Reports >

Food And Beverages

>

Soy Based Food Market Report

Soy Based Food Market Report

Published Date: 31 January 2026 | Report Code: soy-based-food

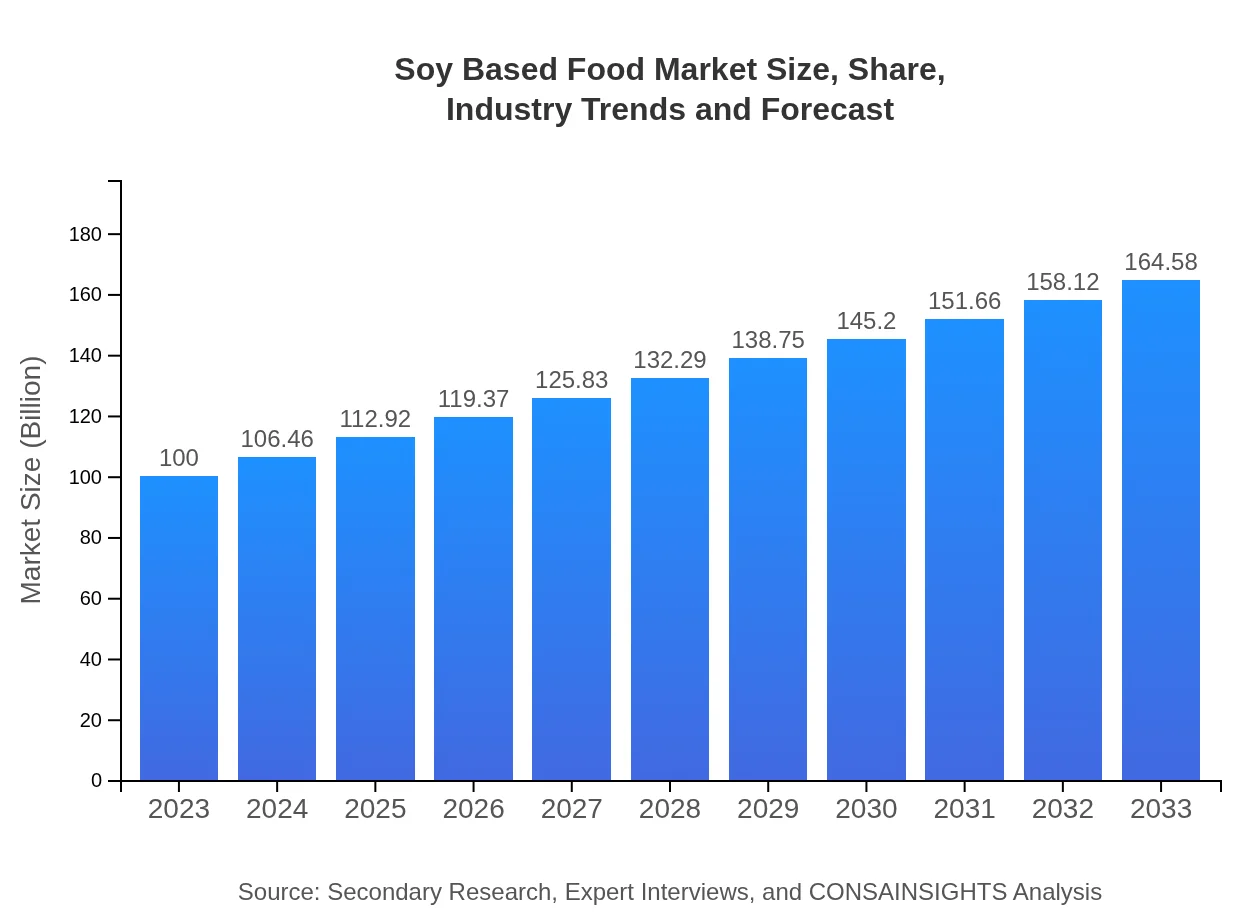

Soy Based Food Market Size, Share, Industry Trends and Forecast to 2033

This report provides an extensive analysis of the Soy Based Food market, covering market dynamics, size, segmentation, and trends for the forecast period from 2023 to 2033, offering key insights into current conditions and future growth.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $100.00 Million |

| CAGR (2023-2033) | 5% |

| 2033 Market Size | $164.58 Million |

| Top Companies | Tofurky, Silk, Edensoy, Horizon Organic |

| Last Modified Date | 31 January 2026 |

Soy Based Food Market Overview

Customize Soy Based Food Market Report market research report

- ✔ Get in-depth analysis of Soy Based Food market size, growth, and forecasts.

- ✔ Understand Soy Based Food's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Soy Based Food

What is the Market Size & CAGR of Soy Based Food market in 2023?

Soy Based Food Industry Analysis

Soy Based Food Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Soy Based Food Market Analysis Report by Region

Europe Soy Based Food Market Report:

The European market for Soy Based Foods is anticipated to expand from $26.50 billion in 2023 to $43.61 billion by 2033. The consumer base in Europe is increasingly leaning towards sustainable and healthy food alternatives, further promoting the shift to soy-based ingredients. Regulations supporting the plant-based movement enhance favorable conditions for market growth across the region.Asia Pacific Soy Based Food Market Report:

The Asia Pacific region is poised for significant growth in the Soy Based Food sector, with a market size projected to increase from $19.27 billion in 2023 to $31.71 billion by 2033. The region's rich history of using soy in traditional diets, coupled with rising health awareness and Western dietary influences, contributes to this growth. Notable countries in the market include China and Japan, where soy products are deeply entrenched in culinary practices.North America Soy Based Food Market Report:

North America, with a market size projected to rise from $38.43 billion in 2023 to $63.25 billion by 2033, remains a critical market for soy-based foods. The growth is propelled by substantial consumer interest in health and fitness, along with the proliferation of plant-based diets among millennials and Gen Z. Increased availability in retail outlets and innovations in soy products are further enhancing market demand.South America Soy Based Food Market Report:

The South American Soy Based Food market is expected to grow from $6.61 billion in 2023 to $10.88 billion by 2033. Increased awareness and demand for plant-based proteins, alongside robust agricultural industries for soy cultivation, are key drivers. Countries like Brazil and Argentina are leading the charge due to their established soy farming and processing capabilities.Middle East & Africa Soy Based Food Market Report:

The Middle East and Africa region is set to grow from $9.19 billion in 2023 to $15.12 billion by 2033. Increasing urbanization, coupled with a rising interest in health and nutrition, is driving demand for soy-based products, along with a growing population that seeks alternative protein sources.Tell us your focus area and get a customized research report.

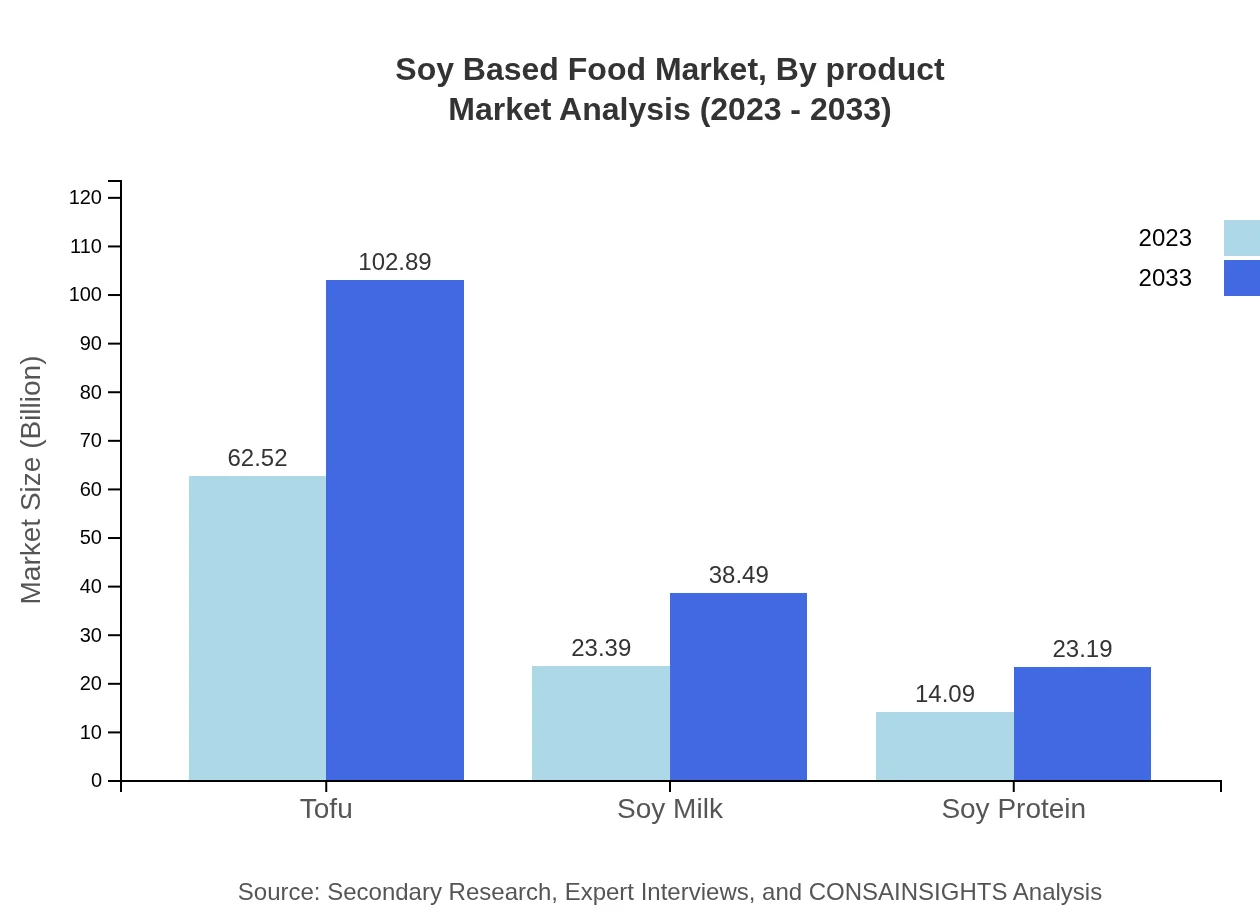

Soy Based Food Market Analysis By Product

In the Soy Based Food market, the by-product segment highlights the performance of various soy-derived products. Soy milk, expected to grow from $23.39 billion in 2023 to $38.49 billion in 2033, is gaining significant traction due to lactose intolerance in many consumers. Tofu, on the other hand, which has a projected market size from $62.52 billion to $102.89 billion in the same period, is becoming a staple protein source, particularly among vegetarians and vegans. These product categories are key contributors to the overall market performance.

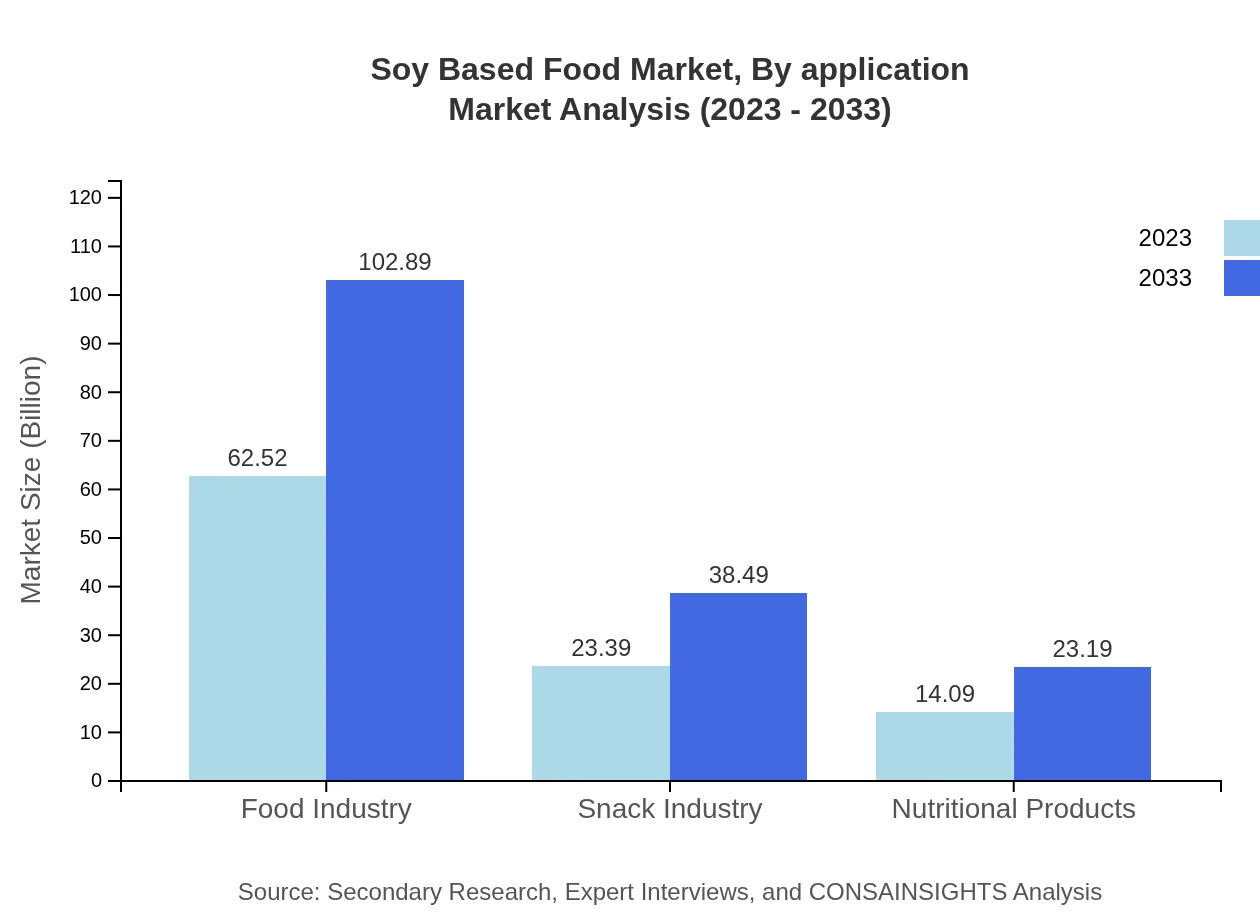

Soy Based Food Market Analysis By Application

The application of soy-based foods spans across multiple industries, with a significant share in the food industry, projected to grow from $62.52 billion in 2023 to $102.89 billion by 2033. This segment reflects the versatility of soy as both an ingredient and a meal solution. Additionally, the snack industry is also on a growth trajectory, expecting an increase from $23.39 billion to $38.49 billion in the same period as consumers look for healthier snack alternatives.

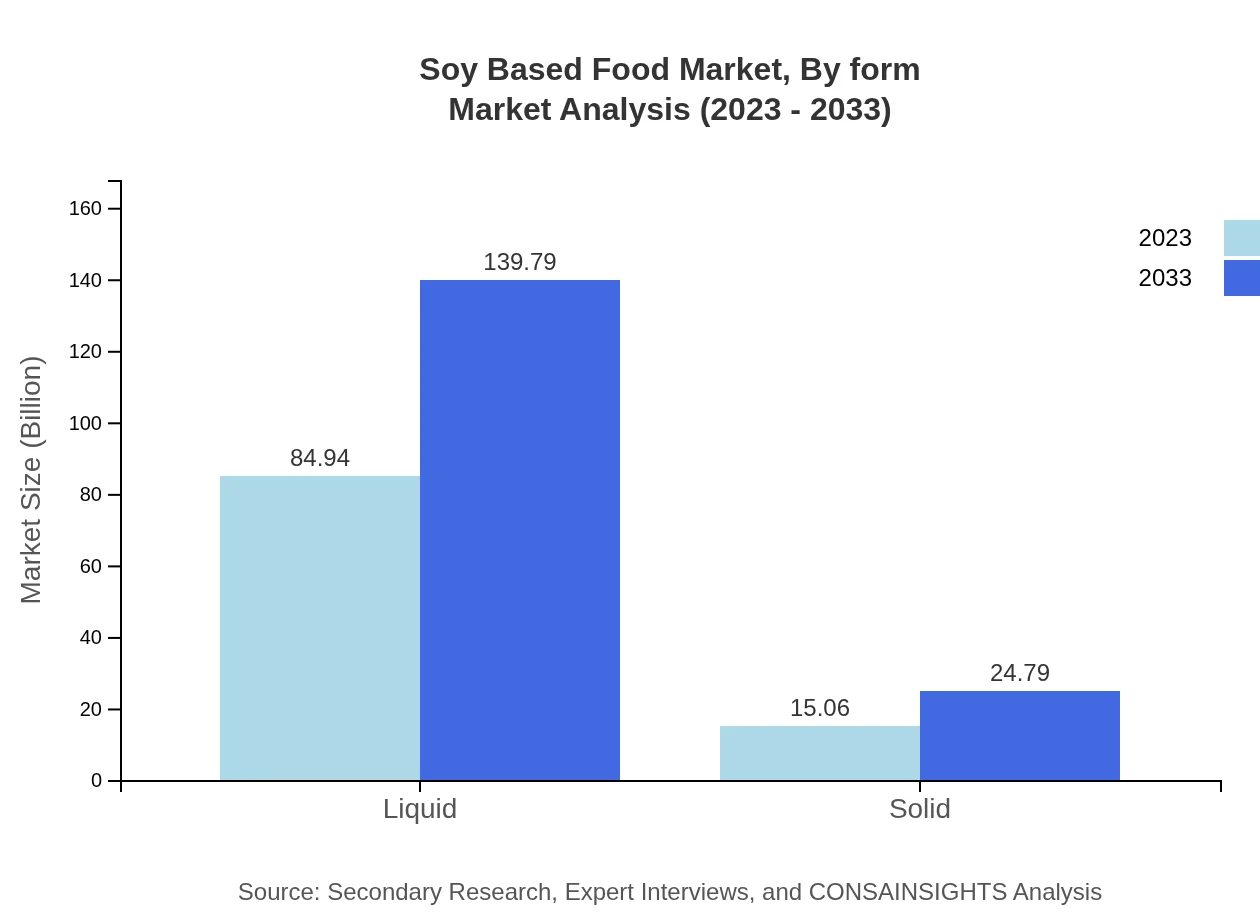

Soy Based Food Market Analysis By Form

In terms of form, the liquid segment is the leading category, with market size projected to rise from $84.94 billion in 2023 to $139.79 billion by 2033. The solid segment is also notable, with a rise from $15.06 billion to $24.79 billion, showing that there is an enduring preference for both liquid and solid forms of soy-based food products across diverse consumer bases.

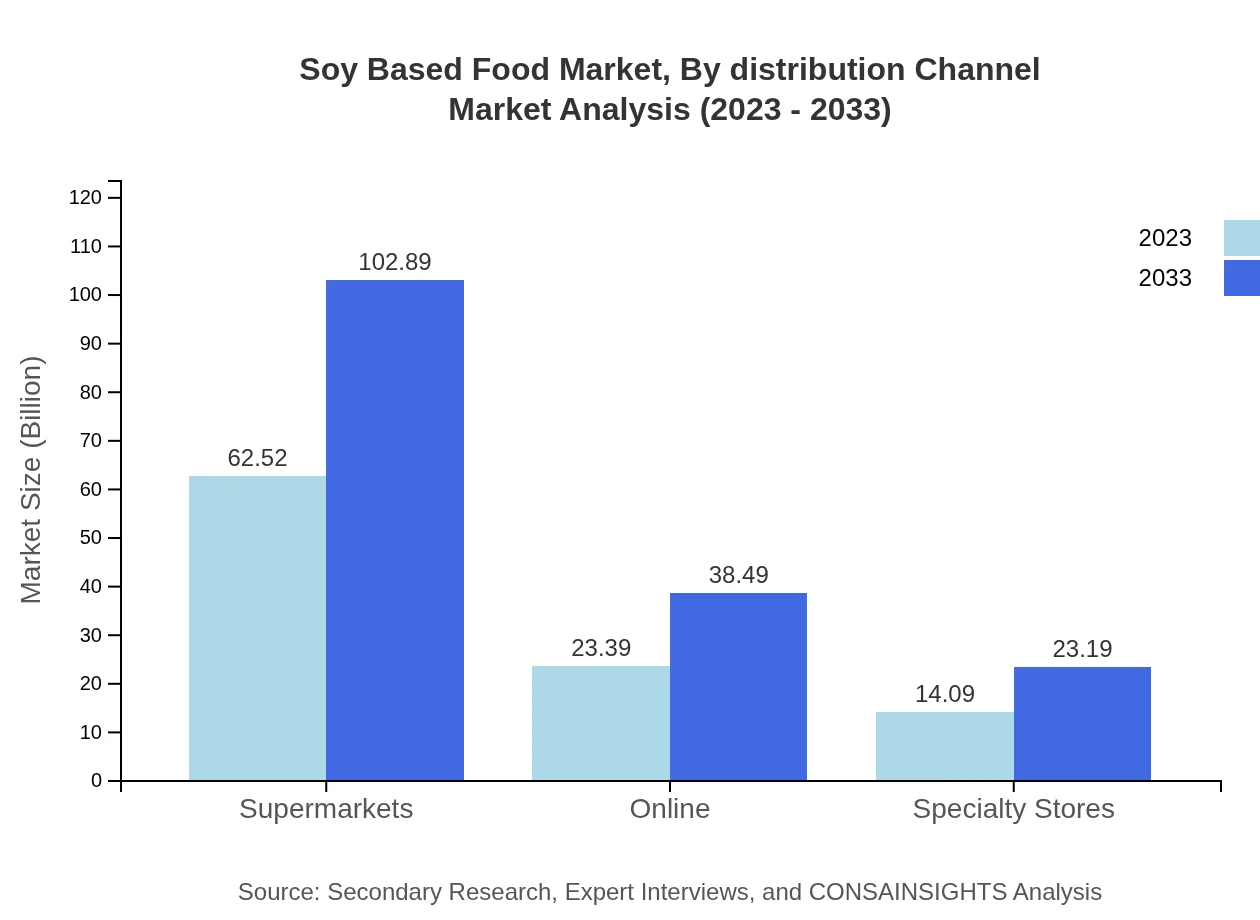

Soy Based Food Market Analysis By Distribution Channel

The distribution of soy-based foods is primarily through supermarkets, projected to grow significantly from $62.52 billion to $102.89 billion by 2033. Online distribution channels are also gaining momentum, with growth from $23.39 billion to $38.49 billion, reflecting changing shopping behaviors and the increase in demand for convenient shopping solutions for health-conscious consumers.

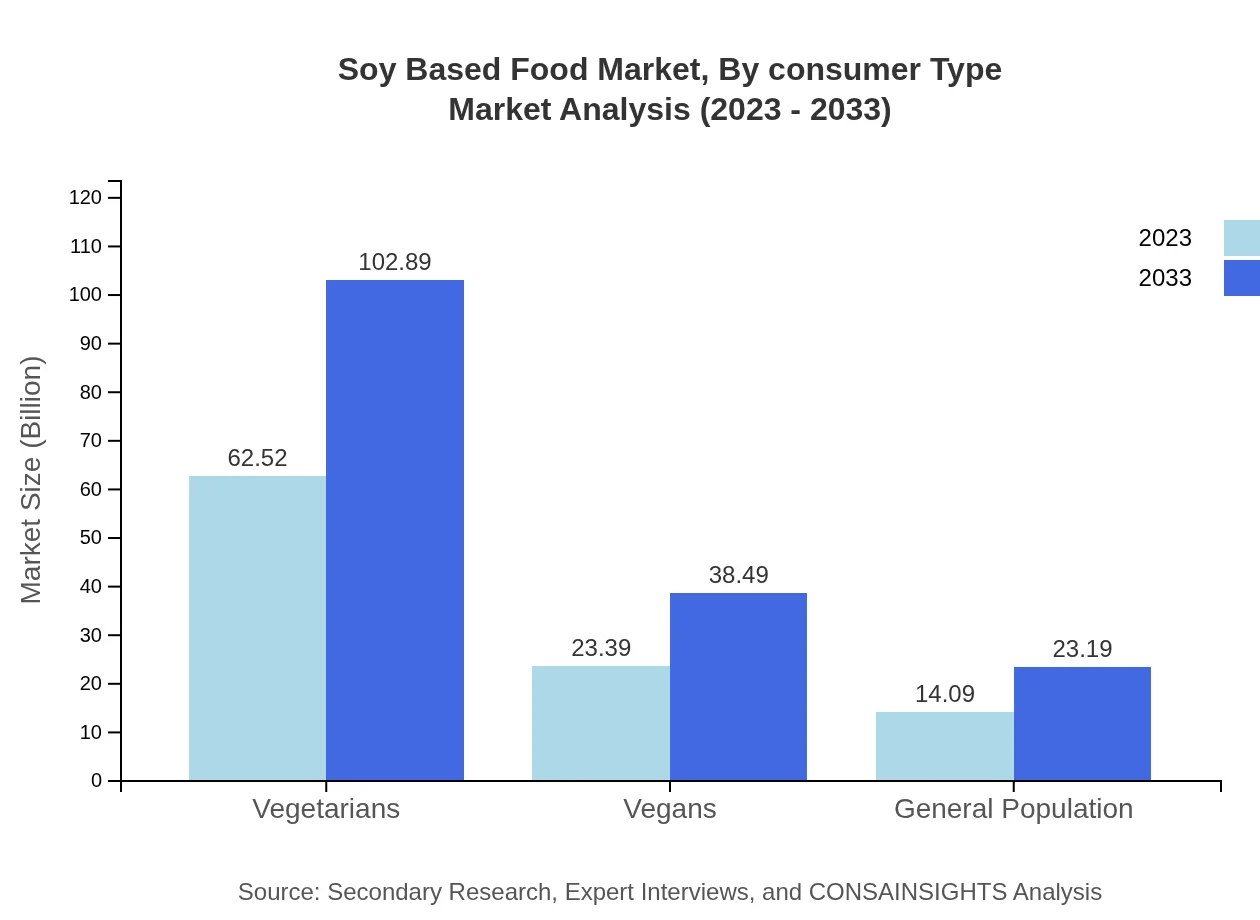

Soy Based Food Market Analysis By Consumer Type

The consumer base for soy-based foods includes vegetarians, vegans, and the general population, each representing unique market segments. The vegetarian segment has a significant forecast growth from $62.52 billion to $102.89 billion by 2033, whereas the vegan segment is expected to expand from $23.39 billion to $38.49 billion, showcasing the increasing interest in plant-based diets among these groups.

Soy Based Food Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Soy Based Food Industry

Tofurky:

Tofurky is a leading company in plant-based soy food products, renowned for its innovative tofu and tempeh-based offerings, serving both vegetarian and vegan consumers while emphasizing sustainability.Silk:

Silk is a prominent brand specializing in soy milk and dairy alternatives, highly recognized for its quality and variety, contributing significantly to the growing consumption of soy-based beverages in North America.Edensoy:

Edensoy is known for producing high-quality organic soy milk products, gaining a solid customer base among health-conscious consumers looking for nutritious plant-based options.Horizon Organic:

Horizon Organic focuses on organic dairy and soy alternatives, promoting sustainable farming practices and a commitment to quality that attracts environmentally conscious consumers.We're grateful to work with incredible clients.

FAQs

What is the market size of soy Based food?

The soy-based food market has a base market size of $100 million, with a projected compound annual growth rate (CAGR) of 5%. This indicates robust growth potential in the sector moving toward the future, particularly by 2033.

What are the key market players or companies in the soy Based food industry?

Key players in the soy-based food industry include prominent manufacturers and brands focusing on diverse soy products. These companies actively drive innovation and marketing, ensuring their products cater to rising consumer demand for plant-based alternatives.

What are the primary factors driving the growth in the soy Based food industry?

The growth of the soy-based food industry is primarily driven by increasing health consciousness among consumers, rising plant-based diets, and a growing trend towards sustainable and environmentally-friendly food options, which soy products readily offer.

Which region is the fastest Growing in the soy Based food market?

The fastest-growing region in the soy-based food market is North America, with a projected market size increase from $38.43 million in 2023 to approximately $63.25 million by 2033, reflecting significant consumer adoption of plant-based diets.

Does ConsaInsights provide customized market report data for the soy Based food industry?

Yes, ConsaInsights offers customized market report data for the soy-based food industry. Clients can receive tailored insights and analyses specific to their needs and interests, aiding strategic decision-making.

What deliverables can I expect from this soy Based food market research project?

From the soy-based food market research project, clients can expect comprehensive deliverables that include data analysis, market forecasts, competitive insights, regional breakdowns, and segment-wise evaluations to support informed business strategies.

What are the market trends of soy Based food?

Current market trends in the soy-based food industry show a rise in demand for soy milk, tofu, and other soy products, driven by increased vegetarianism/veganism and health awareness, along with trends favoring sustainability and ethical consumption.