Reverse Shoulder Arthroplasty Market Report

Published Date: 31 January 2026 | Report Code: reverse-shoulder-arthroplasty

Reverse Shoulder Arthroplasty Market Size, Share, Industry Trends and Forecast to 2033

This report provides an in-depth analysis of the Reverse Shoulder Arthroplasty market, highlighting current trends, market size, growth forecasts, and competitive landscape for the forecast period 2023 to 2033.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

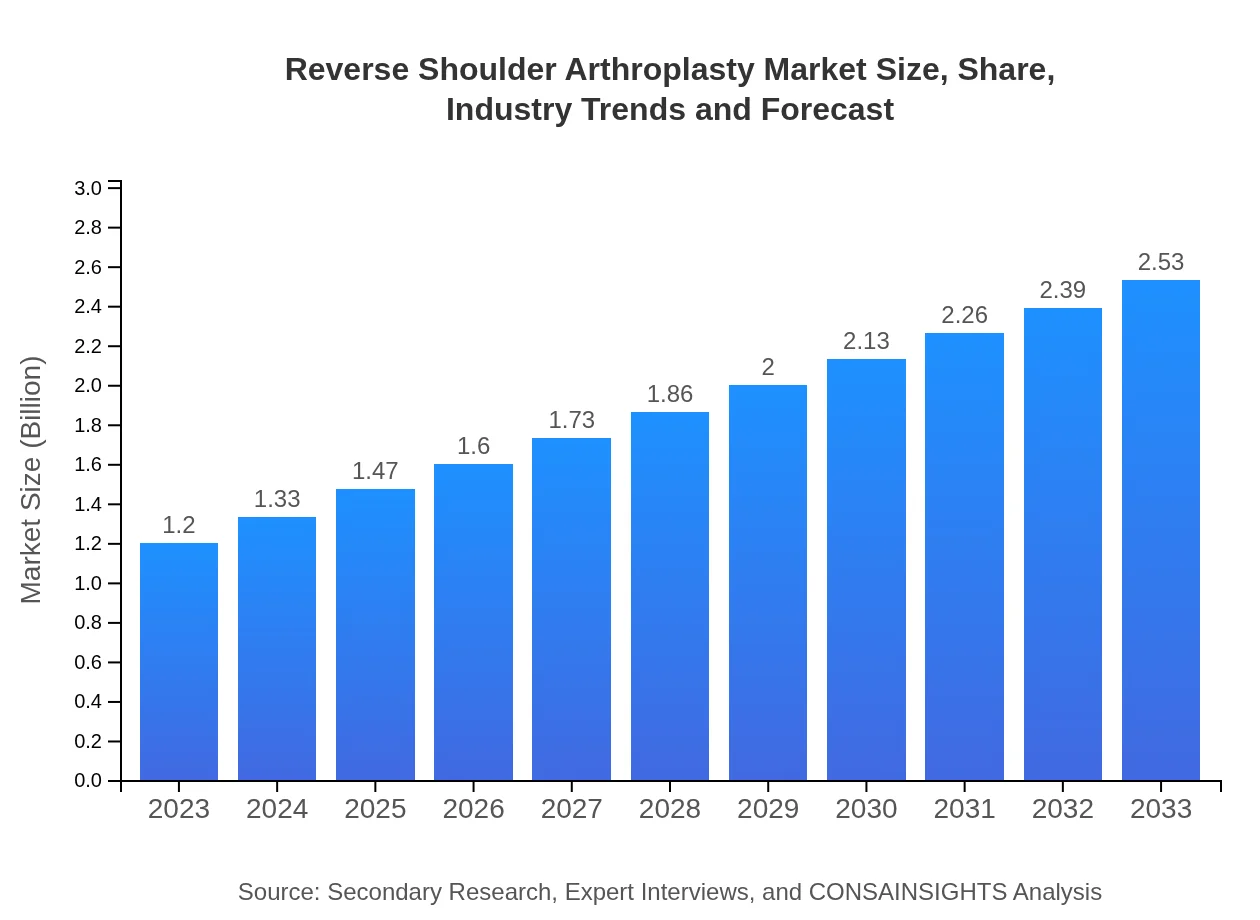

| 2023 Market Size | $1.20 Billion |

| CAGR (2023-2033) | 7.5% |

| 2033 Market Size | $2.53 Billion |

| Top Companies | DePuy Synthes, Zimmer Biomet, Stryker Corporation, Smith & Nephew, Wright Medical Group |

| Last Modified Date | 31 January 2026 |

Reverse Shoulder Arthroplasty Market Overview

Customize Reverse Shoulder Arthroplasty Market Report market research report

- ✔ Get in-depth analysis of Reverse Shoulder Arthroplasty market size, growth, and forecasts.

- ✔ Understand Reverse Shoulder Arthroplasty's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Reverse Shoulder Arthroplasty

What is the Market Size & CAGR of Reverse Shoulder Arthroplasty market in 2023?

Reverse Shoulder Arthroplasty Industry Analysis

Reverse Shoulder Arthroplasty Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Reverse Shoulder Arthroplasty Market Analysis Report by Region

Europe Reverse Shoulder Arthroplasty Market Report:

Europe's market for Reverse Shoulder Arthroplasty is projected to grow from USD 0.42 billion in 2023 to USD 0.89 billion in 2033. The region benefits from high healthcare expenditure, advanced healthcare infrastructure, and a growing elderly population requiring shoulder surgeries.Asia Pacific Reverse Shoulder Arthroplasty Market Report:

In the Asia-Pacific region, the market for Reverse Shoulder Arthroplasty is expected to grow significantly, from USD 0.21 billion in 2023 to USD 0.45 billion by 2033. This growth is driven by improved healthcare infrastructure, increasing patient awareness regarding shoulder surgeries, and the rising geriatric population in countries like Japan and Australia.North America Reverse Shoulder Arthroplasty Market Report:

North America dominates the RSA market, with an estimated size of USD 0.40 billion in 2023, growing to USD 0.84 billion by 2033. The market's expansion can be attributed to the high prevalence of shoulder disorders, favorable reimbursement policies, and advancements in surgical techniques.South America Reverse Shoulder Arthroplasty Market Report:

The South American RSA market is anticipated to expand from USD 0.06 billion in 2023 to USD 0.12 billion by 2033. Factors contributing to this growth include improved access to healthcare services and increasing investments in healthcare technologies.Middle East & Africa Reverse Shoulder Arthroplasty Market Report:

The Middle East and Africa market is expected to show steady growth, increasing from USD 0.11 billion in 2023 to USD 0.23 billion by 2033. Investment in healthcare systems and awareness regarding advanced surgical options are key drivers in this region.Tell us your focus area and get a customized research report.

Reverse Shoulder Arthroplasty Market Analysis By Indication

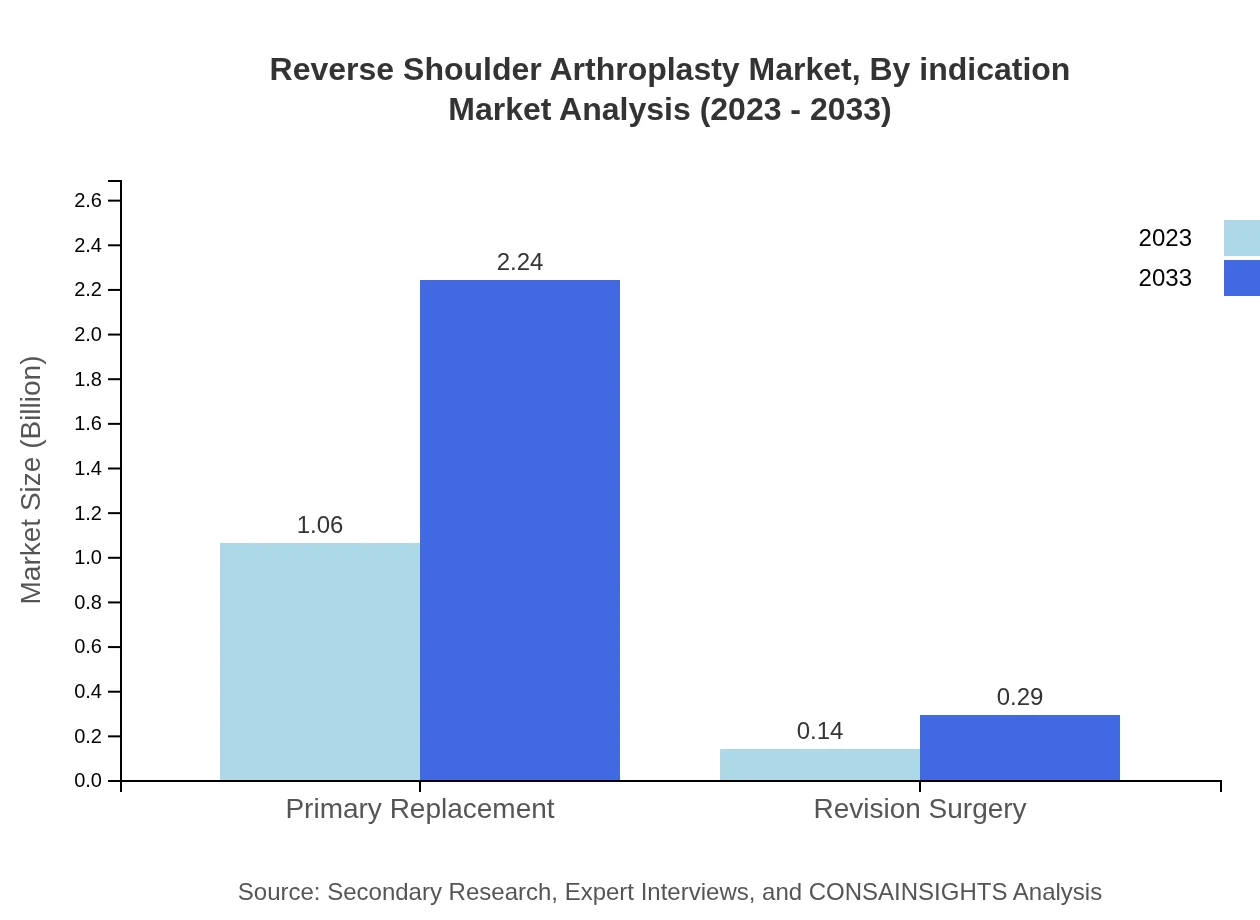

By indication, the market is primarily divided into primary replacements, accounting for approximately 88.65% share in 2023, while revision surgery constitutes 11.35%. This trend is expected to persist, with primary replacements growing from USD 1.06 billion to USD 2.24 billion from 2023 to 2033, signifying the importance of primary RSA procedures for patient recovery.

Reverse Shoulder Arthroplasty Market Analysis By Material

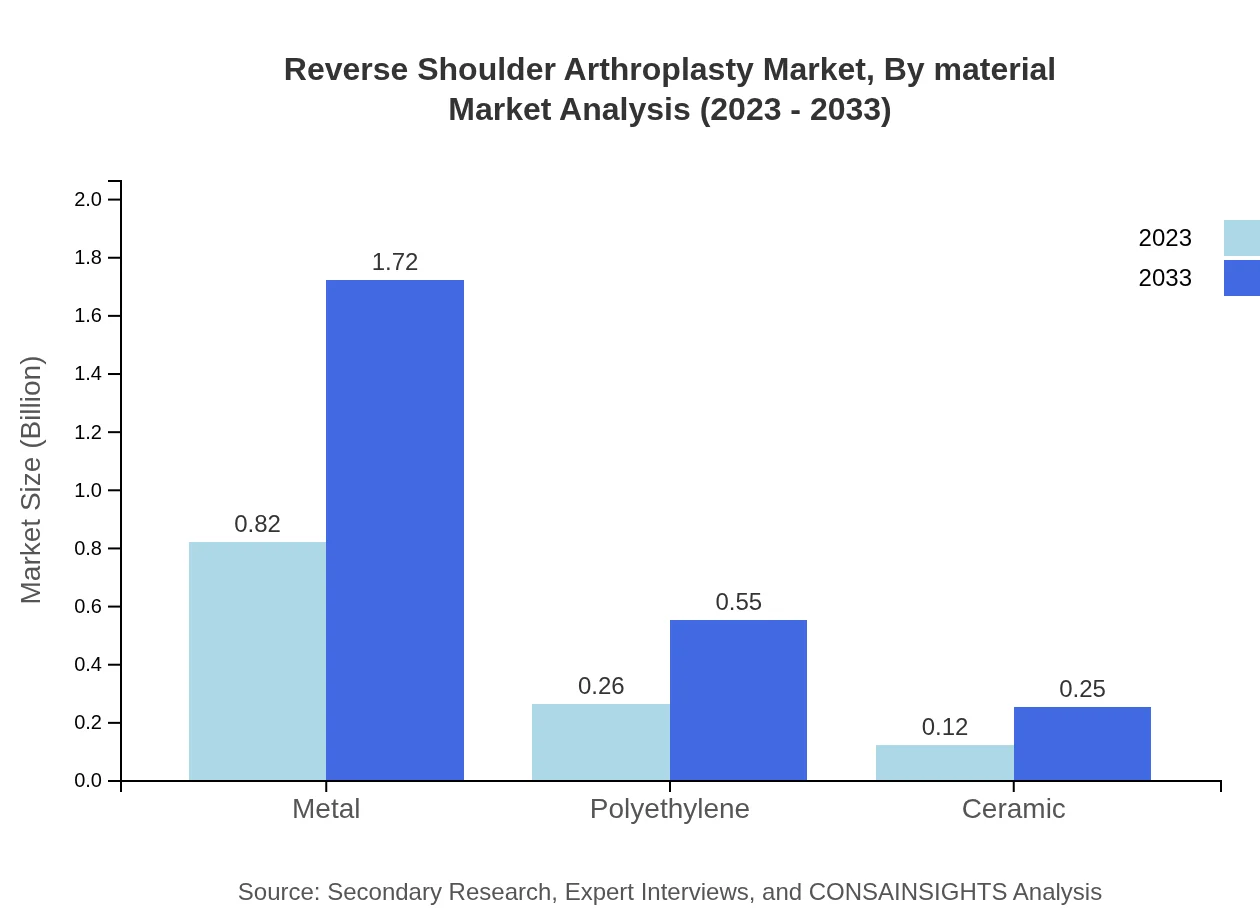

Material segmentation identifies metal, polyethylene, and ceramic implants as key market players. Metal implants dominate the segment, holding 68.21% of the market share in 2023. Growth is projected with metal implants expanding to USD 1.72 billion by 2033, driven by their durability and biomechanical advantages over alternatives.

Reverse Shoulder Arthroplasty Market Analysis By End User

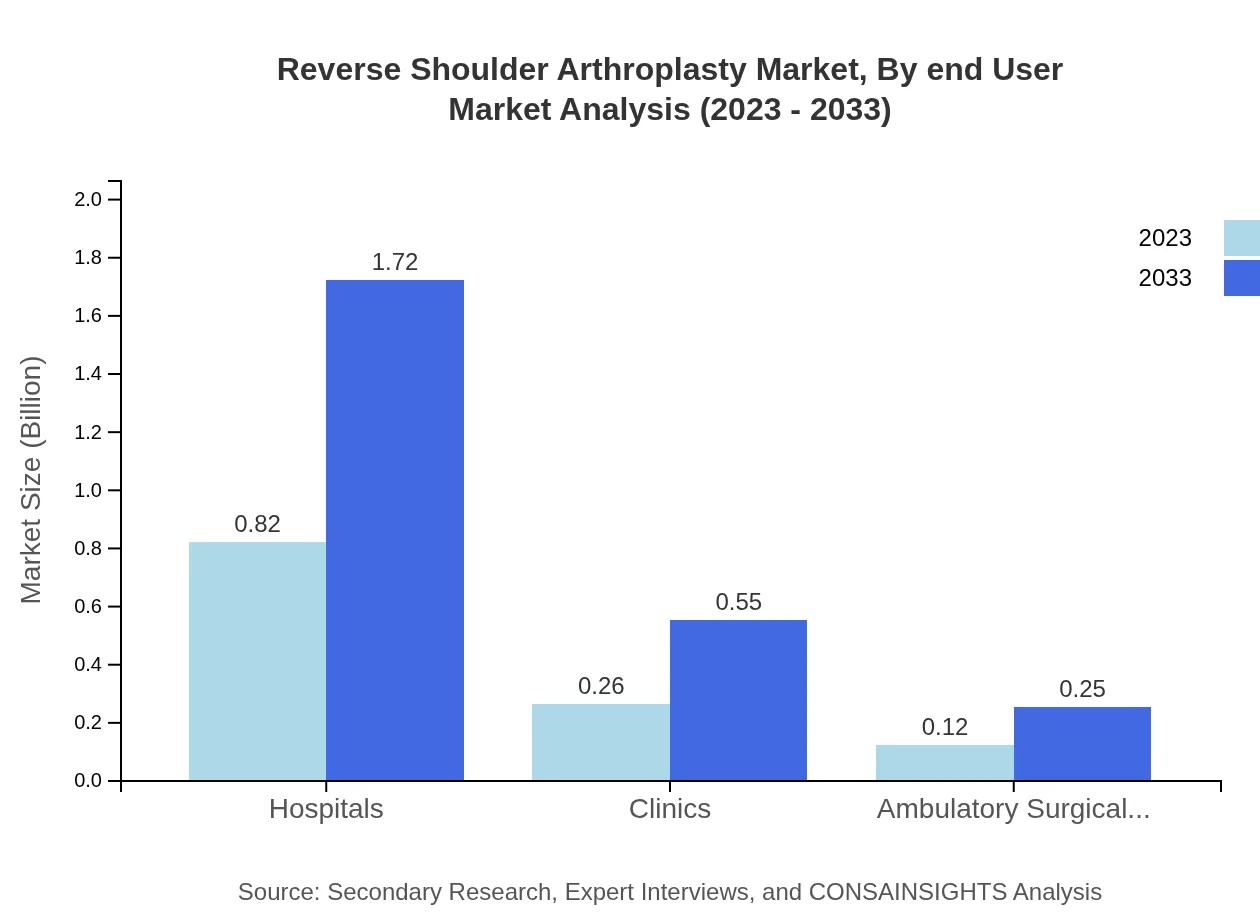

Hospitals are the primary end-users, representing 68.21% of the market in 2023, with projected growth from USD 0.82 billion to USD 1.72 billion. Ambulatory surgical centers are gaining traction, offering minimally invasive procedures, yet they account for a smaller segment at 9.97% in 2023.

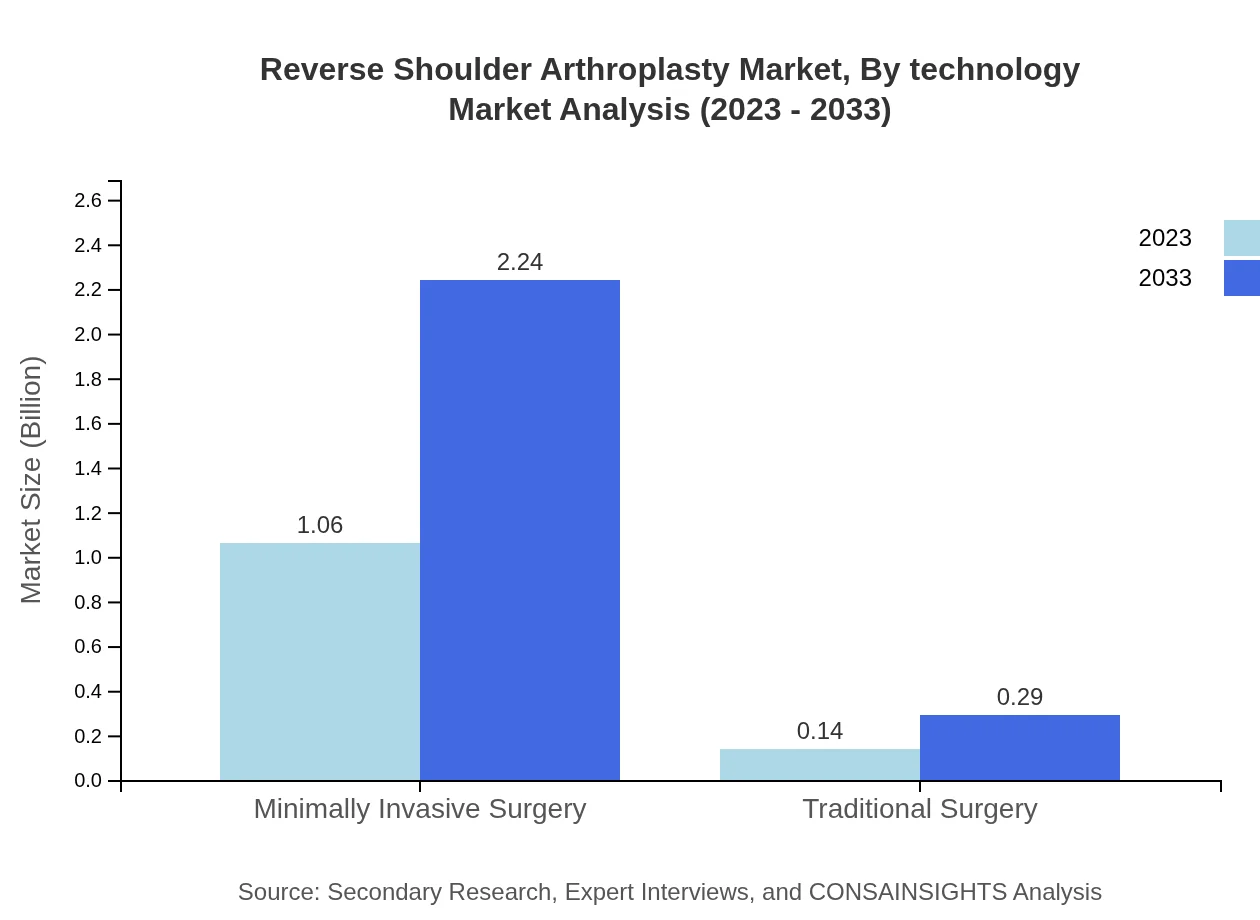

Reverse Shoulder Arthroplasty Market Analysis By Technology

Technologically, minimally invasive surgical methods dominate the market with an 88.65% share in 2023, owing to advantages such as shorter recovery times and fewer complications. Traditional surgeries comprise the remaining 11.35%, indicating a transitioning preference towards advanced technologies in orthopedics.

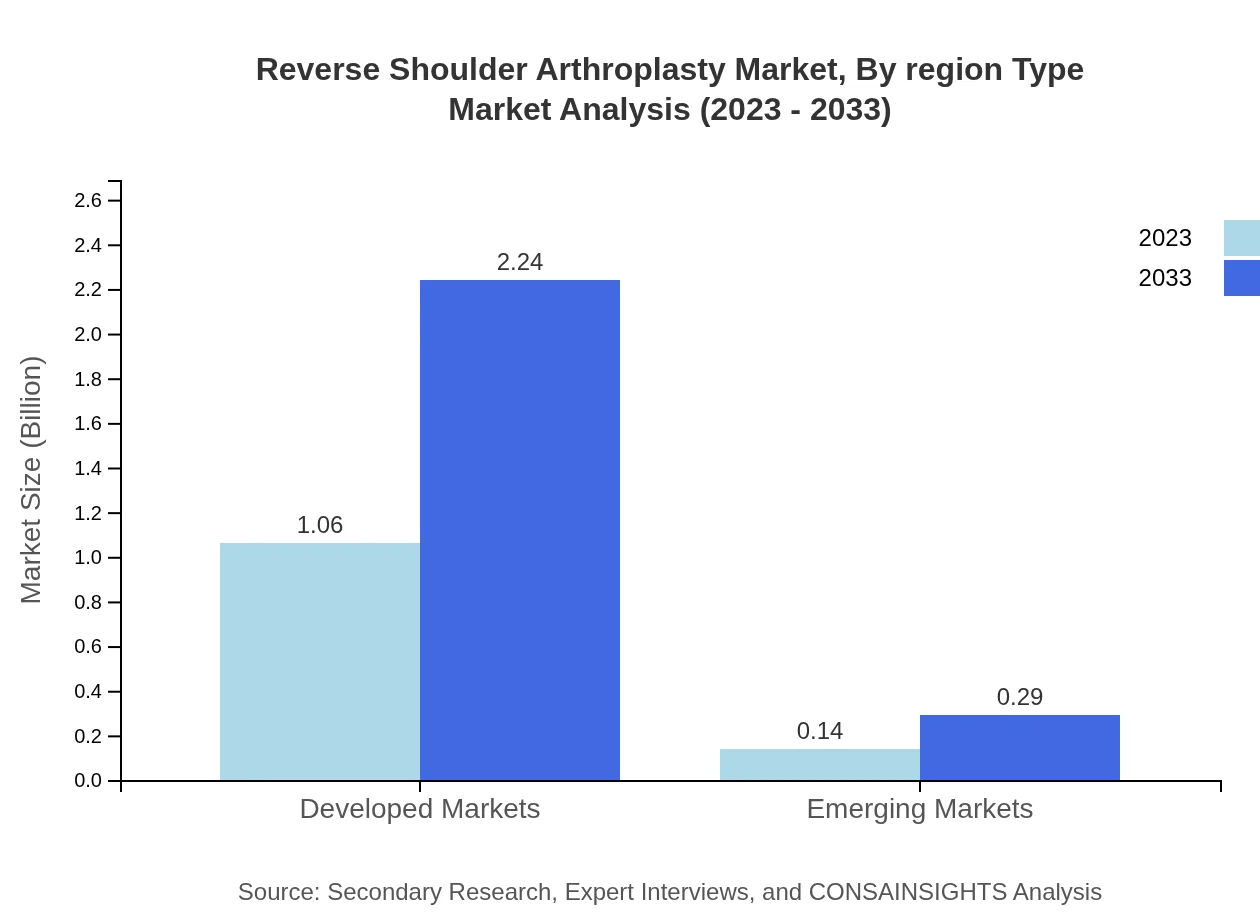

Reverse Shoulder Arthroplasty Market Analysis By Region Type

Geographically, the market is dominated by developed regions, specifically North America and Europe, which together contribute significantly to the global RSA market. Emerging markets are expected to show progressive growth as healthcare access improves and surgical options become more prevalent.

Reverse Shoulder Arthroplasty Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Reverse Shoulder Arthroplasty Industry

DePuy Synthes:

A leader in orthopedic solutions, DePuy Synthes focuses on developing innovative implants that enhance the performance, safety, and efficacy of shoulder replacement surgeries.Zimmer Biomet:

Zimmer Biomet is renowned for its advanced orthopedic technologies and has a significant market presence in the RSA sector, offering a range of shoulder arthroplasty solutions.Stryker Corporation:

Stryker Corporation is a key player in medical technology, providing a variety of innovative products and services for shoulder surgeries, contributing to enhanced surgical outcomes.Smith & Nephew:

This company is committed to advancing surgery through innovative solutions and has a strong portfolio in shoulder arthroplasty aimed at improving patient care.Wright Medical Group:

Wright Medical specializes in extremities and biologics, focusing on developing new technologies to improve the outcomes of shoulder surgeries.We're grateful to work with incredible clients.

FAQs

What is the market size of reverse Shoulder Arthroplasty?

The global reverse shoulder arthroplasty market was valued at approximately $1.2 billion in 2023, with a projected CAGR of 7.5%. By 2033, the market is expected to continue expanding significantly, reflecting increasing adoption in clinical practices.

What are the key market players or companies in this reverse Shoulder Arthroplasty industry?

Key players in the reverse shoulder arthroplasty market include major orthopedic device companies such as Zimmer Biomet, DePuy Synthes, Stryker, and Arthrex. Their innovation and product development continue to shape the landscape of shoulder arthroplasty.

What are the primary factors driving the growth in the reverse Shoulder Arthroplasty industry?

Growth drivers for the reverse-shoulder-arthroplasty market include the rising incidence of shoulder arthritis, advancements in surgical techniques, increased awareness about shoulder joint replacements, and an aging population that is more prone to orthopedic conditions.

Which region is the fastest Growing in the reverse Shoulder Arthroplasty?

The fastest-growing region in the reverse shoulder arthroplasty market is North America, projected to grow from $0.40 billion in 2023 to $0.84 billion by 2033, driven by technological advancements, robust healthcare infrastructure, and high demand for orthopedic procedures.

Does ConsaInsights provide customized market report data for the reverse Shoulder Arthroplasty industry?

Yes, ConsaInsights offers customized market report data tailored to client's specific needs in the reverse shoulder arthroplasty industry, enabling more relevant insights and strategic decisions.

What deliverables can I expect from this reverse Shoulder Arthroplasty market research project?

Deliverables include comprehensive market analysis reports, detailed regional segmentation, competitive landscape evaluations, trend analysis, and forecasts covering growth rates and market shares, ensuring in-depth insights.

What are the market trends of reverse Shoulder Arthroplasty?

Current trends in the reverse shoulder arthroplasty market include increased adoption of minimally invasive surgical techniques, the rise of outpatient procedures, and a shift towards personalized implant designs to enhance surgical outcomes.