Semiconductor Silicon Wafer Market Report

Published Date: 31 January 2026 | Report Code: semiconductor-silicon-wafer

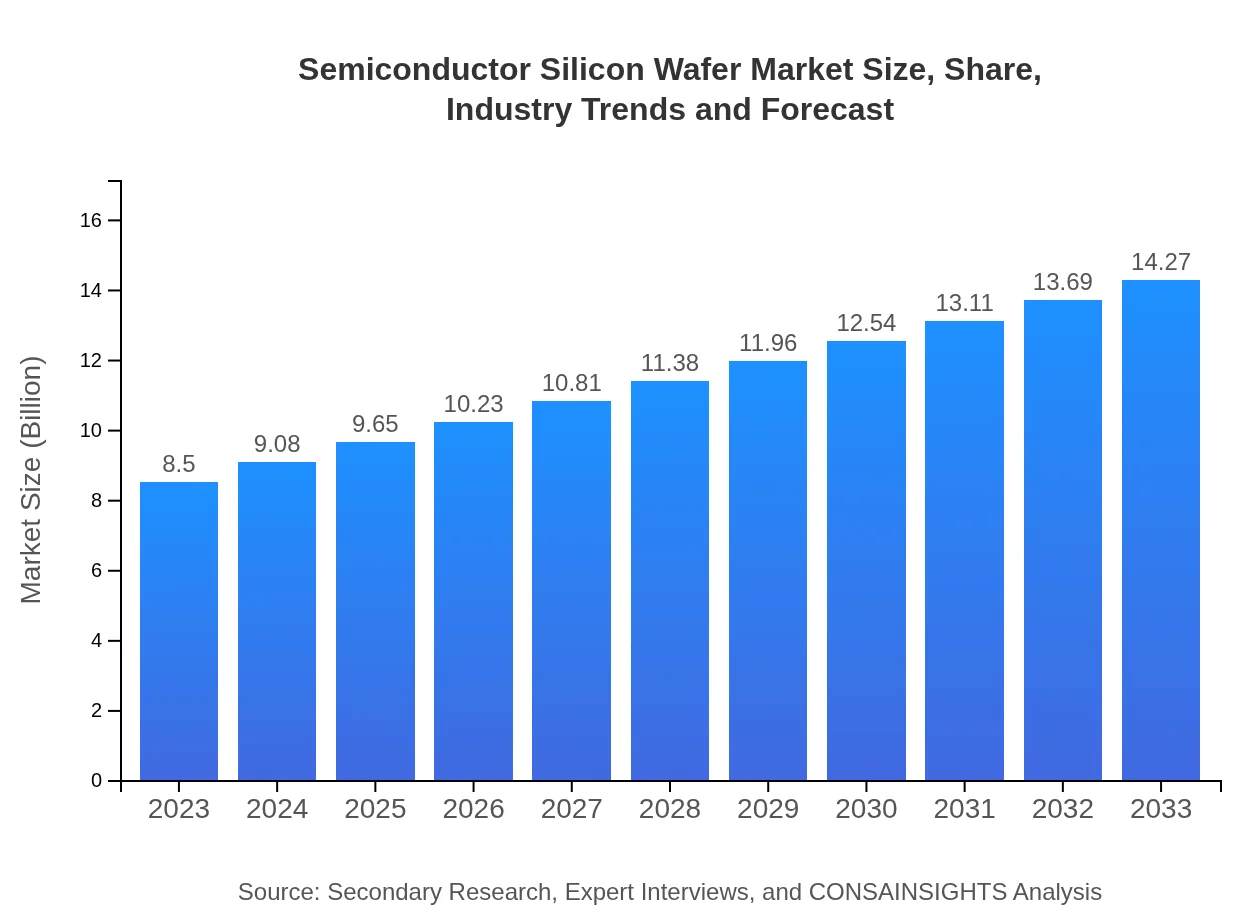

Semiconductor Silicon Wafer Market Size, Share, Industry Trends and Forecast to 2033

This report provides a comprehensive analysis of the Semiconductor Silicon Wafer market, focusing on market trends, forecasts, and technological advancements from 2023 to 2033.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $8.50 Billion |

| CAGR (2023-2033) | 5.2% |

| 2033 Market Size | $14.27 Billion |

| Top Companies | Siltronic AG, Shin-Etsu Chemical Co., Ltd., SUMCO Corporation, GlobalWafers Co., Ltd. |

| Last Modified Date | 31 January 2026 |

Semiconductor Silicon Wafer Market Overview

Customize Semiconductor Silicon Wafer Market Report market research report

- ✔ Get in-depth analysis of Semiconductor Silicon Wafer market size, growth, and forecasts.

- ✔ Understand Semiconductor Silicon Wafer's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Semiconductor Silicon Wafer

What is the Market Size & CAGR of Semiconductor Silicon Wafer market in 2023?

Semiconductor Silicon Wafer Industry Analysis

Semiconductor Silicon Wafer Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Semiconductor Silicon Wafer Market Analysis Report by Region

Europe Semiconductor Silicon Wafer Market Report:

In Europe, the market is set to grow from $2.20 billion in 2023 to $3.69 billion by 2033. The region emphasizes high-quality standards in semiconductor production and is focusing on innovations in the automotive sector, especially concerning electric vehicles and smart technologies.Asia Pacific Semiconductor Silicon Wafer Market Report:

The Asia Pacific region is dominant in the semiconductor silicon wafer market, accounting for a significant share due to the presence of major manufacturers in countries like Taiwan, South Korea, and Japan. The market size is projected to grow from $1.77 billion in 2023 to $2.97 billion by 2033, driven by increasing demand in consumer electronics and telecommunications sectors, emphasizing investment in advanced semiconductor technologies.North America Semiconductor Silicon Wafer Market Report:

North America's market for semiconductor silicon wafers is also poised for growth, with the market size projected to elevate from $3.02 billion in 2023 to $5.06 billion in 2033. This increase is fueled by advancements in automotive electronics, infrastructure for renewable energy, and robust IT investments, predominantly in the U.S.South America Semiconductor Silicon Wafer Market Report:

In South America, the semiconductor silicon wafer market is expanding, with a market size of $0.69 billion in 2023 expected to reach $1.16 billion by 2033. Growth is attributed to rising technological adoption and increasing demand for electronic devices, chiefly in Brazil and Argentina, where government initiatives support tech investments.Middle East & Africa Semiconductor Silicon Wafer Market Report:

The Middle East and Africa semiconductor silicon wafer market is anticipated to expand from $0.82 billion in 2023 to $1.38 billion by 2033. The CAGR growth is propelled by increased electronics consumption and strategic collaborations to enhance local manufacturing capabilities, especially in the UAE and South Africa.Tell us your focus area and get a customized research report.

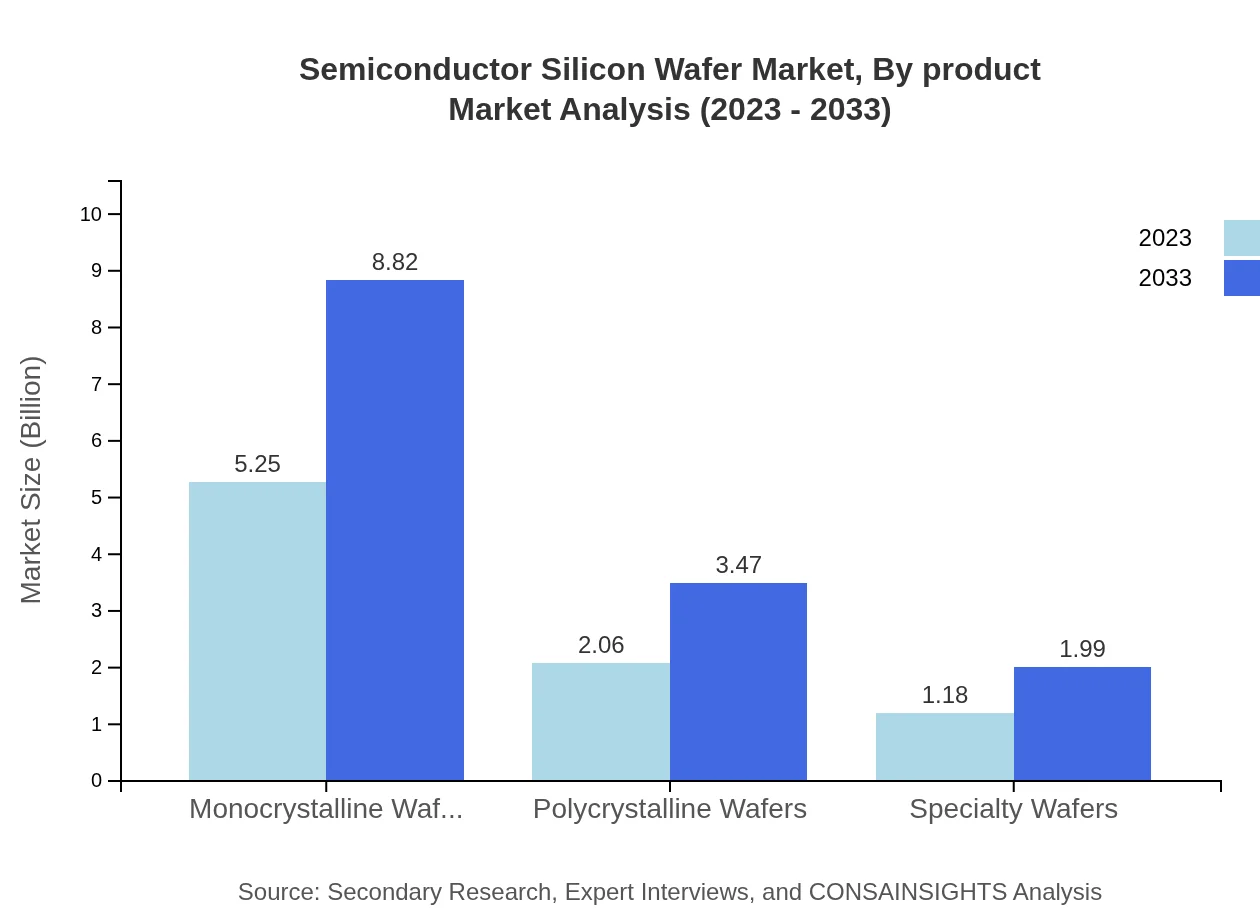

Semiconductor Silicon Wafer Market Analysis By Product

The leading product type in the market is Monocrystalline Wafers, valued at $5.25 billion in 2023 and projected to grow to $8.82 billion by 2033, capturing a market share of 61.78%. Polycrystalline Wafers follow with a size of $2.06 billion expected to reach $3.47 billion, holding 24.29% market share. Specialty Wafers, while smaller, are increasing noticeably with a projected growth from $1.18 billion to $1.99 billion, representing 13.93% of the market.

Semiconductor Silicon Wafer Market Analysis By Application

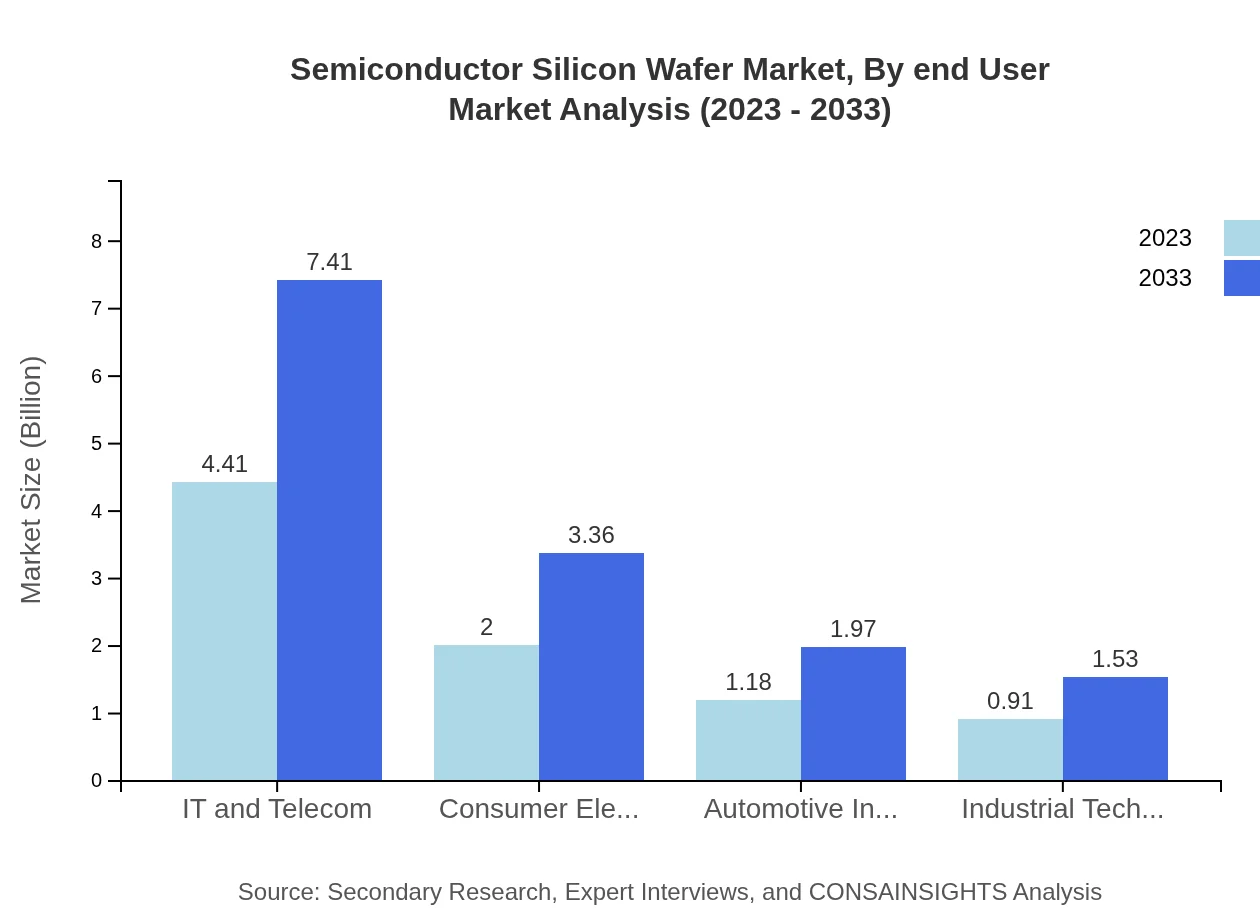

The IT and Telecom sector dominates the application segment with a size of $4.41 billion in 2023 and an expectation to grow to $7.41 billion by 2033, capturing 51.9% of the share. The Consumer Electronics segment is also significant, starting at $2 billion in 2023, and anticipated to grow to $3.36 billion, representing 23.58%. The Automotive Industry, with increasing integration of electronics in vehicles, has a projected growth from $1.18 billion to $1.97 billion, showcasing a growing 13.83% segment share.

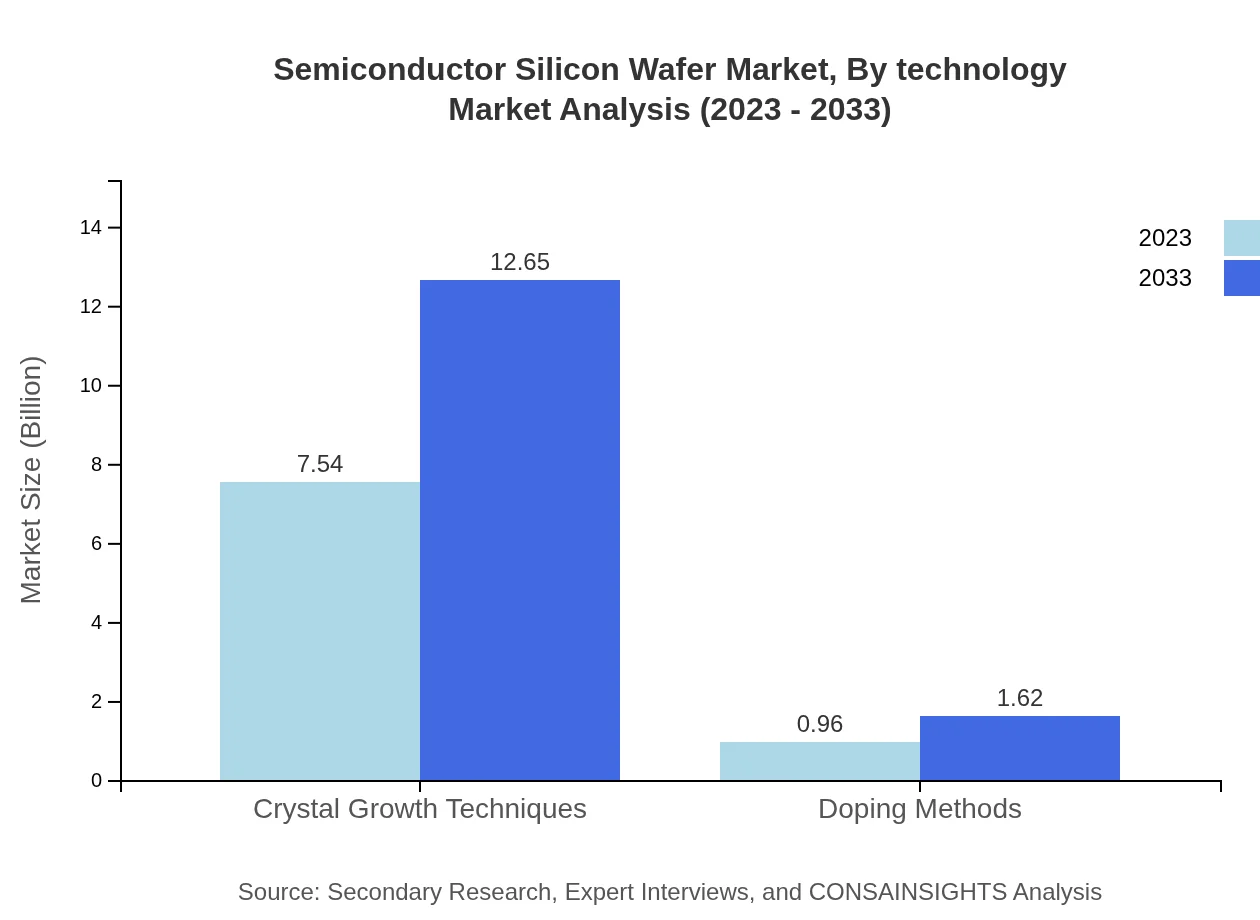

Semiconductor Silicon Wafer Market Analysis By Technology

In technology segmentation, Crystal Growth Techniques lead the market with a size of $7.54 billion in 2023, anticipated to reach $12.65 billion by 2033, possessing an 88.65% share. Doping Methods hold a relatively smaller segment, starting at $0.96 billion and expected to grow to $1.62 billion, representing a 11.35% share. These technologies are pivotal in enhancing the performance and efficiency of silicon wafers.

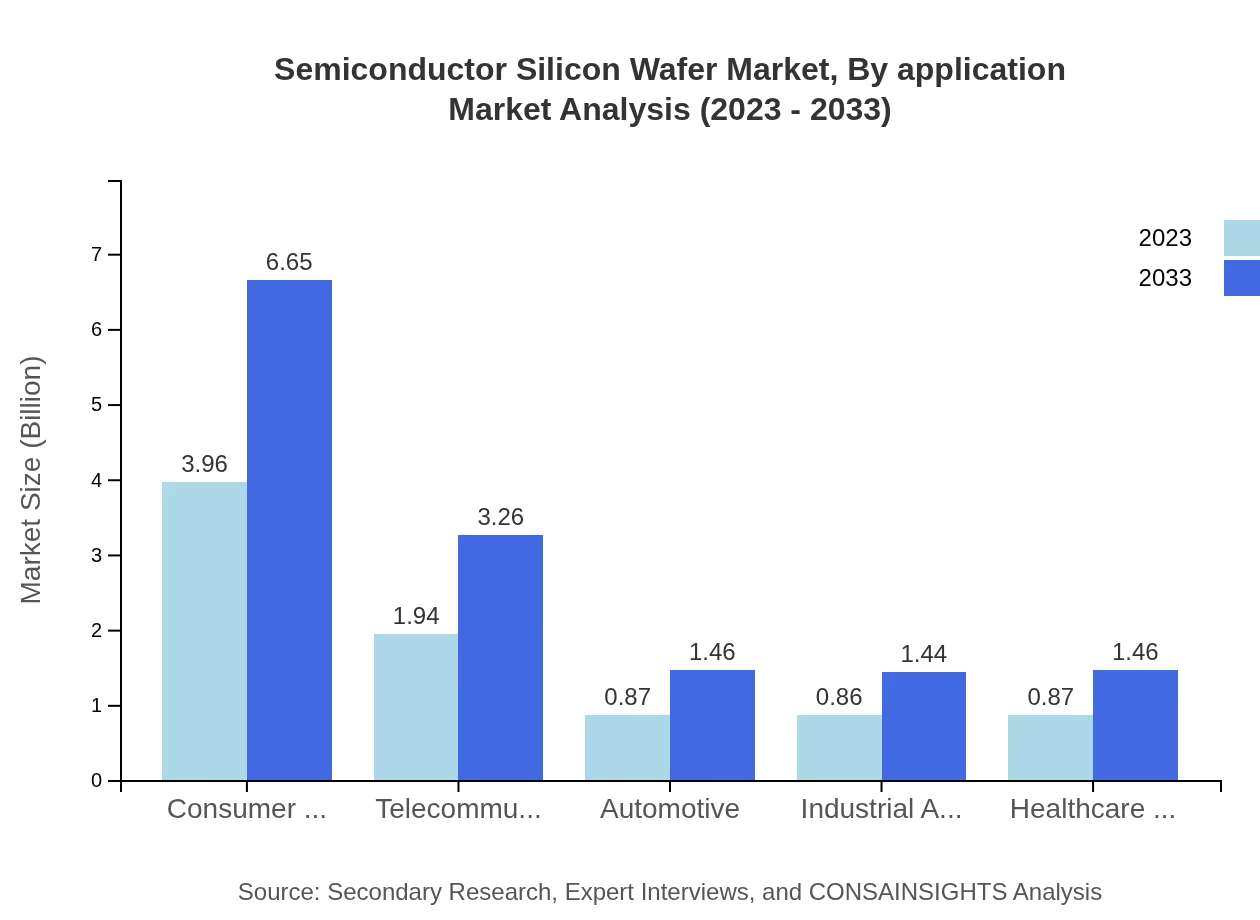

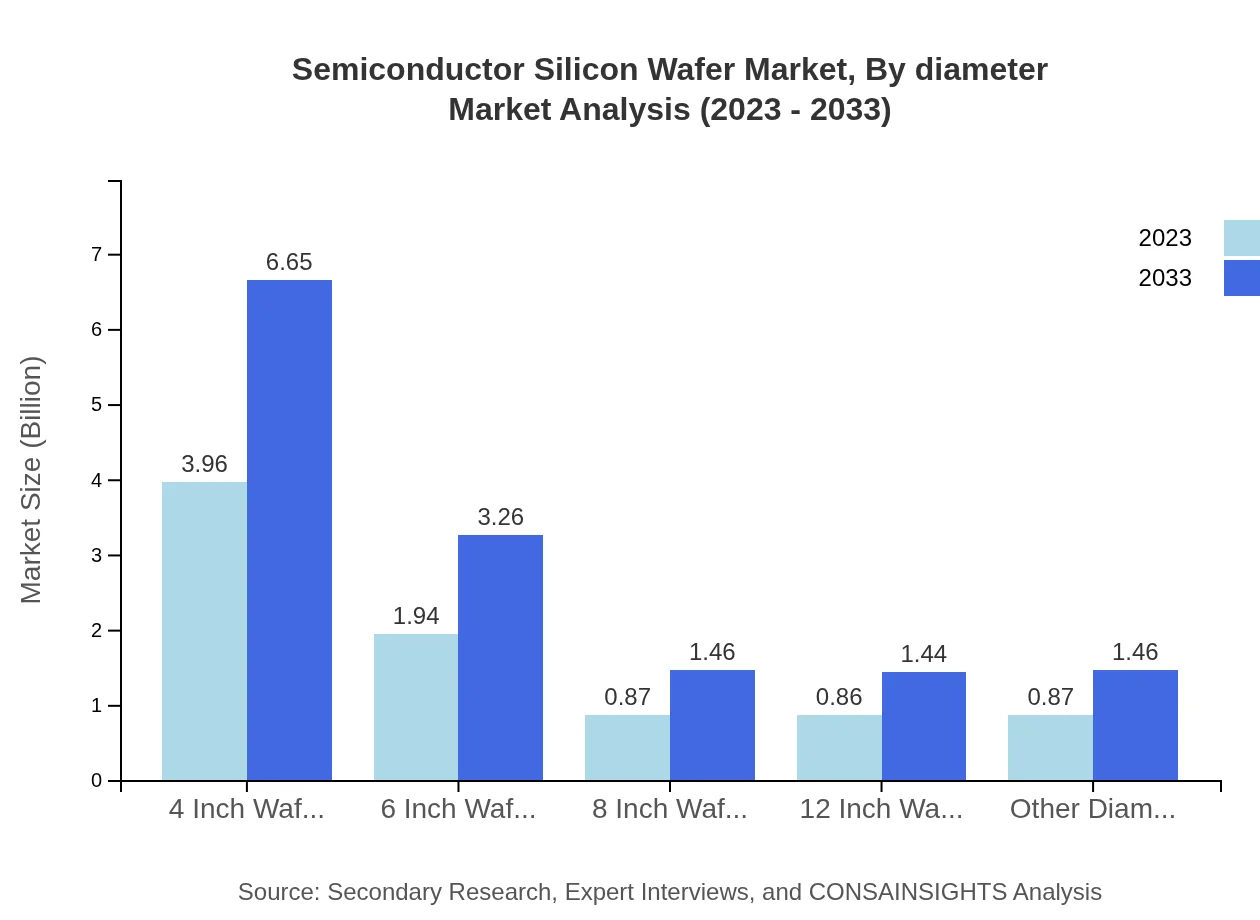

Semiconductor Silicon Wafer Market Analysis By Diameter

Four-inch wafers constitute a substantial market segment, with a size of $3.96 billion in 2023, projected to grow to $6.65 billion by 2033. Six-inch and eight-inch wafers also contribute significantly, with projections of $1.94 billion to $3.26 billion and $0.87 billion to $1.46 billion respectively. Twelve-inch wafers, while niche, are expected to expand from $0.86 billion to $1.44 billion, indicative of evolving market needs for larger diameter wafers.

Semiconductor Silicon Wafer Market Analysis By End User

Key end-user industries driving market demand include Consumer Electronics and Telecommunications, with market sizes of $3.96 billion and $1.94 billion respectively in 2023, both projected to grow significantly. Industries such as Automotive and Healthcare Devices are also expected to see notable growth due to rising demand for innovative technologies in vehicles and medical devices, further enhancing the overall market landscape.

Semiconductor Silicon Wafer Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Semiconductor Silicon Wafer Industry

Siltronic AG:

A leading producer of silicon wafers, Siltronic specializes in the production of monocrystalline silicon wafers and has a strong market presence in Europe and Asia.Shin-Etsu Chemical Co., Ltd.:

As a major supplier of silicon wafers worldwide, Shin-Etsu develops advanced materials and processes for high-efficiency semiconductor production.SUMCO Corporation:

A prominent manufacturer of silicon wafers, SUMCO focuses on producing high-quality products for various semiconductor applications including memory chips.GlobalWafers Co., Ltd.:

A key player in the silicon wafer market, GlobalWafers provides a diverse range of products and has a significant presence in both Asia and North America.We're grateful to work with incredible clients.

FAQs

What is the market size of Semiconductor Silicon Wafer?

The global Semiconductor Silicon Wafer market is valued at approximately $8.5 billion in 2023, with a projected CAGR of 5.2% through 2033, indicating robust growth and increasing demand across various sectors.

What are the key market players or companies in the Semiconductor Silicon Wafer industry?

Prominent companies in the Semiconductor Silicon Wafer industry include GlobalWafers, Siltronic AG, Shin-Etsu Chemical Co., and SOITEC. These players are pivotal due to their advanced technologies and significant production capacities.

What are the primary factors driving the growth in the Semiconductor Silicon Wafer industry?

The growth in the Semiconductor Silicon Wafer industry is primarily driven by the increasing demand for consumer electronics, advancements in automotive technology, and the rise in IoT applications, which necessitate more silicon wafers for production.

Which region is the fastest Growing in the Semiconductor Silicon Wafer market?

Asia Pacific is the fastest-growing region in the Semiconductor Silicon Wafer market, expanding from a market size of $1.77 billion in 2023 to an estimated $2.97 billion by 2033, fueled by heavy semiconductor manufacturing investments.

Does ConsaInsights provide customized market report data for the Semiconductor Silicon Wafer industry?

Yes, ConsaInsights offers customized market report data tailored to client specifications within the Semiconductor Silicon Wafer industry, ensuring relevant insights through bespoke research and analysis.

What deliverables can I expect from this Semiconductor Silicon Wafer market research project?

Expect comprehensive market reports, strategic insights, competitor analysis, segment performance evaluations, and future growth forecasts from the Semiconductor Silicon Wafer market research project.

What are the market trends of Semiconductor Silicon Wafer?

Key trends in the Semiconductor Silicon Wafer market include the transition towards advanced wafer technologies, increasing demand for specialty wafers, and sustainability initiatives aimed at reducing environmental impact.