Reports >

Life Sciences

>

Teleradiology Market Report

Teleradiology Market Report

First published: 08 October 2024 | Last updated: 28 May 2026 | Report Code: teleradiology

Teleradiology Market — USD 10.3 billion in 2023, Growing to USD 35.82B by 2033 at 12.7% CAGR

This report provides a comprehensive analysis of the Teleradiology market, exploring current trends, growth projections, and market dynamics from 2023 to 2033. Valuable insights on regional performances and leading players in the industry are also discussed.

Key Takeaways

- Global market expands from $10.30 Billion in 2023 to $35.82 Billion in 2033 at a 12.7% CAGR.

- North America is largest regional market, while no single fastest-growing region is stated because regional CAGR differences remain within 0.15 percentage points.

- Cloud-based solutions and artificial intelligence are core technological enablers in service delivery and workflow efficiency.

- Hospitals, diagnostic centers, research institutes and home care settings are key end-user segments driving demand.

- Top providers referenced include Radiology Partners, vRad (Virtual Radiologic), and Telemedicine Clinic.

Teleradiology Market Report — Executive Summary

North America remains largest market by forecast-period value, while no single fastest-growing region is stated because top regional growth rates are separated by less than 0.15 percentage points. The Teleradiology Market Report examines market growth driven by rising demand for remote image interpretation and improvements in digital transmission. Adoption is supported by cloud-based solutions and artificial intelligence that streamline workflows, alongside demographic pressures such as an aging population and increased chronic disease prevalence. Service models include transmission, interpretation and consultation, delivered across hospitals, diagnostic centers, research institutes and home care settings. Regionally, North America is the largest market. The competitive field features Radiology Partners, vRad (Virtual Radiologic), and Telemedicine Clinic. The analysis uses primary interviews and secondary sources to validate market trajectories and to outline strategic priorities for technology providers, healthcare organizations and investors.

Key Growth Drivers

- Expansion of cloud-based platforms enabling remote image storage and access across facilities.

- Integration of artificial intelligence to accelerate and standardize image interpretation workflows.

- Increasing prevalence of chronic conditions and an aging patient base requiring frequent diagnostic imaging.

- Rising need for improved diagnostic access in underserved and remote areas.

- Shift toward telehealth models that prioritize rapid, cost-effective diagnostic services.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $10.30 Billion |

| CAGR (2023-2033) | 12.7% |

| 2033 Market Size | $35.82 Billion |

| Top Companies | Radiology Partners, vRad (Virtual Radiologic), Telemedicine Clinic |

| Published Date | 08 October 2024 |

| Last Modified Date | 28 May 2026 |

Teleradiology Market Overview

Customize Teleradiology Market Report market research report

- ✔ Get in-depth analysis of Teleradiology market size, growth, and forecasts.

- ✔ Understand Teleradiology's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Teleradiology

What is the Market Size & CAGR of Teleradiology Market Report market in 2023?

Teleradiology Industry Analysis

Teleradiology Market Segmentation and Scope

Tell us your focus area and get a customized research report.

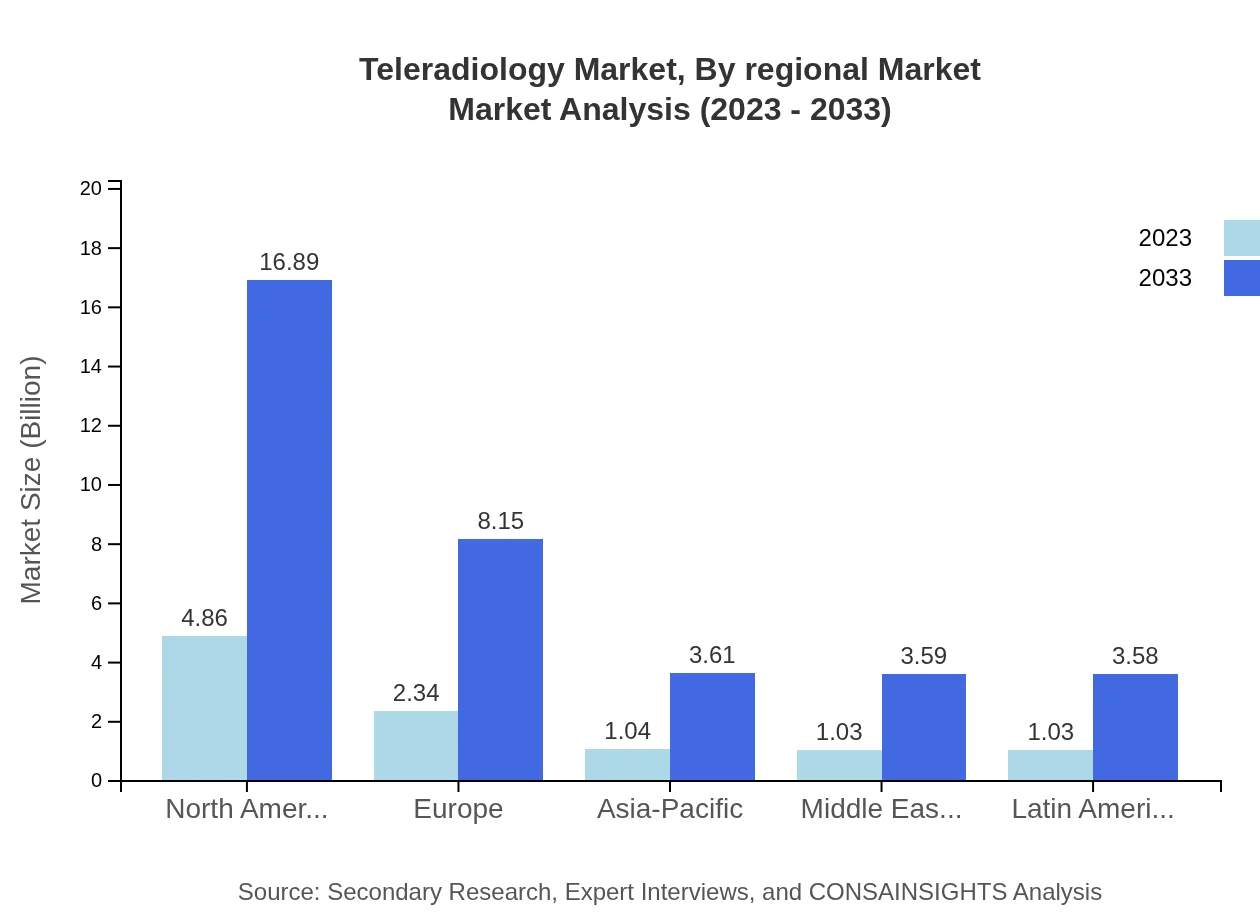

Teleradiology Market Report Market Analysis Report by Region

Europe Teleradiology Market Report:

Europe grows from $2.94 Billion in 2023 to $10.22 Billion in 2033. Adoption is supported by digitization of imaging workflows, telehealth policy developments, and increasing integration of cloud-based and AI-enabled solutions in clinical settings.Asia Pacific Teleradiology Market Report:

Asia Pacific grows from $2 Billion in 2023 to $6.95 Billion in 2033. Market expansion reflects rising demand for diagnostic imaging, efforts to extend specialist radiology access to remote areas, and growing deployment of cloud and AI tools.North America Teleradiology Market Report:

North America is largest regional market, rising from $3.4 Billion in 2023 to $11.82 Billion in 2033. Regional demand is underpinned by established healthcare infrastructure, broad telehealth adoption, and investments in cloud and AI technologies that support remote imaging services.South America Teleradiology Market Report:

Latin America grows from $0.94 Billion in 2023 to $3.27 Billion in 2033. Growth is driven by initiatives to enhance healthcare access in underserved regions, greater telemedicine uptake, and the gradual modernization of imaging infrastructure.Middle East & Africa Teleradiology Market Report:

Middle East and Africa grows from $1.02 Billion in 2023 to $3.55 Billion in 2033. Regional drivers include investments to improve diagnostic capacity, telehealth adoption to reach remote populations, and the rollout of cloud-enabled imaging platforms.Tell us your focus area and get a customized research report.

Research Methodology

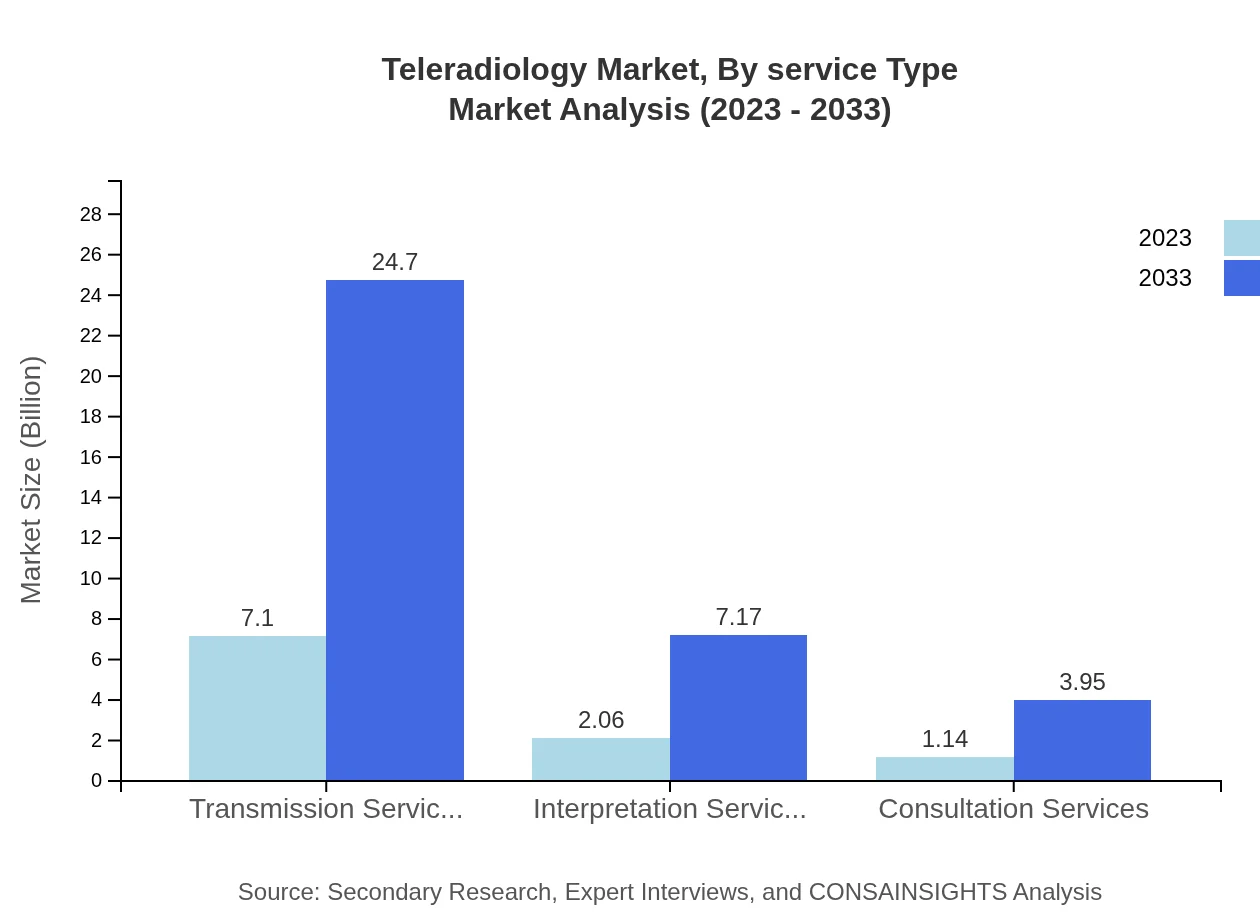

Teleradiology Market Analysis By Service Type

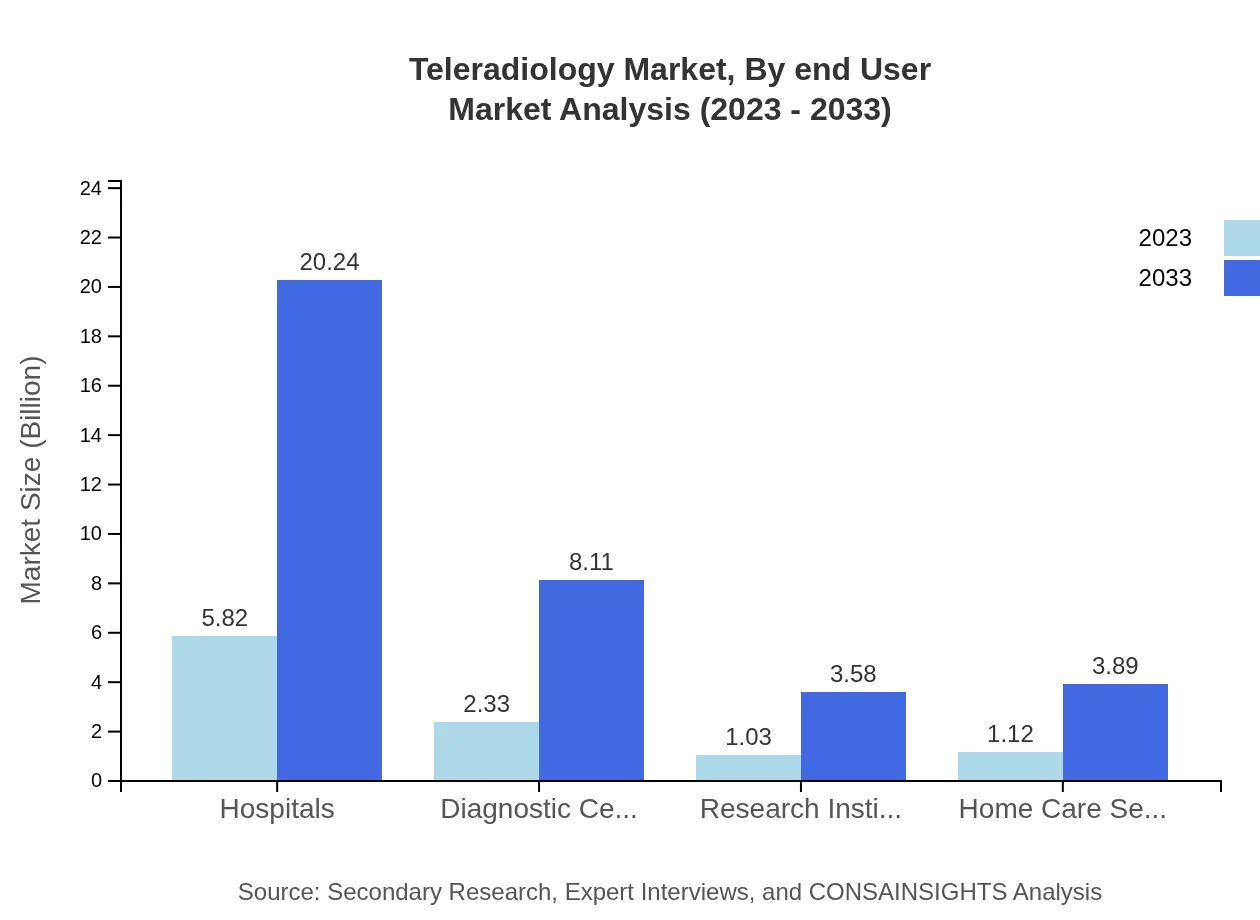

The Teleradiology market by service type includes Hospitals, Diagnostic Centers, Research Institutes, and Home Care Settings. Hospitals dominate this segment, representing $5.82 billion in 2023 and projected to grow to $20.24 billion by 2033. Diagnostic Centers also show strong performance with a market value of $2.33 billion in 2023 and expected growth to $8.11 billion in 2033.

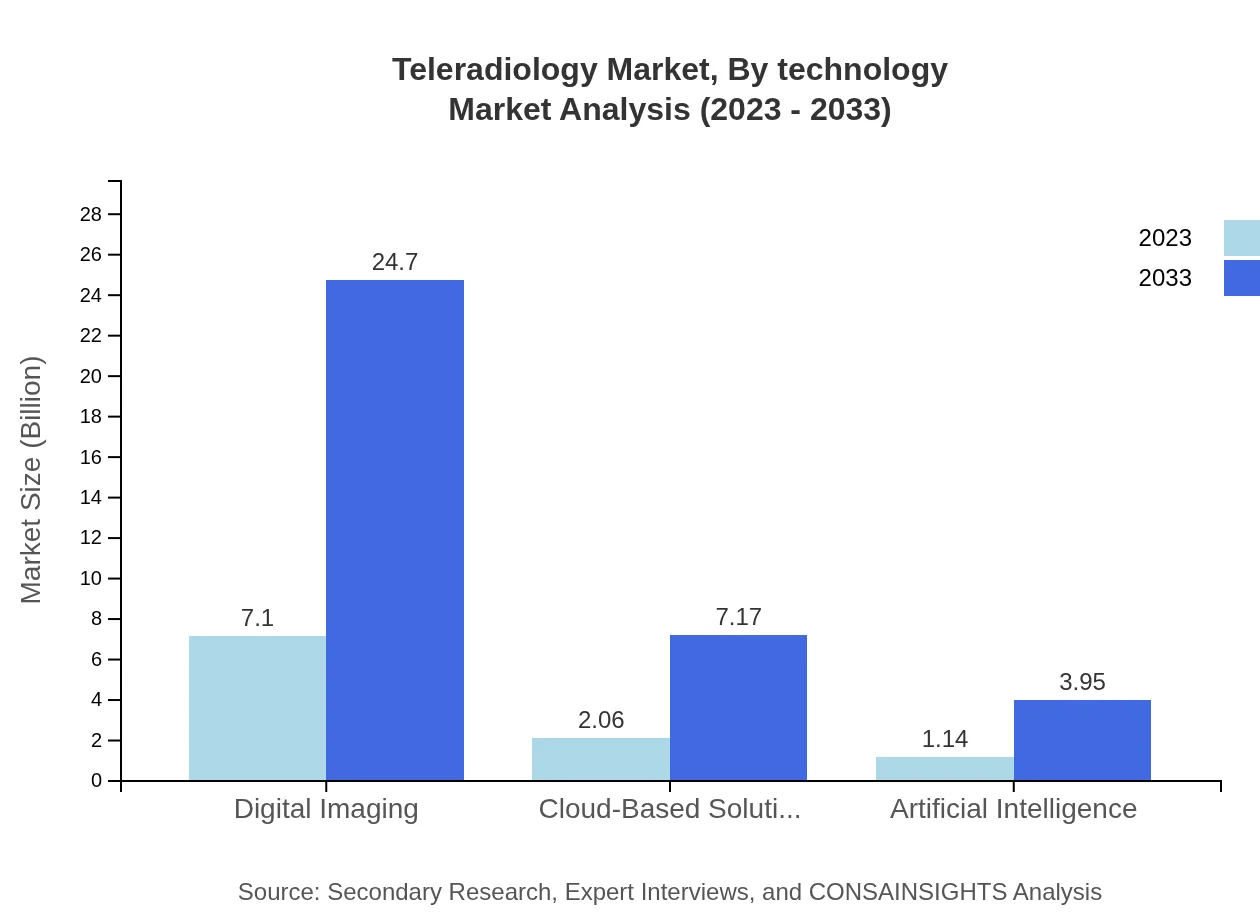

Teleradiology Market Analysis By Technology

The technology segment features Digital Imaging, Cloud-Based Solutions, and Artificial Intelligence. Digital Imaging leads with a market size of $7.10 billion in 2023, projected to reach $24.70 billion by 2033. Cloud-Based Solutions and Artificial Intelligence are also vital, with respective valuations of $2.06 billion and $1.14 billion in 2023, expanding significantly by 2033.

Teleradiology Market Analysis By End User

End-user segmentation reflects the distribution of Teleradiology services across sectors such as hospitals and research institutes. Hospitals represent a significant market share of 56.52% in 2023. Research Institutes are emerging entities with a consistent share of 10%.

Teleradiology Market Analysis By Regional Market

This section evaluates the Teleradiology market from regional perspectives, showcasing unique growth dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. North America leads with an approximate size of $4.86 billion in 2023, while Asia-Pacific is growing at a rapid pace, demonstrating a market increase from $1.04 billion to $3.61 billion by 2033.

Teleradiology Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Teleradiology Industry

Radiology Partners:

Radiology Partners is a leading teleradiology provider in the United States, focusing on improving the quality of imaging services and enhancing patient care through innovative technology.vRad (Virtual Radiologic):

vRad is a prominent teleradiology service provider known for its advanced imaging technology and a large team of board-certified radiologists, offering services to healthcare providers across the United States.Telemedicine Clinic:

Telemedicine Clinic specializes in providing remote diagnostic services, connecting patients with certified specialists through their platform, significantly improving healthcare access.We're grateful to work with incredible clients.

FAQs

What is the market size of the Teleradiology market in 2023?

The market size in 2023 is $10.30 Billion, as reported for the global Teleradiology market in the provided dataset.

How big will the Teleradiology market be in 2033?

The market is projected to reach $35.82 Billion by 2033 according to the input data covering the forecast period 2023 to 2033.

What is CAGR of the market during 2023 to 2033?

The compound annual growth rate for the market spanning 2023 to 2033 is 12.7%, based on the provided forecast figures.

Is there a single fastest Growing region in the Teleradiology Market Report market?

No single fastest-growing region is stated for the Teleradiology Market Report market because the top regional implied CAGR values are within 0.15 percentage points of each other, making the ranking too close to call reliably.

Which companies are noted as leading participants?

Top companies listed include Radiology Partners, vRad (Virtual Radiologic), and Telemedicine Clinic in the supplied report information.

What end User segments are covered in the analysis?

End-user categories include Hospitals, Diagnostic Centers, Research Institutes, and Home Care Settings, as specified among the report’s subsegments.

What technology categories are highlighted?

Technology subsegments noted are Digital Imaging, Cloud-Based Solutions, and Artificial Intelligence within the supplied segment list.

How are services categorized in the report?

Service types are Transmission Services, Interpretation Services, and Consultation Services as enumerated in the input segment facts.