Power Semiconductor Market Report

Published Date: 31 January 2026 | Report Code: power-semiconductor

Power Semiconductor Market Size, Share, Industry Trends and Forecast to 2033

This report presents a comprehensive analysis of the Power Semiconductor market from 2023 to 2033. It covers market size estimates, CAGR, regional insights, industry trends, and key players, offering readers valuable data for strategic decision-making.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

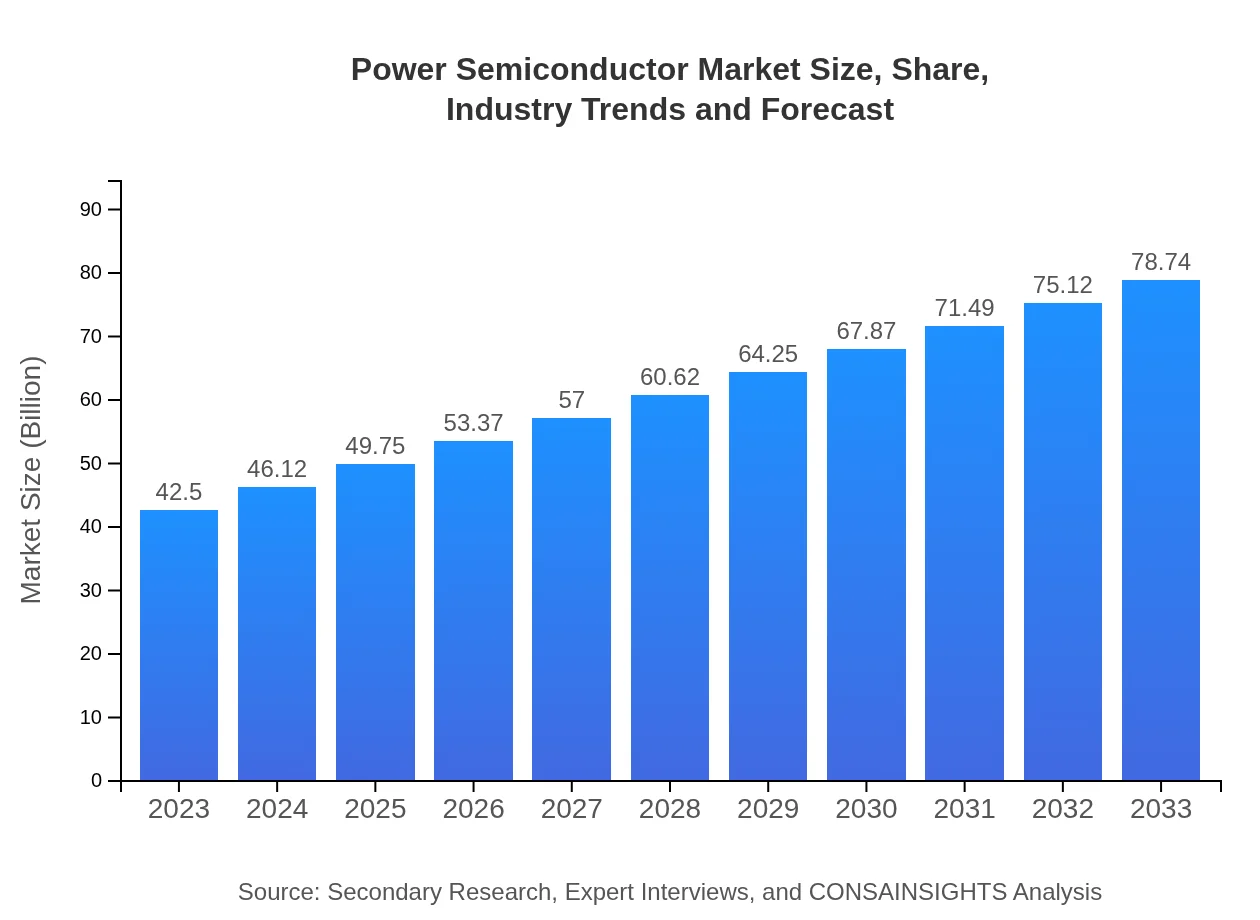

| 2023 Market Size | $42.50 Billion |

| CAGR (2023-2033) | 6.2% |

| 2033 Market Size | $78.74 Billion |

| Top Companies | Infineon Technologies, Texas Instruments, STMicroelectronics, NXP Semiconductors, ON Semiconductor |

| Last Modified Date | 31 January 2026 |

Power Semiconductor Market Overview

Customize Power Semiconductor Market Report market research report

- ✔ Get in-depth analysis of Power Semiconductor market size, growth, and forecasts.

- ✔ Understand Power Semiconductor's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Power Semiconductor

What is the Market Size & CAGR of Power Semiconductor market in 2023?

Power Semiconductor Industry Analysis

Power Semiconductor Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Power Semiconductor Market Analysis Report by Region

Europe Power Semiconductor Market Report:

The European Power Semiconductor market is expected to expand from $12.24 billion in 2023 to $22.68 billion by 2033. Regulatory measures and initiatives towards sustainable energy are driving investments in efficient technologies, particularly in automotive and industrial sectors.Asia Pacific Power Semiconductor Market Report:

In 2023, the Power Semiconductor market in Asia Pacific is valued at $7.83 billion, growing to approximately $14.51 billion by 2033. This region is driven by strong manufacturing bases in countries like China, Japan, and South Korea, alongside increasing investments in electric vehicles and renewable energy, contributing to significant market growth.North America Power Semiconductor Market Report:

North America, with a market size of $16.09 billion in 2023, is expected to reach $29.80 billion by 2033. The region benefits from strong technological innovation and a focus on energy-efficient solutions, particularly in electric vehicle applications and industrial automation.South America Power Semiconductor Market Report:

The South American Power Semiconductor market is forecasted to grow from $0.57 billion in 2023 to $1.05 billion by 2033. The growth is primarily due to rising demand in automotive and renewable energy sectors, although infrastructure challenges present constraints on rapid advancements.Middle East & Africa Power Semiconductor Market Report:

The market in the Middle East and Africa is projected to grow from $5.78 billion in 2023 to $10.70 billion by 2033. Although the region faces various challenges regarding energy infrastructure, opportunities remain particularly in renewable energy development and increasing automotive applications.Tell us your focus area and get a customized research report.

Power Semiconductor Market Analysis By Technology

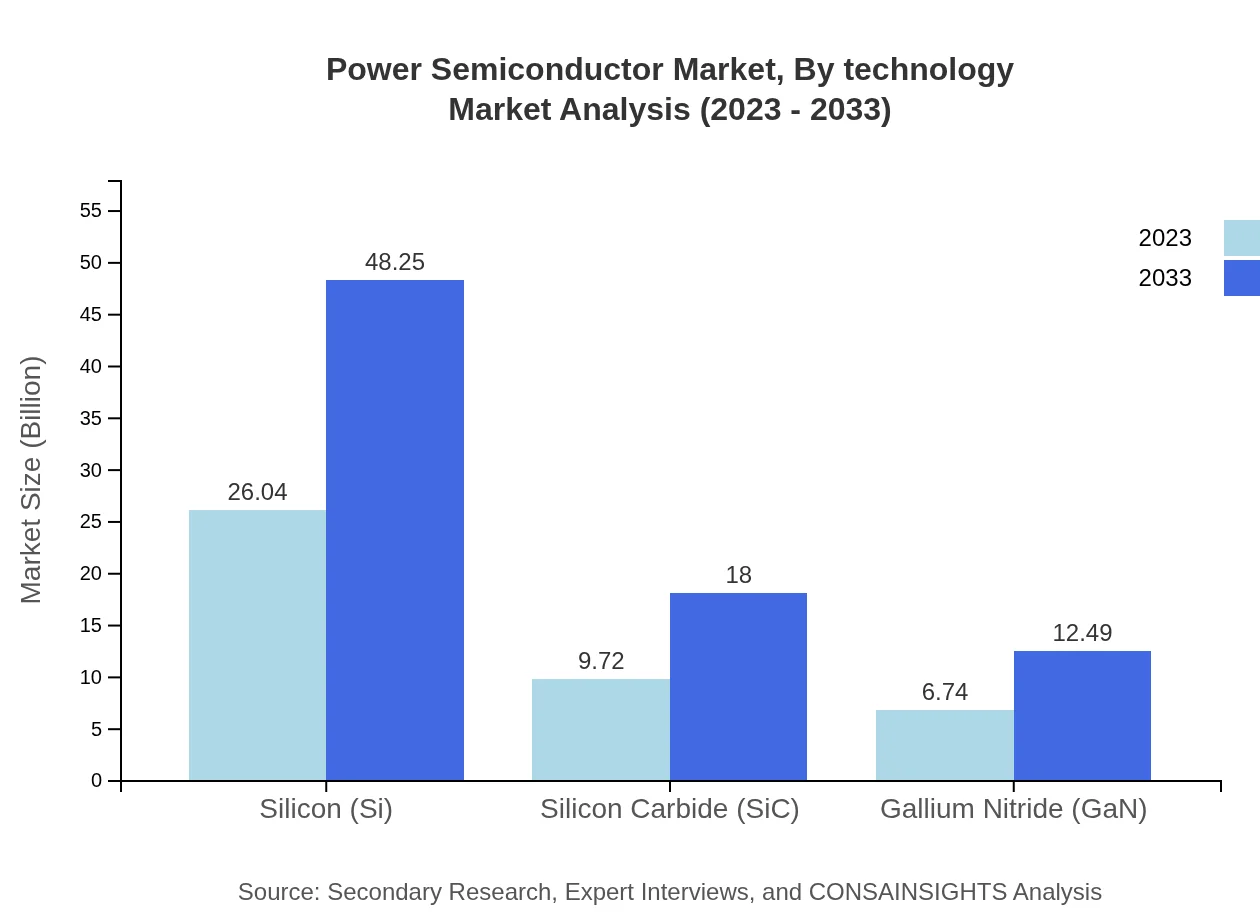

The Power Semiconductor market is segmented by technology into Silicon, Silicon Carbide (SiC), and Gallium Nitride (GaN). In 2023, Silicon leads the market with a size of $26.04 billion, expected to grow to $48.25 billion by 2033. SiC and GaN technologies also show significant promise, with market sizes of $9.72 billion and $6.74 billion in 2023, growing to $18 billion and $12.49 billion, respectively, as industries transition to higher efficiency systems.

Power Semiconductor Market Analysis By Application

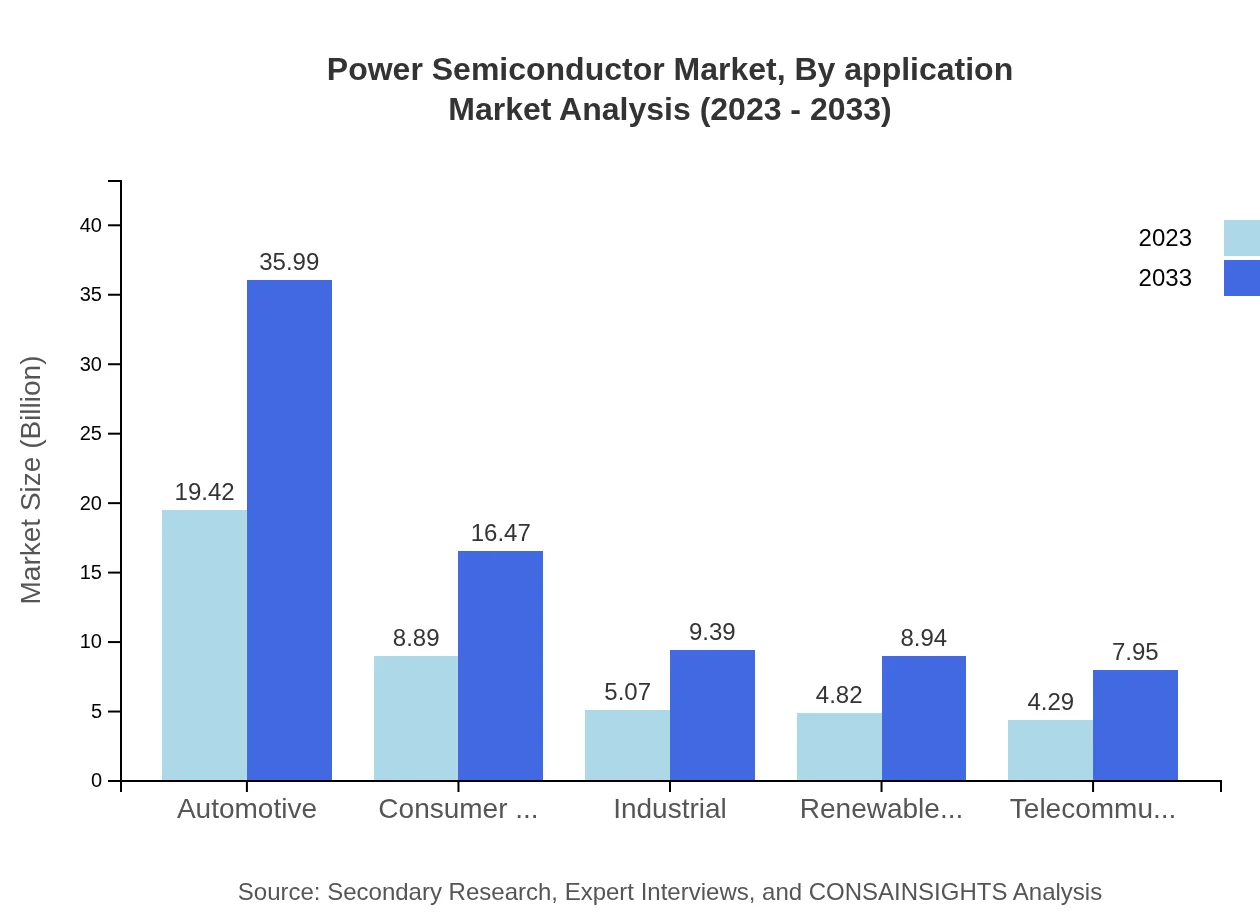

Segmentation by application reveals the Automotive segment to be the largest, estimated at $19.42 billion in 2023, rising to $35.99 billion by 2033. Consumer Electronics follows, with projections of $8.89 billion to $16.47 billion, while Renewable Energy is forecasted to grow from $4.82 billion in 2023 to $8.94 billion by 2033, all indicating robust demand for power semiconductors across multiple applications.

Power Semiconductor Market Analysis By Component

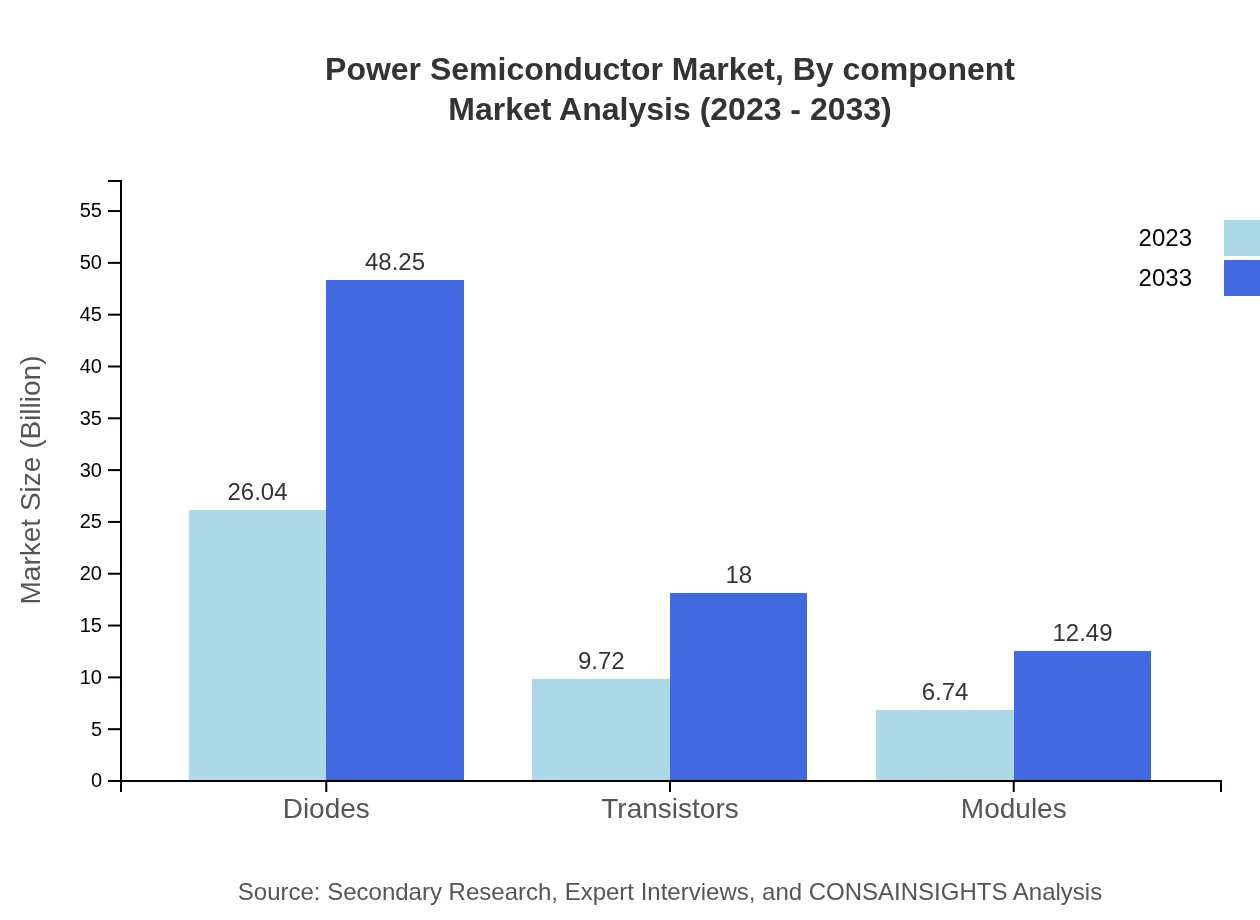

The Power Semiconductor market is also categorized by components, including Diodes, Transistors, Modules, and Power Supplies. Diodes represent the largest share, with $26.04 billion in 2023, escalating to $48.25 billion by 2033. Power Supplies and Modules demonstrate valuable growth trends as well, underlining the importance of each component in various electronic and energy management applications.

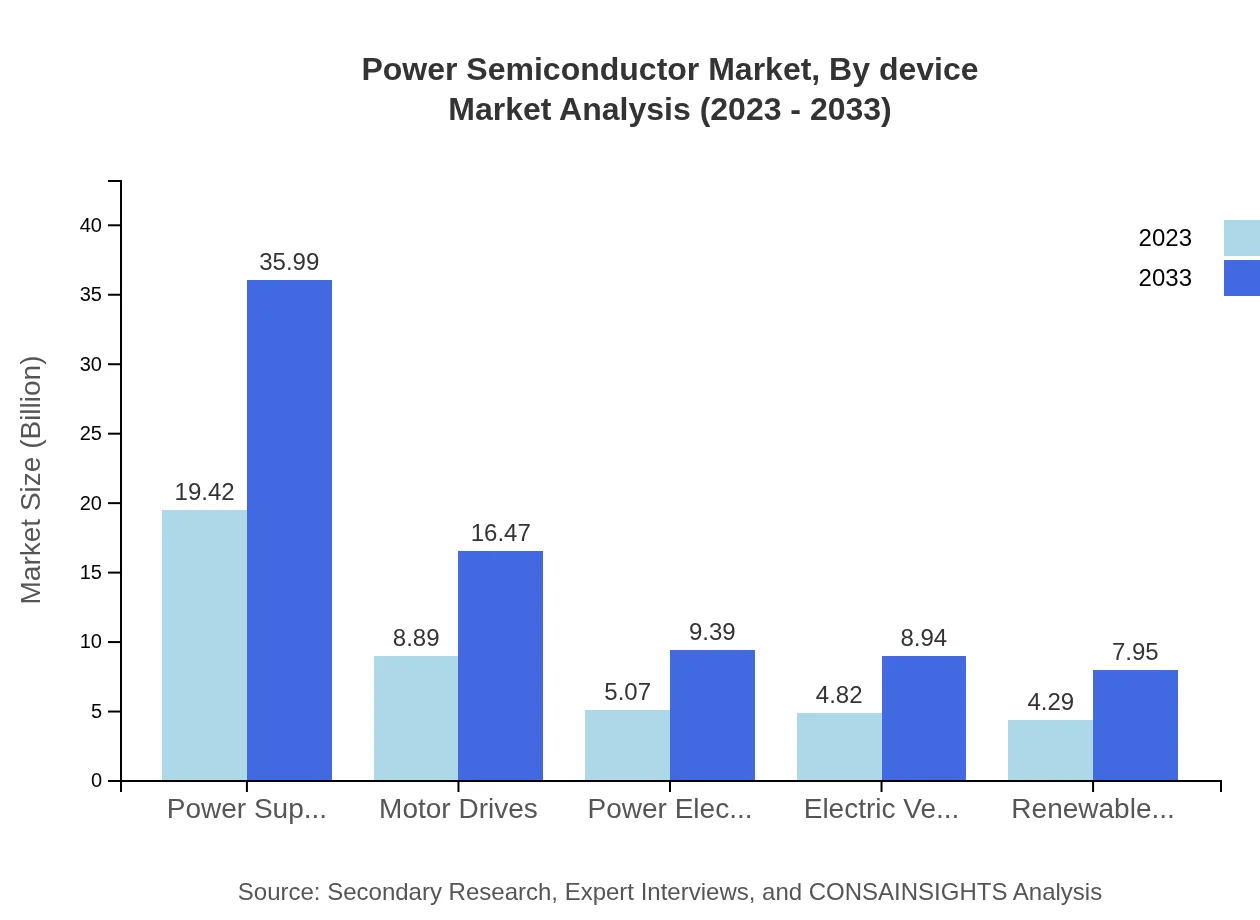

Power Semiconductor Market Analysis By Device

Analysis by device includes segments such as electric vehicles, renewable energy systems, and consumer electronics. Notably, electric vehicles are anticipated to exhibit substantial growth, evolving from $4.82 billion in 2023 to $8.94 billion by 2033. This segment emphasizes the increasing incorporation of power semiconductors in devices demanding high efficiency and performance.

Power Semiconductor Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Power Semiconductor Industry

Infineon Technologies:

Infineon is a leading semiconductor manufacturer specializing in power semiconductors for automotive, industrial, and consumer applications, aiming for energy efficiency and sustainable solutions.Texas Instruments:

Texas Instruments is renowned for its innovations in analog electronics and power management semiconductors, providing high-quality and reliable products across diverse industries.STMicroelectronics:

STMicroelectronics focuses on developing innovative and energy-efficient power semiconductor solutions for automotive, industrial, and communication applications.NXP Semiconductors:

NXP is recognized for its expertise in automotive semiconductors and secure connectivity solutions, addressing the demand for smart, connected, and energy-efficient devices.ON Semiconductor:

ON Semiconductor provides a comprehensive portfolio of power semiconductor products and focuses on enabling customers to develop advanced applications.We're grateful to work with incredible clients.

FAQs

What is the market size of power Semiconductor?

The global power semiconductor market is projected to grow from $42.5 billion in 2023, with a CAGR of 6.2%, indicating strong demand over the next decade, reaching substantial market value by 2033.

What are the key market players or companies in the power Semiconductor industry?

Key players in the power semiconductor market include prominent companies like Infineon Technologies, Texas Instruments, ON Semiconductor, STMicroelectronics, and Vishay Intertechnology, which lead in innovation and production.

What are the primary factors driving the growth in the power semiconductor industry?

The growth in the power semiconductor industry is largely driven by the increasing adoption of electric vehicles, renewable energy systems, and advancements in consumer electronics, alongside the rising demand for energy-efficient devices.

Which region is the fastest Growing in the power semiconductor?

Asia Pacific is the fastest-growing region in the power semiconductor market, with the market expected to expand from $7.83 billion in 2023 to $14.51 billion by 2033 due to rapid technological advancements.

Does ConsaInsights provide customized market report data for the power Semiconductor industry?

Yes, ConsaInsights offers customized market report data tailored to specific needs within the power semiconductor industry, allowing clients to gain insights pertinent to their business strategy.

What deliverables can I expect from this power Semiconductor market research project?

From the power semiconductor market research project, clients can expect comprehensive reports featuring market analysis, growth projections, competitive landscape, and detailed segmentation across various channels.

What are the market trends of power semiconductor?

Key market trends in the power semiconductor sector include a significant shift towards silicon carbide (SiC) and gallium nitride (GaN) technologies, as well as increased investments in smart grid and renewable energy solutions.