Reports >

Life Sciences

>

Uk Ivd Market Report

Uk Ivd Market Report

Published Date: 31 January 2026 | Report Code: uk-ivd

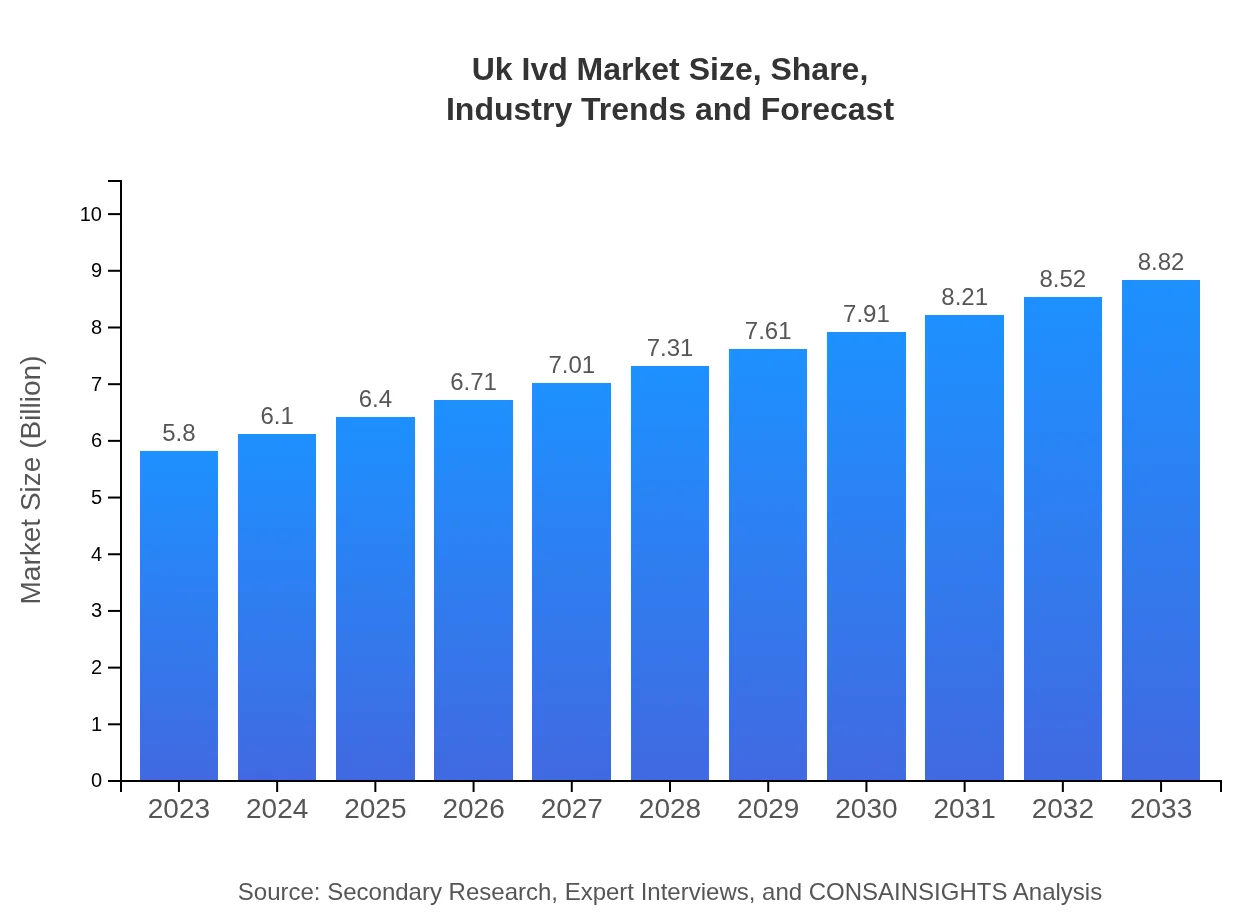

Uk Ivd Market Size, Share, Industry Trends and Forecast to 2033

This report provides a comprehensive analysis of the UK IVD market from 2023 to 2033, highlighting market trends, sizing, segmentation, and regional insights, including technology advancements and competitive landscape.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $5.80 Billion |

| CAGR (2023-2033) | 4.2% |

| 2033 Market Size | $8.82 Billion |

| Top Companies | Roche Diagnostics, Abbott Laboratories, Siemens Healthineers, Thermo Fisher Scientific |

| Last Modified Date | 31 January 2026 |

UK IVD Market Overview

Customize Uk Ivd Market Report market research report

- ✔ Get in-depth analysis of Uk Ivd market size, growth, and forecasts.

- ✔ Understand Uk Ivd's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Uk Ivd

What is the Market Size & CAGR of the UK IVD market in 2023 and 2033?

UK IVD Industry Analysis

UK IVD Market Segmentation and Scope

Tell us your focus area and get a customized research report.

UK IVD Market Analysis Report by Region

Europe Uk Ivd Market Report:

The UK IVD market, a part of the greater European market valued at £1.41 billion in 2023, is expected to grow to £2.15 billion by 2033, supported by an aging population and a strong emphasis on early disease detection.Asia Pacific Uk Ivd Market Report:

In 2023, the Asia Pacific IVD market is valued at approximately £1.24 billion, expected to grow to £1.88 billion by 2033. This region is characterized by rapid technological adoption and an increasing emphasis on affordable healthcare solutions, supported by government initiatives.North America Uk Ivd Market Report:

The North American market, valued at £1.88 billion in 2023, is projected to reach £2.85 billion by 2033, driven by high healthcare expenditure, technological advancements, and the presence of major companies in the region.South America Uk Ivd Market Report:

The South American IVD market is anticipated to rise from £0.50 billion in 2023 to £0.76 billion by 2033. Growth is driven by an expanding middle class, increasing health awareness, and investments in healthcare infrastructure.Middle East & Africa Uk Ivd Market Report:

In the Middle East and Africa, the IVD market is expected to grow from £0.78 billion in 2023 to £1.18 billion by 2033 due to increasing healthcare investments and higher disease incidence rates.Tell us your focus area and get a customized research report.

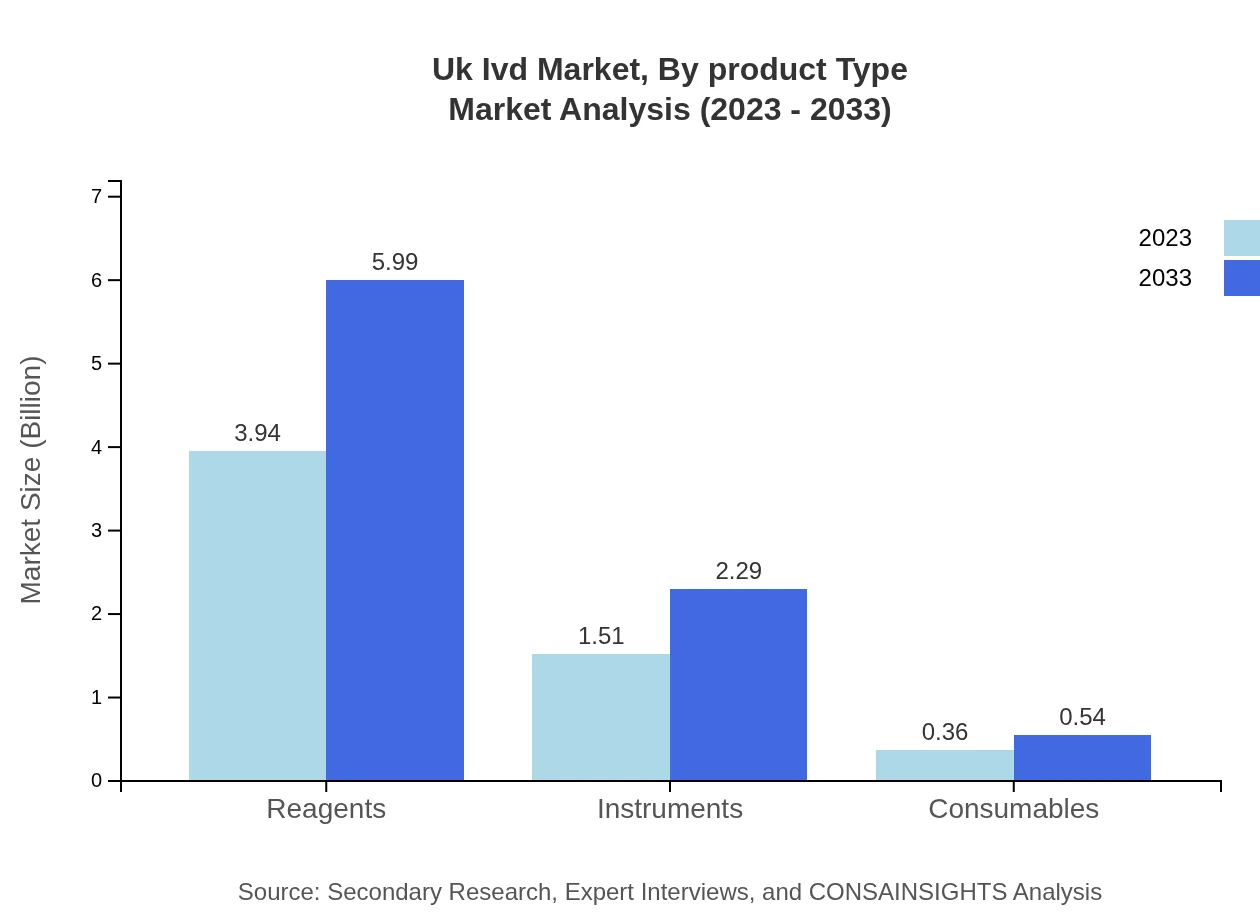

Uk Ivd Market Analysis By Product Type

The primary product types in the UK IVD market include immunoassays, molecular diagnostics, reagents, instruments, and consumables. Immunoassays dominate the market, expected to grow from £3.94 billion in 2023 to £5.99 billion by 2033, maintaining a market share of 67.91%. Molecular diagnostics are growing increasingly significant, projected to rise from £1.51 billion to £2.29 billion and capturing 25.95% of the market share.

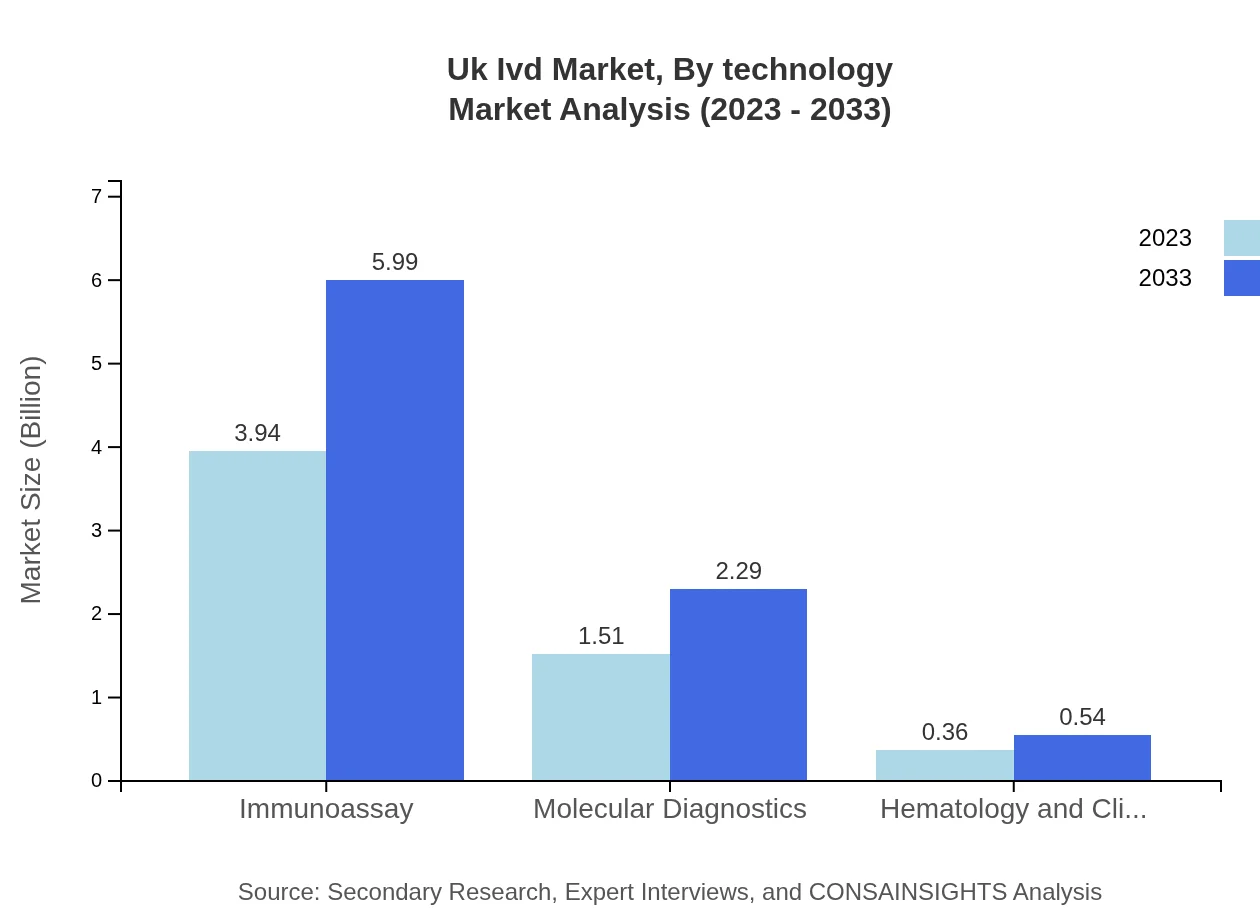

Uk Ivd Market Analysis By Technology

Technologies leading the UK IVD market include ELISA, PCR, and NGS. ELISA remains the most used technology, displaying strong growth potential. The push towards precision medicine and rapid testing solutions continues to drive technological advancements in this sector.

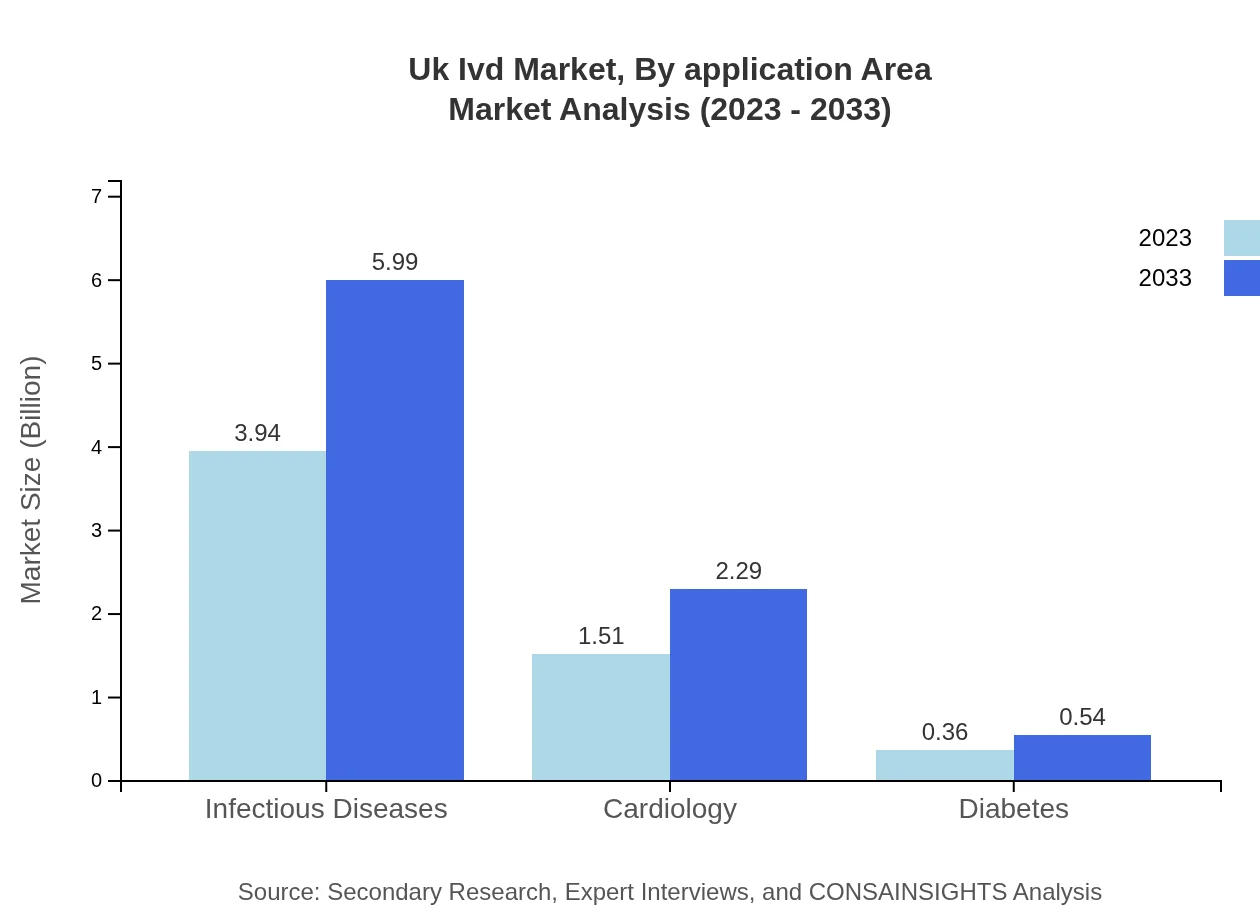

Uk Ivd Market Analysis By Application Area

Major application areas comprise infectious diseases, cardiology, diabetes, and oncology. Particularly, infectious diseases testing is projected to hold the largest share due to heightened awareness and demand for rapid diagnostics amidst ongoing public health initiatives.

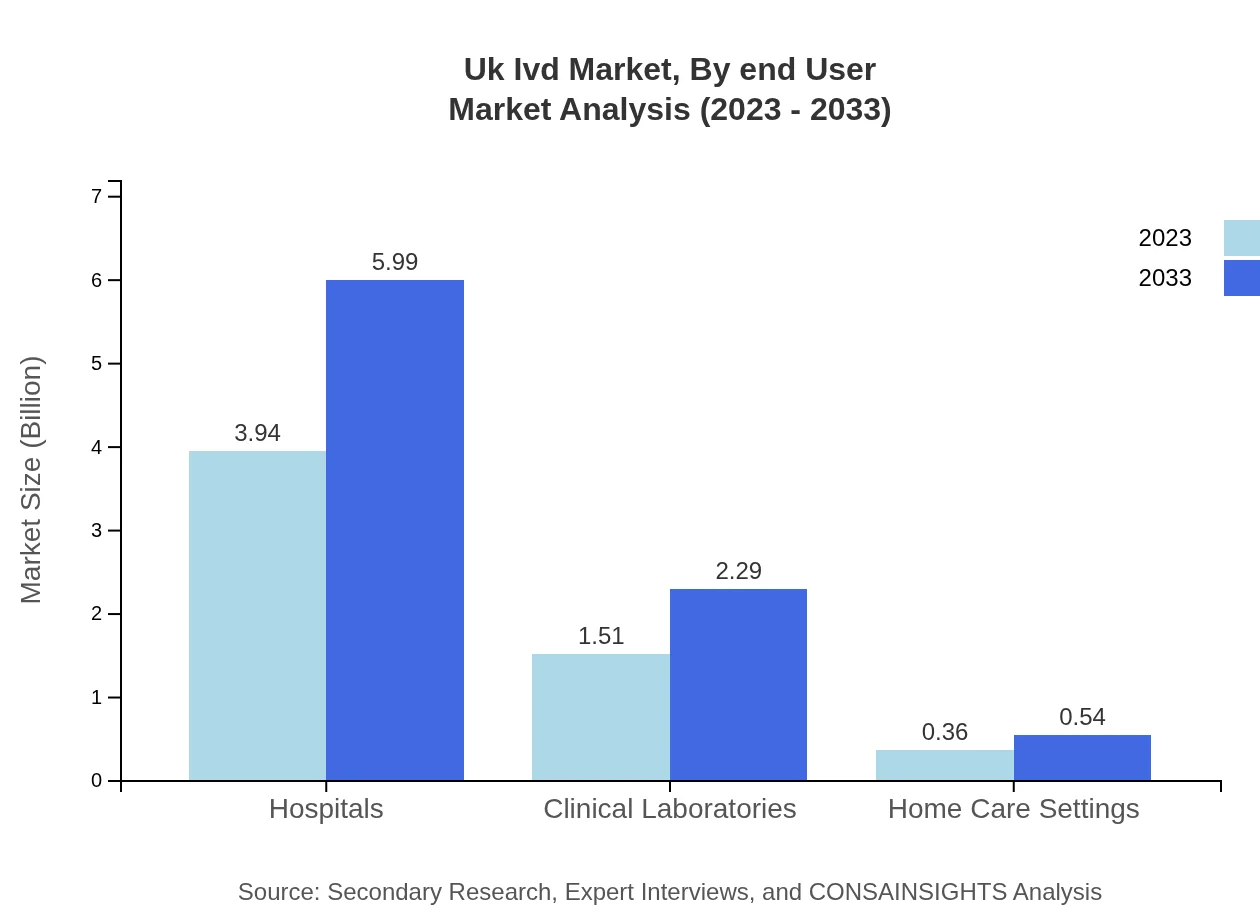

Uk Ivd Market Analysis By End User

Hospitals are the leading end-users for IVD products, with a market share of 67.91% in 2023. Clinical laboratories and home care settings also contribute significantly, with shares of 25.95% and 6.14%, respectively. This structure highlights the critical role hospitals play in diagnostic services.

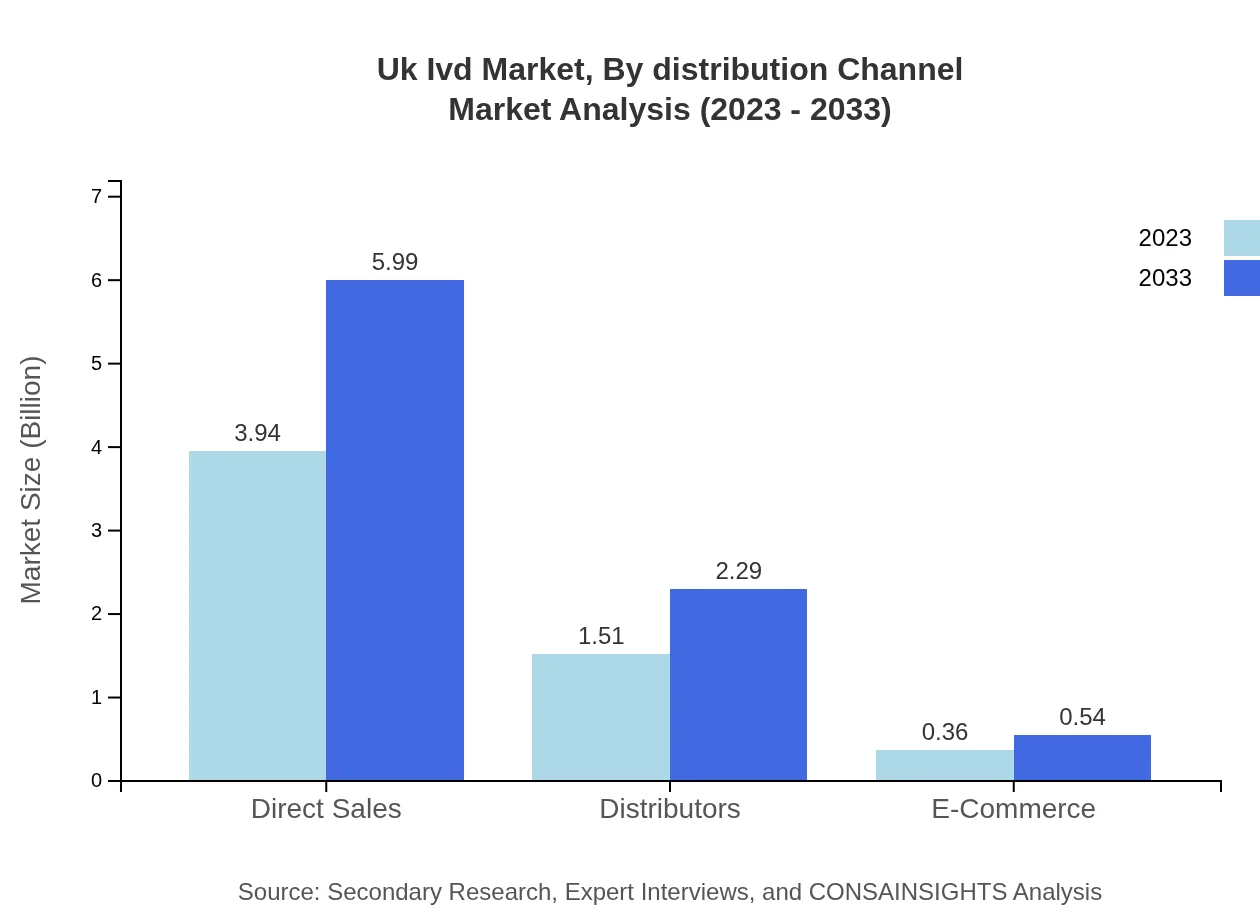

Uk Ivd Market Analysis By Distribution Channel

The market is predominantly segmented through direct sales, distributors, and e-commerce. Direct sales account for 67.91% of the market share, indicating a preference for established relationships with healthcare providers, while e-commerce is gaining traction, reflecting a shift towards digital marketplaces.

UK IVD Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in the UK IVD Industry

Roche Diagnostics:

A leader in the diagnostics industry, Roche offers a range of innovative IVD products focused on accuracy and speed, significantly contributing to the early diagnosis and personalized treatment.Abbott Laboratories:

With a strong portfolio in immunoassays and molecular diagnostics, Abbott is recognized for its advanced diagnostics technology and commitment to enhancing patient outcomes.Siemens Healthineers:

Siemens Healthineers stands out for its comprehensive IVD product range and commitment to innovation, driving growth with cutting-edge solutions for healthcare.Thermo Fisher Scientific:

Thermo Fisher is a key player in the IVD sector, focusing on molecular diagnostics and high-throughput solutions, positioning itself as a leader in the life sciences field.We're grateful to work with incredible clients.

FAQs

What is the market size of UK IVD?

The UK in-vitro diagnostics (IVD) market is estimated to be valued at approximately $5.8 billion in 2023, with a projected compound annual growth rate (CAGR) of 4.2% through 2033, indicating sustained growth in this sector.

What are the key market players or companies in the UK IVD industry?

Some of the leading players in the UK IVD market include Roche Diagnostics, Abbott Laboratories, Siemens Healthineers, Danaher Corporation, and Hologic, which dominate through innovation and extensive distribution networks.

What are the primary factors driving the growth in the UK IVD industry?

Key drivers of growth in the UK IVD market include an aging population, increased prevalence of chronic diseases, advancements in technology, and rising demand for point-of-care testing solutions that improve diagnostic accuracy and efficiency.

Which region is the fastest Growing in the UK IVD?

Europe, particularly the UK, exhibits notable growth in the IVD market, expanding from $1.41 billion in 2023 to an estimated $2.15 billion by 2033, reflecting a focus on advanced healthcare solutions in this region.

Does ConsaInsights provide customized market report data for the UK IVD industry?

Yes, ConsaInsights offers tailored market report data for the UK IVD industry, allowing clients to gain specific insights suited to their business needs, including regional trends and segment analyses.

What deliverables can I expect from this UK IVD market research project?

From the UK IVD market research project, clients can expect detailed reports including market forecasts, competitive analysis, regional breakdowns, segment insights, and strategic recommendations for stakeholders.

What are the market trends of UK IVD?

Current trends in the UK IVD market include heightened interest in molecular diagnostics, increased use of digital health tools, growing emphasis on personalized medicine, and shifts towards home-based testing solutions.