Sternal Closure Systems Market Report

First published: 12 October 2024 | Last updated: 28 May 2026 | Report Code: sternal-closure-systems

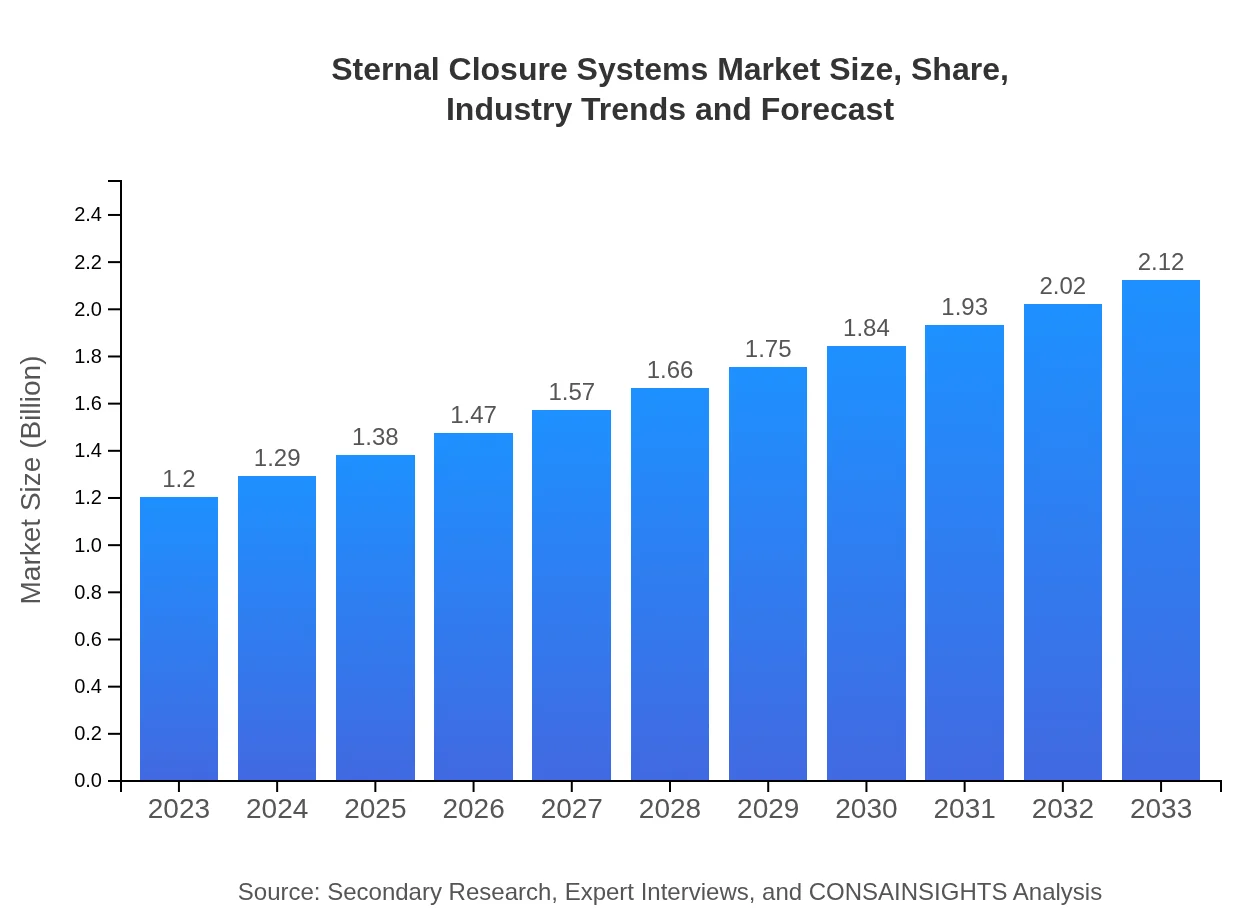

Sternal Closure Systems Market — USD 1.2 billion in 2023, Growing to USD 2.12B by 2033 at 5.7% CAGR

This report analyzes the Sternal Closure Systems market, providing insights into market size, trends, and forecasts from 2023 to 2033. It highlights segmentation, regional analysis, competitive landscape, and future trends that shape the industry landscape.

Key Takeaways

- Global market value grows from $1.20 Billion in 2023 to $2.12 Billion in 2033, with a 5.7% CAGR over 2023 to 2033.

- Europe is largest regional market; Latin America is regional market region based on implied CAGR across 2023 to 2033.

- Latin America is identified as the regional market region, rising from $0.03 Billion in 2023 to $0.06 Billion in 2033.

- North America moves from $0.4 Billion in 2023 to $0.71 Billion in 2033, reflecting sustained demand in clinical settings.

- Materials, technology advances, and expanding surgical volumes underpin adoption; key players include Medtronic, Boston Scientific, Stryker, and Zimmer Biomet.

Sternal Closure Systems Market Report — Executive Summary

Regional analysis shows Europe as largest market and Latin America as fastest-growing region by implied CAGR. This report examines the Sternal Closure Systems market, which stood at $1.20 Billion in 2023 and is projected to reach $2.12 Billion by 2033 at a 5.7% CAGR for 2023 to 2033. Growth is driven by rising surgical volumes, technological improvements in fixation methods, and broader adoption of advanced biomaterials. Regional performance varies: Europe is the largest market, while Latin America shows the highest growth rate. The analysis covers product types such as wires, plates, and devices; applications including cardiac, trauma, and reconstruction surgery; end-users like hospitals and ambulatory surgery centers; and materials and technique categories. Competitive activity centers on clinical validation and product innovation, with Medtronic, Boston Scientific, Stryker, and Zimmer Biomet actively investing in new offerings. The study uses primary expert interviews and secondary company and publication data, combined with triangulation and internal validation, to present an evidence-based outlook and actionable insights for stakeholders.

Key Growth Drivers

- Increasing number of cardiac and thoracic surgical procedures raising demand for reliable sternal fixation.

- Advances in biomaterials and fixation technologies improving patient outcomes and procedural options.

- Greater adoption of minimally invasive approaches driving interest in innovative closure systems.

- Hospital and surgical center investments in surgical infrastructure supporting product uptake.

- Vendor R&D activity and clinical evidence generation enhancing adoption across key markets.

Sternal Closure Systems Market Overview

Customize Sternal Closure Systems Market Report market research report

- ✔ Get in-depth analysis of Sternal Closure Systems market size, growth, and forecasts.

- ✔ Understand Sternal Closure Systems's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Sternal Closure Systems

What is the Market Size & CAGR of Sternal Closure Systems Market Report market in 2023?

Sternal Closure Systems Industry Analysis

Sternal Closure Systems Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Sternal Closure Systems Market Report Market Analysis Report by Region

Europe Sternal Closure Systems Market Report:

Europe is largest regional market, rising from $0.4 Billion in 2023 to $0.71 Billion in 2033. 4 Billion in 2023 to $0.71 Billion in 2033, making it the largest regional market. Drivers include mature healthcare infrastructure, rising procedural rates, and uptake of advanced fixation methods and biomaterials.Asia Pacific Sternal Closure Systems Market Report:

Asia Pacific grows from $0.21 Billion in 2023 to $0.38 Billion in 2033. Growth stems from expanding access to surgical care, growing clinical capacity, and gradual adoption of newer closure technologies in key healthcare centers.North America Sternal Closure Systems Market Report:

North America grows from $0.4 Billion in 2023 to $0.71 Billion in 2033. The region's trajectory reflects sustained surgical volumes, established hospital systems, and ongoing investments in procedural technology and device adoption that support demand.South America Sternal Closure Systems Market Report:

Latin America is fastest-growing region by implied CAGR, increasing from $0.03 Billion in 2023 to $0.06 Billion in 2033. 03 Billion in 2023 to $0.06 Billion in 2033 and is identified as the regional growth market at an implied 7.18% CAGR, supported by improving healthcare access and increasing surgical procedure volumes.Middle East & Africa Sternal Closure Systems Market Report:

Middle East and Africa grows from $0.15 Billion in 2023 to $0.26 Billion in 2033. 15 Billion in 2023 to $0.26 Billion in 2033, with growth linked to investments in hospital infrastructure, rising prevalence of surgical interventions, and adoption of better fixation solutions.Tell us your focus area and get a customized research report.

Research Methodology

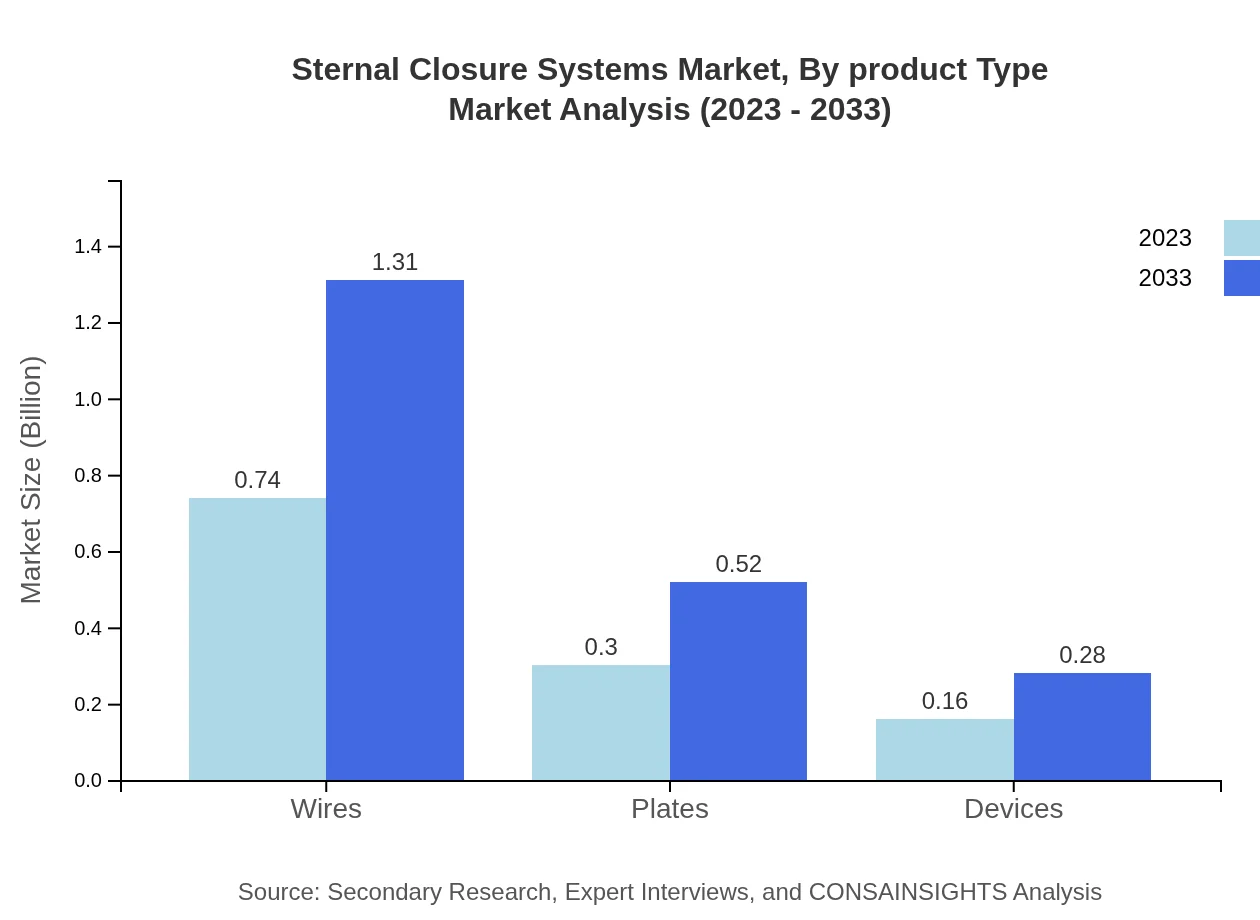

Sternal Closure Systems Market Analysis By Product Type

The segmentations by product type include Wires (2023 market: $0.74, 2033 market: $1.31), Plates (2023 market: $0.30, 2033 market: $0.52), and Devices (2023 market: $0.16, 2033 market: $0.28). Wires constitute the largest share within the market, signing their importance in surgical practice.

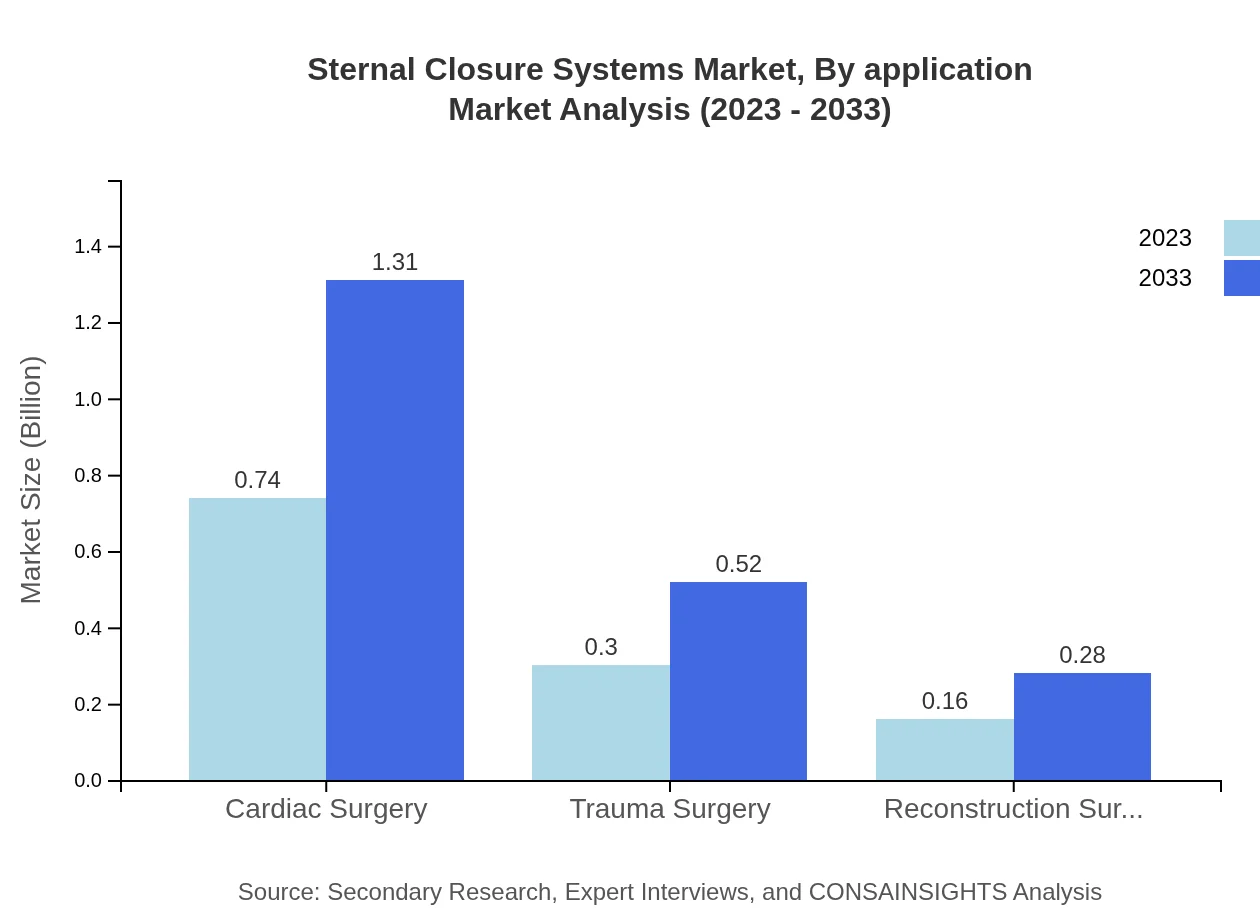

Sternal Closure Systems Market Analysis By Application

The market is divided into applications such as Cardiac Surgery (2023 market: $0.74, 2033 market: $1.31), Trauma Surgery (2023 market: $0.30, 2033 market: $0.52), and Reconstruction Surgery (2023 market: $0.16, 2033 market: $0.28). Cardiac surgery remains dominant due to the high volume of procedures.

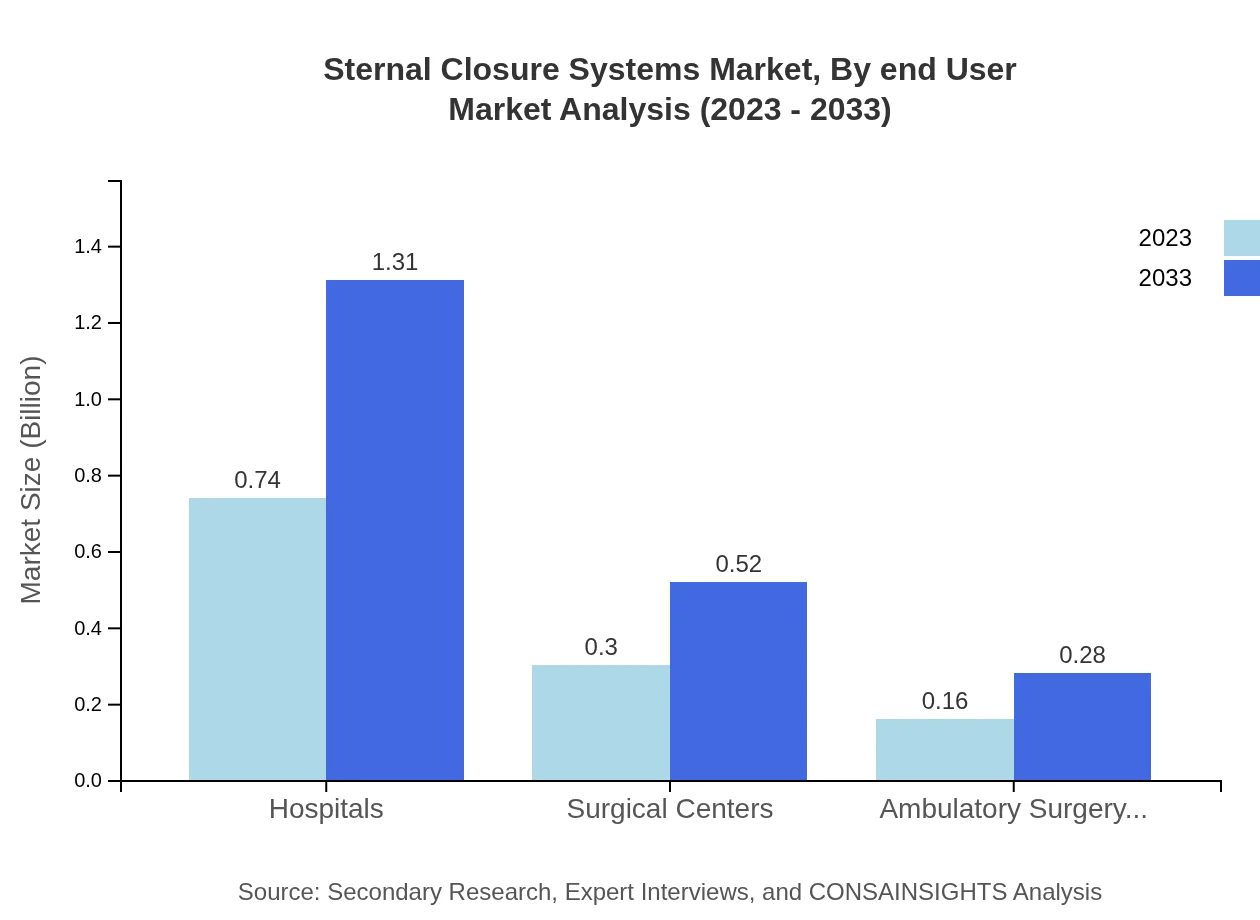

Sternal Closure Systems Market Analysis By End User

Key end-user segments include Hospitals (2023 market: $0.74, 2033 market: $1.31), Surgical Centers (2023 market: $0.30, 2033 market: $0.52), and Ambulatory Surgery Centers (2023 market: $0.16, 2033 market: $0.28). Hospitals continue to account for the majority of market share.

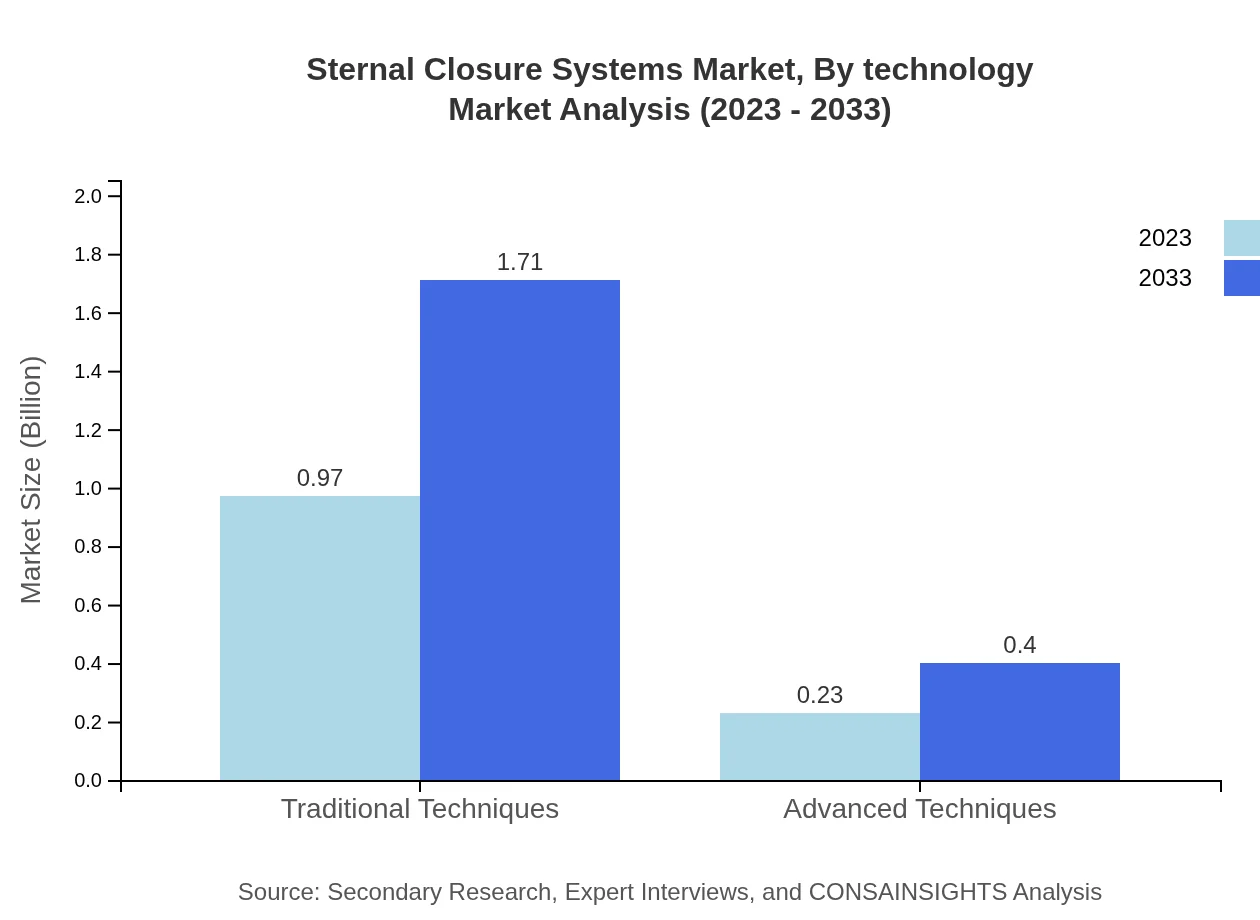

Sternal Closure Systems Market Analysis By Technology

Technological approaches include Traditional Techniques (2023 market: $0.97, 2033 market: $1.71) and Advanced Techniques (2023 market: $0.23, 2033 market: $0.40). Traditional techniques dominate, but advanced techniques are gradually gaining traction.

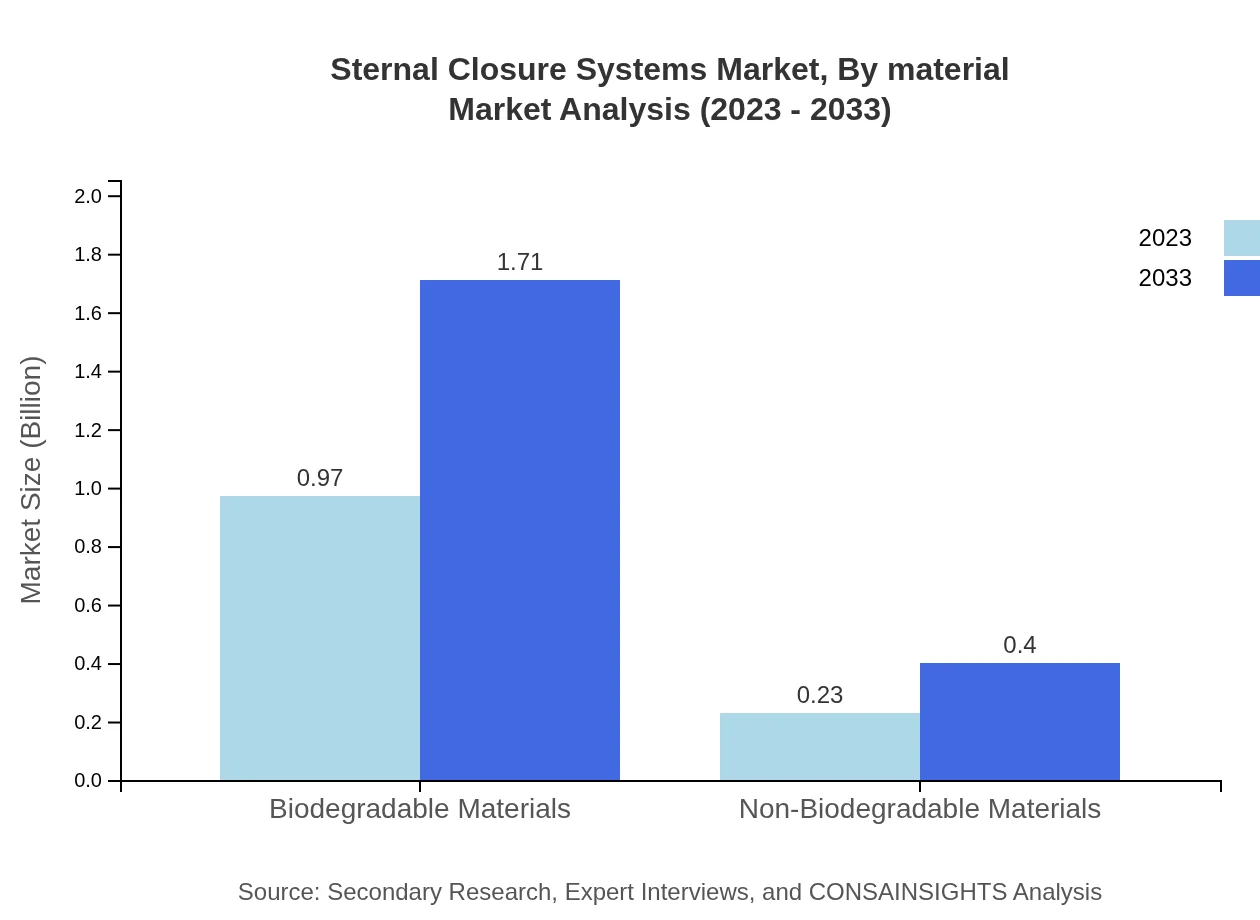

Sternal Closure Systems Market Analysis By Material

Material segmentation includes Biodegradable Materials (2023 market: $0.97, 2033 market: $1.71) and Non-Biodegradable Materials (2023 market: $0.23, 2033 market: $0.40). Biodegradable options are increasingly favored due to their benefits in post-surgical recovery.

Sternal Closure Systems Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Sternal Closure Systems Industry

Medtronic :

A global leader in medical technologies, Medtronic provides innovative sternal closure solutions, emphasizing improved patient outcomes and surgical efficiency.Boston Scientific:

Boston Scientific develops advanced devices for sternal closure and is focused on innovative technologies to enhance cardiac surgery performance.Stryker :

Stryker is renowned for its range of surgical products, including sternal closure systems, supporting more effective and safer surgical procedures.Zimmer Biomet:

Zimmer Biomet focuses on innovative orthopedic and surgical solutions, including advanced sternal closure products that enhance surgical performance.We're grateful to work with incredible clients.

FAQs

What is the market size of the Sternal Closure Systems Market Report in 2023?

The market size in 2023 is $1.20 Billion, as stated in the report data provided for the 2023 baseline year.

How big is the market expected to be in 2033?

The market is projected to reach $2.12 Billion by 2033 according to the supplied forecast figures.

What is CAGR for the forecast period?

The compound annual growth rate for the 2023 to 2033 forecast period is 5.7% as provided in the input dataset.

Which region is the fastest Growing in the Sternal Closure Systems Market Report market?

Latin America is the fastest-growing region, projected to expand from $0.03 Billion in 2023 to $0.06 Billion in 2033, reflecting an implied 7.18% CAGR over the forecast period.

Which region is the fastest Growing?

Latin America is described as the regional market region, rising from $0.03 Billion in 2023 to $0.06 Billion in 2033 at an implied 7.18% CAGR.

Who are the top companies in this market?

Top companies listed include Medtronic, Boston Scientific, Stryker, and Zimmer Biomet as key participants in the competitive landscape.

What product types are covered in the segmentation?

Product-type segmentation includes wires, plates, and devices, as specified in the provided segment facts.

What end User categories are included?

End-users covered are hospitals, surgical centers, and ambulatory surgery centers according to the supplied segmentation data.

How are technologies categorized in the report?

Technologies are split into traditional techniques and advanced techniques, based on the explicit sub-segment listing supplied.

What materials are considered in the analysis?

Materials sub-segments include biodegradable materials and non-biodegradable materials as provided in the input.