Vascular Stent Market Report

Published Date: 31 January 2026 | Report Code: vascular-stent

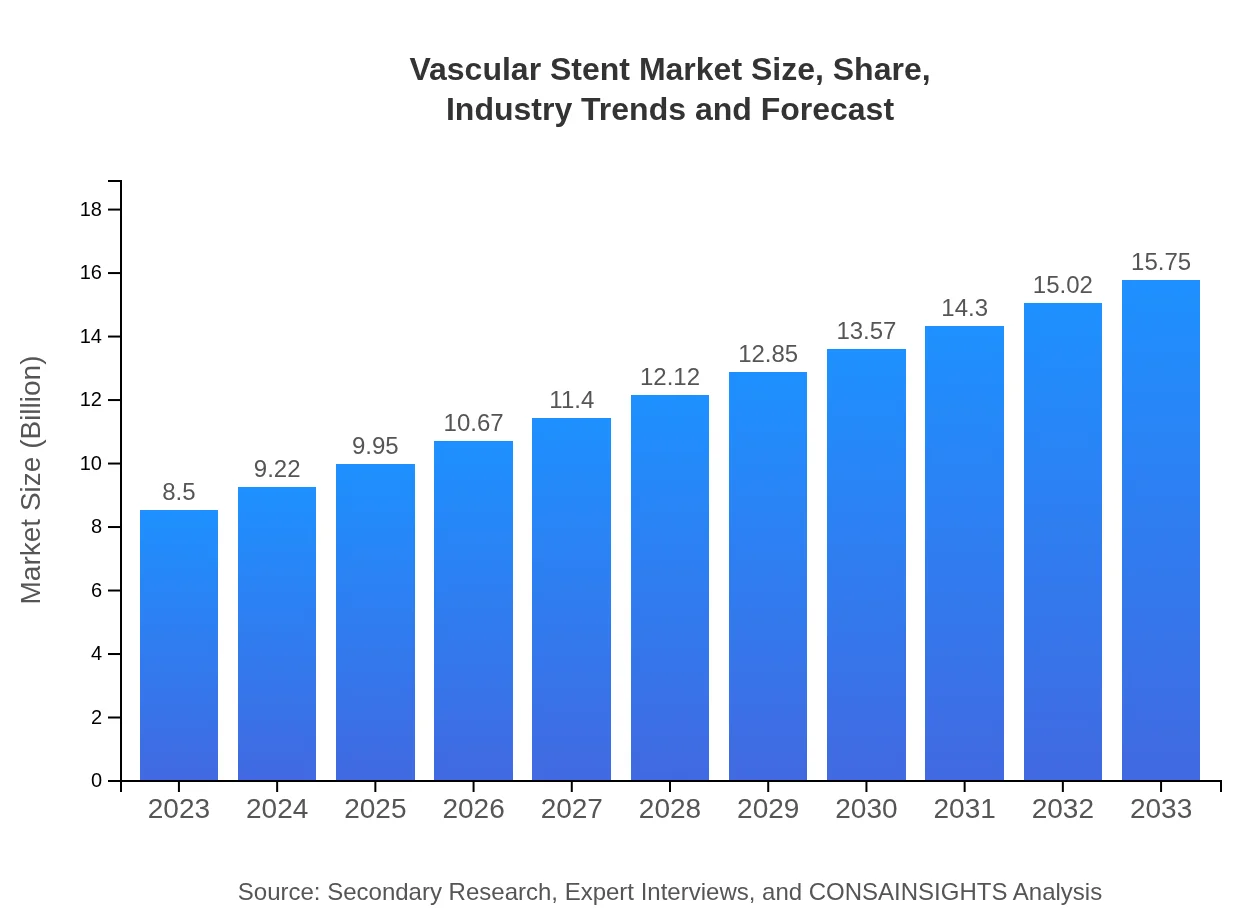

Vascular Stent Market Size, Share, Industry Trends and Forecast to 2033

This report provides a comprehensive analysis of the vascular stent market from 2023 to 2033, including insights on market size, growth trends, industry analysis, and regional dynamics, alongside detailed segmentation based on product type, material, application, end-user, and distribution channel.

| Metric | Value |

|---|---|

| Study Period | 2023 - 2033 |

| 2023 Market Size | $8.50 Billion |

| CAGR (2023-2033) | 6.2% |

| 2033 Market Size | $15.75 Billion |

| Top Companies | Medtronic , Boston Scientific Corporation, Abbott Laboratories, B. Braun Melsungen AG |

| Last Modified Date | 31 January 2026 |

Vascular Stent Market Overview

Customize Vascular Stent Market Report market research report

- ✔ Get in-depth analysis of Vascular Stent market size, growth, and forecasts.

- ✔ Understand Vascular Stent's regional dynamics and industry-specific trends.

- ✔ Identify potential applications, end-user demand, and growth segments in Vascular Stent

What is the Market Size & CAGR of the Vascular Stent market in 2023 and 2033?

Vascular Stent Industry Analysis

Vascular Stent Market Segmentation and Scope

Tell us your focus area and get a customized research report.

Vascular Stent Market Analysis Report by Region

Europe Vascular Stent Market Report:

The European vascular stent market was valued at $2.54 billion in 2023 and is projected to reach $4.71 billion by 2033. Factors contributing to this growth include high levels of investment in healthcare technologies, stringent regulatory standards, and rising incidences of vascular diseases.Asia Pacific Vascular Stent Market Report:

The Asia Pacific vascular stent market is projected to grow from $1.61 billion in 2023 to $2.99 billion in 2033, driven by a rapidly aging population and the increasing prevalence of cardiovascular diseases. Improved healthcare infrastructure and the introduction of advanced medical technologies in countries like China and India further boost this market.North America Vascular Stent Market Report:

In North America, the vascular stent market is expected to increase from $3.12 billion in 2023 to $5.78 billion by 2033. The United States dominates the market due to high healthcare expenditure, advanced healthcare technology, and a strong focus on research and innovation.South America Vascular Stent Market Report:

The South American market for vascular stents is anticipated to grow modestly from $0.19 billion in 2023 to $0.35 billion in 2033. The growth is influenced by rising healthcare investments and increased awareness of cardiovascular health, despite challenges like economic fluctuation in certain countries.Middle East & Africa Vascular Stent Market Report:

The vascular stent market in the Middle East and Africa is expected to rise from $1.04 billion in 2023 to $1.93 billion in 2033. The increase is propelled by improving healthcare systems and an expanding patient pool looking for advanced vascular intervention solutions.Tell us your focus area and get a customized research report.

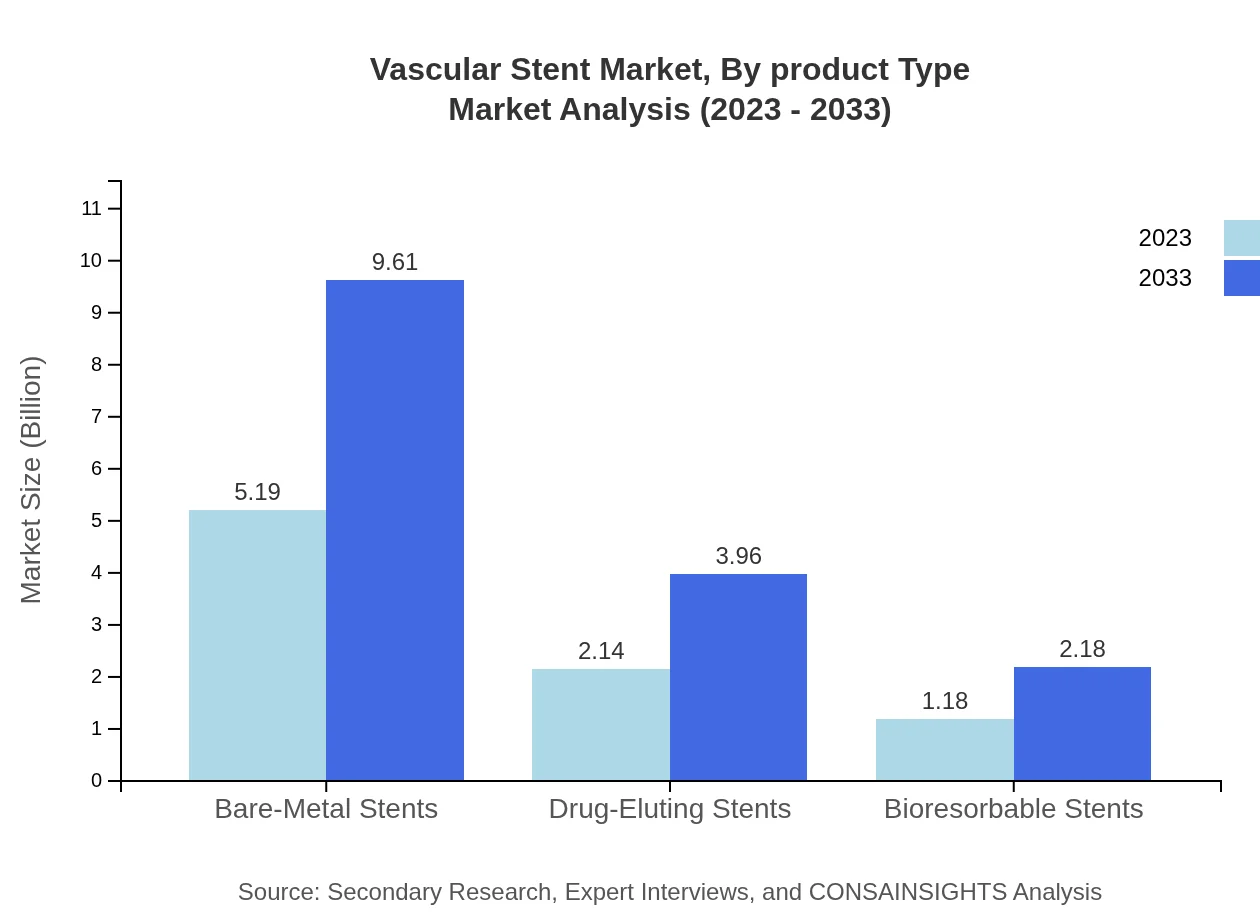

Vascular Stent Market Analysis By Product Type

The vascular stent market can be divided into two primary product types. Metal stents dominate the market, with a share of 81.16% in 2023, valued at $6.90 billion, and expect to reach $12.78 billion by 2033. Polymer stents, while holding a smaller market share of 18.84%, are projected to grow from $1.60 billion to $2.97 billion, reflecting innovations in biocompatible materials.

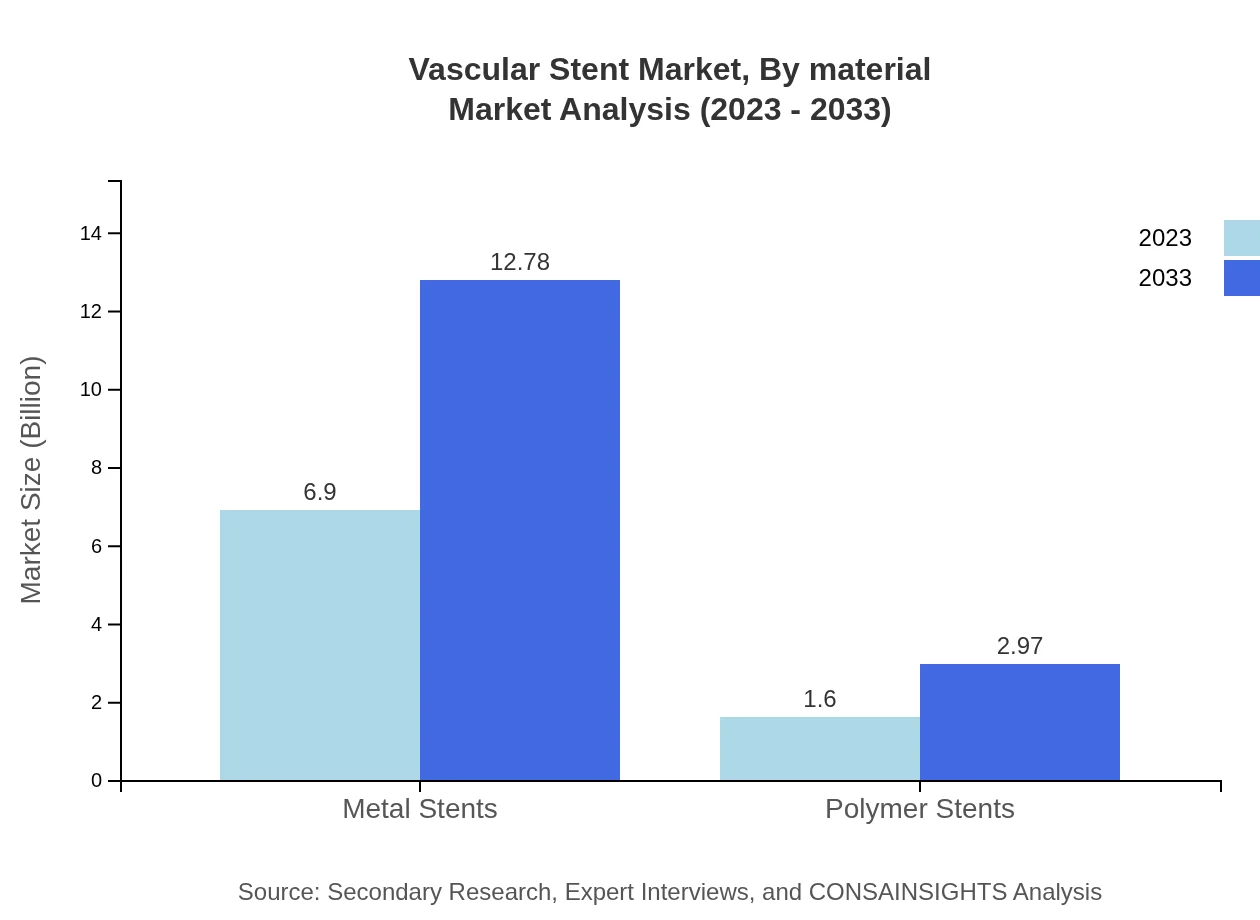

Vascular Stent Market Analysis By Material

The material segmentation indicates that metal stents, including bare-metal and drug-eluting types, are the market leaders. The bare-metal stent market accounts for 61.03% in both 2023 and 2033, while drug-eluting stents represent a significant 25.14% share. Polymer stents are emerging as effective alternatives, contributing to market diversity.

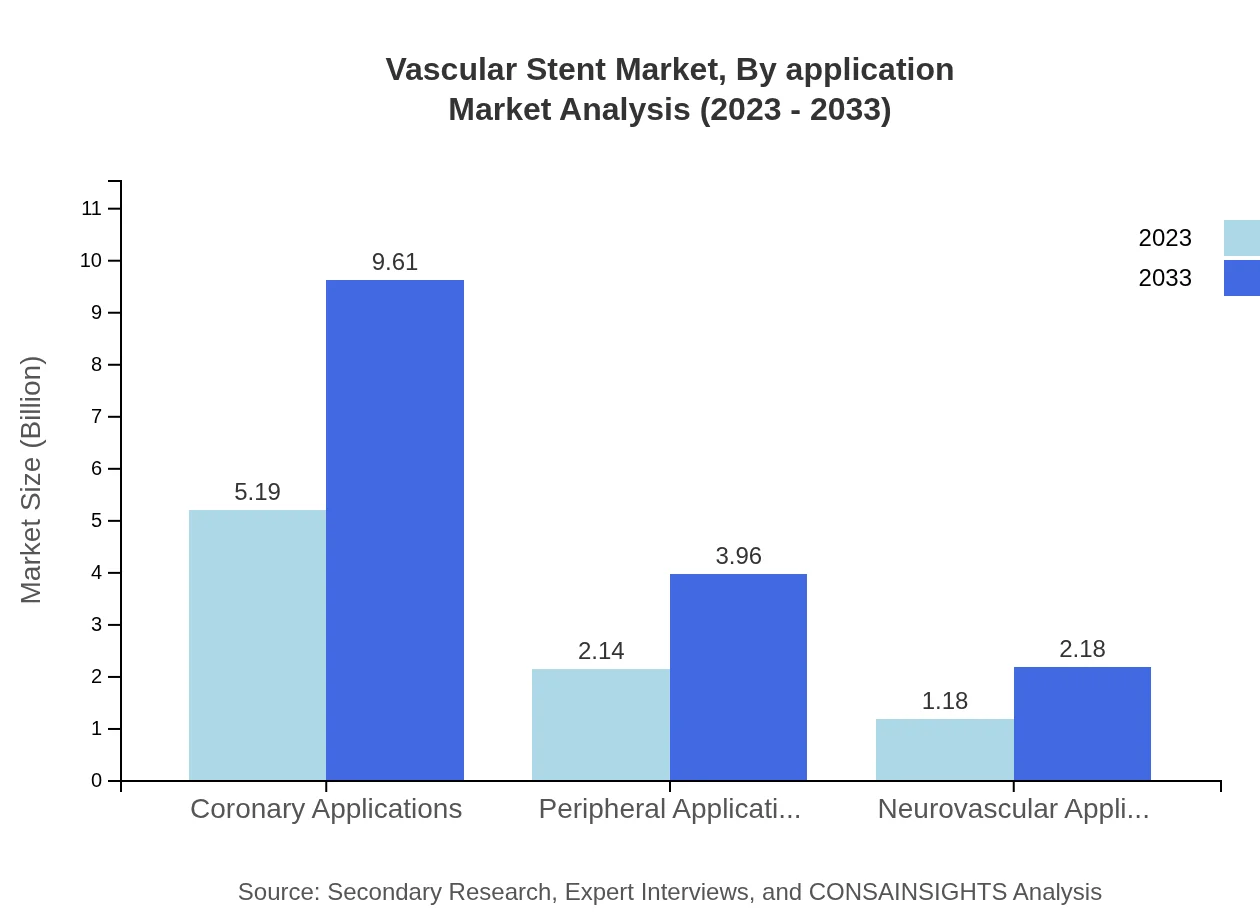

Vascular Stent Market Analysis By Application

Coronary applications hold the largest market share at 61.03% in 2023, projected to maintain this leading position through to 2033, owing to the high prevalence of coronary artery diseases. Peripheral and neurovascular applications, while smaller at 25.14% and 13.83% respectively, are on the rise due to advancements in peripheral stent technology.

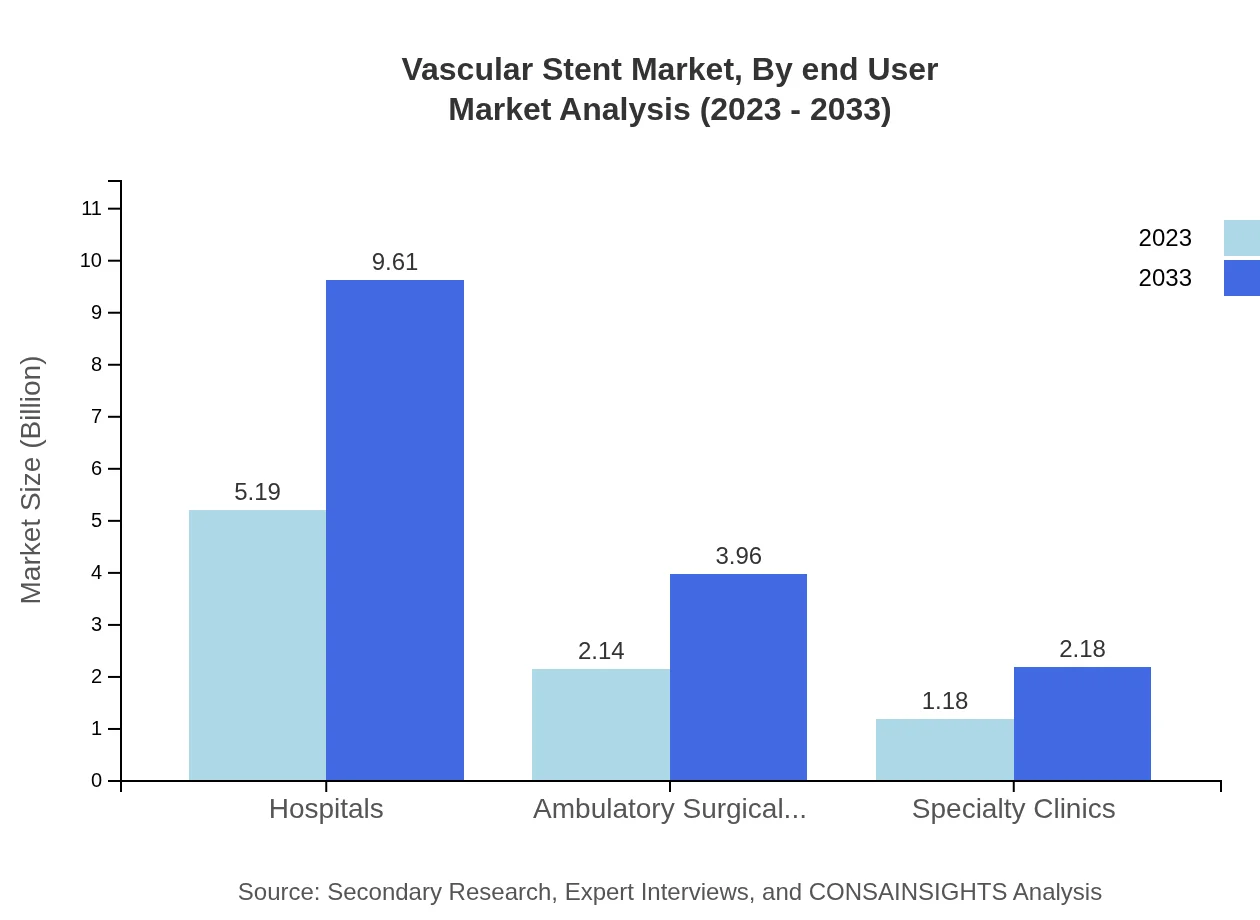

Vascular Stent Market Analysis By End User

Hospitals represent the primary end-user segment, accounting for 61.03% of the market in 2023 and slated to maintain this figure through 2033. Ambulatory surgical centers and specialty clinics follow, capturing 25.14% and 13.83% shares, respectively, as surgical approaches change, adapting to outpatient preferences.

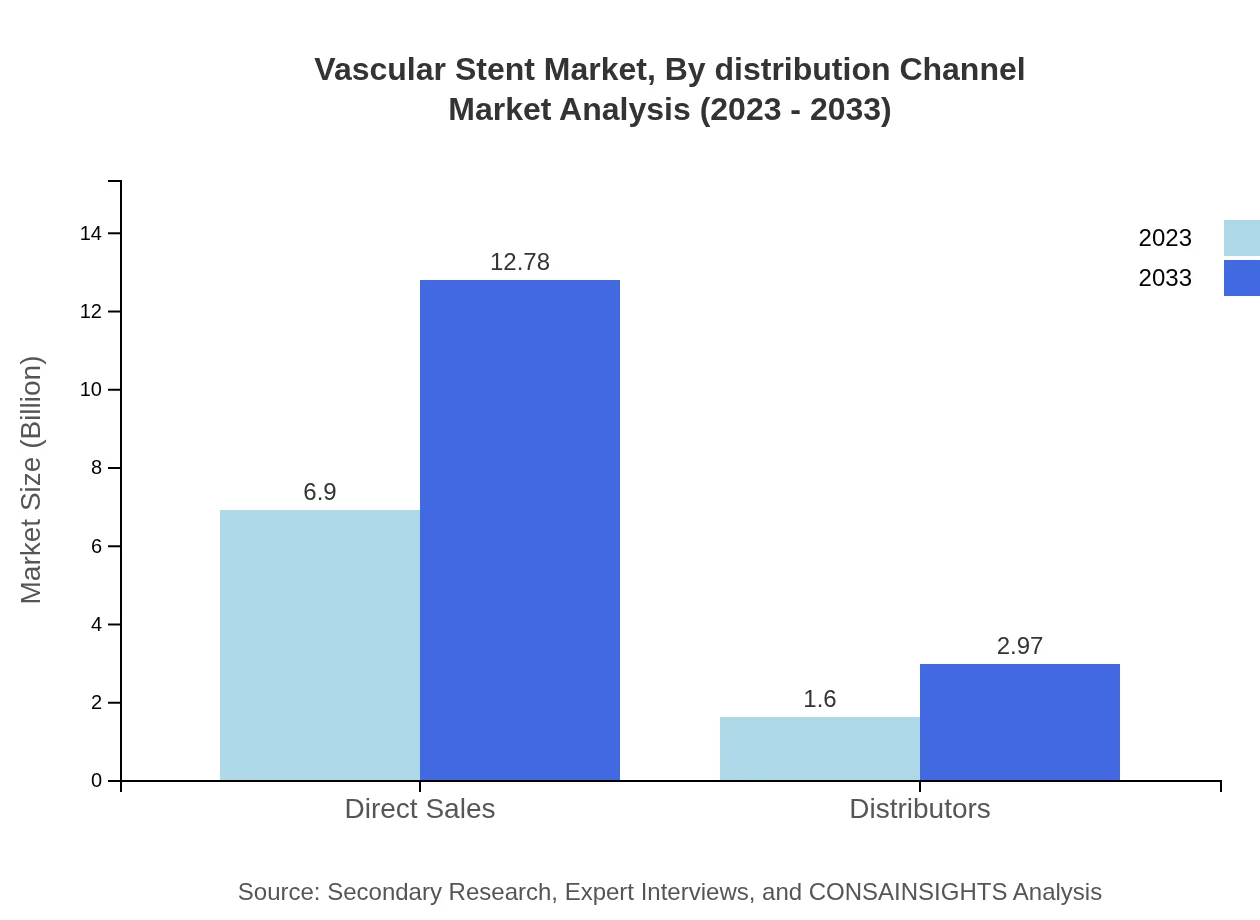

Vascular Stent Market Analysis By Distribution Channel

Direct sales dominate the distribution channel segment, holding an 81.16% market share in 2023 and projected to see consistent growth. Distributors capture the remaining 18.84%, reflecting the importance of both direct sales relationships and distributor networks within hospital procurement systems.

Vascular Stent Market Trends and Future Forecast

Tell us your focus area and get a customized research report.

Global Market Leaders and Top Companies in Vascular Stent Industry

Medtronic :

Medtronic is a leading global healthcare solutions company that develops and manufactures a broad range of innovative medical devices, including vascular stents, recognized for their quality and efficacy.Boston Scientific Corporation:

Boston Scientific Corporation is a prominent player in the vascular stent market, offering a range of innovative stent solutions that address the needs of patients and healthcare professionals across diverse cardiac and vascular conditions.Abbott Laboratories:

Abbott is a global leader in healthcare, providing advanced cardiovascular products including drug-eluting stents that help physicians improve catheterization outcomes and optimize patient care.B. Braun Melsungen AG:

B. Braun Melsungen AG focuses on the development of innovative vascular interventions, maintaining a commitment to safety, innovation, and meeting the needs of healthcare providers.We're grateful to work with incredible clients.

FAQs

What is the market size of vascular Stent?

The vascular stent market is projected to reach approximately $8.5 billion by 2033, growing at a CAGR of 6.2% from 2023. This growth reflects increasing demand for minimally invasive procedures and advancements in stent technology.

What are the key market players or companies in this vascular Stent industry?

Key players in the vascular stent market include major companies such as Medtronic, Boston Scientific, Abbott Laboratories, and Johnson & Johnson, which are known for their innovative solutions and extensive distribution networks.

What are the primary factors driving the growth in the vascular Stent industry?

Primary growth factors in the vascular-stent industry include rising cardiovascular diseases, increasing aging populations, advancements in stent technologies, and growing preference for minimally invasive procedures, facilitating better patient outcomes.

Which region is the fastest Growing in the vascular Stent?

The Asia Pacific region is anticipated to be the fastest growing in the vascular stent market, expected to increase from $1.61 billion in 2023 to $2.99 billion by 2033, driven by a surge in healthcare infrastructure developments.

Does ConsaInsights provide customized market report data for the vascular Stent industry?

Yes, ConsaInsights offers customized market report data tailored to specific needs in the vascular stent industry, allowing clients to gain detailed insights pertinent to targeted market segments and regional developments.

What deliverables can I expect from this vascular Stent market research project?

Deliverables from the vascular-stent market research project include comprehensive reports detailing market size, trends, competitive analysis, regional insights, and forecasts, along with tailored insights to meet specific client objectives.

What are the market trends of vascular Stent?

Current trends in the vascular stent market include increasing adoption of drug-eluting stents, technological advancements in implant design, a shift towards biodegradable materials, and a growing focus on patient-centric approaches in stent application.