Urgent Care Center Market Report

Published Date: 31 January 2026 | Report Code: urgent-care-center

Urgent Care Center Market Size, Share, Industry Trends and Forecast to 2033

This report presents an in-depth analysis of the Urgent Care Center market, including market size forecasts, segment analyses, and regional insights for the years 2023 through 2033. It provides valuable data for understanding trends, competitive positioning, and growth opportunities within this dynamic industry.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

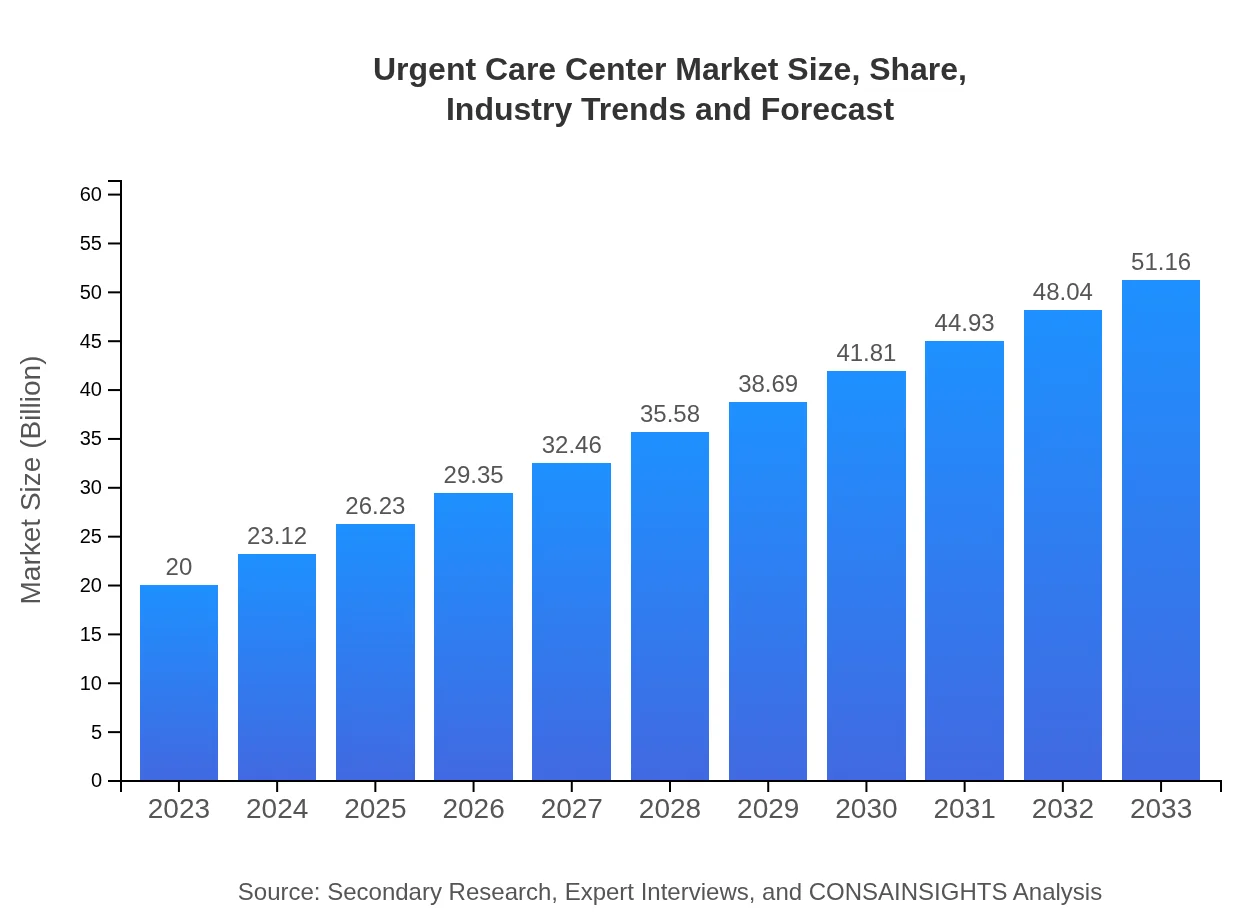

| 2023 Market Size | $20.00 Billion |

| CAGR (2023-2033) | 9.5% |

| 2033 Market Size | $51.16 Billion |

| Top Companies | Patient First, CareNow, MD Now, NextCare |

| Last Modified Date | 31 January 2026 |

Urgent Care Center Market Overview

Customize Urgent Care Center Market Report market research report

- ✔ Get in-depth analysis of Urgent Care Center market size, growth, and forecasts.

- ✔ Understand Urgent Care Center's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Urgent Care Center

What is the Market Size & CAGR of Urgent Care Center market in 2023?

Urgent Care Center Industry Analysis

Urgent Care Center Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Urgent Care Center Market Analysis Report by Region

Europe Urgent Care Center Market Report:

The European Urgent Care Center market is projected to grow from $6.16 billion in 2023 to $15.75 billion by 2033, driven by a combination of changing healthcare policies that favor outpatient care and increased demand for immediate medical services.Asia Pacific Urgent Care Center Market Report:

The Asia Pacific market is expected to grow from $3.96 billion in 2023 to $10.12 billion by 2033, with a CAGR of over 10%. Increasing urbanization and a rising awareness of healthcare accessibility drive growth in countries like China and India.North America Urgent Care Center Market Report:

North America leads the market with a size of $6.76 billion in 2023, expected to reach $17.30 billion by 2033, marking a CAGR of 9.7%. Factors such as high private insurance penetration and increasing patient traffic to urgent care centers bolster the region's dominance.South America Urgent Care Center Market Report:

In South America, the market size is projected to increase from $1.43 billion in 2023 to $3.65 billion in 2033, growing at a CAGR of 9.6%. The development of healthcare infrastructure and government initiatives to improve healthcare access promote the growth of urgent care centers.Middle East & Africa Urgent Care Center Market Report:

In the Middle East and Africa region, the market is anticipated to grow from $1.70 billion in 2023 to $4.34 billion by 2033. Expansion in healthcare services, combined with increasing health awareness, supports this growth trajectory.Tell us your focus area and get a customized research report.

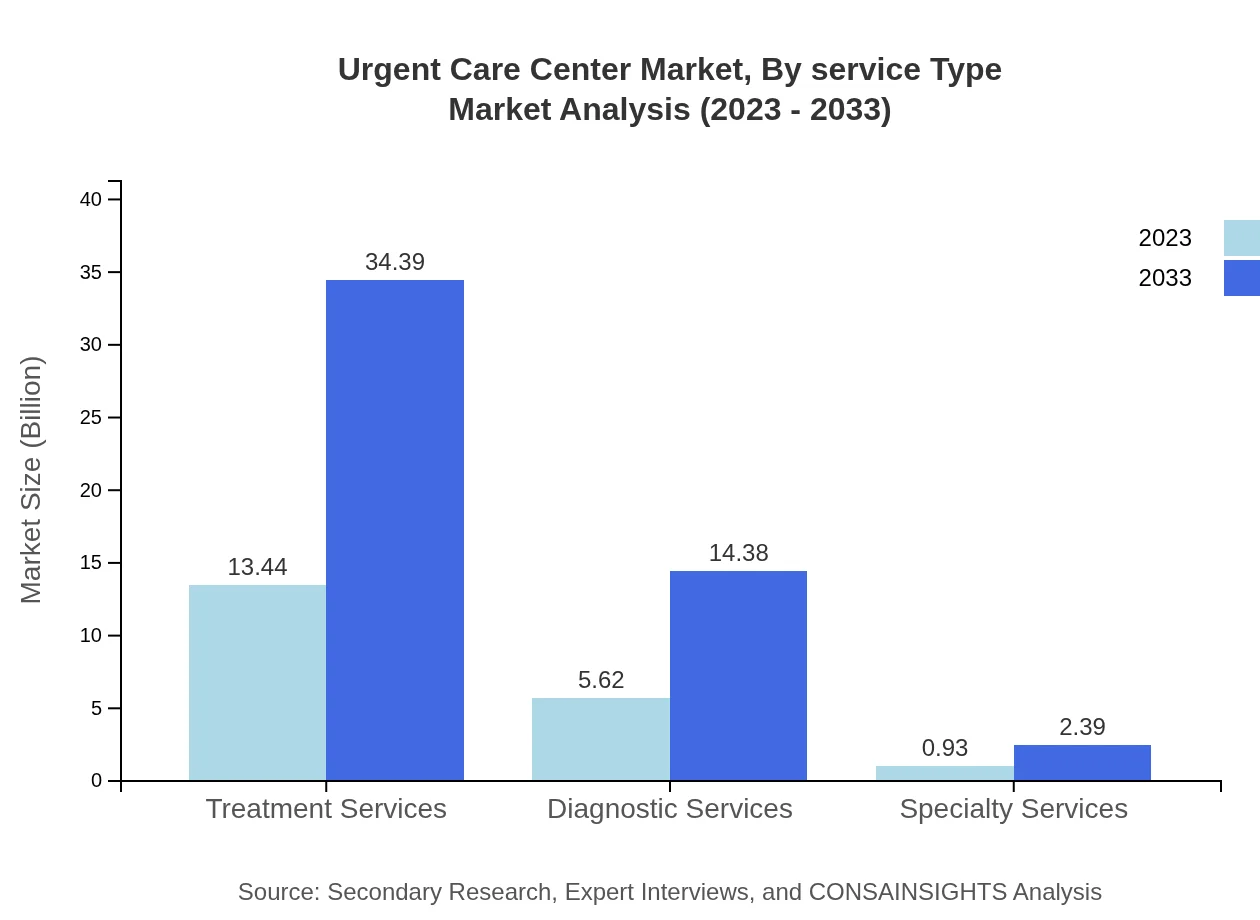

Urgent Care Center Market Analysis By Service Type

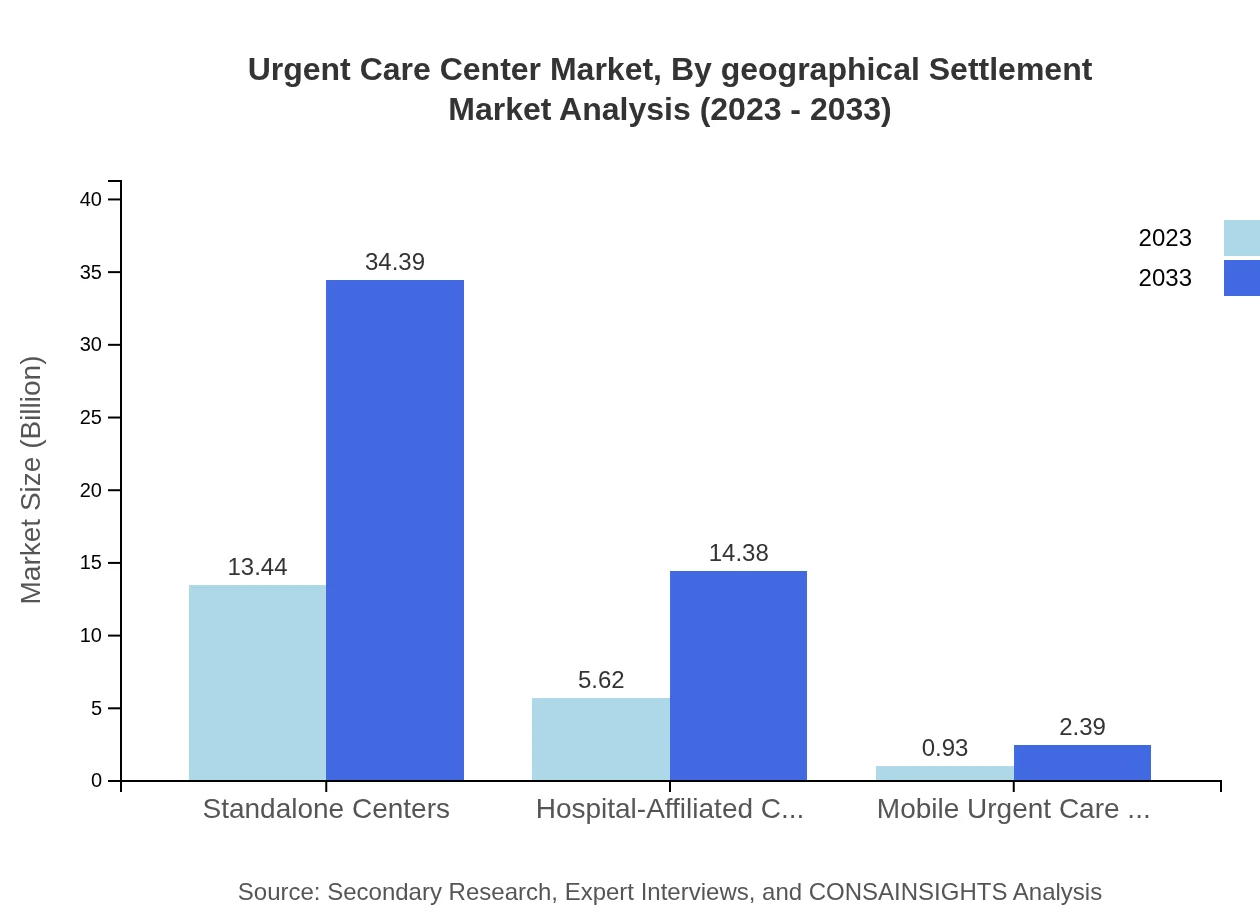

The market for Treatment Services is leading with a significant growth from $13.44 billion in 2023 to $34.39 billion by 2033. Diagnostic Services also show substantial growth, expanding from $5.62 billion to $14.38 billion in the same period. Specialty Services, although smaller, are expected to increase from $0.93 billion to $2.39 billion, reflecting a growing interest in specialized urgent care.

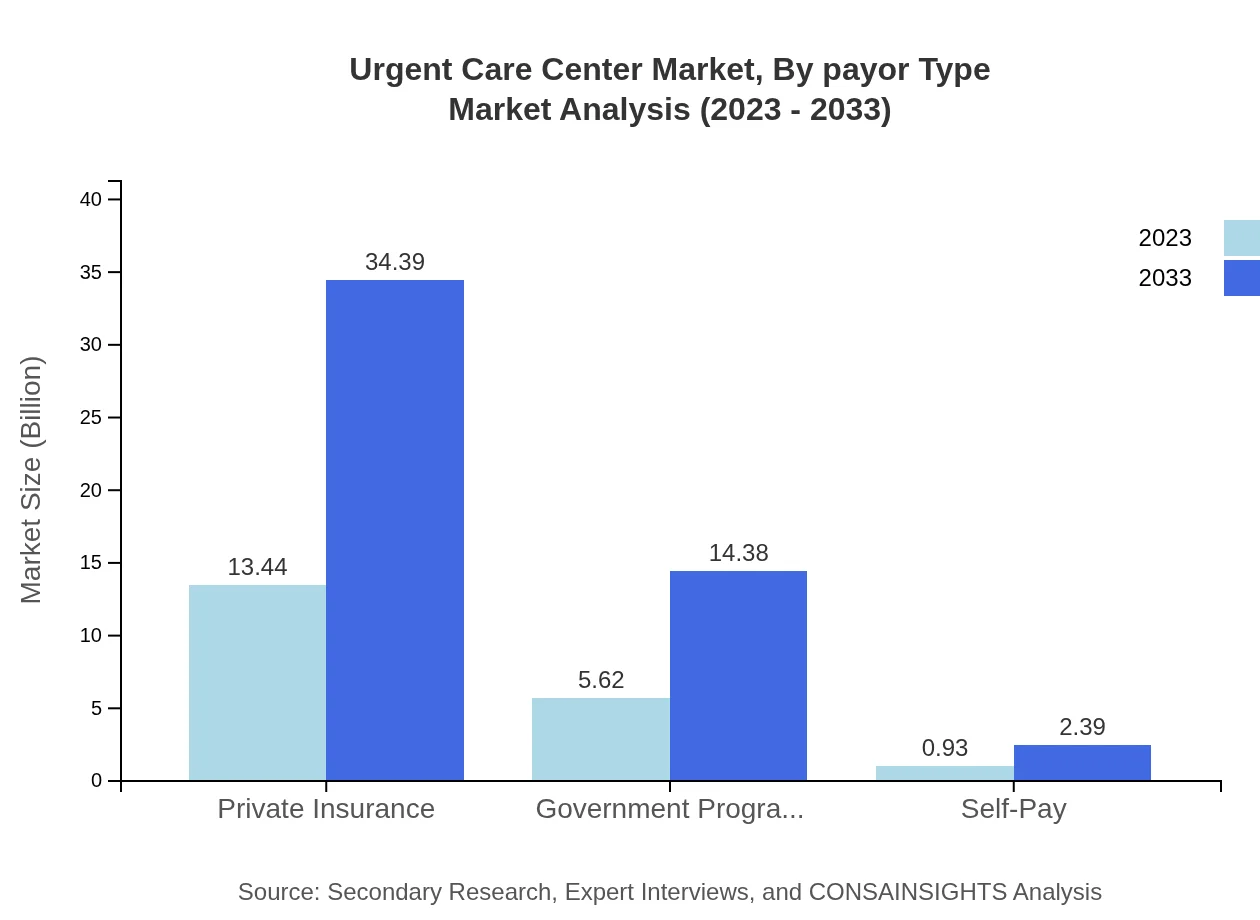

Urgent Care Center Market Analysis By Payor Type

Private Insurance dominates the payer landscape, growing from $13.44 billion in 2023 to $34.39 billion by 2033, maintaining a share of 67.22%. Government Programs are expected to grow from $5.62 billion to $14.38 billion, capturing 28.11% of the market, while Self-Pay options remain smaller, from $0.93 billion to $2.39 billion, holding a steady 4.67% share.

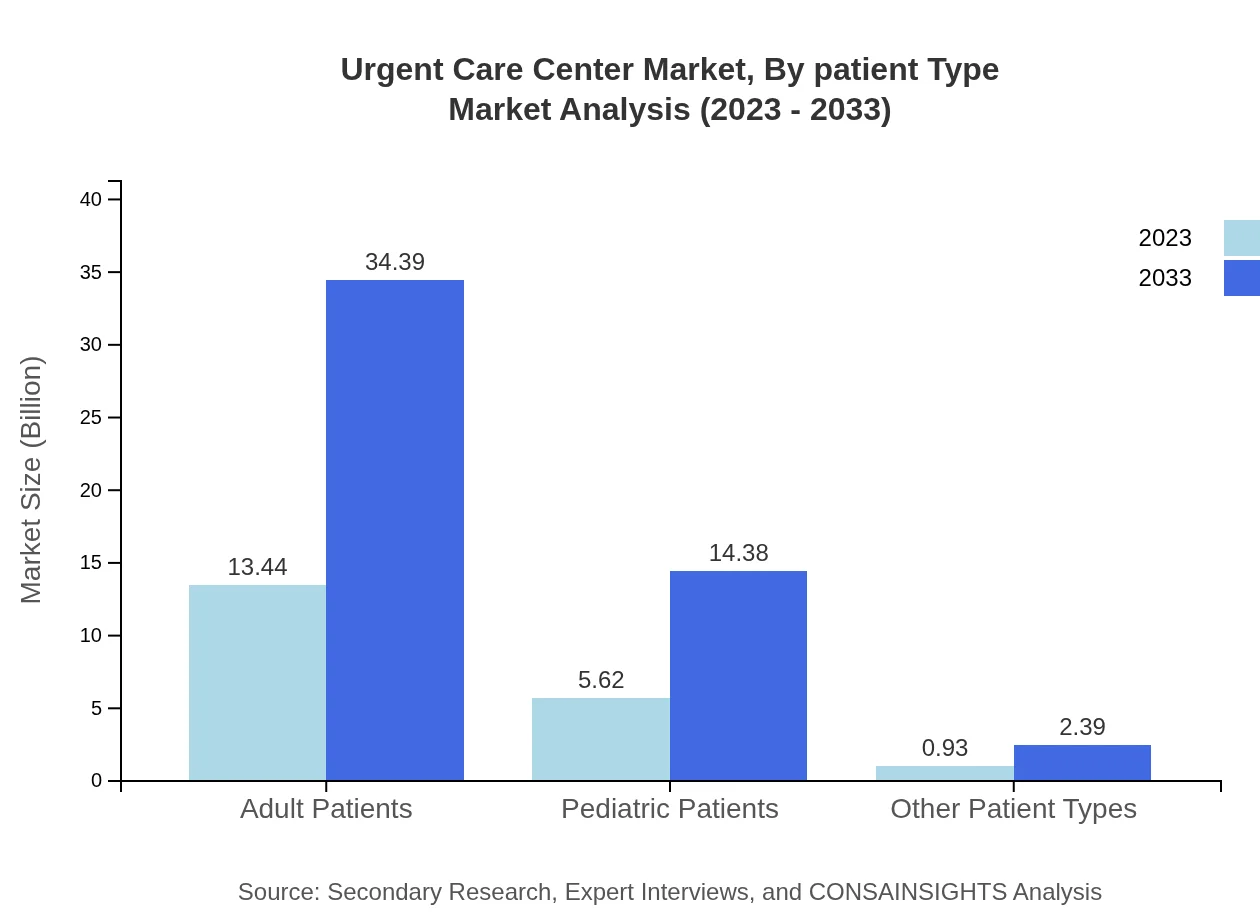

Urgent Care Center Market Analysis By Patient Type

The Adult Patients segment leads with a market size of $13.44 billion in 2023, projected to grow to $34.39 billion by 2033, sustaining a 67.22% market share. Pediatric Patients follow with an increase from $5.62 billion to $14.38 billion previously sharing 28.11%, while Other Patient Types remain a small segment from $0.93 billion to $2.39 billion, also retaining a 4.67% share.

Urgent Care Center Market Analysis By Geographical Settlement

Geographically, the North American market leads significantly in size and growth potential, while Europe and Asia Pacific follow with substantial increases. South America shows a growing interest in urgent care services, and the Middle East and Africa represent emerging markets with increasing investments in healthcare infrastructure.

Urgent Care Center Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Urgent Care Center Industry

Patient First:

Patient First operates numerous urgent care centers across the US, focusing on high-quality patient care and accessible healthcare services.CareNow:

CareNow is known for its extensive network of urgent care centers in the US, offering convenient medical services and a commitment to patient satisfaction.MD Now:

MD Now is a leading urgent care provider in Florida, focusing on providing accessible, affordable care while incorporating advanced technology in healthcare delivery.NextCare:

NextCare offers urgent care services across multiple states with a focus on innovative patient care solutions and operational efficiency.We're grateful to work with incredible clients.

FAQs

What is the market size of Urgent Care Center?

The global urgent care center market is valued at approximately $20 billion in 2023, with a projected CAGR of 9.5%. This growth indicates a rising demand for efficient, accessible healthcare services across various regions.

What are the key market players or companies in the Urgent Care Center industry?

Key players in the urgent care center industry include WellNow Urgent Care, American Family Care, and Next Level Urgent Care. These companies are prominent for their extensive networks and commitment to patient-centric services.

What are the primary factors driving the growth in the Urgent Care Center industry?

The urgent care center industry is driven by increasing patient demand for immediate care services, rising healthcare costs, and the growing prevalence of non-emergency medical conditions, which make urgent care centers an appealing option for many patients.

Which region is the fastest Growing in the Urgent Care Center market?

The North America region is the fastest-growing in the urgent care center market, projected to grow from $6.76 billion in 2023 to approximately $17.30 billion by 2033. This growth is influenced by high healthcare spending and widespread acceptance of urgent care services.

Does ConsaInsights provide customized market report data for the Urgent Care Center industry?

Yes, ConsaInsights offers tailored market report data specific to the urgent care center industry. This customization enables clients to gain insights that align with their unique business objectives and market conditions.

What deliverables can I expect from this Urgent Care Center market research project?

Clients can expect comprehensive deliverables, including detailed market size analysis, growth forecasts, and insights on regional segments, competitive landscape, and key trends impacting the urgent care center industry.

What are the market trends of Urgent Care Center?

Current trends in the urgent care center market include increasing consumer preference for low-cost alternatives to emergency room visits, technological advancements in telemedicine, and an upswing in partnerships with insurance providers.