Reports >

Life Sciences

>

Trauma Products Market Report

Trauma Products Market Report

Published Date: 31 January 2026 | Report Code: trauma-products

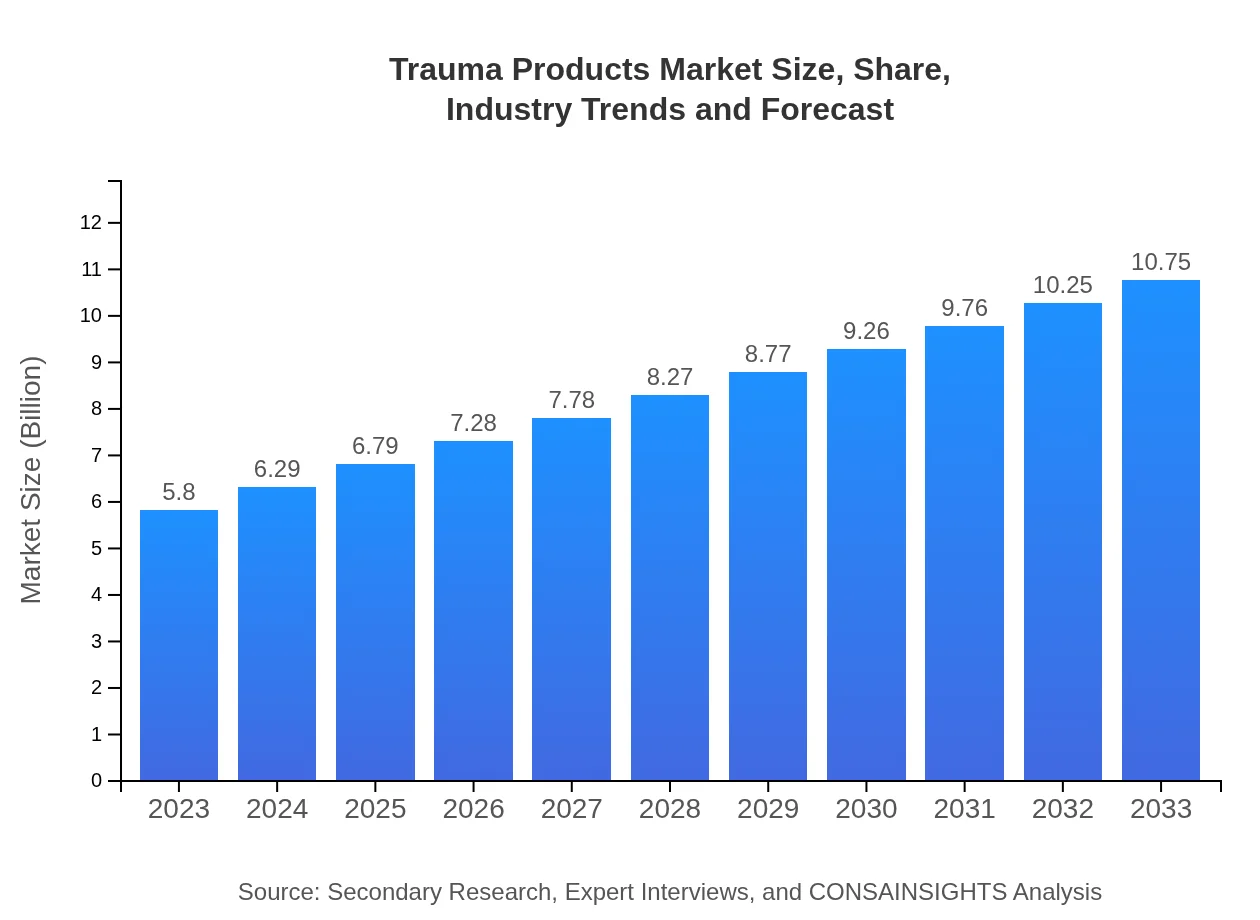

Trauma Products Market Size, Share, Industry Trends and Forecast to 2033

This report provides an in-depth analysis of the Trauma Products market from 2023 to 2033, covering market size, growth forecasts, industry trends, and segmentation insights across various regions and applications.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.80 Billion |

| CAGR (2023-2033) | 6.2% |

| 2033 Market Size | $10.75 Billion |

| Top Companies | Johnson & Johnson, Medtronic , Stryker Corporation |

| Last Modified Date | 31 January 2026 |

Trauma Products Market Overview

Customize Trauma Products Market Report market research report

- ✔ Get in-depth analysis of Trauma Products market size, growth, and forecasts.

- ✔ Understand Trauma Products's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Trauma Products

What is the Market Size & CAGR of Trauma Products market in 2023?

Trauma Products Industry Analysis

Trauma Products Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Trauma Products Market Analysis Report by Region

Europe Trauma Products Market Report:

The European market valued at $1.40 billion in 2023 is expected to grow to $2.60 billion by 2033. The presence of advanced healthcare technologies and supportive government policies related to health and safety standards contribute to this growth.Asia Pacific Trauma Products Market Report:

In the Asia Pacific region, the Trauma Products market was valued at $1.22 billion in 2023, with projections indicating a growth to $2.25 billion by 2033. Factors contributing to this growth include increasing vehicular accidents and advancements in healthcare infrastructures.North America Trauma Products Market Report:

North America holds a significant portion of the market, valued at $2.09 billion in 2023 and expected to increase to $3.87 billion by 2033. High prevalence of sports injuries and an aging population are significant factors driving this region's growth.South America Trauma Products Market Report:

The South American market was valued at $0.33 billion in 2023 and is projected to reach $0.62 billion by 2033. Limited healthcare access and economic challenges remain key barriers but improvements in urban healthcare services are driving gradual growth.Middle East & Africa Trauma Products Market Report:

The Middle East and Africa market is projected to grow from $0.76 billion in 2023 to $1.41 billion by 2033. War and conflict-related injuries, alongside improvements in healthcare provision, especially in urban centers, are central to this expansion.Tell us your focus area and get a customized research report.

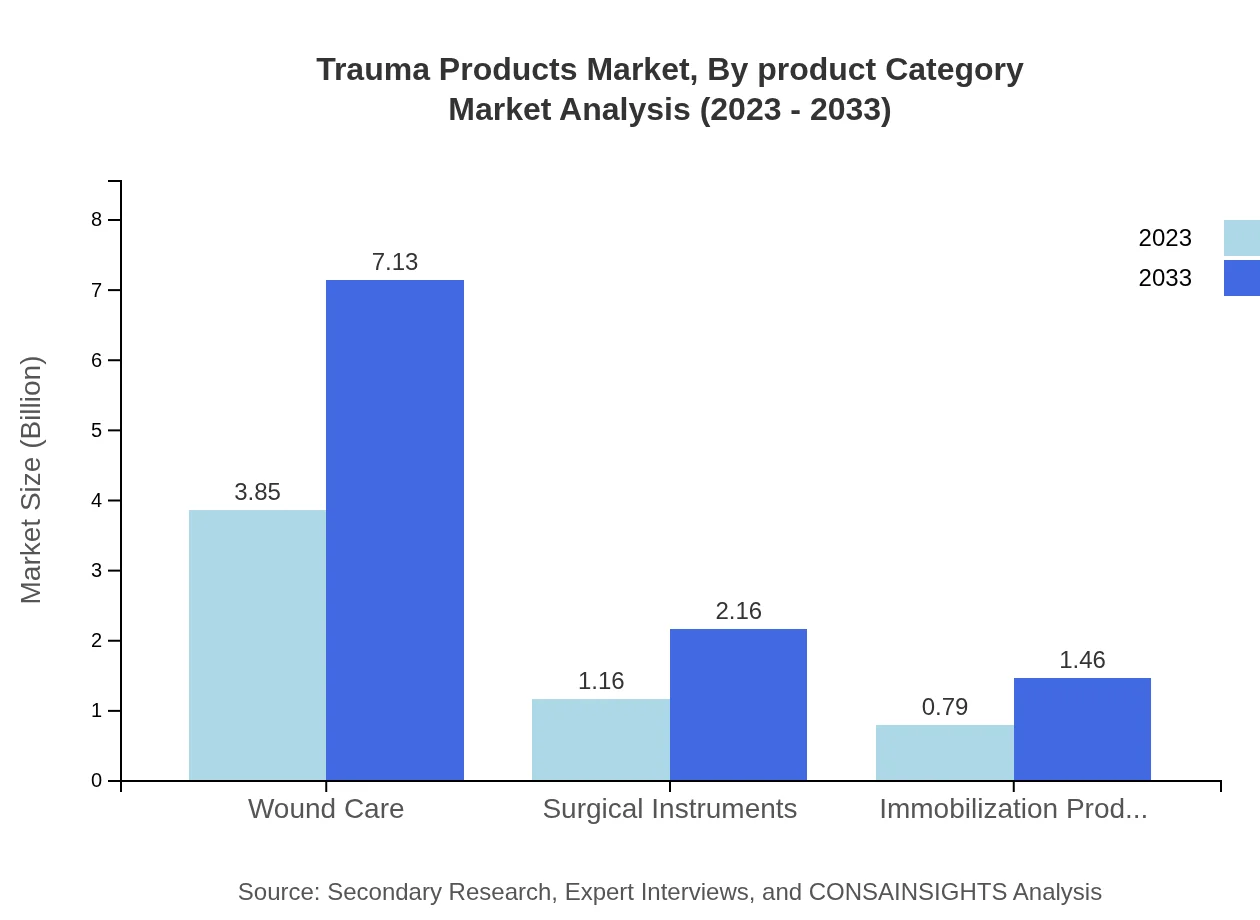

Trauma Products Market Analysis By Product Category

The Trauma Products market, by product category, showcases significant growth in supplies such as surgical instruments and immobilization products. In 2023, surgical instruments accounted for a market size of $1.16 billion, expected to reach $2.16 billion by 2033, driven by increased surgical procedures globally.

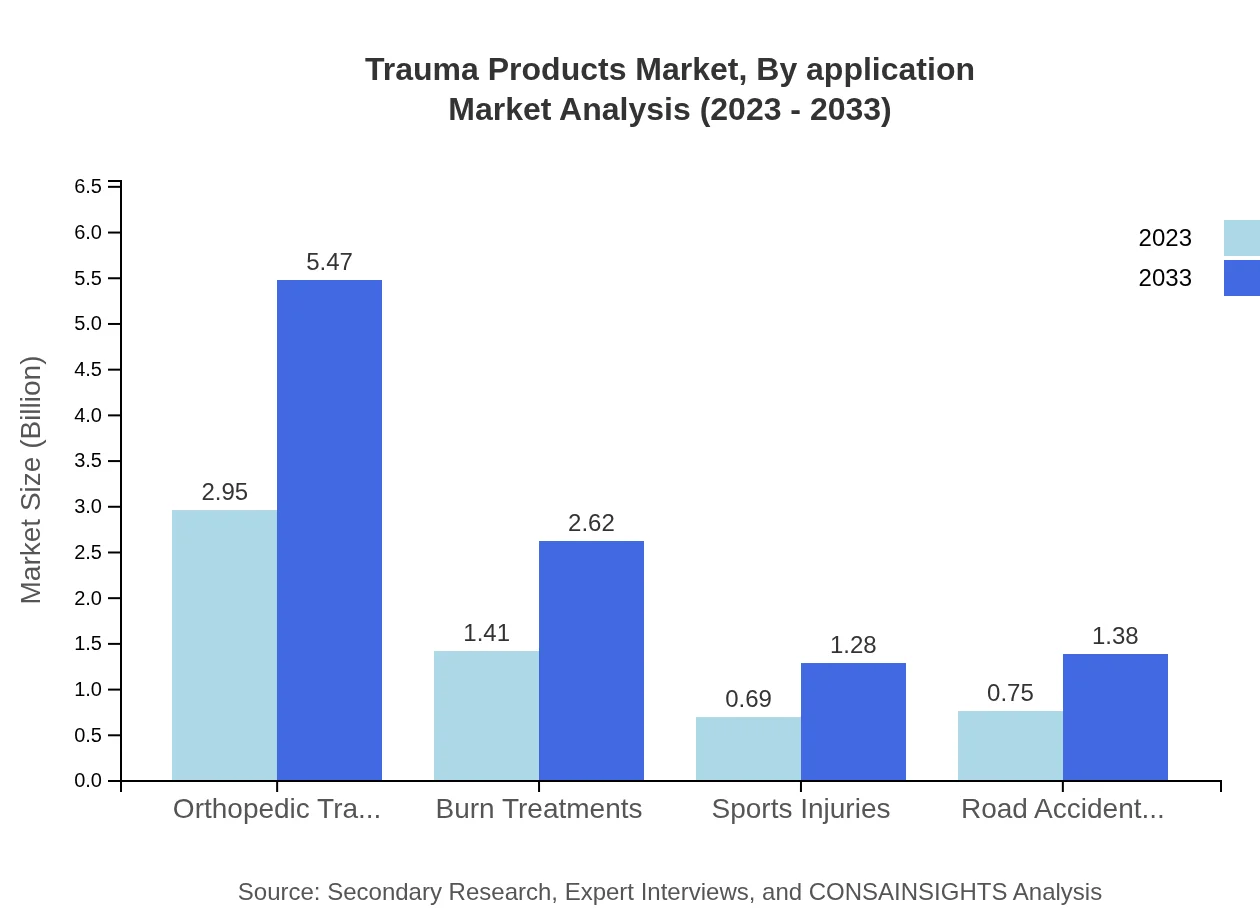

Trauma Products Market Analysis By Application

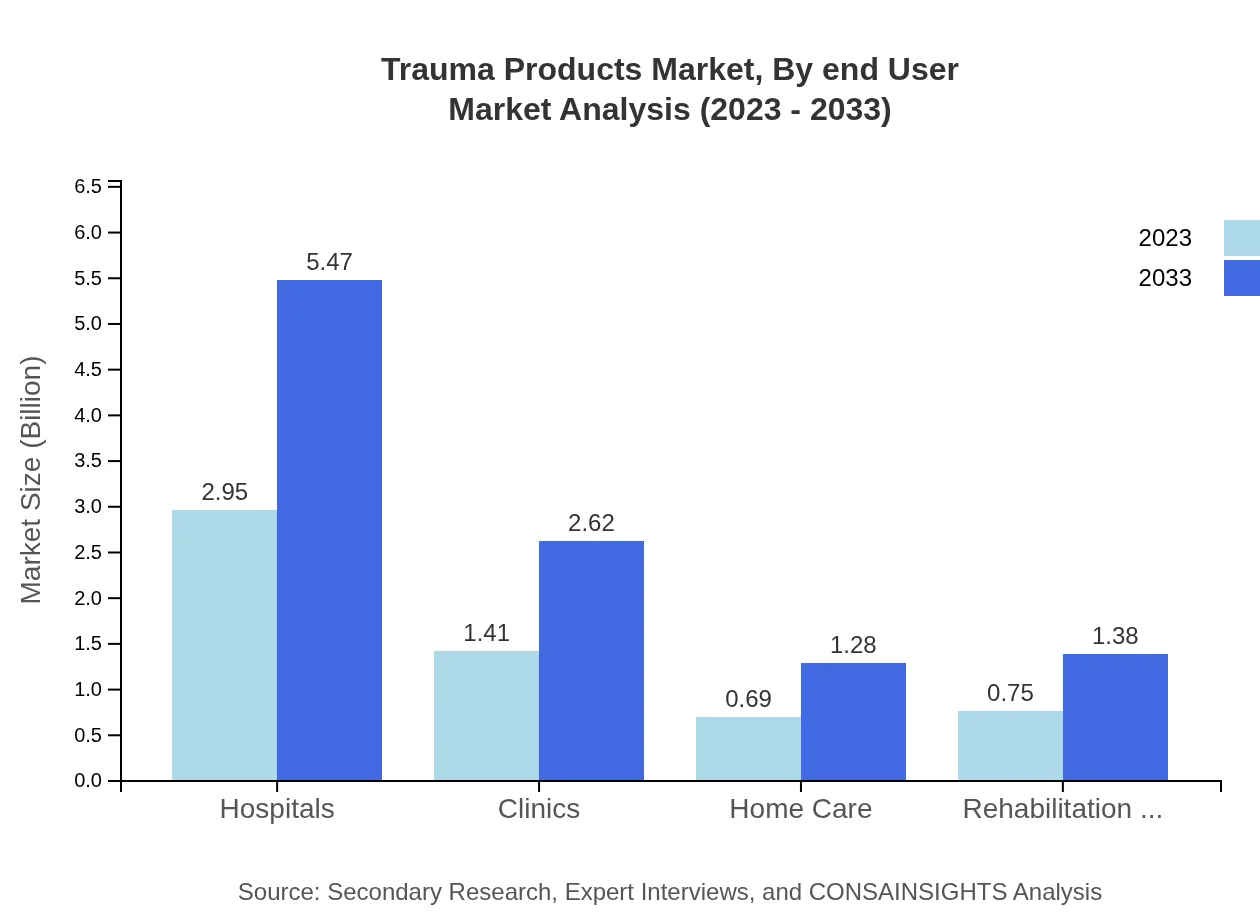

Focusing on applications, orthopedic traumas make up a substantial segment, valued at $2.95 billion in 2023, projected to grow to $5.47 billion by 2033. The increasing investment in sports and outdoor activities fuels demand for trauma products in this category.

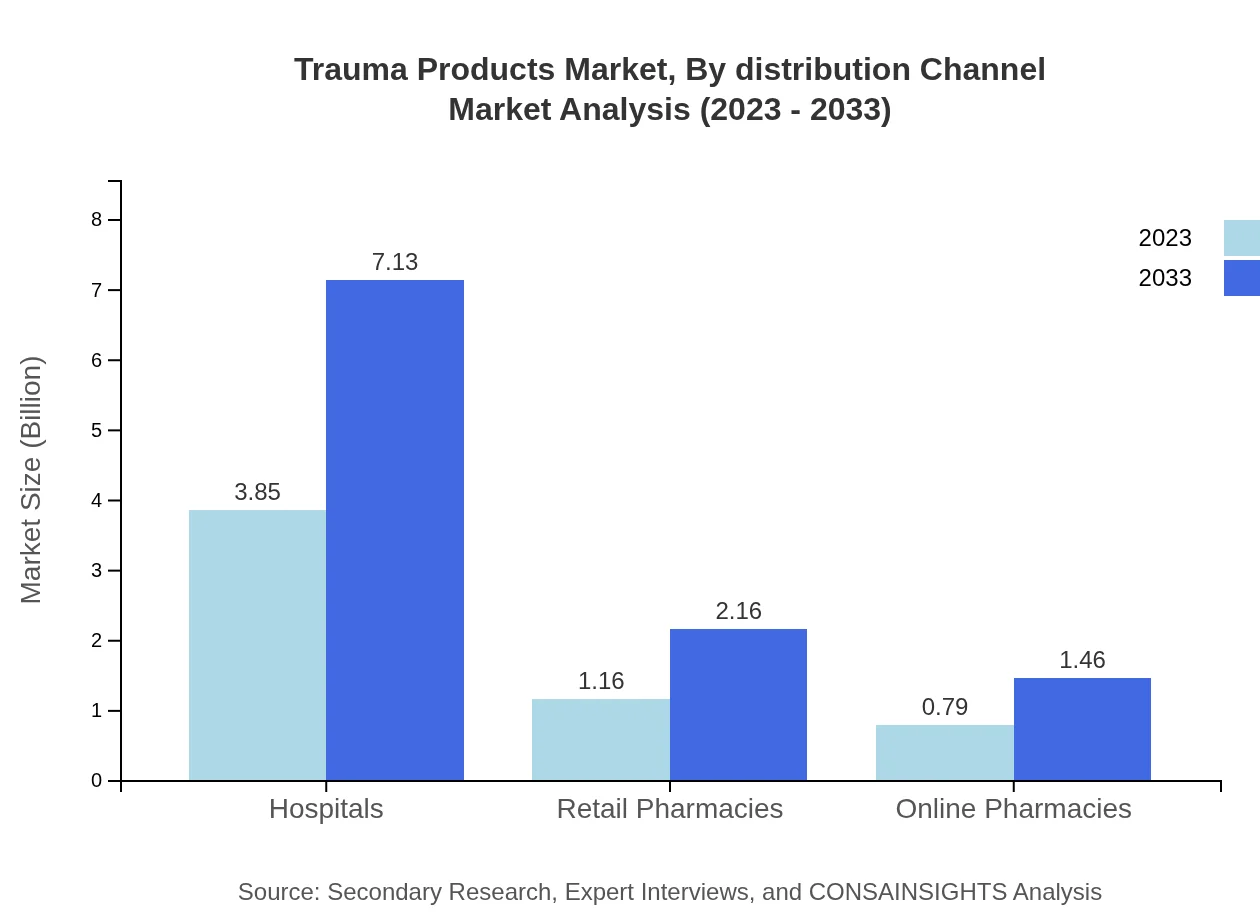

Trauma Products Market Analysis By Distribution Channel

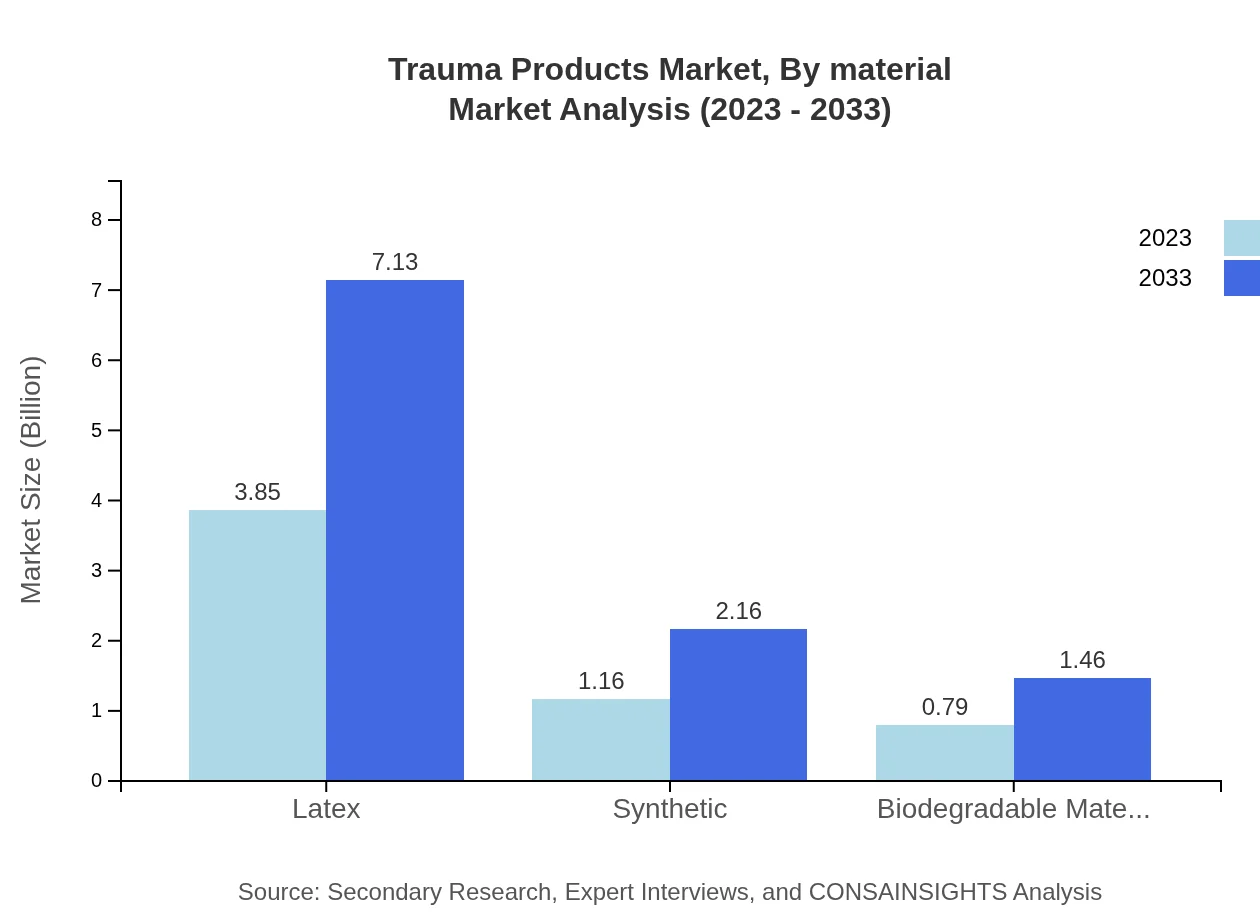

Distribution channels for trauma products are diversifying, with hospitals being the largest segment, accounting for $3.85 billion in 2023, expected to grow to $7.13 billion by 2033. The rise of online pharmacies is also notable, growing from $0.79 billion to $1.46 billion.

Trauma Products Market Analysis By End User

Hospitals continue to dominate the end-user market for trauma products with a consistent share of 66.34%. Home care also plays a critical role, with growth highlighting the need for at-home care options for recovery, expanding from $0.69 billion to $1.28 billion by 2033.

Trauma Products Market Analysis By Material

Material selection in trauma products shows a clear trend toward the use of biodegradable materials, which are gaining traction due to environmental concerns. Biodegradable materials are set to grow significantly from $0.79 billion in 2023 to $1.46 billion by 2033.

Trauma Products Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Trauma Products Industry

Johnson & Johnson:

A leading player in the trauma products market, offering a wide range of medical devices and solutions aimed at trauma management.Medtronic :

Recognized for its innovative products, particularly in surgical instruments and bone repair solutions in trauma care.Stryker Corporation:

A major manufacturer known for its trauma surgical systems and orthopedics, contributing significantly to the market's growth.We're grateful to work with incredible clients.

FAQs

What is the market size of trauma Products?

The trauma products market size is valued at $5.8 billion in 2023, with a projected CAGR of 6.2% over the next decade. By 2033, the market is expected to grow significantly, indicating strong demand for trauma-related products globally.

What are the key market players or companies in this trauma Products industry?

Key players in the trauma products industry include multinational corporations focusing on medical supplies, hospitals, and rehabilitation centers. These companies innovate continuously to enhance product portfolio and ensure competitiveness in this rapidly growing market.

What are the primary factors driving the growth in the trauma products industry?

The growth in the trauma products industry is driven by rising incidences of accidents, increasing geriatric population, advancements in medical technology, and greater healthcare expenditure. These factors necessitate the need for effective trauma care solutions.

Which region is the fastest Growing in the trauma Products?

The fastest-growing region in the trauma products market is North America, projected to grow from $2.09 billion in 2023 to $3.87 billion by 2033. Europe and Asia Pacific also show significant growth, driven by healthcare advancements and population demographics.

Does ConsaInsights provide customized market report data for the trauma Products industry?

Yes, ConsaInsights offers customized market report data tailored to specific requirements within the trauma products industry. This includes detailed analyses, market forecasts, and strategic insights relevant to your business needs.

What deliverables can I expect from this trauma Products market research project?

Expect insightful deliverables such as comprehensive market analysis, competitive landscape evaluation, trend identification, regional breakdowns, and segment analysis. These will provide actionable insights to aid decision-making in the trauma products sector.

What are the market trends of trauma Products?

Current trends in the trauma products market include increasing demand for advanced wound care materials, the rise of e-commerce in pharmaceutical distribution, and the integration of technology. Enhanced focus on rehabilitation solutions and home care markets is also notable.