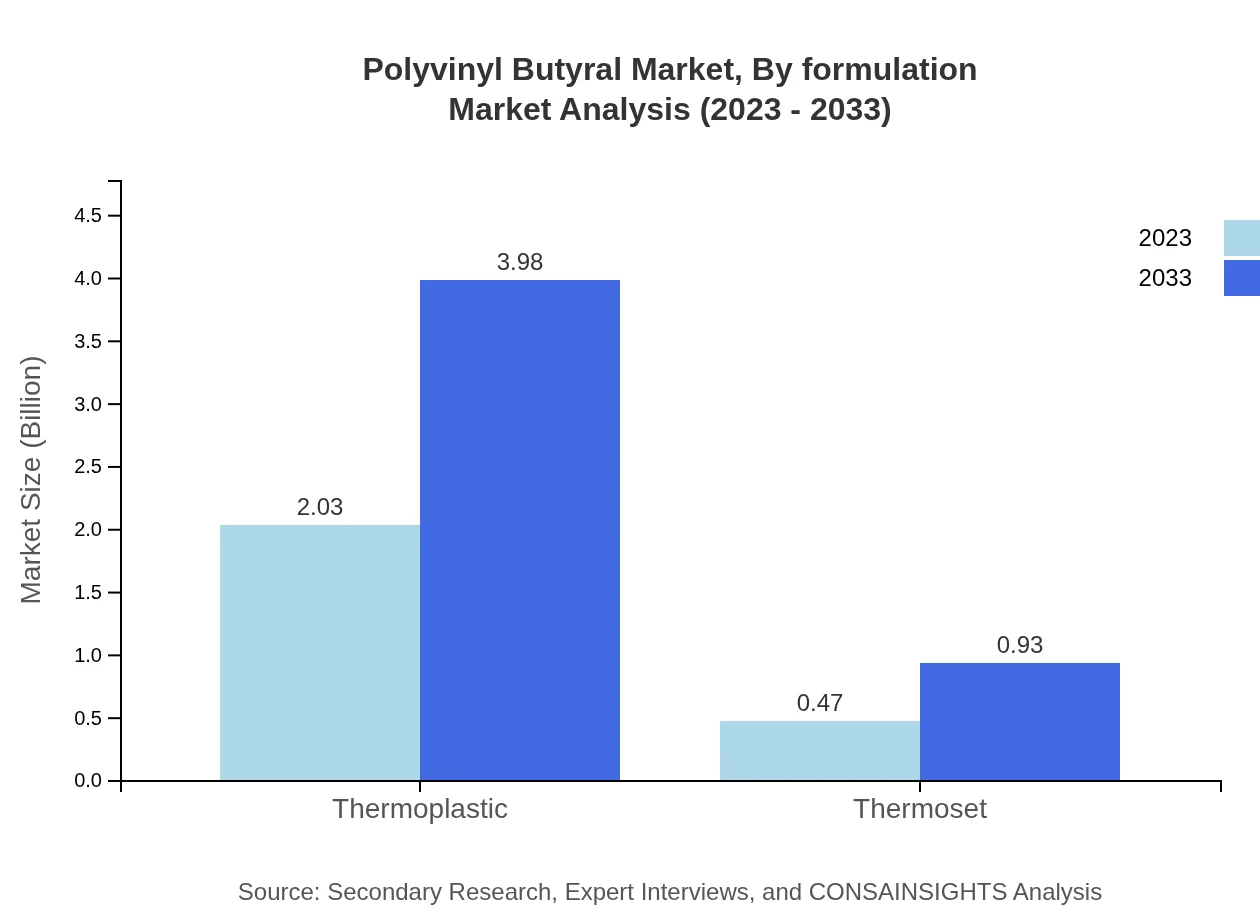

Polyvinyl Butyral Market Analysis By Formulation

PVB is typically available in two main formulations: thermoplastic and thermoset. Thermoplastic formulations currently dominate the market, with a size of $2.03 billion in 2023 against thermoset formulations at $0.47 billion. The thermoplastic segment is expected to experience robust growth from technological advancements.

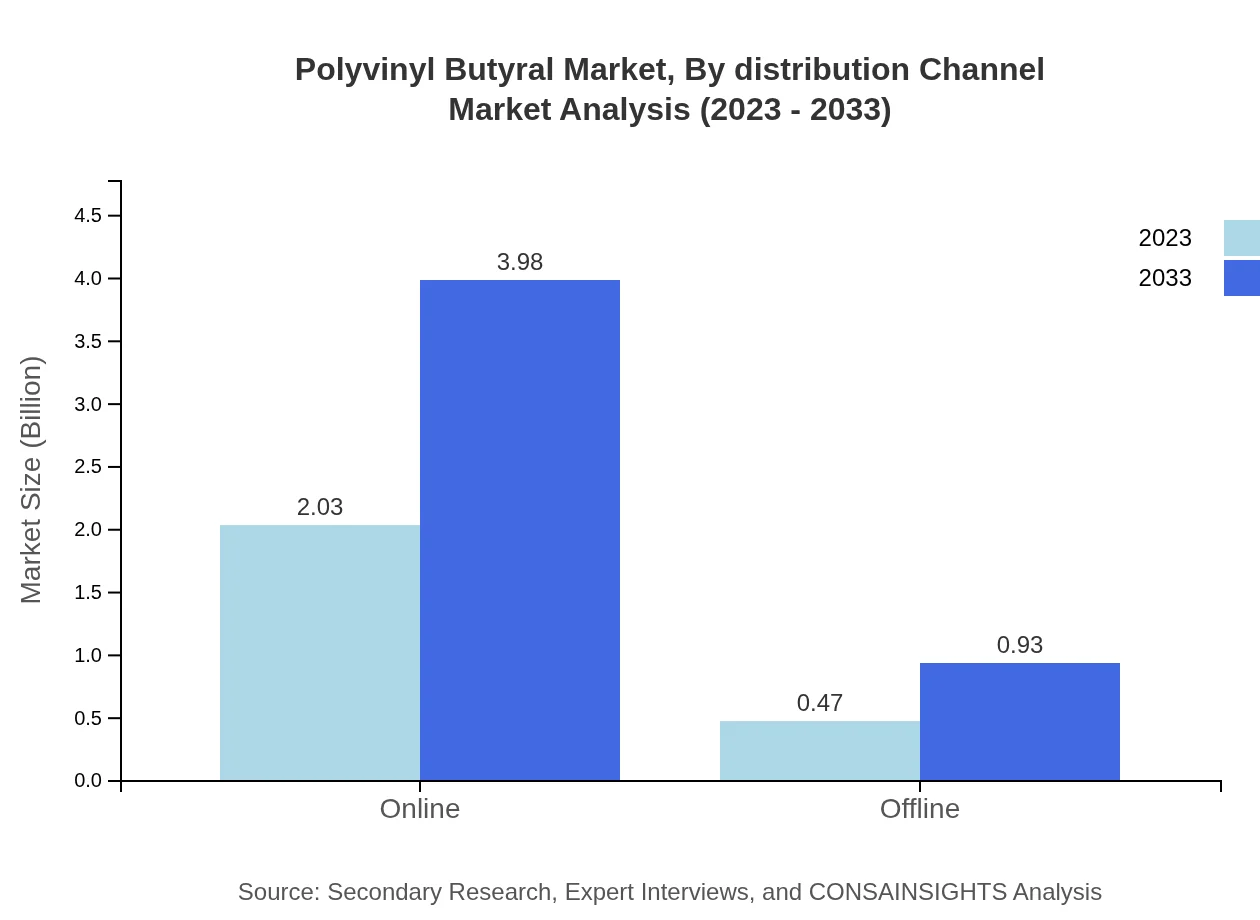

Polyvinyl Butyral Market Analysis By Distribution Channel

The distribution of PVB primarily occurs through online channels, which accounted for 81.05% of the market share, expected to remain dominant through the forecast period. Offline channels also play a significant role, projected to attract more consumers seeking direct purchasing options.

Polyvinyl Butyral Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Polyvinyl Butyral Industry

Eastman Chemical Company:

Eastman leads in PVB production, focusing on quality and innovation in safety glass solutions across automotive and architectural applications.Kuraray Co., Ltd.:

As a premier manufacturer of PVB, Kuraray emphasizes sustainable production methods and advanced engineering solutions to address diverse customer needs.Sekisui Chemicals:

Sekisui offers high-performance PVB products, positioned strongly in the construction and automotive sectors, driven by extensive R&D.We're grateful to work with incredible clients.

FAQs

What is the market size of polyvinyl Butyral?

The global polyvinyl-butyral market is valued at approximately $2.5 billion in 2023 with a projected CAGR of 6.8%, indicating strong growth potential through 2033.

What are the key market players or companies in the polyvinyl Butyral industry?

Key players in the polyvinyl-butyral market include DuPont, Eastman Chemical Company, Sekisui Chemical Co., Ltd., and Kuraray Co., Ltd. These companies lead in production capacity and technological advancements.

What are the primary factors driving the growth in the polyvinyl Butyral industry?

Growth in the polyvinyl-butyral industry is driven by increasing demand in the automotive and construction sectors, along with rising advancements in safety glass applications and innovations in material technology.

Which region is the fastest Growing in the polyvinyl Butyral?

Asia Pacific is the fastest-growing region for polyvinyl-butyral, expected to grow from $0.53 billion in 2023 to approximately $1.05 billion by 2033, fueled primarily by automotive and construction activities.

Does ConsaInsights provide customized market report data for the polyvinyl Butyral industry?

Yes, ConsaInsights offers customized market report data tailored to specific client needs in the polyvinyl-butyral industry, providing detailed insights and regional analysis.

What deliverables can I expect from this polyvinyl Butyral market research project?

Expect comprehensive deliverables including an in-depth report, market sizing forecasts, competitive analysis, regional insights, and actionable recommendations tailored to your business objectives.

What are the market trends of polyvinyl Butyral?

Current market trends in polyvinyl-butyral include a growing focus on sustainability, enhanced product applications in automotive glazing, and increased integration of smart technologies in manufacturing processes.